Apex Group announced that it has been appointed by Participant Capital Advisors to provide fund and financial services.

As the affiliated asset management arm of Royal Palm Companies, Participant Capital allows wealth managers and their clients to invest in real estate opportunities that have traditionally only been available to institutions via a suite of investment vehicles.

Apex Group will provide fund administration services to Participant Capital’s Luxembourg domiciled funds. Fund administration is at the core of Apex Group’s single-source solution, delivering timely, accurate and independent services, underpinned by market leading technology platforms. According to a recent Total Economic Impact (TEI) report by Forrester Consulting, clients of Apex Group’s single-source solution achieve, on average, cost benefits of $5.39m, with a net present value of $2.75m over a three-year period.

These services will be provided by Apex Group’s growing Miami office, which offers the Group’s full single-source solution to asset managers, financial institutions, private clients and family offices, with a focus on the delivery of services to clients in the Miami, Florida and Latin American markets. This mandate is expected to be expanded in due course to provide additional depositary and digital banking services via Apex Group subsidiary EDB.

Alex Contreras, SVP Business Development at Apex Group comments: “As the Miami Real Estate market continues to go from strength to strength, we are excited to announce our appointment by Participant Capital, who we look forward to supporting through our integrated approach to fund and financial services. Our single-source solutions, underpinned by our experienced team, will enable Participant Capital to streamline their operational processes, and allow them to continue to focus on accelerating the growth of their business and continue to deliver attractive returns for investors.”

Felix Haydar, Operations Director, Participant Capital further adds: “We have chosen to partner with Apex Group at a critical time in our growth trajectory, as we look to expand our real estate fund offerings to a wider range of investors. In selecting Apex Group, we found a partner that offered scalable fund administration services and the ability to access additional cross-border financial services in one convenient relationship. The Miami team has been responsible and shown a depth of experience in servicing our private equity real estate vehicles.”

MFS Investment Management is announcing the opening of a new office in Montevideo, Uruguay. The office is located in the Zonamerica free trade zone area, and will be home to the sales and support staff serving the Southern Cone region.

“Expansion into Uruguay reaffirms our longstanding strategic commitment to Latin America overall and the Southern Cone region where we have been building long standing relationships for nearly three decades. We are proud to bring MFS’ nearly 100 years of investment experience and expertise to Uruguay. We believe this new office will allow us to continue creating value for our clients responsibly for many years to come,” said L. José Corena, managing director for the Americas for MFS.

The Free Trade Zone offers a favorable business environment, a growing local investor base and a strategic location from which MFS can more effectively serve the Southern Cone region moving forward.

“From our new base in Montevideo, we are well placed to deepen existing relationships as well as grow new relationships throughout the Southern Cone. As the appetite for investing continues to grow across Latin America, MFS will leverage its presence in Uruguay to enhance its clients’ experience throughout the region,” said Stephan von Hartenstein, a senior regional consultant who will be based out of the new office.

Originally founded in Boston, Massachusetts, in 1924, MFS has been serving the Americas for more than 35 years. The new office will allow MFS to continue to serve its many longstanding relationships throughout the region, including Argentina, where it has some of its deepest and long lasting distribution relationships. Furthermore, the office will complement the firm’s Miami, Florida and Santiago, Chile offices serving the Americas, in addition to coordinating with sales teams in the firm’s Boston headquarters and London office.

“For more than three decades, we have offered our actively managed equity, fixed income and multi asset strategies in the region to meet the demand of a growing investor base. We are extremely pleased to have a new central location from which to engage distribution partners and advisors going forward,” said Ignacio Duranona, senior regional consultant, who will partner with von Hartenstein in the new office.

MFS manages more than $529 billion globally for individuals and institutions. Within the Americas and across major global markets, the firm offers the MFS Meridian® Funds, a line of 36 equity, bond and multi asset funds, in addition to institutional separate accounts and other investment vehicles globally, according the firm information.

Dynasty Financial Partners announced that the firm has named Bob Shea to a new role as Chief Investment Strategist and has also taken a new ownership stake in FCF Advisors. FCF Advisors is a boutique Asset Management firm and Index provider based in NY, specializing in free cash flow focused research and investment strategies.

In this role, Mr. Shea will lead Dynasty’s Investment Committee, provide top-down asset allocation insights and guidance and lead investment manager selection. In addition, he will construct and maintain Dynasty’s Outsourced Chief Investment Officer (OCIO) portfolios, be responsible for asset manager relationships, and participate on the investment committees of the firm’s clients.

He will report to Ed Swenson, Chief Operating Officer of Dynasty.

Dynasty’s Investment Platform reported $32.6 Billion in Assets Under Advisement (AUA) as of the end of Q2, 2022, according the firm information.

“Bob’s analytical skills and deep experience in the investment arena make him a great fit for this new role,” said Mr. Swenson. “We are thrilled to have Bob on the team and look forward to supporting him as he builds out the Investment Group’s capabilities to catalyze growth in our advisory businesses.”

Mr. Shea joins Dynasty from investment firm FCF Advisors where he was the CEO and CIO. He began his career at Goldman Sachs where he worked from 1991-2004 and where he served as Partner, Co-Head of Cash Equity Trading.

As part of the announcement Dynasty is also taking an ownership stake in FCF advisors.

Independent advisors can tap the Dynasty Investment Platform specifically for research, or to completely outsource all or part of their investment management funds through the firm’s OCIO program. The group’s analysts focus on a wide range of asset classes, including equities, fixed income/capital markets and alternative investments, the company said.

Mr. Shea joins Dynasty as the firm is preparing to host its annual Investors Forum for independent advisors in early December. The conference is one of the largest investment forums in the industry for RIAs. This year’s conference will take place in Houston, TX from December 5th– 7th. Mr. Shea will be a featured speaker along with other executives from leading investment firms.

Will you remember that unlike 2020 and 2021, when S&P 500 investors were rewarded with returns of 18.4% and 28.7%, 2022 was the year you got out of the market altogether? Or will you remember in the face of 2022’s challenges—which included rampant inflation, rising interest rates, horrific natural disasters, the persistent threat of COVID-19, and the ongoing war in Ukraine—you ignored the investment market and focused on your hobbies?

Will you remember that because of poor performance, you abandoned the stock and bond investment mix you’d maintained for years? Or will you remember that, aside from year-end portfolio rebalancing, your holdings remained relatively unchanged?

For many years, institutions and individuals have come to rely upon a long-term portfolio mix that has served them well. Developed by Nobel Laureate Harry Markowitz in 1952, and comprised of 60% stocks and 40% bonds, for many years the portfolio has rewarded investors with attractive investment returns earned by assuming low levels of risk.

From 1980 through July 2022, the 60/40 portfolio delivered positive returns in 35 of 42 years. Investors who have relied upon this investment mix have seen their portfolios increase in value 83% of the time. As any statistician will tell you, the positive long-term performance of the 60/40 portfolio is “statistically significant”, not the result of chance or luck. With an average annual rate of return of 9.89% for the 30 years ending in 2021, 60/40 investors have been rewarded for staying the course. But this year, the strategy has performed poorly and is down 19.34% through October 5, 2022.

Despite the 60/40 portfolio’s positive long-term returns, this year’s poor performance has prompted investment experts to point investors in the direction of “alternatives” such as private equity, infrastructure, long/short strategies, and real estate. In addition to being asset types that are inaccessible to many investors, alternative managers also employ investment techniques such as using leverage or hedging that have the potential to either amplify gains or losses.

While alternatives do serve a purpose in diversified investment portfolios, they are not necessarily the best investment for everyday investors, because alternatives:

Are often more appropriate for large, institutional-type investment portfolios. While a small allocation to alternatives may make sense for typical investors, allocating a significant percentage of a portfolio to non-traditional investments makes sense for investors whose portfolios are valued at $1 million or more. Often, these investors are looking for negatively correlated investments that don’t rise and fall in tandem with stocks and/or those that may provide alternative streams of income. During years like 2022, when both the stock and bond markets have performed poorly, alternative investment positions have the potential to temper investment volatility.

Possess characteristics that everyday investors dislike. For many years, individual investors have grown to appreciate the transparency, regulatory oversight, liquidity, and manageable fees that characterize traditional investments. The same can’t be said for alternatives. In many cases, they are complex, unregulated, illiquid, and costly in terms of fees.

Are most beneficial when added to portfolios in anticipation of market downturns. Instead of adding alternative investments during market downturns, investors should add them to their portfolios when traditional investments are performing well and alternatives are out of favor.

Making significant investment portfolio changes during a bear market is never a good idea. Instead, successful investing is an endeavor that requires investors to muster incredible short-term patience to achieve their long-term financial goals.

Financial advisor Jim Martin and a team of four professionals launched a new multi-family office and investment firm called Nordwand Capital in Radnor, PA with a presence in New York, NY and Boston, MA.

Nordwand Capital is a multi-family office and investment firm serving select families with whom the team has worked for many years. With approximately $5 billion in client assets, “the firm cultivates a prudent long-term investment philosophy that prioritizes performance across asset classes”, the release said. Nordwand is focused on generational continuity, philanthropy, and service as core tenets of investing and client service.

In addition to being a Registered Investment Advisor, the firm has established Nordwand Investments, LLC as an independent entity designed to facilitate co-investment opportunities with some of the world’s most sophisticated investors in a fully aligned manner and with favorable economic structures.

Nordwand Investments will be the GP of several listed and private investment funds and opportunistic Special Purpose Vehicles and has received in excess of $250 million in seed capital for its first three funds from its founding family partners.

“We needed to meet the needs of 21st-century ultra-wealthy clients. which requires creativity and flexibility,” said Mr. Martin. “In response, we launched Nordwand Capital as a fully independent firm that is nimble and responsive enough to seize investment opportunities as they arise. Our new firm offers flexibility, speed, and creative structuring, giving our clients more attractive investment options.”

“It’s clear the team made this decision because it’s in the best interest of their clients,” said Shirl Penney, CEO of Dynasty Financial Partners. “This is one of the largest fully independent firms launching in 2022 and it shows the continuation of the trend of the most successful financial advisors and investment professionals moving toward full independence. We are delighted to welcome Jim and the whole Nordwand team to the Dynasty Network.”

Nordwand Capital has selected Fidelity Brokerage Services LLC as its custodian. Fidelity Institutional® (FI) provides clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC, Members NYSE, SIPC. Fidelity Family Office Services is a division of Fidelity Brokerage Services LLC.

Jim Martin joins Nordwand Capital as Chief Executive Officer and Chief Investment Officer. He was most recently a Managing Director at Morgan Stanley Private Wealth Management, which he joined in 2016 from Credit Suisse’s private-banking division. He has been recognized nationally by Barron’s as a Top 100 Advisor in 2021 and 2022*. Earlier, Jim was a founding member of Donaldson, Lufkin & Jenrette’s Philadelphia office. Mr. Martin maintains his Series 7 and 66 certifications. He received a B.S. in Finance from St. Joseph’s University.

Joining Jim Martin are the following professionals: Christopher Boyle,Chief Operating Officer, Theodore W. Brooks, CFA, Head of Listed Strategies, Connor Martin, Senior Associate, Daniel Kane, Senior Associate.

As volatile as U.S. stock and bond markets have been this year, emerging markets (EM) have had it worse. EM stocks are currently in one of their longest bear markets, with the MSCI Emerging Markets Index down about 40% from its February 2021 peak.

The cause of this poor performance has a lot to do with China and its regulatory crackdowns on its global technology franchises, restrictions on debt restructuring among homebuilders and zero-COVID policy, which has produced rolling lockdowns and interrupted economic momentum.

Together, these have produced disappointing growth. And because China is a major trading partner to virtually all other EM regions, and accounts for one-third of the market capitalization in most EM benchmark indices, its fate weighs heavily on investor willingness to allocate to EM.

Global inflation in oil and food prices and the strong U.S. dollar have further dragged on the markets. The strong dollar raises the cost of dollar-denominated debt and imports for emerging markets.

Together, these challenges have led global investors to slash EM positions and shun the asset class, driving historically cheap valuations. The MSCI EM Index now trades at about 10 times forward earnings estimates, and the MSCI China Index about eight times.

This is in marked contrast to the S&P 500 Index, which still boasts a forward price-to-earnings ratio of 17 and is over-owned by investors globally.

Three Potential Catalysts for a Rebound

A more pro-growth, stimulus-oriented stance in China: Morgan Stanley economists believe China will begin prioritizing economic development over some of its goals related to security and social stability, which have been front and center for the past two years. We also see a possible end to China’s zero-COVID policy by the new fiscal year in April 2023. A full re-opening could allow private consumption to rebound substantially and boost China’s inflation-adjusted GDP growth from below 3% to 4.5% in 2023. Importantly, as China pursued a very different policy response to COVID from most of the West, it is not experiencing high inflation or rising interest rates. This gives Beijing significant runway for stimulus.

A peak in the strength of the U.S. dollar: We may see the dollar losing momentum as the Federal Reserve’s rate-hiking cycle matures and as relative economic growth outside of the U.S. improves. As the dollar potentially weakens, EM countries could benefit from the relative appreciation of their own currency. Additionally, commodity exporters, such as countries in Latin America, could see commodity prices strengthening due to greater global demand.

Shifting global trade relationships: While U.S.-China relations remain complicated, the reorganization of strategic supply chains could create new opportunities for EM nations other than China. In areas such as consumer and industrial goods, we anticipate new relationships between the U.S. and India, Latin America and non-China-linked countries in Southeast Asia. Meanwhile, we also expect China to continue to court economic integration with some of those same countries, extending efforts first nurtured through its Belt and Road infrastructure program.

All in, we think it may be time for investors to reassess their exposure to emerging markets. Investors should consider rebalancing EM exposure with an eye toward China onshore companies, as well as opportunities in South Korea, Taiwan and Brazil.

UBS launched a new offering, in collaboration with Addepar and Mirador, that will provide UBS’s ultra high net worth clientsin the US with a consolidated, real-time view of their entire portfolio across assets and liabilities, including traditional, non-traditional and illiquid assets.

UBS’s financial advisors will now have access to comprehensive analytics, which will help them more effectively visualize their clients’ investment performance, cash flows, and worth, while assessing the opportunities and risks across their portfolios.

“We recognize that our advisors need an intuitive, visual and modern offering that will provide a complete picture of their clients’ full portfolio – from stocks and bonds to alternative investments and their private art collections,” said John Mathews, Head of Private Wealth Management at UBS. “With this unique offering, our clients will have the ability to gain a deeper understanding of their wealth – guided by their financial advisor – to help them make more informed decisions to meet their financial goals.”

Built with open architecture, Addepar integrates the leading-edge software, data and service partners from across the fintech industry. Addepar’s data, analysis and reporting capabilities will help UBS’s advisors consolidate clients’ performance calculations presented in an easily accessible graphic interface to unlock additional insights on returns and investment trends.

“Our partnership redefines what’s possible for advisors and their clients and truly empowers data-driven investment decisions in a timely, complete and secure way,” said Eric Poirier, CEO, Addepar. “Working with UBS, it’s clear that they recognize the importance of having the best technology, data and solutions to meet their clients’ needs – now and in the future.”

As part of the Addepar partner ecosystem, Mirador’s financial data technology experts will support UBS’s advisors with data management, custom visualization and tailored reporting, as well as operations and system maintenance.

“We are thrilled to have UBS as our first enterprise-wide client,” said Jeremy Langlois, Chief Revenue Officer, Mirador. “We look forward to working with the firm’s advisors to provide tailored solutions to help their clients understand their needs and unique ownership, family and legal entity structures to achieve their financial goals.”

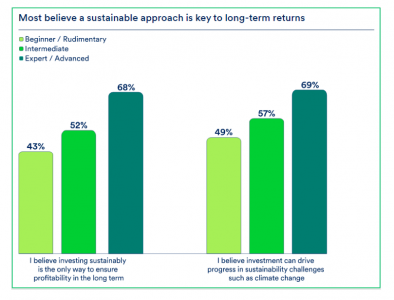

“Expert” investors are more likely to believe that investing sustainably is key to driving long-term returns compared with people who rate themselves as less knowledgeable, Schroders Global Investor Study 2022 has found.

The sustainability-focused findings of Schroders’ flagship study, which has surveyed more than 23,000 people who invest from 33 locations globally, found that more than two-thirds (68%) of people who class themselves as having “expert/advanced” investment knowledge believe sustainable investment is the only way to ensure profitability in the long term.

This compares with 52% of ‘”intermediate” investors and 43% of those who believe they have ‘”beginner/rudimentary” investment knowledge. Similarly, 69% of “expert” investors share the view that investing sustainably can support positive change when it comes to challenges such as climate change.

Hannah Simons, Head of Sustainability Strategy at Schroders, commented: “The interaction between sustainability and returns has seen some polarising results this year. While beginner investors appear more sceptical, the majority of people believe sustainability is crucial to delivering long-term returns. This is encouraging to see and further emphasises the crucial role asset managers have to play in terms of helping investors better understand how investing sustainably can not only help overcome challenges such as climate change, but also support their long-term returns. Indeed, we see an intrinsic link between long-term sustainable investment returns and solving some of the world’s social and environmental challenges.”

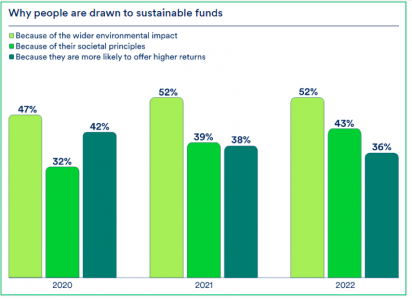

Specifically, the study found that environmental impact was the main reason people are attracted to sustainable investing. However, investing according to social issues has grown in importance compared with previous years. Interestingly, financial gains only ranked third in investors’ list of priorities, having declined over the past two years, falling from 42% in 2020 to 36% this year.

However, a focus on delivering financial returns unsurprisingly still remains a priority for many investors. More than half (56%) seek a fund that focuses primarily on delivering financial returns while integrating sustainability factors. That is particularly the case for people in Asia (61%) and the Americas (60%), while people in Europe were more likely to choose a fund with sustainability characteristics (51%).

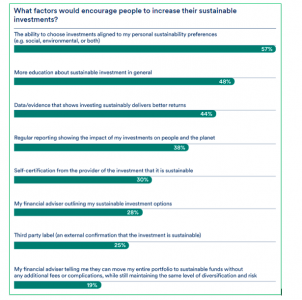

The study also found that people would increasingly invest in sustainable funds if they were able to invest in line with their preferences. More than half of investors across all self-defined expertise levels said that the ability to choose investments that align with their personal sustainability preferences would encourage them to increase their allocation to sustainable investments.

In terms of investors’ specific sustainability goals, quality education was seen as the most important globally, with a fifth of those surveyed (21%) ranking this option first.

Education and evidence of better performance and impact also key factors to encourage sustainable investment

Countries with higher poverty levels appeared to prioritise addressing poverty over other factors. In India, eliminating poverty was the top priority (having been selected by 21% of investors). In contrast, investors in Switzerland selected educational improvements as the priority.

As well as the ability to choose investments aligned to their personal sustainability preferences, just under half (48%) said that more education around sustainable investing would encourage them to allocate more sustainably. The lack of clear definitions of sustainable investments was cited as one of the most significant barriers to investing sustainably by all knowledge levels.

Completing the top three, some 44% of people stated that more data and evidence showing that investing sustainably delivers better returns would encourage them to increase their investments.

Andy Howard, Global Head of Sustainable Investment at Schroders, said: “This year’s survey results show that environmental challenges remain one of the key reasons individuals are looking to invest sustainably. However, the ‘S’ in ‘ESG’ can’t be forgotten, with human capital, education and equality all top of people’s investment priorities. Financial education is a key element in driving more capital towards sustainable investing. It is clear from our research that what people seek is essentially guidance and clarity. The more people are able to understand the products they invest in and their impact on society and the environment, the more capital we should see flowing into sustainable investing.”

Insigneo and iCapital announced a partnership to provide Insigneo’s US and Latin American financial advisors and their clients with access to iCapital’s private market and hedge fund offerings.

“We recognize the growing importance of alternative investments, especially in today’s market environment,” said Insigneo Chairman and CEO Raul Henriquez. “To that end, Insigneo is proud to partner with iCapital, which enables us to leverage their technological capabilities to provide Insigneo’s clients with easy access to a premiere lineup of alternative investing opportunities.”

Added Mirko Joldzic, Insigneo’s Head of Investment Solutions: “We are excited that our global client base will greatly benefit from iCapital’s technology and solutions while accessing a broad range of private market opportunities within private equity, private debt, and real assets, in addition to a variety of hedge fund strategies.”

iCapital and Insigneo both recognize a growing demand for private market and hedge fund investments in Latam.

“We are pleased to announce our partnership with Insigneo, a distinguished wealth management firm with a primary focus on Latin America, and support them in our shared mission to make institutional-quality private market and hedge fund allocations more accessible to financial advisors and their clients,” says Marco Bizzozero, Head of International at iCapital. “Latin America is of strategic importance to iCapital, and we are delighted to grow our business in the region with such an experienced partner.”

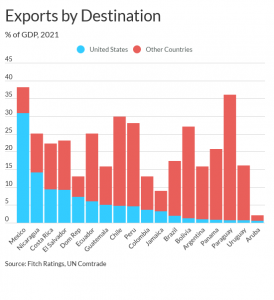

Latin America (LatAm) and the Caribbean are the most susceptible regions to a US recession, Fitch Ratings says in a new report. This reflects LatAm and the Caribbean’s geographical proximity and various transmission channels, which tie them to US economic cycles and policy decisions.

Fitch cut its US 2023 growth forecast to 0.5% in its most recent Global Economic Outlook published September 2022; it forecasts a mild US recession beginning in 2Q23.

The main transmission channels into LatAm and the Caribbean are trade, remittances, tourism and commodity prices. Within these regions, the countries’ different economic characteristics mean the impact could vary considerably.

Lower US external demand primarily affects Mexico due to its export-dependence and geographical proximity (Mexico is among the US’s top three trading partners).

A large portion of Central American exports are demanded by the US, although these countries tend to have a more diverse export markets base.

South American economies have limited trade links with the US, but are indirectly affected via the impact on global trade and commodity prices.

Weakening US household incomes and employment could imperil migrants’ capacity to send remittances home, and discourage tourism.

Remittances account for more than 20% of GDP for some Central American countries. Caribbean and Central American economies are vulnerable to a sudden stop in tourist arrivals, particularly Aruba (the world’s most tourist-dependent country as a share of GDP).

A US recession, in tandem with Fed tightening, adds to challenges for frontier markets, as costlier external financing could complicate policy options, and for the region’s more developed economies if their current account deficits are large.

We expect limited pressure on LatAm and Caribbean’s sovereign ratings from a mild US recession. Any ratings impact will ultimately depend on the magnitude of the US economic shock and each country’s capacity to absorb it.

‘Latin America and the Caribbean’s Vulnerabilities to a US Recession’ is available at www.fitchratings.com or by clicking on the link above.