Trident Trust announces the extension of its offering for US-based alternative investment managers, with the opening of a fund services representative office in Houston, Texas.

The new location follows our strategy of putting our people where its clients need them, providing a local point of contact for both our existing clients and the wider funds community in the state, the firm said.

Chelsea Harrington, Senior Manager in its fund accounting team, has relocated to Houston from our 130-strong fund services hub in Atlanta to open the new office.

“Our presence in Texas means that we now offer fund services out of four US locations, with representative offices already in place in New York and Miami”, the statement added.

UBS Wealth Management USA announced that Financial Advisors Brian Mariash and James Barton “Bart” Lowther have joined the firm in Sarasota, Florida. Together with their six-person team, Mariash Lowther Wealth Management, they manage nearly $640 million in client assets for ultra-high net worth individuals and families.

“On behalf of UBS, we’re excited to welcome Brian, Bart and their entire team to the firm,” said Greg Kadet, Managing Director and Florida Market Director at UBS Wealth Management USA. “The team’s experience, dedication to clients, and passion for philanthropy are a great addition to our business as we look to continue to expand and enhance our ability to serve clients in this growing market.”

“As partners for over 10 years, Brian and Bart have a deep commitment to helping clients and their families navigate complex financial matters,” said Karmen Keup, Southwest Florida Market Director at UBS Wealth Management USA. “With our unique suite of capabilities at UBS, I have no doubt the team will continue to successfully deliver for clients in the years to come.”

Brian Mariash joins UBS from Merrill Wealth Management, where he spent the past 15 years working as a Financial Advisor. He joined the financial services industry in 2001, after a career in music education. Brian brings an learning-based approach to wealth management, and his personal mission to educate, connect and contribute has become part of the mission of the team he founded, Mariash Lowther Wealth Management. His practice focuses on advising ultra-high net worth retirees, C-suite executives and small business owners.

Brian holds the Certified Investment Management Analyst® designation (CIMA®), administered by the Investments & Wealth Institute™ (The Institute) at The Wharton School of Business, and the Accredited Asset Management Specialist™, AAMS™® designation from The College for Financial Planning Institutes Corp. As an active member and supporter of his local community, Brian previously served on the board of the Child Protection Center of Sarasota as well as the board for Jewish Family and Children Services. He is the proud father of three children and resides in downtown Sarasota.

Bart Lowther began his financial services career at Merrill Wealth Management in 2010. Through his practice, he focuses on helping clients manage and preserve their wealth through various, complex market cycles based on their individual needs. Together with his team, Bart focuses on delivering a comprehensive approach to managing wealth that begins with listening to a client’s unique financial needs to help ensure each strategy is grounded in an understanding of what each client wants to achieve. He also specializes in providing clients with investment planning advice for retirement.

Bart received his finance degree from the A.B. Freeman School of Business at Tulane University in 2010. He holds the Certified Financial Planner (CFP®) certification as well as the Chartered Retirement Planning Counselor (CRPC®) designation from the College for Financial Planning. Bart is passionate about giving back to his local community, and serves on the boards of The Circus Arts Conservatory and All Faith’s Food Bank. A Sarasota native, Bart enjoys playing music, going to the beach, and spending time with his dogs, Layla and Beaux.

Brian and Bart are joined by Financial Advisor Jesse Perez, CFP®, as well as Client Associates Shannon Murphy, Dionysios Skaliotis and Sovanna Sok.

US Republicans, supported by a few Democrats, pushed back against a rule that would make it easier for fund managers to consider sustainability in investment decisions. The debate shows including climate considerations in investing remains controversial. But we believe sustainability continues to gain traction and is becoming a key to investment success.

US President Joe Biden is expected to veto a Republican bill aimed at preventing pension fund managers from basing investment decisions on factors like climate change. The bill, which gained Senate approval on Wednesday after two Democrats joined Republicans, illustrates the potential for partisan divisions to impede the sustainability agenda.

Backers of the resolution say that the primary criterion has to be the financial return on investment, and that it would not stop funds from considering ESG issues altogether. The White House, however, has said President Biden will veto the measure.

The conflict highlights that considering the ESG performance of companies in investment decisions remains politically contentious. But we believe sustainability is becoming an increasingly important guide for investors.

Sustainability is a helpful guide to corporate performance for investors. Multiple studies have shown that companies that manage sustainability issues better tend to perform better. We also believe that firms that manage their business, stakeholders, and environmental impact better should be well-positioned to deliver on financial results. Research has also shown strong investment returns associated with the successful engagement of ESG issues. The annualized returns for MSCI ACWI ESG Leaders outperformed global equities (MSCI ACWI) both on a five-year and 10-year basis.

SI offers a diverse opportunity set. Certain parts of the sustainability investment universe underperformed last year as investors exited growth-oriented sectors in favor of value. But we think the volatility among growth companies says more about the importance of portfolio diversification than the SI approach itself. For example, we see numerous value-oriented opportunities in food supply chains, waste management, and recycling. In addition, ESG improver equities (Rockefeller Improvers ESG Index) have outperformed the Bloomberg US 3000 Total Return Index by two percentage points a year over the past five years.

Resilient fund flows to sustainable strategies underscore the commitment of investors. According to Morningstar, sustainable fund flows were more resilient throughout 2022 than broad market flows. This was especially evident in the fourth quarter, when global sustainable fund assets increased 11.6% quarter-over-quarter, almost double the growth of the broader market. Notably, “dark green” funds (those with sustainable investment as their key objective) in Europe saw uninterrupted inflows throughout the entire year, suggesting consistent investor commitment.

With strong capital commitments from governments and businesses alike, we continue to believe that sustainability should be a key long-term driver of investment returns. We recommend investors diversify across sectors, styles, and asset classes, and also see opportunities in themes including the circular economy, clean air and carbon reduction, smart mobility, and energy efficiency.

ZEDRA announces the opening of a new office in South Dakota, expanding the trust services provided to both international and domestic US clients.

ZEDRA’s new office will strengthen the firm’s presence in the Americas and promote its proven active wealth expertise in the US private wealth space. The new office, led by its Managing Director, Jon Olson, will offer a full set of trust administration services tailored to international clients, spanning from high-net-worth-individuals, families, entrepreneurs as well as their relevant advisors.

The office opening follows a number of recent acquisitions in the Americas, including US and Curaçao-based, Atlas Fund Services, now rebranded to ZEDRA Funds, which provides long-term, tailored, and reliable alternative investment fund services to US-based investment managers. ZEDRA also acquired US Global Expansion Specialist, Axelia Partners, in 2022, now rebranded to ZEDRA Global Expansion Services US, which facilitates the expansion in the US of predominantly European headquartered businesses and entrepreneurs.

Commenting on the office opening, Ivo Hemelraad, CEO at ZEDRA, said: “We have been working with private clients for decades, providing that all-important strategic oversight of a nuanced big-picture. “The expansion of ZEDRA’s trust services in the US supports our reputation as an international leader for trust services and is a natural next step in bolstering the firm’s global offering for private clients, cementing the business opportunities of our Miami office across North and Latin America.”

Jon Olson, Managing Director of ZEDRA in South Dakota, said: “We are excited about the endless possibilities that the new office represents, both for the firm and our clients.

“As ZEDRA has established itself as a strong and trusted partner in Europe and Asia in the trust services business, we look forward to repeating our successes in the Americas by offering all the advantages of South Dakota trust laws to our clients.”

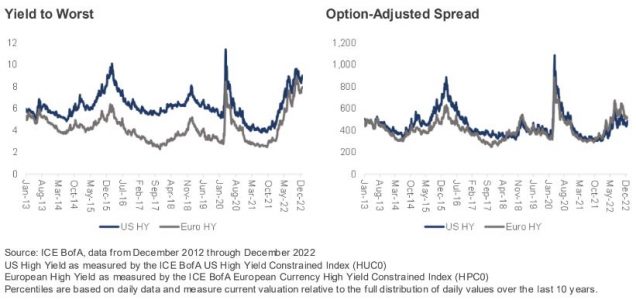

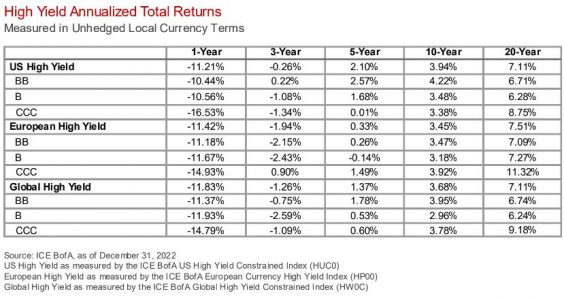

High yield slumped alongside other asset classes in 2022, with the ICE BofA US High Yield Constrained Index declining -11.21%. Yields increased a hefty 4.7% on the year, rising to 9.0%. Only 37% of the increase in yield was

driven by spread widening, as the market’s option-adjusted spread (OAS) increased a relatively modest 172 bps to a spread of 483 bps.

“Looking forward, we view valuations as very attractive on a yield basis – both US and European high yield are in the cheapest yield decile over the last 10 years. Despite the slowing economy, we are constructive on high yield, forecasting 10-12% returns for the full year 2023. Our spirited outlook is based on the asset class’ relatively healthy fundamentals, highly supportive market technicals, and the attractive yields on offer that help to compensate for the risks of investing in high yield”, reports Nomura Corporate Research and Asset Management INC (NCRAM) in the “High Yield Outlook”.

Mixed Macroeconomic Backdrop

2022 was a year to remember for both risk assets and rates investors, as neither equities nor fixed income provided any respite from the relentless bear market. The S&P 500 declined -18.1%, and the 10-year US Treasury lost -16.3%. Other developed and emerging markets witnessed similarly distressed outcomes for their domestic 60/40 portfolios. Commodities lost their effectiveness as a hedge after an early -2022 rally. WTI crude gained 4.2% on the year, falling -35.1% from its zenith in March.

The year began with the US Fed tacitly acknowledging that surging inflation would not be “transitory.” The Fed and many other global central banks spent 2022 aggressively withdrawing the liquidity they had pumped into their economies during the pandemic. One notable anecdote is the decline in US M2 money supply growth from a shock-and-awe level of 26.8% y/y during the pandemic to 0% annual growth in November 2022, the slowest pace since at least 1959. Market sentiment subsequently shifted from fretting about inflation to worrying about a pending recession. Russia’s invasion of Ukraine added to investors’ consternation in 2022, particularly in Europe, driving up commodity prices and further snarling supply chains.

As the year progressed the global economy softened, sapping demand for commodities and providing firms with breathing room to catch up on backorders and otherwise normalize supply chains, enabling inflation to retreat from peak readings.

As the calendar turns to 2023, says NCRAM, investors remain concerned that the Fed may channel the King of Pop, Michael Jackson, and his “Don’t Stop ‘til You Get Enough” refrain, driving the US economy into recession as a side effect of its efforts to contain inflation.

NCRAM is somewhat more sanguine about the economic outlook. “While we forecast a shallow recession in 2023, we also expect the Fed to pause rate hikes in 1Q23, and the economy to begin its recovery in the second half of the year in anticipation of easier monetary conditions”. According to the outlook, the Fed could begin easing before year-end if inflation and growth continue to react to the 425 bps of tightening plus early stage QT that the Fed implemented in 2022. Markets are unlikely wait for the economic recovery to take hold before rallying, creating a more favorable environment for investing in 2023.

Supportive High Yield Fundamentals

Despite the slowing economy, high yield fundamentals remain relatively sound. US high yield issuers ’ 3Q EBITDA declined -6% sequentially, but rose 17% y/y. High yield companies continue to generate cash flow and are using those resources to prepare for a weaker economy. Leverage in the US high yield market has declined from 5.2x during the pandemic to 3.1x to start 2023.

“The default rate over the last 12 months has held steady at less than 1%. We expect a small increase in defaults as the economy slips into a shallow recession, but given the low leverage carried by high yield issuers and the absence of a market sector under significant stress (e.g. energy in 2015-16 or housing during the financial crisis), we expect the default rate to remain below the 3.2% long-term average. Another reason we are confident that defaults will remain under control is the improvement in credit quality in the US high yield market in recent years. Historically, the high yield market has seen as low as 35% BB-rated bonds, and coming out of the financial crisis, nearly 25% of the market was rated CCC and below.”

Today the market is more than 50% BB, and only about 10% CCC. High quality issuers are generally better positioned to withstand a recession.

Muscular Market Technicals

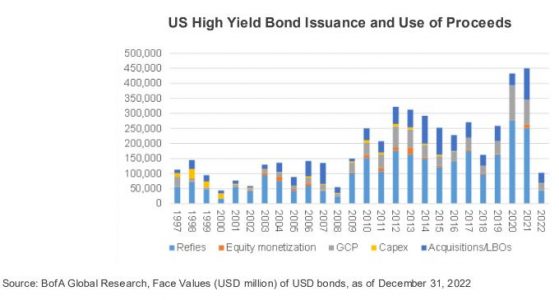

High yield technicals are very robust, according to NCRAM’s outlook. The US high yield market shrank by nearly $200 billion of market cap in 2022. Calls, tenders, and maturities totaled close to $200 billion for the year. More than $100 billion of high yield bonds were upgraded to investment grade, countered by less than $10 billion of investment grade that was downgraded to high yield. This means that close to $300 billion left the high yield market in 2022 vs. just over $100 billion of new high yield issuance. The nearly $200 billion decline in high yield

bonds outstanding (excluding secondary market buybacks by high yield issuers) is more than 10% of total US high yield market cap (market size is just shy of $1.5 trillion).

“We expect the rising star trend to continue in 2023, as large issuers such as Occidental Petroleum and

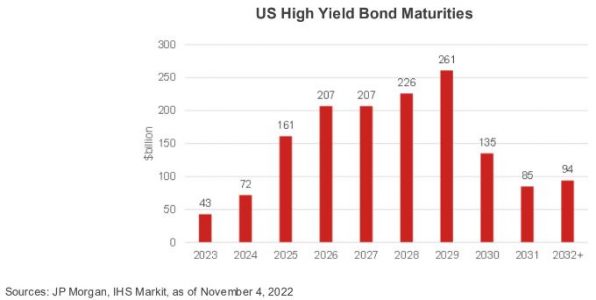

Ford could potentially ascend to investment grade. High yield issuers were able to avoid tapping the market in adverse conditions in 2022, because much of the debt stock that would have come due last year was refinanced in the heavy issuance years of 2020-21. There are few high yield bonds maturing before 2025, and approximately 80% of high yield issuers have no bond maturities in the next 2 years, another reason we are confident that defaults will avoid a spike in 2023.”

Attractive Entry Point

The yield to worst for both US and European high yield is quite generous relative to recent history, even if US high yield is not overly cheap on a spread basis. “We believe the yields on offer, along with the previously described fundamental and technical backdrop, support our forecast of 10-12% high yield returns in 2023”, says NCRAM.

JP Morgan Research calculates that over the last 37 years, when investors have put money to work in US high yield with yields of 8-9%, the median 12-month forward return was 11.4%. Given the improved credit quality profile of the market, one would expect investors to demand a lower risk premium to hold high yield.

Thus, NCRAM estimates that US spreads look more attractive relative to history on a quality-adjusted basis. Also note that average high yield bond prices in both the US and Europe are trading close to their deepest discounts in

the last decade, improving the risk-reward ratio for an asset that (if all goes well) matures at par.

NCRAM’s total return forecast assumes the US will lapse into a mild recession, but the high yield market will be able to ride out the slowdown. “Even if our growth forecast is too optimistic and the recession is more painful than expected, rapidly declining US Treasury yields would counter-balance high yield spread widening. With carry around 9%, we believe high yield will generate positive returns even if the depth of the recession surprises to the negative side”, concludes the NCRAM’s outlook.

Photo courtesyFernando Pérez Castillo, Carolina Thompson and Ximena Guevara

Insigneo announced the affiliation of Ximena Guevara and Carolina Thompson, along with their Client Associate, Fernando Perez Castillo.

The 20-year industry veterans, who both join Insigneo as Senior Vice President, together have over $120M in assets under management, producing close to $1M in annual revenues, according to company information.

The team will be based at the firm’s Miami headquarters.

Jose Salazar, Insigneo’s US Market Head said, “Insigneo is thrilled to have Carolina, Ximena, and Fernando join our team of outstanding financial advisors. We look forward to working together with them and helping them grow their wealth-management business.”

The duo met at Citibank Private Bank Miami in the early 2000s, and later went to UBS Financial Services in Coral Gables, where they worked for almost a decade. They worked with Morgan Stanley for the past three years. Both are Series 7 and 66 licensed, and cover markets including Mexico, Ecuador, Colombia, Venezuela, and Argentina. Their business mix primarily consists of brokerage with some advisory, investing in traditional products along with lending and banking products. Perez Castillo, who joined the team at Morgan Stanley, where he worked for five years, is also Series 7 and 66 licensed.

“We are excited to be part of Insigneo’s best-in-class, flexible platform catering to international and domestic high-net-worth clients. We share with Insigneo the same passion to work side-by-side with our clients to help them achieve their financial objectives,” Ximena and Carolina added.

For many business families, sustaining prosperity for the long run depends on how well they plan for transfers of business assets and family wealth from one generation to the next, according to the KPMG Private Enterprise Global Family Business Tax Monitor. The report advises business families with footprints in multiple jurisdictions to monitor potential new or increased taxes and consider taking action in advance.

The report has been a go-to source for family business tax planning for almost a decade, comparing the vastly different tax liabilities among jurisdictions on the transfer of family business through gifting during the owners’ lifetime (including on retirement) and through inheritance.

Among the 57 jurisdictions covered in the report, some have geared their tax policies in ways that recognize how a thriving family business sector contributes to a vibrant economy. Others give no special tax exemptions for intergenerational family business transfers, increasing tax costs and likely reducing the family’s ability to compete with business families in more tax-friendly jurisdictions.

“Location can make a world of difference! Tax-efficient transfers between generations can leave wealth in the hands of entrepreneurial families to invest in profit-producing activities — and that can help stimulate job creation and innovation for future generations,” says Tom McGuiness, Global Leader, Family Business, KPMG Private Enterprise, KPMG International

KPMG Private Enterprise’s report found that globally, South Korea, France, the US and the UK impose the highest tax rates for transfer of a family business valued at EUR10 million by inheritance, before any tax breaks are accounted for. After exemptions, South Africa takes the biggest bite from family business inheritances valued at EUR10 million, followed by Canada and Japan. For inheritances of family businesses over EUR100 million, the most expensive taxing jurisdiction is South Korea after exemptions, with South Africa and the US coming in second and third.

For transfers during the owner’s lifetime (gifts) of family businesses valued at EUR10 million, Venezuela imposes the highest taxes globally before exemptions, followed by Spain, South Korea and France. After exemptions, South Africa and Japan come second and third behind Venezuela as the jurisdictions imposing the highest tax costs on business transfers by gift. These comparisons are similar for family businesses valued at EUR100 million before and after exemptions.

Top priorities for today’s business families

The report also provides insights on what business families consider their biggest priorities and risks and calls attention to three emerging trends — branching out, building up and giving back. The trends cruciallyreveal an increase in business families and their assets becoming more global, a rise in the importance of governance and a renewed focus on the management of family wealth and the notion of giving back with philanthropic activities commanding more time.

“Amid rising geopolitical tension and unparalleled economic uncertainty, the leading business families that we work with are diversifying globally and putting more focus on the sustainability of their businesses, their wealth and their communities,” says Tom McGuiness, Global Leader, Family Business, KPMG Private Enterprise, KPMG International. “By doing so, they can position their families for sustainable success down the generations. As a result, we are seeing more business families around the world that are focused on branching out, building up and giving back.”

To download the full report, please click on the following link.

Photo courtesyJosé Luis Jiménez, Mapfre Chief Investment Officer

Mapfre AM has acquired a further 26% equity stake in French ESG specialist mutual fund boutique La Financière Responsable (LFR), taking its total holding to 51% as it targets growth of SRI derived strategies and seeks to boost its international footprint into the French fund market.

The Group previously acquired 25% of LFR in 2017 to adopt its proprietary ESG-focused stock selection process, which aligns with Mapfre AM’s strategic approach to responsible investment and economic, social and environmental (ESG) commitments. At the time, this was the first transaction involving a Spanish asset management company buying into a foreign firm in the industry.

The deal secured MAPFRE AM access to an exclusive strategy and methodology for selecting investments and applying ESG criteria to new products, as well as to the rest of the Group’s range of funds and balance sheet.

Business upsides flowing from that initial stake and the positive ongoing relationship between MAPFRE AM and LFR has led to growing the stake.

José Luis Jiménez, Mapfre Chief Investment Officer, commented: “Since 2017, we have been committed to sustainable investment, and LFR has nearly 25 years of such experience in this industry. In the past five years, we have jointly launched SRI products, which have the peculiarity of having their own methodology for the final selection of the securities that make up the funds’ portfolios, something that is highly appreciated by our clients.”

An example of synergies seen at the product level is the Mapfre AM Inclusión Responsable fund, which has been cited by the United Nations Global Compact as an example of best practice. The fund’s portfolio encompasses those companies most committed to labour inclusion of people with disabilities.

Another is the Mapfre AM Capital Responsable fund. Qualified as an EU Sustainable Finance Disclosure Regulation (SFDR) Article 8 mutual fund and holding a ‘Label ISR’ from the labeling scheme supported by the French government, it recently was awarded a Five-Star rating from Quantalys, the independent fund data and analysis provider.

LFR, which has assets of nearly 650 million euros, will maintain operations with its customers and retain the brand.

Olivier Johanet, President of La Financière Responsable, commented: “Since 2017, the Mapfre and LFR teams have been working together in order to develop an excellent relationship and cooperation that benefits the clients of both companies. We very much welcome this closer relationship, which is a very important step in broadening the scope of our partnership.”

Mapfre AM is renewing its confidence in the current teams at LFR to continue to build its investment capacity and grow in the European market with institutional investors, IFAs and other asset managers.

Polen Capital announced the expansion of its Emerging Markets franchise, hiring LGM’s core Emerging Markets and China Equity investment teams. The agreement sees an additional six investment professionals joining Polen Capital, bringing the expanded franchise to now include six strategies and 10 investment professionals, based in London and Polen’s newly launched Hong Kong office.

The LGM teams, which were previously part of Columbia Threadneedle Investments, will enhance Polen’s capabilities and expertise in emerging markets and China as clients increasingly seek exposure to these markets. Polen will onboard and rebrand the team’s core emerging markets strategies and products including Emerging Markets Growth, China Growth and Emerging Markets Small Company Growth.

“Our expansion into Asia, and emerging markets overall, represents an attractive opportunity for Polen and our clients that will increase our exposure, people and capabilities in the fastest growing parts of the world,” said Stan Moss, CEO of Polen Capital. “The LGM team is aligned with Polen strategically and culturally, and mirrors our client-centric focus on long-term outcomes. Having a consistent, sustainable operating model and robust, centralized infrastructure will support the team’s ability to do what they do best.”

This expansion reunifies a historically effective team as several members of Polen’s Emerging Markets Growth team joined Polen from LGM. It also marks a meaningful expansion of its global research capabilities, now with on-the-ground professionals in Hong Kong, enhancing Polen’s ability to identify companies that can deliver sustainable, above-average earnings growth.

“We are excited our former LGM colleagues are joining us here at Polen. The team brings deep experience and a long track record building concentrated, quality growth portfolios in emerging markets, which aligns well with Polen’s focused investment philosophy,” said Damian Bird, Head of the Polen Emerging Markets Growth team. “Broadly speaking, most investors are vastly underexposed to emerging markets. We think their long-term economic growth potential will fuel attractive investment opportunities for the foreseeable future, and we are pleased to offer clients best-in-class emerging markets capabilities.”

San Francisco has this year secured the top spot in Schroders Global Cities Index, boosted by its world-leading venture capital industry. The Golden Gate City’s east coast counterpart, Boston, took second spot with London ranked third.

The elevation of San Francisco follows the introduction of a specific venture capital score to the Index. In short, the Innovation measurement, which previously assessed the strength of universities in a city, now also monitors the amount of venture funding directed to businesses in a specific location.

San Francisco as the heartland of technology innovation, and Boston, as a biomedical innovation centre, have seen their rankings improve as a result of this score being introduced.

Schroders’ Global Cities Index seeks to rank global cities across four key criteria: Economic, Environmental, Innovation and Transport. It also aims to identify the cities which combine economic dynamism with world-class universities, forward-thinking environmental policies and excellent transport infrastructure.

In addition to London’s top three ranking, the next best-placed UK city was Manchester in 28th.

Hugo Machin, Portfolio Manager, Schroders Global Cities, said:

“San Francisco’s rise to first place as well as the strong performance of a number of US West Coast cities such as Seattle and Los Angeles, may come as a surprise given the net migration towards the US’ ‘Sun Belt’ cities that has been widely reported. However, the introduction of a venture capital score has significantly boosted their positions.

“Today’s index shows that, despite the impact of the Pandemic and remote working, cities remain the economic drivers of the world economy. Their ability to provide collaborative spaces for work and deliver fantastic restaurants, theatre and retail experiences cannot be replicated online.

“In this context, cities will need to be armed with excellent transport links, affordable housing, green space and strong educational institutions to remain relevant. Furthermore, government policy will need to support the development of buildings that have excellent sustainability credentials.”

Risers and fallers

San Diego and Berlin were the only other two cities to have any meaningful movement in the top 30. Both scored well on venture capital funding and environmental policy.

Four Chinese Cities were also in the top 30, in spite of the well-documented lockdowns challenges. The index found that these cities’ strong Chinese universities and successful tech industries have sustained their rankings.

Indian and Indonesian cities also rose rapidly up the rankings. Cities such as Mumbai, Kuala Lumpur and Jakarta have benefited from an increased focus on technology and innovation, as well as highly-educated workforces.