Insigneo announces that Insigneo Securities, LLC and Insigneo Advisory Services, LLC have entered into a definitive agreement to acquire the Latin American consumer brokerage and investment accounts of PNC Investments, PNC Managed Account Solutions, and PNC Bank.

PNC will retain the deposit and loan accounts of customers with brokerage assets and assets under management moving to Insigneo and will continue to support the U.S. banking needs of their international clients. This strategic move represents a significant milestone for Insigneo as it further solidifies its position as a leader in the independent wealth management industry, the firm said.

With this acquisition, Insigneo will be opening new offices in Texas and expand its capabilities to serve a broader Mexican client base, while adhering to its mission of delivering exceptional client service, enabled by state-of-the-art technology, and driven by continuous innovation, the company added.

“The acquisition of PNC’s Latin American brokerage and investment operations further cements Insigneo’s position in the Americas as a leader in international wealth management,” said Raul Henriquez, Chairman and CEO of Insigneo Financial Group. “We are committed to the region with our strategy of empowering investment professionals to deliver excellent service and compelling investment strategies and solutions to clients globally”.

The acquisition is expected to close in the coming months.

In line with Vontobel’s ambition to drive the next stage of growth in the US, Vontobel SFA is expanding its Business Development team. Claudia Ruemmelein and Hansjuerg Raez are joining SFA as Senior Business Developers in the Miami and New York offices on September 1, 2023.

“Together with our ongoing efforts in the US, we believe that this integral next step will enable us to deliver on our strategic ambition, further build out our client base and service our partners and clients more effectively”, the firm said.

The Business Developers are the first point of contact for UBS financial advisors in the US, who continue to recommend SFA to their clients looking to diversify their assets internationally and thus offer tailored investments in Switzerland.

The important responsibility of the Business Developers is to maintain and expand our collaboration with UBS financial advisors, keep them informed about the Vontobel SFA offering, and reliably provide advice and support. The team, which includes employees in Zurich, New York and Miami, is to be expanded to around 10 experts over the next years under the leadership of Patrick Schurtenberger.

Hansjuerg Raez

Claudia will be based in Miami and brings more than 15 years of experience in the financial services industry, with a successful track record of building and developing new business in the Asset Management and Private Equity sectors. She joins us from Mesa Capital Advisors, where she covered Latin American institutional and UHNWI/Family Office clients investing in alternative investments.

Prior to that, she held various roles at First Avenue Partners, Apollo Management and PriceWaterhouse Coopers in New York, London and Frankfurt.

Hansjuerg will be based in New York and also brings more than 15 years of experience in the financial services industry. He joins us from UBS AGNew York, where he was responsible for multinational corporate clients and the expansion of that business for the last nine years.

Prior to that, he was at Trafigura in Stamford, Shanghai and Lucerne in various roles. Hansjuerg holds a bachelor’s degree in Business Administration from the University of Bern, Switzerland.

Achieving a portfolio under management of USD 500 million of high-net-worth families in a short period of time is not easy, considering the aggressive competition among firms and colleagues visiting the same clients and offering the same products. The elements that can differentiate us are what determine success or failure.

Over the years, we have overcome international and regional crises that have made us experts in how to protect and increase wealth in the face of changes that occur.

But now, the challenge is greater, because we not only have to face the post-pandemic economic changes, including changes in consumer behavior, but also the management of the inflationary phenomena and global interest rate hikes.

Additionally, we are facing a change in our industry, not only due to the arrival of AI (Artificial Intelligence), but also because major firms are migrating their strategies, and advisors are caught amid this chaos.

Therefore, we must make decisions thinking about our plan for the next 10 years, both for ourselves and for our clients.

Analyzing the situation:

a) Many large firms have shifted their focus from “putting their clients first” to ceasing service to those who are not their primary market… without prior notice, or clear future expectations.

b) There are many parameters to analyze, and everything is based on who your clients are: individual or institutional, country, size, sophistication in investments, with or without banking services (credit cards, transfers, loans); and whether your approach is comprehensive, supporting your clients with their assets and efficient planning and organization of their wealth, or if you prefer to only focus on their investments.

c) Clients demand personalized, flexible, and prompt attention; many “large” firms become bureaucratic and when their focus is not on the client, they lose their responsiveness, either relying on machines or on newly advisors focused on promoting “combo” portfolios that often do not meet the complex profile and needs of the client.

d) Advisors understand the clients’ “preservation profile“: strong jurisdictions in which to diversify with properties and financial assets held in well capitalized firms, with diversified portfolios seeking high income and capital growth, taking advantage of market opportunities within their profile (which is generally more conservative than established… when corrections occur) and therefore managing their assets accordingly, as trusted individuals with whom we have weathered various storms together. Our clients seek captains who know how to navigate and reach the destination.

e) We know where their money comes from, and it truly gives us a unique opportunity to respect their work, admire their achievements, and understand the dynamics of our clients, their families, and businesses in order to plan for intangibles – what is more important: the potential 20% market correction which generally recovers over time, or a family going through a divorce and “losing” 50% of their assets? Or an international client in the US with a personal investment account potentially losing up to 40% of their portfolio above USD 60,000 in US securities due to inheritance taxes? (*IRS info). It is part of our work, along with other professionals, to plan with companies, trusts, and other tax-efficient structures.

f) To preserve wealth, we involve future heirs so that they are aware that investment accounts are the funds generated and not spent over many years by their predecessors, along with the compounding effect (* Rule of 72 info), e.g., a portfolio doubles at 7.2% annual rate every 10 years). This way, when they receive them, they don’t “gamble” with them or spend them with their “new” friends.

g) Providing tools is always more educational than giving away, and for this purpose, there are strategies such as borrowing against the family portfolio (so they develop their projects with the discipline of having the obligation to repay); a strategy that is also used to acquire properties in a tax-efficient manner or support local businesses while maintaining the medium to long-term investment portfolio. It is also good for them to learn how it works because diversification and “time in the markets” are the only secrets to financial success.

Considering this description of the context, we must ask ourselves:

At what point in your life are you…

Do you have the resilience to be a “soldier of your firm”, following orders to “close your clients’ accounts” in exchange for receiving the clients of the colleague who dares to take the step, or to retire? Or do you have the energy to be loyal to your clients to do all the work of establishing their accounts again and understand that there will be surprises along the way with the clients themselves, your colleagues, or the new firm or structure you choose?

Think about the future and try to understand who you want to work for in the next 10 to 15 years: a firm, your own firm, or clients? Your current clients or those who take the step with you (and truly value you)? New clients, markets, team, or strategic alliances?

The feeling that is generated when a partner or client accompanies you is tremendous and generous; they are there for you, just as you have been there for them… and naturally, you will take care of them, their children, and referrals.

It would be expected that the relationships built on years of effort and hard work surpass temporary separations of months (due to compliance with protocols and sector-specific rules).

According to a Wealth-X report, high net worth clients often follow their investment advisors when they decide to switch firms. This is due to the trust and experience that they have developed with their advisor over the years. The report also highlights that client loyalty to the investment advisor outweighs loyalty to the firm itself. Additionally, a survey conducted by PwC reveals that 64% of high-net-worth clients consider the personal relationship with their financial advisor as an important factor when choosing a wealth management firm.

Speaking of motivation, if one is recognized in the industry, besides choosing wisely and going where one feels better, you can “capitalize” on the change, and the work is very well rewarded…

A very personal article, as a Portfolio Manager, a market researcher, and with my own convictions… the same beliefs that led me to enter 2022 with over 30% of my clients’ USD 500 million in cash because I anticipated interest rate hikes and cash along with a small proportion in alternative investments (properties) was the only thing that could protect them.

And, as someone dedicated to my clients, recognized by Forbes, Working Mother, Women We Admire-Miami, and even being congratulated in Times Square… now, anticipating the events and adapting to the new reality, I have stepped out of my comfort zone to search, compare, and find the best place for my clients, a “boutique-style within one of the best capitalized financial institutions in USA with extensive resources,” or as my clients say, “we went from Rolex to Patek Philippe.”

Therefore, considering the question “should I stay, or should I go?”, and in order to grow, check the following points:

The significant growth in wealth management by boutique firms, as indicated in the Wealth-X report, also highlights that boutique firms have been successful in attracting high-profile clients such as successful business owners, institutional investors, and affluent families. This is due to their ability to quickly adapt to the changing needs of these clients, offering tailored solutions and high-quality personalized service, particularly in markets emerging and growing economies.

The increasing demand for online financial services and mobile applications by clients.

The increase in investment in North American firms. Additionally, the importance of understanding tax and legal regulations in both countries and properly preserving money in an efficient tax structure.

The search for estate planning services and investment in real estate in the United States.

Clients’ preference for responsible investment and strong personal relationships based on trust and tailored to cultural needs.

And, I will share my thoughts on strategy at this moment: position your cash… remember that in the last two decades there have only been high interest rates a couple of times, and therefore, considering the decrease in inflation, among many other variables, I believe that interest rates will decrease in the coming years; based on that, I suggest increasing the fixed income investments in your portfolio’s asset allocation, targeting yields of at least 5% with a conservative mix of securities such as fixed-term deposits – CDs (FDIC-insured certificates of deposit), as well as investment-grade bonds. It’s also time to extend the duration and increase maturities to maintain high cash flows and potential appreciation (you can stagger maturities for liquidity if needed). For additional income, growth, and currency diversification, consider including funds & ETFs (Exchange Traded Funds), which for emerging markets (bonds and stocks) are a good way to better protect principal, thanks to diversification and tax efficiency – at least, ‘offshore’ offer to international clients.

In conclusion, taking into account these considerations supported by reliable reports and sources, remember the words of Warren Buffett: ‘It takes 20 years to build a reputation and only 5 minutes to ruin it,’ as it will help you make the right decision.

Whether it’s staying with your current firm, moving to another firm, becoming independent, changing sectors, or even taking a break or retiring… It’s time to make that decision with courage, conviction, and triumph. Keep soaring high and enjoy the journey while continuing to be the best version of yourself.

Frederick Shaw, Country Head – United States at Apex Group

Apex Group announces the appointment of Frederick Shaw as Country Head – United States, responsible for overseeing the delivery of Apex Group’s single-source solution to clients in the geography.

Shaw brings two decades of experience in the financial services industry, joining Apex Group from private markets investor, Hamilton Lane, where he held the role of Chief Risk Officer and Global Head of Operations.

During his tenure, Shaw led teams overseeing the company’s domestic and international regulatory compliance and risk management frameworks along with its global operations complex. Prior to joining Hamilton Lane in 2011, Shaw held senior compliance and operational roles in international banks and alternative asset management.

In his new role, Shaw will oversee Apex Group’s rapidly expanding US business, which now employs over 600 people across 15 local offices.

The Group’s domestic US clients, as well as international clients investing into the US, benefit from the efficiency of a single-source solution, including access to a broad range of services including Digital Banking, Depositary, Fund Raising Services, and pioneering ESG Ratings and Advisory Solutions, offered globally and delivered locally, the firm said.

In addition to strong organic growth, Apex Group has also recently completed the integration and rebrand of theacquisition of Greenhough Consulting Group, bolstering its corporate and business services offering for funds and corporates, the company added.

Shaw will work closely Apex Group’s experienced regional leadership team, including recently appointed Group President, Samir Pandiri, Georges Archibald, Chief Innovation Officer and Regional Managing Director, Americas and Elaine Chim, Global Head of Closed Ended Products.

Georges Archibald, Chief Innovation Officer and Regional Managing Director, Americas, comments: “We are thrilled to welcome an executive with Fred’s knowledge and outstanding market reputation to our senior leadership team. His extensive buy side experience will provide valuable insights into the requirements of our current and future clients and enable us to further enhance their operational efficiency and performance. Fred shares our commitment to maintaining regulatory standards while embracing new ideas and approaches as we evolve to become the service provider of the future.”

Frederick Shaw, Country Head – US adds: “I am excited by the opportunity to join Apex Group, drawing on my client-side experience to drive continued service excellence, innovation and growth for clients. Apex Group has successfully disrupted the US market, as an independent provider of a compelling single-source solution which supports the entire value chain of a business. I look forward to playing a part in the business’ continued success, by leveraging Apex Group’s technology and solutions to better address the priorities of our clients.”

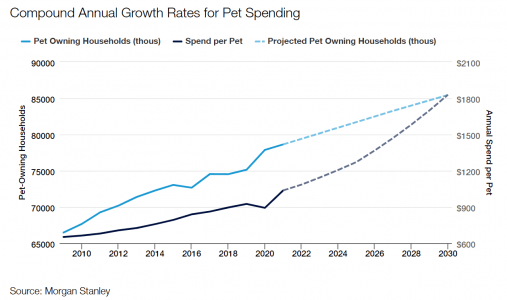

The COVID-19 pandemic has impacted us in numerous ways, setting off a cascade of dramatic changes to our lifestyles, and amid the unique circumstances of the lockdown environment, many turned to pets for companionship. The American Pet Products Association estimates that pet ownership increased from 56% of households in 1988, to 67% in 2019 and 70% post pandemic, mostly driven by millennials. Dogs comprise 57% of pet ownership, followed by cats at 27%.

Households across the U.S., Europe and Asia are shrinking due to a combination of lower birth rates, delayed marriages and overall rising costs of living and having children. In the U.S., for example, the average number of people per household dropped from an average of 3.5 in the 1960s to roughly 2.5 by 2020. As family formation has taken a back seat, and as many employees were told to work remotely during the pandemic, many millennials have chosen to have “fur babies” over children, especially during the COVID-19 pandemic. According to census data as of July 2019, millennials have overtaken baby boomers as the largest generation with 72 million members, and they experienced the highest increase in pet ownership among all age groups.

Millennials (born from 1981 to 1996), as well as Gen Z (1997 to 2013), are also the age groups that are most likely to consider their pets to be part of the family. Their desire to humanize their pets means they’re more willing than any other age group to spend a larger portion of their incomes on keeping their pets healthy and happy. More important, these two age groups are also expected to own roughly 60% of U.S. dogs by 2025, exceeding the pet ownership of the boomer generation. We believe this increase, and these age groups’ stronger attachment or “humanization” of their pets, will together provide a durable tailwind for the pet sector for many years to come. As seen below, Morgan Stanley predicts an acceleration to an 8% compound annual growth rate for U.S. pet expenditures by 2030, one of the largest rates of return in any retail segment.

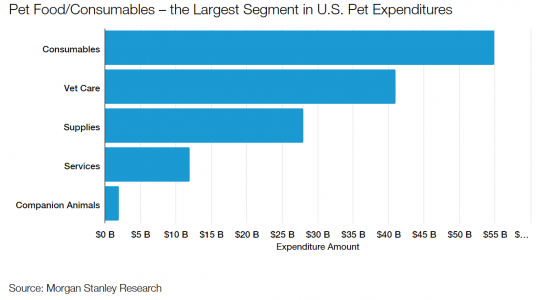

In addition, while emerging-markets countries such as India, Mexico, China and Brazil are currently lagging developed nations in pet ownership per capita, there is broad-based growth. In fact, according to a pet industry report by Bloomberg Intelligence, the global pet industry is expected to reach $493 billion by 2030, representing a drastic 54% increase from current levels. Although the U.S. will likely continue to be the largest market, emerging markets countries are also expected to deliver growth due to under-penetration of packaged dog food. Under-penetration and premiumization should continue to drive the largest consumables segment, while the basic need for pets to eat reduces cyclicality.

With a growing number of Americans regarding their pets as essentially a member of their family, the “pet humanization” trend has spawned an explosion of new businesses that focuses on providing better pet nutrition and care. Pet “parents,” especially in the developed world, have become increasingly educated about pet diets, and they are willing to devote more of their hard-earned money on premium, natural or branded pet foods. The “premiumization” of pet food has accelerated in popularity, particularly among millennials, who are more willing than other age groups to make financial trade-offs here and invest in their pets’ health.

More to the point, U.S. millennial consumers are moving away from highly processed and lower-quality dry food (i.e., kibble) to pet foods that are minimally processed or so-called “raw” or “gently cooked” with human-grade ingredients. Gourmet-level dog and cat food is one of the fastest-growing areas in the pet food market due to its superior nutrition and lack of additives. Fresh pet food is believed to provide benefits like more energy, shinier coats, less stinky breath and healthier skin. Moreover, for consumers, cost seems to matter less and less in today’s landscape.

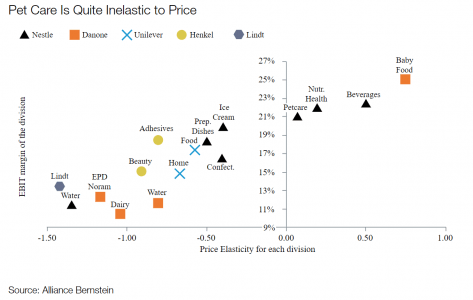

The premium pet food category appears to be one of the last areas where consumers are making “trade-down” decisions — that is, where they are willing to substitute for cheaper products — even despite high inflation eating away at household incomes. And once pet parents find high-quality foods that work for their pets, they’re unlikely to switch. As a result, pet food — and especially premium pet food — is proving to be one of the most resilient areas compared to other spending categories. As seen below, the price elasticity of the pet care category, which includes pet food, is almost as inelastic as those of baby food.

Lastly, adoption and acceleration of e-commerce have helped further bolster the pet food sector. Pet food e-commerce was already growing at a healthy pace before the pandemic, but digital paths to purchasing pet food have gained even more traction in recent years. Carrying home heavy boxes of dog food, or other pet products, like cat litter, isn’t appealing. And pet owners, especially those in the younger generations, are seeing the value of online shopping as well as direct and auto-shipping to their doorsteps. According to a 2021 report from Packaged Facts, pet food e-commerce will account for 55% of total U.S. pet food sales by 2025. That is up from approximately 30% today, above the 20% average for all U.S. retail.

The culture shift around pets has helped propel a rising demand for natural and premium pet goods. We believe the pet food industry is one of the most recession-resistant defensive plays, but also a structural growth story in the market.

Analysis by Mustafa Arikan, equity research analyst for Thornburg Investment Management.

Wipfli, a top 20 advisory and accounting firm, published the results of two industry surveys from the wealth management and asset management sectors to gain insights into their current economic challenges and how they’re positioning themselves for long-term market stability.

Ongoing rate hikes, uncertain market performance, geopolitical tensions, and increased competition all contribute to overall cautious economic predictions in both the new State of the wealth management and State of asset management industry reports.

“Our research indicates common themes uniting wealth management and asset management firms’ priorities,” said Anna Kooi, financial services and institutions practice leader at Wipfli. “Employee retention and recruitment, client engagement, and technology integration are all crucial for future success, and firms have to balance budget allocations and investments in each area appropriately.”

Both wealth management and asset management firms anticipate shifting economic times ahead, with 62% of wealth management firms and 72% of asset management firms expecting a U.S. recession in the next 12 months. Accordingly, the majority of survey participants for each industry estimate conservative market growth of five to eight percent over the next 12 months (55% wealth, 65% asset). Less than a third for both industries anticipate standard growth of eight to ten percent.

Recruiting top talent and implementing technology are key concerns for both industries. About two-thirds of both industries (66% wealth, 69% asset) list employee recruitment as one of their top concerns, and asset management firms note that talent management is their most important strategic focus. Also, asset management firms are ahead of the curve in recognizing how technology can assist and automate tasks for employees, while wealth management firms are also focused on new client acquisition and cultivation.

“Wealth management firms need to focus on targeted strategies that will help them foster long-term stability and viability,” said Paul Lally, wealth and asset management industry leader, principal at Wipfli. “In today’s uncertain economy, it’s critical for firms to adapt and constantly reassess their growth strategies.”

For example, most wealth management firms surveyed listed new client demographics as a key priority, but the majority also reported making no changes to their client acquisition strategies. In addition, offering employee flexibility was seen as key to addressing recruiting concerns, yet 64% of wealth respondents also expected employees to work in the office five days a week. Workplace flexibility and increased employee benefits will be key for firms to attract new talent, and wealth management firms should ensure that their growth plans align with their overall goals and initiatives to avoid contradictions in their strategies.

Asset management respondents are experiencing a massive shift in how technology is applied in their day-to-day operations. Three-quarters of asset firms surveyed named “managing and implementing change” as the top factor driving their goal achievement. With the onset of industry-changing technologies like artificial intelligence enhancing their work, asset management firms know they are on the precipice of a new era.

“Asset management firms recognize the important role technology will need to play due to the ever increasing complexity of investment opportunities and client demands.” said Ron Niemaszyk, partner for Wipfli’s wealth and asset management practice. “New and older generations of clients are increasingly comfortable with technology, and expect firms to provide a level of reporting on metrics well beyond that of monthly returns. Investors are now looking for insights into their portfolios’ risks and exposure to ESG initiatives. Firms who begin offering this type of reporting now can establish an edge in client acquisition over less progressive competitors.”

Technological integration is transforming how wealth management and asset management firms do business. In both industries, some firms are already using technology to support more efficient client onboarding and account management processes, as well as using data analytics to inform business decisions. Eighty-three percent of asset management firms are using business analytics to support data-driven decisions, and 58% of wealth management firms have increased their use of analytics in key business strategies.

The wealth management survey was based on responses from 102 wealth management firms across 28 states, and the asset management survey had 99 firms respond across 31 states. Both the State of the asset management report and the State of the wealth management report can be found on Wipfli’s website.

Ocorian has strengthened its financial crime and anti-money laundering support for clients with a key appointment. It has promoted Joe French to Managing Director and Head of its Financial Crime and Consulting Services.

Joe French is promoted to his new role having previously worked for Ocorian’s Newgate Compliance Limited for over six years. His experience includes 13 years with HM Revenue & Customs leading intelligence teams which developed domestic and international criminal and civil cases in relation to money laundering, fraud and cyber-crime. Prior to this he worked for the Financial Conduct Authority, after starting his career with Royal Bank of Scotland.

This comes as recent international research with more than 130 family office professionals, commissioned by Ocorian, said growing regulatory pressures are a key driver behind 91% expecting their outsourcing to grow over the next three years.

Ricky Popat, Director – Regulatory & Compliance at Ocorian said: “Joe’s appointment and our growing financial crime team emphasises our focus on excellence in this area. We know that many clients including family offices struggle to source regulatory support, so we’re delighted to be able to enhance our services to clients with particular emphasis on digital assets.”

Joe French added: “Regulatory demands are increasing rapidly across all jurisdictions and businesses often find it difficult to ensure they remain compliant on a continuous basis and financial crime is a major focus for regulators worldwide. I’m excited to be part of a growing team at Ocorian who can offer clients the very best advice and continue and to supporting clients with pragmatic and flexible solutions building on the wide range of services provided by Ocorian.”

Investors Trust announces the launch of ITA University, its innovative online educational platform. In alliance with IE University and CFA Institute, Investors Trust continues its commitment to provide the financial advisor of the future with the best resources available.

This educational platform will be available only for financial advisors working with Investors Trust and aims to deliver a one-of-a-kind approach to higher education for IFAs looking to expand their skills and professional knowledge.

ITA University will provide tailor-made courses, certifications, and other educational resources in collaboration with Investors Trust’s strategic partners IE University and CFA Institute. By joining efforts with these prestigious institutions, financial advisors working with Investors Trust will have access to top-rated personalized training in order to deliver the best service to their clients.

“We believe education is key to keep growing in an evolving and always changing industry. ITA University is another representation of Investors Trust’s commitment to the development and success of our financial advisors,” said Ariel Amigo, Chief Marketing & Distribution Officer.

Investors Trust is excited for the launch of this powerful educational platform and to work alongside top-rated institutions in order to keep providing excellence in the insurance and investments industry.

The income necessary to buy a starter home has risen most in Florida, according to a new report from Redfin.

In Miami buyers need to earn $79,500 (up 24.8%) to afford the typical $300,000 starter home. Rounding out the top three is Newark, NJ, where buyers need $88,800 (up 21.1%) to afford a $335,000 home. Fort Lauderdale, Miami and Newark also had the biggest starter-home price increases, with prices up 15.8% year over year, 13.2% and 9.8%, respectively.

In addition, Fort Lauderdale buyers need to earn $58,300 per year to purchase a $220,000 home, the typical price for a starter home in that area, up 28% from a year earlier. That’s the biggest uptick of the 50 most populous U.S. metros.

Even though starter-home prices have risen most in Florida, they’re still less expensive than a place like Austin or Phoenix, where home prices skyrocketed during the pandemic and have since come down some.

Prices are rising in Florida because despite increasing climate risks, out-of-town remote workers and retirees are flocking in. That’s largely due to warm weather and relative affordability; even though prices there soared during the pandemic, homes are still typically less expensive than a place like New York, Boston or Los Angeles. Five of the 10 most popular metros for relocating homebuyers are in Florida.

The U.S. Average

A first-time homebuyer must earn roughly $64,500 per year to afford the typical U.S. “starter” home, up 13% ($7,200) from a year ago.

The typical starter home sold for a record $243,000 in June, up 2.1% from a year earlier and up more than 45% from before the pandemic. Average mortgage rates hit 6.7% in June, up from 5.5% the year before and just under 4% before the pandemic.

Prices for starter homes continue to tick up because there are so few homes for sale, often prompting competition and pushing up prices for the ones that do hit the market. New listings of starter homes for sale dropped 23% from a year earlier in June, the biggest drop since the start of the pandemic. The total number of starter homes on the market is down 15%, also the biggest drop since the start of the pandemic. Limited listings and still-rising prices, exacerbated by high mortgage rates, have stifled sales activity. Sales of starter homes dropped 17% year over year in June.

“Buyers searching for starter homes in today’s market are on a wild goose chase because in many parts of the country, there’s no such thing as a starter home anymore,” said Redfin Senior Economist Sheharyar Bokhari. “The most affordable homes for sale are no longer affordable to people with lower budgets due to the combination of rising prices and rising rates. That’s locking many Americans out of the housing market altogether, preventing them from building equity and ultimately building lasting wealth. People who are already homeowners are sitting pretty, comparatively, because most of them have benefited from home values soaring over the last few years. That could lead to the wealth gap in this country becoming even more drastic.”

Home prices shot up during the pandemic due to record-low mortgage rates and remote work, and now rising mortgage rates are exacerbating the affordability crisis, especially for first-time buyers. A person looking to buy today’s typical starter home would have a monthly mortgage payment of $1,610, up 13% from a year ago and nearly double the typical payment just before the pandemic. Average U.S. wages have risen 4.4% from a year ago and roughly 20% from before the pandemic, not nearly enough to make up for the jump in monthly mortgage payments.

Many prospective first-time homebuyers are between a rock and a hard place because rents remain elevated, too. The typical U.S. asking rent is just $24 shy of the $2,053 peak hit in 2022.

Over the last few years, inflation, rising interest rates and high costs for just about everything have impacted nearly everyone – but for Gen Z, the economic environment has had a profound impact, a new U.S. Bank survey found.

Members of this generation, who range in age from 18 to 26, are overwhelmed by recent economic news, are unsure how to start investing, compare their financial progress to others – including their parents, people they see on social media, and people better off than they are – and are highly motivated by experiences and the pursuit of personal interests and opportunities. Members of the Millennial generation, aged 27-42, share many of these same feelings.

“Younger generations are dealing with inflation, high interest rates, and high prices, but they also inherited a much different world than older generations: since 1980, college tuition has increased by 169%; the average price of a home is up 540%; and average student-loan debt now sits at $37,000,” said Gunjan Kedia, vice chair of Wealth, Corporate, Commercial and Institutional Banking at U.S. Bank. “It’s no wonder they are unsure about beginning an investing journey. But despite these headwinds, they are passionate about investing in causes they believe in and are seeking financial guidance.

“We did this survey to better understand the challenges the younger generation is facing, how they are (or aren’t) investing and why, and how we can help them start investing before they lose too much time. Some of the findings that really stood out for me are that financial worries and decision fatigue are impacting young investors’ confidence, they are overwhelmed and unsure how to begin investing, and nearly 80% of investors responded to the economic climate by changing their investment strategies in some way in the past three months.”

Among the highlights of the report are the search for a better quality of life, personal interests and new experiences drive the investment decisions of younger generations.

In addition, Gen Zers view wealth differently than older generations and will sacrifice returns to invest in causes they believe in.

Finally, younger generations compare themselves to others and social networks.

The new data is from a proprietary U.S. Bank survey of 3,000 active investors and 1,000 aspiring investors of all generations. The survey was conducted May 12-24, 2023.

To read the full report, please click on the following link.