As high inflation and lower expected investment returns continue to challenge institutional asset owners, many indicate a desire to increase their allocations to alternative investments, according to Cerulli’s latest report, North America Institutional Markets 2022: Shifting Allocations Amid Market Uncertainty.

Among alternative investment allocations, asset owners plan to allocate to infrastructure (28%) and real estate investments (26%), given their ability to hedge against inflation in the next 24 months.

Asset owners also indicate an increase to private equity (20%), private debt (20%), and hedge funds (18%) to bolster returns.

“Institutional investors are operating in a significantly different market environment in 2022 than they had been over the last several years as a result of persistent inflation. Many institutions are evaluating investment options that help prevent decreases in assets or funded statuses,” remarks Chris Swansey, senior analyst.

In addition to shifting allocations, the research points to an increase in consultant intermediation among institutional mandates—35% of institutional investors plan to increase their use of an investment consultant in the next 24 months. “Many plans are looking for guidance in navigating a turbulent market as inflation, rising interest rates, and lower capital market expectations translate to falling asset values and higher future liabilities,” adds Swansey.

Public defined benefit (DB) plans lead all institutional investor channels in the proportion of investors that expect to begin using an investment consultant (33%).

When hiring an asset manager for alternative asset class mandates, specialization in a specific asset class (96%), strong performance (94%), and competitive fees (92%) are important factors, according to the research.

Looking forward, Cerulli believes that managers are likely to see increased pressure on fees—almost all institutional asset owners (94%) negotiate management fees and a majority are doing so on a mandate-by-mandate basis during the sales process.

“It is clear that most institutional asset owners are looking for discounts on management fees below the stated fee schedule. Lower market returns will likely increase pressure on management fees, and asset managers that can keep fees competitive and meet investors’ needs for performance and specialization will win out,” states Swansey.

To view the full report, please click on the following link

Investors Trust and QB Partners have entered into a strategic partnership that will help with tax, trust, estate, pension, domicile, cross border and other holistic planning issues.

This partnership aims to provide professional advisers with practical, accessible and solutions-driven technical support, the press release said.

David White, Managing Director of QB Partners said: “QB Partners has grown the consultancy side of its business significantly in recent years . Our technical consultants are all from life assurance backgrounds and have a combined experience of over 200 years in this sector, so we are a great fit for life assurance companies who wish to outsource their technical support. QB Partners are completely independent and in addition to providing support to several life assurance companies, we also work with investment platforms, pension and trust providers as well as directly supporting financial advisers, so we have a genuinely 360 degree view of the cross border market.”

By joining forces, “both companies are able to combine their years of experience and expertise to collaborate and bring High Net Worth clients the best financial advice while providing advisers independent support allowing them to deliver top quality service and products”, the memo adds.

“All of this means that Investors Trust and QB partners can provide our advisory network with all the support they need for HNW client issues and consolidates ITAs leading position and continues our commitment to grow the business further in the next 20 years,” said Ariel Amigo, Chief Marketing Ocer and Distribution Ocer at Investors Trust.

Investors Trust and QB Partners are thrilled to work together in order to enhance the clients and advisers experience, the companies pronounced.

“It is their success and years of experience that have characterized QB Partners in the field over the past 13 years”, the memo concluded.

The AML Act and the CTA substantially changed and modernized the U.S. Bank Secrecy Act (BSA) and related AML laws and regulations. However, because many of the new statutory provisions will require rule makings, reports, analyses, and other measures, its full impact remains to be seen and may be slowly realized over the next few years, says a report distributed by the Financial & International Business Association (FIBA).

The Final Rule, which takes effect Jan. 1, 2024, “is a significant step in the implementation of this enhanced BSA/AML regulatory framework”, FIBA said.

With the Final Rule, the United States now joins at least 30 other countries that have implemented some form of central register of beneficial ownership information. Entities that may qualify as reporting companies under the Final Rule should prepare their stakeholders.

FIBA highlights several points in its press release that are extensively detailedin the guide sponsored by GreenbergTraurig.

For example, Final Rule requires U.S. entities and foreign entities registered to conduct business in the U.S. to report beneficial ownership information to FinCEN unless they meet an enumerated exception.

The Association explains that beneficial owners include each individual who, directly or indirectly, either exercises substantial control over a reporting company, or owns or controls at least 25% of the ownership interests of a reporting company.

Moreover, individuals who create a reporting entity also are required to report personal identifying information to FinCEN.

The Securities and Exchange Commission (SEC) announced charges against eight individuals in a $100 million securities fraud scheme in which they used the social media platforms Twitter and Discord to manipulate exchange-traded stocks.

According to the SEC, since at least January 2020, seven of the defendants, Perry Matlock, Edward Constantin, Thomas Cooperman, Gary Deel, Mitchell Hennessey, Stefan Hrvatin and John Rybarcyzk, promoted themselves as successful traders and cultivated hundreds of thousands of followers on Twitter and in stock trading chatrooms on Discord.

These seven defendants allegedly purchased certain stocks and then encouraged their substantial social media following to buy those selected stocks by posting price targets or indicating they were buying, holding, or adding to their stock positions. However, as the complaint alleges, when share prices and/or trading volumes rose in the promoted securities, the individuals regularly sold their shares without ever having disclosed their plans to dump the securities while they were promoting them.

“As our complaint states, the defendants used social media to amass a large following of novice investors and then took advantage of their followers by repeatedly feeding them a steady diet of misinformation, which resulted in fraudulent profits of approximately $100 million,” said Joseph Sansone, Chief of the SEC Enforcement Division’s Market Abuse Unit. ”

The complaint further charges Daniel Knight, of Texas, with aiding and abetting the alleged scheme by, among other things, co-hosting a podcast in which he promoted many of the other individuals as expert traders and provided them with a forum for their manipulative statements. Knight also traded in concert with the other defendants and regularly generated profits from the manipulation.

The SEC’s complaint, filed in the U.S. District Court for the Southern District of Texas, seeks permanent injunctions, disgorgement, prejudgment interest, and civil penalties against each defendant, as well as a penny stock bar against Hrvatin. Criminal charges against all eight individuals also were filed in a parallel action brought by the Department of Justice’s Fraud Section and the U.S. Attorney’s Office for the Southern District of Texas.

The SEC’s investigation, which is ongoing, is being handled by Andrew Palid, David Scheffler, and Michele T. Perillo of the Market Abuse Unit (MAU) in the Boston Regional Office, with assistance from Darren Boerner of the MAU, Stuart Jackson, Kathryn Schumann-foster, and Marina Martynova of the Division of Risk and Economic Analysis (DERA) and Howard Kaplan of the Office of Investigative and Market Analytics.

The investigation resulted from a referral from the Division of Examinations by Mark A. Gera, John Kachmor, Nitish Bahadur, and Raymond Tan in the Boston Regional Office. The litigation will be led by David D’Addio and Amy Burkart of the Boston Regional Office.

The SEC appreciates the assistance of the Criminal Fraud Section of the U.S. Department of Justice, the United States Attorney’s Office for the Southern District of Texas, the Federal Bureau of Investigation, and the Financial Industry Regulatory Authority.

Rebeca Patterson, Chief Investment Strategist at Bridgewater Associates.

Bridgewater Associates is losing its Chief Investment Strategist, Rebecca Patterson, who has decided to resign from her position and leave the company. As she herself has explained, in a post published on her LinkedIn, her decision will be effective at the end of the year.

“After three years of working with incredibly talented, dedicated, and caring colleagues during unprecedented times for the global economy and markets, I have decided to explore my next chapter at the end of this year. Bridgewater Associates was an incredible experience for me, and I am so appreciative of the mentorship I’ve received and the connections I have built. After 25-plus years of researching and investing, I’ve come to realize that my strengths and passion as an investor are best aligned with more discretionary, less systematic approaches,” Patterson said.

She took the time to thank for the opportunity “to have helped build on Bridgewater’s already unparalleled research, including through our Daily Observations, to publicly share our insights with the world, and to engage with clients to shape investment solutions that address their goals”.

In addition, Patterson acknowledged the leadership of Nir Bar, Greg Jensen and Bob Prince and thanked them for their friendship.

“This has been challenging in the best possible ways – a period of personal and professional growth that I am so thankful for. And of course, I will always be grateful to Ray Dalio for convincing me to come to Bridgewater and truly challenge my thinking as an investor”, she concluded.

Patterson joined Bridgewater, the world’s largest hedge fund ($150 billion in assets), in 2020 as chief investment strategist. In addition, as a member of several of the firm’s business committees, including its executive committee, Patterson helped lead the firm’s diversity and inclusion efforts. Prior to Bridgewater, Patterson oversaw $85 billion in assets as chief investment officer at Bessemer Trust, and, prior to that, she spent her career at JP Morgan, where she spent 15 years as an analyst in the firm’s European, Singapore and U.S. offices.

Despite the challenges environmental, social, and governance (ESG) investing has faced in 2022, asset managers across Europe still regard ESG marketing as a key feature of their overall marketing efforts, as well as a powerful sales booster in the long term, according to the latest issue of The Cerulli Edge—Global Edition.

This year, the short-term credibility of ESG has been questioned in Europe, prompted by the recent high market volatility and heightened regulatory scrutiny.

However, despite these challenges, 49% of the asset managers across Europe that Cerulli surveyed consider ESG marketing a very important feature of their overall marketing efforts. Looking ahead to the next 12 to 24 months, 76% believe that the importance of ESG to their marketing efforts will grow.

“An average of 48% of the managers in the largest European fund markets believe that ESG capability is an important enabler of sales and 75% of respondents intend to focus on increasing their production of ESG marketing materials over the next 12 to 24 months,” says Fabrizio Zumbo, director, European asset and wealth management research at Cerulli.

Asset managers’ sales departments are thinking the same way: 51% of the sales executives view the need for a strong ESG proposition as a very important driver of change within sales teams, and 47% said ESG capability is a key topic they have discussed with clients this year.

When it comes to ESG-related themes, 41% of the asset managers plan to promote energy efficiency in their ESG-focused marketing efforts over the next 12 to 24 months. Another 39% will focus on climate change and carbon emissions.

Investors’ lack of financial awareness remains a challenge, particularly for asset managers targeting a retail audience. “Managers that can combine clear and tailored ESG-related communication with strong compliance and reporting features will stand out in the long term,” says Zumbo. “Managers targeting a retail audience should allocate more resources to providing financial education and marketing campaigns to increase investors’ awareness of topics such as the importance of the energy transition, reducing carbon emissions, and investing in line with the UN’s Sustainable Development Goals.”

On the other hand, for 75% of the asset managers in the U.S., the perception that ESG is politically motivated is a moderate challenge to increasing client receptiveness to ESG issues, up from 49% in 2021. To overcome investor skepticism, managers should discuss the merits of ESG and sustainable investing with their clients, highlighting how and why they are using ESG data to drive long-term economic value.

In addition, Asian portfolios are, to some extent, more focused on regional assets and their respective local securities. This focus has sheltered Asian portfolios from the Russia-Ukraine war. Some 88% of the Asian asset owners Cerulli surveyed feel market movements caused by the war are either limited or have short-term return implications that are recoverable. More than half (58%) of respondents said the war has not had much impact on their ESG portfolios.

The property market is beginning to react to the Fed’s tightening cycle. It is no surprise that quickly rising interest rates, stubbornly high inflation, and fears of a looming recession are changing the risk-reward calculation for many real estate investors in both public and private markets.

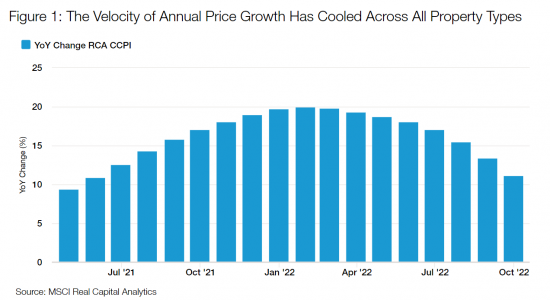

After more than three decades of a low inflation environment, the U.S economy is experiencing broad-based inflation at rates not seen in many years. As a result, the Federal Reserve has raised rates five consecutive times over the past year. For example, as seen in Figure 1, while most real estate indices are still showing double-digit gains over the past year, the overall pace of growth across major U.S commercial properties has already decelerated. Taking a closer look at the table below, the RCA CCPI (Real Capital Analytics commercial real estate prices) National All-Property Index rose 11.1% over the past year, which is a slower pace than that of the record growth seen in January 2022, prior to the Fed’s aggressive rate hikes. We anticipate valuations will continue to contract, potentially creating an opportunity for investors to buy at more attractive prices.

Despite shifts in the market driven by the upward pressure on interest rates and rising inflation, we believe that certain segments of the real estate market feature attractive long-term fundamentals. This is especially true for property types that can benefit from inelastic demand, shorter lease terms, and pricing power that can keep up with inflation. With the right properties, real estate can be an important ally to investors’ portfolios amid evolving macro conditions.

Sizing up Opportunities and Risks

The broad category of real estate includes various sub-asset classes. Commercial real estate, in particular, includes buildings that can generate rental income for investors and are generally spread across four main sectors — multifamily (or apartment buildings), office, industrial, and retail. It also includes more specialized sectors such as hotels, data centers, self-storage, senior housing, student housing, and life-sciences.

Choppier waters ahead will call for a more nuanced approach to distinguishing properties within these sectors that will be better equipped to handle a softer economy and a potentially prolonged inflationary environment. Given the macroeconomic conditions ahead, we favor real estate assets that possess strong long-term fundamentals with attractive valuations, as well as characteristics such as strong pricing power and durable cashflows to better combat inflation.

More specifically, our team prefers properties that have shorter lease terms to ensure that rent escalations can keep up with — or not fall too far behind — near- to mid-term inflation levels. For example, multifamily apartments offer a 12-month term lease structure. Additionally, a portion of tenants turn over each month to allow for frequent opportunities for landlords to reset rents to track inflation. Other worthwhile opportunities to consider include niche areas such as self-storage and hospitality, where rents are charged on a monthly or even nightly basis. However, both asset classes could be affected by a slowing economy. Industrial properties are another area where we see attractive opportunities. Although industrial real estate assets do not generally feature short-term leases, they continue to enjoy strong long-term fundamentals due to secular shifts.

On the flip side, certain segments of the retail sector feature higher levels of risk due to secular trends, although pockets of opportunity do exist. During the pandemic, consumer preferences continued to shift toward the convenience of online shopping versus at brick-and-mortar stores. Although this has since reversed, we anticipate a continued bifurcation of performance within the retail sector, with retail asset type and location driving performance. Moving forward, we see merchants continuing to increase their online presence, while adopting a multichannel strategy to capture sales.

The office sector also presents unique risks. Generally, office buildings tend to have relatively long lease terms (e.g., 5-10 years) which creates inflationary risk for investors compared to multifamily units. In addition, remote and hybrid work have accelerated the need to redesign office spaces with a focus on collaboration and amenities. Thus, we are seeing a significant bifurcation between high-end, newly-developed office buildings — those with state-of-the-art amenities intended to attract workers back in the office — versus older offices that haven’t made such capital improvements. Similar to retail, a “winner take all” pattern may be emerging as currently 15% of office buildings contain roughly 80% of office vacancy nationally, according to Cushman and Wakefield.[1] All things considered, the office sector contains many risks, with limited pockets of value.

We believe having a strong research process that looks across siloes, including public and private markets, will be critical in identifying idiosyncratic risks and uncovering opportunities across all real estate asset classes

Putting it all Together

While macroeconomic conditions will always continue to evolve and present challenges, we believe uncertain times can also create opportunities if managers know where to look for them. As discussed, real estate as an asset class still possesses many attractive characteristics even in a higher rate and inflationary environment, especially in areas where strong rental pricing power exists, lease terms are shorter, and secular trends provide a catalyst for growth. We find that both multifamily and industrial properties hold some of these key advantages compared to other real estate sectors.

Looking ahead, we believe real estate market volatility will persist and market conditions will remain challenging due to the continued transition toward a higher cost of capital environment. This could bring near-term pains, but also long-term opportunities to real estate investors. During this period of heightened complexity, we believe constructing a balanced real estate portfolio that focuses on properties with attractive valuations that can deliver dependable cash flows will be crucial in mitigating the risks associated with the transition toward a lower economic growth and higher rate environment.

Morningstar announced the launch of Morningstar Research Portal (Research Portal), an investment research platform for financial advisors.

Research Portal harnesses Morningstar’s independent ratings and research, together with live market data and interactive charting, in an intuitive web-based platform, empowering advisors to bring personalized and timely investment ideas to their clients.

“Clients are looking for more from their advisors as their investment choices increase and the trend toward personalization continues. Research Portal interconnects Morningstar’s research with powerful new tools that enable advisors to swiftly identify investments that meet their clients’ needs, communicate those recommendations, and then monitor their investments continuously in a seamless way,” said Marc DeMoss, head of Morningstar research products.

“Morningstar’s research and ratings are expanding in line with the evolving motivations of today’s investor, and Research Portal helps advisors drive more timely and relevant client conversations.”

Research Portal makes the investment insights across Morningstar’s full analyst and quantitative coverage universe – more than 140,000 stocks, 320,000 mutual funds, and 24,000 ETFs – easily accessible to advisors via a modern, fast interface.

The platform’s workflows – such as the Watchlist, Model Portfolios, Pick Lists, and Compare functions – help a user discover and evaluate investment ideas under chosen criteria. Research Portal then keeps users up-to-date on the investments they care about with a dashboard that tracks global market activity and a Calendar feature that displays upcoming events, all of which can be customized for specific universes of investments.

The suite of tools within Research Portal closely connects advisors to Morningstar research so they can personalize their conversations with clients. For example, with Pick Lists, an advisor could reference the Europe Core list when seeking ideas for European exposure. The enhanced screener also has multiple configurable views that make it quick to broadly search for a security across custom filters.

In addition to data analysis, Research Portal can also be used thematically. The Morningstar Insights tab surfaces the latest editorial content from Morningstar thought leaders, grouped by topics like sustainability, policy impact, and retirement. Analyst notes, security and sustainability reports, and more are also available within the platform, the firm said.

Research Portal is available now to individual advisors and on an enterprise level. It is also integrated within Morningstar Advisor Workstation, replacing Morningstar Analyst Research Center, and within Morningstar Direct, replacing its now-retired Research Portal widget.

Apex Group a global financial services provider announces the growth of its Miami office.

Apex Group now employs over 1,300 experts in the Americas region, across a network of over 25 offices. Apex Group’s Miami presence, located in the prestigious Brickell financial district, employs an experienced team of experts, led by Jay Maher, Senior Advisor and former CEO, Americas at Mainstream Group who joins following the business’ successful acquisition by Apex Group. Maher is supported by senior executives including David Ries, Head of Private Equity Solutions and Alex Contreras, SVP, Business Development.

Apex Group in Miami provides the Group’s full single-source solution to asset managers, financial institutions, private clients and family offices, with a focus on the delivery of services to clients in the Miami, Florida and Latin American markets.

The expansion of Apex Group’s Miami presence follows a period of record new business growth for Apex Group’s Americas region with recent client wins including Participant Capital, Compass Group LLC, a leading independent Latin American asset manager and Florida-based Midtown Capital Partners LLC.

This announcement builds on Apex Group’s strategic growth plan for the Americas, including the acquisitions of events and technology platform Context365, real estate services provider SandsPoint Capital Advisors, tax services firm FTS, Canada-based fund services provider Prometa, as well as the additions in Latin America of BRL Trust Investimentos, Brazil’s leading independent fund administrator and acquisition of MAF, the fund administration business of the Brazil-based Banco Modal.

Georges Archibald, Chief Innovation Officer and Regional Managing Director, Americasat Apex Group comments: “Our clients across the Americas come to us to provide scalable support to bolster the efficiency of their in-house teams. We view the South-East of the US and the Latin American markets as a strategic growth priority and presenting a compelling opportunity for us – and for many of our international client base. The continued growth of our Miami office enables us to better deliver our global experience and outlook to support our clients locally in these regions.”

Jay Maher, Senior Advisor, Apex Group adds: “We are delighted to continue to expand our Americas’ footprint in Miami so that Apex Group further strengthens its position as the global provider of choice for corporates and fund managers, wherever they may be located. Local delivery of our single-source solution partnered with Apex Group’s truly global reach will enable us to help our clients to scale more quickly and efficiently, to fuel their continued growth and success.”

U.S. Bancorp announced that it has completed the acquisition of MUFG Union Bank’s core regional banking franchise from Mitsubishi UFJ Financial Group, Inc.

The transaction brings together two premier organizations to serve customers and communities across California, Washington, and Oregon and support a dedicated workforce across the West Coast. Customers will benefit from an expanded branch network, greater access to digital banking tools, and increased choice, the memo said.

“The acquisition of MUFG Union Bank underscores U.S. Bank’s commitment to creating economic opportunities for our customers and communities across the West Coast,” said Andy Cecere, chairman, president and chief executive officer of U.S. Bancorp. “The closing of this acquisition brings together two premier organizations and their teams who are focused on putting customers first.”

U.S. Bank will provide MUFG Union Bank customers with information regarding the conversion of their accounts in the coming weeks. Until conversion of MUFG Union Bank systems and accounts, customers will continue to be served by their respective branches, website and mobile apps. Systems integration and account conversion is expected to occur in the first half of 2023.

Additionally, once customer conversion has occurred, implementation of U.S. Bank’s five-year, $100 billion community benefits plan will begin.