Leslie Gillin Bohner, Chief Fiduciary Officer of Fiduciary Trust International

Fiduciary Trust International, a global wealth manager and wholly-owned subsidiary of Franklin Templeton, announces that Leslie Gillin Bohner has been named chief fiduciary officer.

In this newly created role, Bohner will oversee all trust operations and administration, and will continue to lead the firm’s Delaware business. She will also join the Executive Committee.

“Trust represents a significant portion of our clientele, and Leslie’s appointment is a testament to her many years managing complex fiduciary services,” said John M. Dowd, chief executive officer of Fiduciary Trust International.

“Leslie is an instrumental member of our team, and we are committed to growing our fiduciary business as we deliver services that meet our clients’ evolving needs,” he adds.

Bohner will continue to be based out of the organization’s Radnor, PA office and report to Dowd. She joined Fiduciary Trust International in May 2020 as a result of the company’s acquisition of The Pennsylvania Trust Company.

Prior to this appointment, Bohner served as chief fiduciary officer and general counsel for the Pennsylvania region. In these roles, she managed risk across all areas of the business, overseeing all legal and fiduciary matters, and providing guidance to a team of trust and tax professionals on fiduciary and wealth advisory matters.

“As chief fiduciary officer, I look forward to working with leaders across our organization to deliver the services that meet our clients’ needs,” said Bohner. “At Fiduciary Trust International, we understand our important responsibility in ensuring that our clients’ wishes are fulfilled and their legacy is preserved for generations to come. We feel privileged to have the opportunity to remain their trusted partner in this process.”

Bohner is admitted to practice law in Pennsylvania and is a member of the Probate and Trust Law Section of the Philadelphia Bar Association. She received her J.D. (summa cum laude), Certificate in Estate Planning, and LLM (Taxation) from Villanova University’s Charles Widger School of Law, and her B.A. in English from the University of Virginia.

All clients of the two Switzerland-based Vontobel US entities have been brought together under one roof within Vontobel SFA.

“Vontobel has thus become the largest Swiss-domiciled wealth manager for North American clients who are seeking international diversification for their assets and want them to be booked in Switzerland. The assets under management of the combined unit total around CHF 10 billion”, the statement said.

As a result of the legal merger, all clients of the “new” SEC-registered US entity will be able to access the comprehensive services and global investment expertise offered by Vontobel SFA.

Following the integration, Vontobel SFA has more than 100 employees in Zurich, Geneva, New York and Miami, including 30 client advisors and an expanded Investment Management & Advisory team with around 25 employees. In addition, UBS will continue to refer US clients seeking regional diversification to Vontobel SFA.

The CEO of the “new” Vontobel SFA is Peter Romanzina, with Jürgen Wegner serving as Deputy CEO. The Chairman of the Board of Directors of Vontobel SFA is Georg Schubiger, Head Wealth Management at Vontobel, and Jacqueline Hess is Vice

Chair of the Board of Directors of Vontobel SFA, as already announced at end-2022.

“We are very pleased that we can now offer all our North American clients our global investment expertise and investment

services from a single source. Vontobel has already been active in the US for around 40 years. Our numerous discussions with

clients have shown that they count on Vontobel and on our global expertise, which provides them with additional benefits,” said Peter Romanzina, CEO Vontobel SFA.

North America counts as one of Vontobel’s focus markets. At its last Investor Day, the investment firm emphasized that in the future, it will place an even stronger focus on large, established markets such as the US with substantial numbers of sophisticated clients whom Vontobel can help to realize their objectives – drawing on its global investment expertise.

“Building on this broader basis, we want to continue to successfully grow and to further consolidate our position as a leading

Swiss wealth manager for US clients, in line with our strategy. The legal merger is an important step on the way towards making

Vontobel SFA one of the partners of choice for discerning US clients who want to diversify their wealth globally,” added Georg Schubiger, Chairman of the Board of Directors of Vontobel SFA and Head Wealth Management at Vontobel.

Photo courtesySantander Private Banking team at the Euromoney Private Banking Awards ceremony

Santander Private Banking has been named the Best Private Bank in Latin America by Euromoney. Santander leads in several award categories, which are some of the most prestigious accolades in banking. The financial magazine also named Santander as Latin America’s Best Bank for Family Office Services and for Wealth Transfer/Succession Planning.

Santander has also been recognised for its teams’ work in several geographies including the awards of Best International Private Bank in Mexico, Argentina, Brazil, Peru, Uruguay, Poland, and Portugal; Best Private Bank for Ultra-High-Net-Worth Individuals in Spain and Colombia; Best Private Bank for Wealth Transfer/Succession Planning in Brazil; Best Private Bank for ESG in Chile; and Best Digital Private Bank in Mexico

“The breadth and distribution of these awards across Latin America & Europe demonstrates the value of the Santander Private Banking network combined with our local market expertise”, said the company in a press release.

Further to the announcement of 19 March 2023 regarding UBS’s acquisition of Credit Suisse, the Board of Directors of UBS have appointed Sergio P. Ermotti as Group Chief Executive Officer and President of the Group Executive Board, effective on 5 April 2023, after the Annual General Meeting.

He will succeed Ralph Hamers, who has agreed to step down to serve the interests of the new combination, the Swiss financial sector and the country. Ralph Hamers will remain at UBS and work alongside Sergio P. Ermotti as an advisor during a transition period to ensure a successful closure of the transaction and a smooth hand-over.

The Board took the decision in light of the new challenges and priorities facing UBS after the announcement of the acquisition.

Sergio P. Ermotti was the Group Chief Executive Officer of UBS for 9 years and successfully repositioned UBS following the severe challenges arising from the Global Financial Crisis. In particular, he built financial strength and improved resilience by putting the firm’s leading global wealth and asset management business, and Swiss universal bank, at its core. He swiftly transformed the investment bank by cutting its footprint and achieved a profound culture change within the bank which allowed it to regain the trust of clients and other stakeholders, while restoring people’s pride in working for UBS.

This unique experience, together with his deep understanding of the financial services industry in Switzerland and globally, make Sergio P. Ermotti ideally placed to pursue the integration of Credit Suisse. Sergio P. Ermotti is currently Chairman of Swiss Re. To facilitate an orderly transition at Swiss Re, Sergio P. Ermotti will stand for re-election at its AGM on 12 April 2023 and intends to step down after the AGM, following a short hand-over period.

Since assuming the role on 1 November 2020, Ralph Hamers, together with the Group Executive Board, has successfully managed UBS through a challenging market environment and has delivered record results in two successive years. He has encouraged a strong focus on clients and on shaping and executing our strategy, while ensuring tight cost management and strong risk discipline. He has driven the digital and sustainability agenda across the firm to make them important differentiators for our clients.

The financial performance and capital strengths of the group have allowed him to achieve record returns for shareholders through dividends and share repurchases, which has benefited the share price. Finally, Ralph was instrumental in delivering the acquisition of Credit Suisse under extreme circumstances, to the benefit of both banks and the stability of the Swiss financial system.

UBS Chairman Colm Kelleher said: “Ralph has been an outstanding CEO of UBS, driving the group to unprecedented success despite a challenging environment. Under his leadership UBS built the strengths that have put us in a position to stabilize Credit Suisse and ensure a successful integration. On behalf of the whole Board, I would like to express my deep respect and gratitude for all that Ralph has achieved over the last two-and-a-half years and for his instrumental role in delivering the Credit Suisse deal, as well as his understanding of the current situation and willingness to step down. While the acquisition will support UBS’s existing strategy, it imposes new priorities on us. With his unique experience, I am very confident that Sergio will deliver the successful integration that is so essential for both banks’ clients, employees and investors, and for Switzerland. I know Sergio will hit the ground running.”

Ralph Hamers said: “Integrating Credit Suisse is UBS’s single most important task and I am confident that Sergio will successfully guide the bank through this next phase. I am of course sorry to leave UBS, but circumstances have changed in ways that none of us expected. I am stepping aside in the interests of the new combined entity and its stakeholders, including Switzerland and its financial sector – it has been a pleasure and privilege to lead this great bank to where it is today. I would like to thank Colm and the Board for their support and guidance, and I wish Sergio every success. I will support him during a transition period and I know he will lead UBS very effectively in the interests of all.”

Sergio P. Ermotti said: “I am honored to be asked to lead this bank at a time that is so important for all its stakeholders and for Switzerland. I would like to express my gratitude to Ralph for steering UBS so successfully. The task at hand is an urgent and challenging one. In order to do it in a sustainable and successful way, and in the interest of all stakeholders involved, we need to thoughtfully and systematically assess all options. I am conscious of the uncertainty many feel and I promise that, together with my colleagues, our full attention will be on delivering the best possible outcome for our clients, our employees, our shareholders and the Swiss government.”

U.S. stocks were lower in February as the market’s repricing of the Federal Reserve’s rate-hike expectations gave back some of January’s gains. It was a year ago this month that the Fed announced its first rate hike since 2018 as it sought to lower inflation. Recent data suggests that the Fed has quelled some of the inflation surge, but the Fed’s credibility remains in question after initially dismissing inflation’s non-transitory warning signs.

Macroeconomic data has driven most of the market’s volatility for the past six months, and February was no different. The Fed is trying to thread a needle to execute a soft landing that beats inflation and avoids a recession. As investors wait for positive momentum, we see this macro-driven volatility as an opportunity. Mr. Market’s panic and euphoria around inflation prints often create greater discounts to intrinsic value, which is exactly what we are looking for.

Growth stocks have substantially outperformed value stocks to start 2023, and we believe this creates an opportunity for us Value Investors. The “January Effect”, in which laggards from the previous year outperform in the first few weeks of the new year, was especially pronounced to start the year. This price movement has had little to do with fundamental value, but rather is based on more short-term trading dynamics. Rising interest rates will put a premium on the near term cash flows, which we prize in our stock selection process. Inversely, this has pressured and will continue to pressure growth stocks that have longer dated cash flow expectations.

The Convertible market followed equities lower in February after a strong start to the year. Companies that reported earnings this month generally reported strong quarters with cautious outlooks for the year as they remain very focused on expense reduction and profitability over growth. With many convertibles trading more like fixed income than equity equivalent, this focus should benefit convertible holders.

Convertible issuance picked up in the month of February, with attractive terms. We expect companies to use convertibles when raising capital this year to manage interest expense and extend maturities in a covenant lite structure. We believe many companies have delayed coming to the market and converts offer an attractive way for companies to add relatively lowcost capital to their balance sheets. Continued issuance allows investors to stay current and by selectively layering new issues into their, they are able to maintain the asymmetrical risk profile we continue to believe in.

Despite a number of positive developments in the Merger Arb space, setbacks in several deals, plus the volatility in the markets and a return to “risk-off” trading, lead to wider spreads on a mark-to-market basis. In Standard General’s acquisition ofTegna, Inc., the FCC issued a surprise Hearing Designation Order (HDO) which could potentially extend the deal’s timeline beyond the merger agreement‘s termination date. More broadly, the recent elevated market volatility and uncertainty over the Federal Reserve’s trajectory resulted in wider spreads, thereby creating opportunities for us to earn greater absolute returns.

Although markets have gyrated and spreads have widened generally, there were reasons for optimism as a pair of deals that had become the subject of extended antitrust scrutiny won regulatory approval and closed in February. In addition, several notable deals closed including STORE Capital, which was acquired by a consortium led by GIC for $14 billion, KnowBe4Inc., which was acquired by Vista Equity Partners for $4 billion, and CinCor Pharma Inc., which was acquired by AstraZeneca for $1 billion.

Despite interest rate and market volatility, companies continued to announce new acquisitions in February and March. So far in March SeaGen (SGEN-$200.30-NASDAQ) agreed to be acquired by Pfizer for $41 billion in cash, Univar Solutions (UNVR-$34.68NYSE) agreed to be acquired by Apollo Funds for $8 billion in cash, and Qualtrics (XM-$17.65-NASDAQ) agreed to be acquired by a consortium led by Silver Lake Management for $10 billion.

Photo courtesyJosé Carlos González, Founder & CEO of FlexFunds

José Carlos González, Founder & CEO of FlexFunds, explains in an interview with Funds Society how FlexPortfolio, an ETP that offers access to the performance of an underlying portfolio managed by an investment advisor, works and what its advantages are over actively managed certificates (AMCs). González, co-founder and former head of Global X, a New York-based ETF provider, also outlines the client profile of this asset class and discusses which ones he considers most attractive in the current market environment.

What is the FlexPortfolio?

The FlexPortfolio is an ETP that offers access to the performance of an underlying portfolio managed by an investment advisor or portfolio manager, where the assets are liquid or listed. To make an analogy, the FlexPortfolio is similar to an ETF in the United States or an investment fund in Europe.

How do you coordinate creating and administering individualized ETPs while keeping management costs contained?

The process of setting up an ETP is a complex one, involving several service providers with different roles, but FlexFunds makes it simple for its clients. Each firm is involved in a specific area of ETP or FlexPortfolio creation and administration, and FlexFundscoordinates all of these service providers. Some of the most prominent are BNYM as issuing and paying agent, APEX, Intertrust as a trustee, and Interactive Brokers as one of the main custodians. We work with world-class service providers.

One of FlexFunds‘ main achievements over the years has been to “industrialize” this ETP issuance process to keep costs competitive for our clients through investments in state-of-the-art technology platforms and a great team of people. This makes the process efficient: we can issue a FlexPortfolio in half the time and at less than half the cost of any alternative investment vehicle.

What are the advantages of the FlexPortfolio over actively managed certificates (AMCs)?

The FlexPortfolio has aspects in common with actively managed certificates (AMCs). For example, both are funds that allow third-party management. One of the main differences is that AMCs are usually structured and issued by banks, mainly Swiss or European. In contrast, in the case of FlexFunds, the issuer is an Irish SPV (Special Purpose Vehicle), so the credit risk is more easily avoidable. This is especially relevant at certain times, such as the current one, with the recent episode with Credit Suisse.

Could you explain what your greater flexibility and the absence of restrictions on the rebalancing of the underlying account vs. AMCs consist of?

The flexibility of FlexFunds solutions is superior to that offered by an AMC. Let’s take as an example the FlexPortfolio with custody at Interactive Brokers. The portfolio manager has direct access to the trading account of this custodian. They control subscriptions and redemptions of the assets they deem appropriate, according to the investment strategy specified in the prospectus. The variety of products that can be securitized and operated is huge: stocks, bonds of many markets, indexes, futures, options, etc…

Regarding trading hours, our products can be traded practically 24 hours a day without being subject to European trading desk hours.

What does it mean that the FlexPortfolio is “Euroclearable”?

This is one of the fundamental features of the product, and it is also crucial. The fact that our solutions are “Euroclearable” means that financial intermediaries and broker-dealers can buy and sell the product on behalf of their clients. This is essential for investment advisors and clients who want consolidated statements of their positions.

Can I trade the portfolio 24 hours a day?

Yes, as long as the underlying market is open. The investment advisor is free to decide what to buy and what to sell.

Does the presence of leverage in the strategies increase risk?

Many of the strategies that our clients choose when launching ETPs are composed of long/short. In other words, the portfolio manager can be “long” in equities and take short positions. The purpose of many long/short strategies is to reduce volatility.

Our solutions allow our clients access to portfolio margin, providing leverage if the client desires.

For what type of client does FlexFunds recommend this type of product?

Our solutions and ETPs benefit investment advisors with a captive client base who want to repackage their own investment strategy for distribution. One of the advantages offered by the product is that it allows cost reduction through centralized account management and administration instead of separate accounts for each client.

It is also useful when the advisor wants to access private banking and broker-dealers. Our clients can do this through Euroclear and Clearstream.

Is there a particular underlying asset type (or types) that, in the current environment of volatility and uncertainty, is attractive for securitization? Why?

At FlexFunds, we have always had a lot of demand for structuring ETPs from real estate managers. Nowadays, real estate can be interesting because of its inflation hedging capacity, and by definition, it is a product with less volatility than equity markets. At FlexFunds, we are experiencing a lot of demand for repackaging real estate funds, REITs, etc…

For quite some time, our team has contended that goods inflation is indeed transitory. While a slowdown has taken longer than we originally thought, goods inflation is indeed falling. However, the Fed’s chicken-and-egg dynamic of inflation first before rate hikes has them playing catch-up quite aggressively. Other than the recent bank failures, the headline-grabbing data points over the past few months are mostly encouraging and now tell a story of retreating inflation. Although CPI slowed from 9.1% year-over-year in July to 6.4% year-over-year in January, the Fed still needs to keep its foot firmly on the brake.

Slowing inflation is just one part of the equation. While the Fed’s success may allow them to moderate the pace of interest rate hikes or eventually hold rates at a high level, Chairman Powell and the rest of the Fed must also work to restore credibility. In fact, Chairman Powell reiterated his message that inflation remains a way off from where they need to see it and there is more work to do, even as the Fed slowed its tightening pace in February.

Inflation peaked last year in July. Since then, we’ve experienced a slow and steady decline in the headline number. We’ve also seen services inflation taking an increasing share of the price pressures and goods inflation taking a decreasing share. As I have argued, this is important in terms of the Fed’s third mandate, which I believe will determine the timing of the central bank’s pivot. If services inflation remains above two percent, though lower than where we see today, and goods inflation keeps shrinking, the Fed may tolerate core inflation above 2%. Given that services inflation is heavily driven by rising wages, and today, much of this increase is focused on the lower-income population, the Fed views this as ‘good’ inflation. For some time, I have argued that the Fed’s third mandate is one of social stability, or more succinctly, compressing the wage gap.

Chair Powell and the Fed’s race to cross the 2% inflation finish line is made more difficult by the strong US economy headwinds blowing in their faces. Imagine also trying to do this while wading through a flood of government spending stemming from December’s omnibus spending bill. In other words, this battle against inflation is at odds with the easy fiscal policy crosscurrents. Unsurprisingly, I think it will be more difficult for the Fed to go from 6% to 2% inflation than it was to shed the excesses from 9% to 6%.

The silver lining to all of this is that a tightening Fed means that yield and income are back! Investing in T-bills or two-year treasuries will not provide a better economic outcome than investing in areas in which investors can earn a credit risk premium. For a while now we have suggested that the economy will be more able to perform into higher rates. However, we have also said that our belief is that there is such thing as rates too high to sustain growth. We think that about 3.75% is fair value for the 10-year treasury, and we are opportunistically adding protection with treasuries when rates rise above this level and reducing duration when we have seen rates notably below this level. We work to balance the opportunity in both credit and rates and expect that volatility will remain high throughout the year.

Away from rates, all the talk about an imminent recession has pushed spreads further above treasuries in most areas of the market. Given the ongoing strength in consumer spending, we believe the best relative value on a sector level continues to be in securitized debt. These non-agency, asset-backed securities spreads on the AA to BBB ratings spectrum are wider than investment grade corporates.

Although this is generally the case, today’s premiums are wider than usual. We favor ABS and residential mortgage-backed securitized credits, which provide additional protection in the form of fast paydown and underlying collateral to provide some ballast when—not if—we enter a recessionary environment.

We prefer prime borrowers through bonds backed by consumer loans and autos because subprime customers are much more sensitive to evaporating stimulus and heightened inflation. When we elect to take on subprime exposure, it’s because we believe the bonds are “senior” in the capital structure and these bonds tend to pay down very quickly.

Many investors also ask about emerging market debt. We are cautious and selective in these spots given their inherent high levels of global risk. But slowing U.S. growth means EM growth differentials are more favorable in 2023 and an eventual pivot from the Fed will slow the rise of the dollar.

In terms of credit quality, we favor investment-grade corporate bonds over high-yield corporates. In an environment of weak growth, we are weighted toward non-cyclical names in utilities, healthcare, select tech, and high-quality financials. We won’t close the door entirely on high yield—seven to eight percent would capture any investor’s attention¬—but as with emerging markets, we pair our robust bottom-up, fundamental process with a top-down view to be highly selective in our approach.

Looking ahead, we still see some red lights on the dashboard. Few investors have weathered an inflationary storm like this, and the inflationary environment last time was radically different. The last decade’s game of monetary and fiscal stimulus has had profound effects on the global economy, and without a playbook, it’s hard to predict how this experiment may end. Caution is the only rule, and we believe we are positioned well to capture yield and remain defensive.

Tribune by Jeff Klingelhofer, CFA, is Managing Director and Co-Head of Investments at Thornburg Investment Management.

The Securities and Exchange Commission proposed amendments designed to modernize its information collection and analysis methods by, among other things, proposing that a number of filings be submitted to the Commission electronically on EDGAR using structured data where appropriate.

Under current rules, registrants are required to file or otherwise submit many Exchange Act forms, filings, or other submissions in paper form. During the COVID-19 pandemic, many submissions were made in electronic rather than paper form, which was generally well received.

As part of its efforts to modernize the methods by which it collects and analyzes information from registrants, the proposed amendments would require registrants to make these submissions to the Commission electronically.

“We live in a digital age. In 2023, one might think that all filings to the Commission already could be made electronically. That’s not yet true,” said SEC Chair Gary Gensler. “We have the important opportunity to require electronic filing for nearly all of the remaining paper filings required under the Exchange Act. I believe the proposal, if adopted, would save both registrants and the Commission time and resources.”

Specifically, the proposed amendments would require the electronic filing, submission, or posting of certain forms, filings, and other submissions that national securities exchanges, national securities associations, clearing agencies, broker-dealers, security-based swap dealers, and major security-based swap participants make with the Commission.

The proposed amendments would also make certain amendments regarding the Financial and Operational Combined Uniform Single (“FOCUS”) Report to harmonize it with other rules, make technical corrections, and provide clarifications. In addition, the proposed amendments would require withdrawal of notices filed in connection with an exception to counting certain dealing transactions toward determining whether a person is a security-based swap dealer in specified circumstances.

The public comment period will remain open for 30 days after publication in the Federal Register or until May 22, 2023, whichever is later.

Vontobel Asset Management has appointed Ignacio Pedrosa as Head of Latin America and US Offshore.

With 25 years of experience in distribution for asset and wealth management, Ignacio Pedrosa will be responsible for expanding and strengthening Vontobel’s partnerships in LatAm and US Offshore.

He joins Vontobel in its Miami office from BTG Pactual, where he was responsible for third party distribution and servicing institutional investors across LatAm and US Offshore.

Prior to that, he held senior-level positions at various investment firms in Madrid, including Tikehau Investment Management, EDM Asset Management and Bestinver Asset Management. He holds a Bachelor’s in Economics from the Universidad San Pablo-CEU in Madrid.

Additionally, Molly Katherine McVeigh, who has been with the firm since 2020 and a key contributor to business development and enhancing the client experience, will expand her relationship management responsibilities for LatAm and US Offshore.

“These appointments reinforce our client-centric priorities for growth in the US and the broader Americas regions, as well as our engagement with global banks,” said José Luis Ezcurra, Head of the Americas. “We are pleased to have Ignacio and Molly in these strategic roles, driving our commitment to providing quality solutions to investors and distribution partners.”

Vontobel has established its global success through differentiated investment expertise, bringing long-term solutions to investors in the Americas since 1984. Founded as a single boutique offering in the US, the firm has advanced its presence across the Americas as a multi-boutique manager with specialized investment solutions across asset classes to meet investors’

growing demands, the firm added.

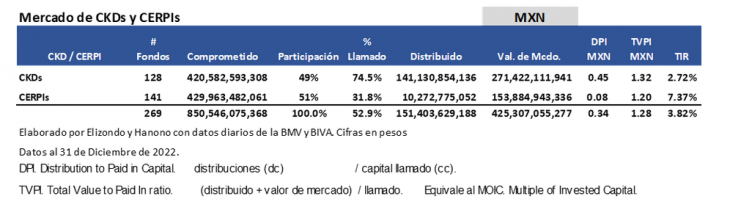

The international investments of the CERPIS in Private Equity, have improved the returns on this asset class by a ratio of three to one. The 128 outstanding CKDs (including those that have been amortized) have a net IRR weighted by 2.7% net in Mexican pesos (MXN) as of December 31, 2022, while the IRR of CERPIs is 7.4%. IRRs are in MXN and not US, because institutional investors who invest in CKDs and CERPIs have their portfolios evaluated in MXN.

The CKDs are the vehicles registered in the Mexican Stock Exchange (BMV and BIVA) that allow institutional investors to invest in local private equity and the CERPIs are the ones that can invest globally.

The weighted IRR of both is 3.8%. There would be several considerations:

The CKDs (128) were born in 2009 (almost 14 years ago) and have called 75% of the capital to date.

The CERPIs (141) although they were born in 2016 it was from 2018 that they began to invest globally, which means that they are almost 5 years old and have called 32%.

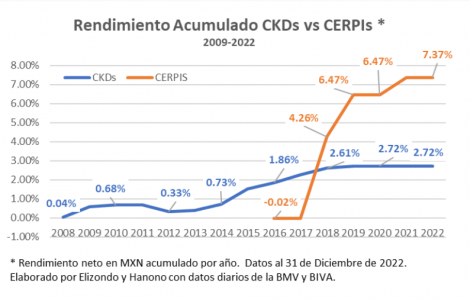

With less time and capital called, CERPIs have improved profitability in this asset class. If the AFOREs had only invested in CKDs today the return would be 2.7% and if they had only invested in CERPIs it would be 7.4% net in MXN. This data is weighted for the 128 CKDs and 141 CERPIs respectively. When graphing the IRR of the CKDs, its evolution year after year has been gradual, while the behavior of the IRR of the CERPIs shows a steeper slope.

The great diversity of options available when investing in global private equity has allowed the AFOREs to select those global funds that have practically no “j curve”. The “j curve” is the investment period of private equity funds in which investments in this asset class show an initial loss (investment period) followed by a dramatic rise. On a chart, this pattern of activity would follow the shape of a “capital J”.

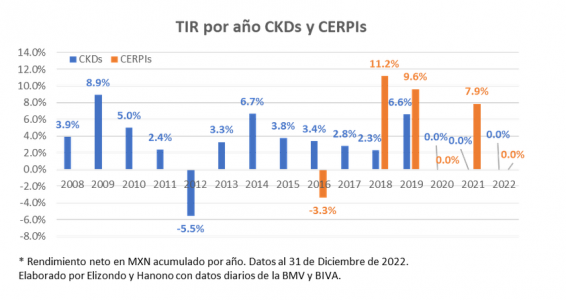

When reviewing the yields per vintage, it is observed that in four years (2009-2010-2014 and 2019) CKDs had yields greater than 5%, the rest being lower; while for CERPIs there are three years with yields above 8% and only one year with negative IRR corresponding to the issuance of the first CERPI (j curve effect).

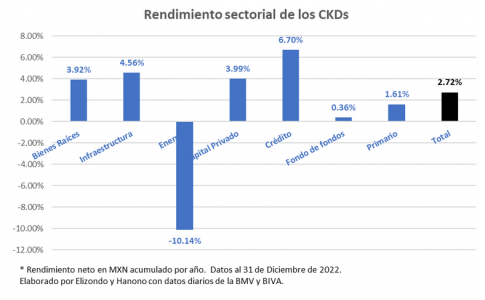

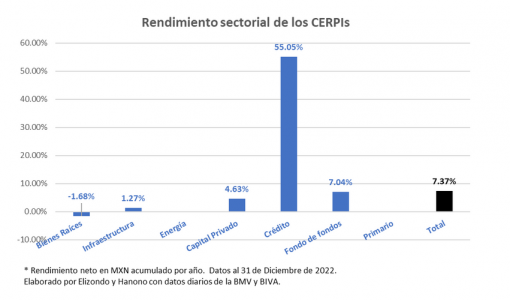

When presenting the net IRR in MXN for CKDs in a sectoral manner as of December 31, 2022, the Credit (17/128 CKDs) and Infrastructure (17/128) sectors are the ones that have offered the best IRRs to date. It is important to recognize a “J curve” with less slope for the most unfavorable sectors. These results change over time by capital calls and market valuation, among other variables.

In the case of CERPIs, the Fund of Funds/Feeder sector (130/141), which concentrates 87% of the market value, has an IRR of 7.0% that weights the market value of the Credit sector (1/141), as well as the other sectors that allow the net IRR weighted in MXN to be raised to 7.4%.

If the 8% rate (preferential rate) is considered as a threshold to distinguish the most profitable funds; with IRR greater than 8% net in MXN there are 37 of 128 CKDs (29%); if those with IRRs greater than 10% are considered, there are 22 CKDs and if those with IRRs greater than 15% net are considered, there are 4 CKDs. Of a total of 64 CKD administrators (GPs) only 19 have IRR greater than 10%, so there are few administrators who present competitive IRR to date.

In the case of CERPIs, 36 of 141 CERPIs (26%) have IRR greater than 8% as of December 31; with IRR greater than 10% there are 30 and with IRR greater than 15% there are 25 CERPIs with data as of December 31. Being an important number of CERPIs Funds of Funds that act as Feeders, if in each CERPI there are two global funds (conservative number) in total there are more than 280 funds, although many of them are the same in the different CERPIs. Diversification is proving important in CERPIs.

Where is the market going?

Historical IRR makes CERPIs look like an alternative that has helped institutional investors to diversify and improve the returns in this asset class.

The competition that has occurred between local and foreign GPs has allowed the institutional investor to compare between the options in the market, selecting those sectors and managers with proven experience and attractive results.

Of course, these comparisons may change as the investment cycle of CKDs and CERPIs concludes, however, today the numbers are skewed in favor of CERPIs.