Insigneo, an international firm specialized in wealth management, has welcomed Renato Bisconcini and Renato Rizzatti to its team. Both join as Managing Directors and investment professionals to expand coverage in Brazil. According to the firm, the team comes from BTG Pactual and brings experience in managing sophisticated portfolios for ultra-high-net-worth and high-net-worth clients in Brazil.

Before their time at BTG Pactual, Bisconcini and Rizzatti held key positions at Morgan Stanley, where they built a strong reputation for delivering tailored financial strategies to Brazilian families and institutional investors. Their decision to join Insigneo reinforces the firm’s commitment to attracting top-tier talent and expanding in Latin America.

“We are thrilled to welcome Renato Bisconcini and Renato Rizzatti to the Insigneo family. Their deep knowledge of the Brazilian market and proven track record are invaluable. These two professionals represent the high caliber of advisors we strive to work with, and their addition strengthens our position as the leading platform for international wealth management,” said Alfredo J. Maldonado, Managing Director and Head of Market for the Northeast Region.

By joining Insigneo, the team will leverage the firm’s open architecture platform and technology to offer clients a wide range of global investment solutions tailored to their evolving needs. Their addition to the Insigneo network represents a strategic step, strengthening its wealth management capabilities with top industry talent across Latin America.

“We are excited to join Insigneo. The firm’s entrepreneurial structure, open architecture platform, and tech-driven infrastructure expand what we can offer, more options, greater customization, and a smoother client experience. Insigneo will allow us to move faster, tailor solutions more precisely, and maintain a client-centered approach across market cycles,” said Bisconcini and Rizzatti in a joint statement.

Citi Private Bank has added Jorrell Best, Lucas Fayad, and Luis Madia de Souza to its Latin America team, according to Antonio Gonzales, head of the region, in a post on his LinkedIn profile.

In the post, Gonzales welcomed the new bankers and emphasized that “these colleagues bring strong experience in wealth management and will be invaluable partners in serving our clients and driving growth in their respective regions.”

Of the new trio, Fayad and Madia de Souza will focus on the Brazilian market, while Best will cover Central America and the Caribbean from Miami, strengthening the regional coverage of the group’s private banking franchise.

Jorrell Best joins Citi Private Bank as a senior banker based in Miami, where he will serve clients in Central America and the Caribbean. He brings experience in wealth advisory for high-net-worth clients and is part of Citi’s U.S. private banking team, focusing on investment and planning solutions for international clients.

Lucas Fayad, meanwhile, joins the Brazil team from UBS Wealth Management, where he served as a private banker in São Paulo. His background centers on serving high-net-worth clients, with a strong focus on portfolio structuring and both local and offshore investment solutions.

Also joining for the Brazilian market is Luis Madia de Souza, who comes to Citi Private Bank after a long career at Itaú, where he worked for over 15 years in various wealth management and client relationship roles. His addition aims to reinforce local coverage and deepen the development of the private banking business in Brazil.

With these appointments, Citi Private Bank continues to strengthen its team in Latin America, a key region within its growth strategy for high- and ultra-high-net-worth clients.

Individual investors are showing growing interest in alternative assets, and firms specializing in this category are, in turn, increasingly focused on wealth management channels. This virtuous cycle, driven by product innovation and the search for returns and diversification, is leaving its mark on the industry globally. Today, it’s hard to find a major player in the private markets space that doesn’t view this trend as a key growth vector.

What was once an exclusive club for large institutional investors has opened up substantially, as industry transformation, and the differing return dynamics of private and public markets, continues to bring retail clients and large asset managers closer together. “Retail investors and pension systems around the world are increasing their participation in private markets, supported by regulatory changes expanding access to alternatives and a growing interest in infrastructure and real assets,” JP Morgan Asset Management noted in a recent report. The firm added, “This democratization of access is reshaping investor bases and fueling further growth.”

Naturally, asset managers are taking note and adjusting their strategies accordingly. While most of the big names in alternatives have yet to report their 2025 results, those that have emphasize the role of wealth management channels in their positive earnings.

A Beneficial Dynamic

Blackstone, for example, reported its best results in 40 years. While retail remains a minority share of the business, the firm highlighted the trend during its recent analyst call. “It’s notable that our capital raised in private wealth grew 53% year-over-year in 2025, reaching $43 billion, and we expect strong inflows again in 2026,” said Chairman and CEO Steve Schwarzman.

EQT, which also released results last week, noted that 26% of all capital raised during the 2024–2025 period came through private wealth channels. In an investor presentation, the firm detailed that its four evergreen funds, with a NAV of $4.1 billion, brought in $1.05 billion in flows during the first half of last year alone.

Other major players in the sector are set to report soon: Hamilton Lane on Tuesday, February 4; followed by KKR and Ares on Wednesday, February 5; Carlyle on Friday, February 6; and Apollo on Tuesday, February 11. All have previously highlighted the strength of private wealth flows and have made business decisions reflecting that momentum.

Carlyle CEO Harvey Schwartz noted that inflows from private clients into evergreen funds have risen from $300 million per quarter to $3 billion since he joined the firm in 2023. Meanwhile, KKR CFO Rob Lewin reported that the firm’s “K-series” vehicles, its family of wealth management–focused funds, raised $4.1 billion in Q3 alone. For Apollo Global Management, President Jim Zelter said the July–September period brought $5 billion in inflows from this segment.

The Key Piece: Semi-Liquids

The development of evergreen products, offering slightly more liquidity than traditional alternatives, is widely seen as critical to the expansion of this distribution channel.

“Retail investors will continue shaping the market,” predicted Eric Deram, Managing Partner at Flexstone Partners. In Natixis’s 2026 Alternatives Outlook, he wrote: “Evergreen semi-liquid products are gaining traction, appealing to both institutional and individual investors thanks to their simplicity and liquidity profile.”

As a result, product development in this area is now a top priority for major asset managers. Ares Management Corporation, for example, announced in its Q3 results that it had raised its 2028 AUM target for semi-liquid products in the wealth segment from $100 billion to $125 billion.

This is the prevailing tone across the industry, and one that will likely feature heavily in analyst and investor conversations during this reporting season. The sector is harnessing growth momentum from an expanding contributor base, and product offerings must evolve accordingly.

A Core Portfolio Component

Various surveys of financial advisors in developed markets show that alternatives are widely used in private portfolios. The fourth edition of the Alternative Investment Survey by CAIS and Mercer in the U.S. found that nine out of ten advisors include this asset class in portfolio management. Within that group, 16% allocate more than 20% to alternatives, while 49% have more than 10% exposure.

Independent RIAs and family offices appear to lead adoption, according to the survey. In this segment, one in four advisors allocates more than 20% to private markets.

Looking ahead, 88% of respondents plan to increase their alternatives allocation over the next two years.

In terms of product preferences, semi-liquids stand out: among advisors using alternatives in client portfolios, 82% use evergreen funds, either exclusively or in combination with other structures, with most of their clients. Private equity and private credit remain the most popular categories.

In Europe, data from the Private Banks and Wealth Managers Fund Selectors Survey by Novantigo show that UHNW clients have the highest exposure to private assets. Of this group, 33% allocate between 5% and 10% of their portfolio to such investments; 23% allocate between 10% and 15%; and 26% allocate more than 15%.

“Looking ahead, all client segments are expected to increase their private markets exposure, particularly in the HNW and UHNW segments,” noted the financial services firm in Efama’s Asset Management in Europe report.

The expansion of this trend in Europe has been supported by regulation, with the Eltif 2.0 era opening access to semi-liquid strategies for individual investors in the region.

Business Implications

Looking forward, the expectation is that this positive trend will continue. “We expect retail investors to become a growing source of AUM and fee-related revenues,” stated S&P Global Ratings in its Global Asset Manager Sector View for 2026.

However, the growing retail investor base also brings risks, the agency noted. “Products designed for individual investors may be more prone to volatility due to higher redemption rates, potentially resulting in more volatile EBITDA and leverage for asset managers with greater retail concentration,” the report said.

On another front, M&A dynamics in the industry suggest that firms are seeking to scale and add new capabilities. According to Deloitte’s Investment Management Outlook for 2026, a significant share of transactions in 2025 targeted wealth management and investment advisory companies.

“The continued expansion of alternatives offerings underscores the vital role that wealth management firms can play” in supporting clients, the firm noted, adding that this shift has also been fueled by the multi-trillion-dollar generational wealth transfer currently underway.

The start of 2026 confirms the resilience of the economic cycle despite geopolitical noise (Greenland, Iran, Venezuela) and political uncertainty (Fed independence, ICE, and a potential shutdown).

Rather than weakening, the baseline scenario is solidifying into a disinflationary expansion, closely resembling the 1995–1999 period. The delayed transmission of the Fed’s three rate cuts in Q4 2025 is beginning to show, just as the fiscal impulse (OBBBA, stimulus checks, tax refunds, and fiscal measures in Japan and Germany) shifts from being a drag to becoming a tailwind for cyclical activity.

Monetary policy: Powell relies on price dynamics

The Fed’s first meeting of 2026 was widely anticipated by markets. Powell delivered a more constructive outlook on growth and the labor market. While his assessment could be read as slightly hawkish, the overall tone was dovish. The focus of his remarks shifted from labor market conditions to price dynamics.

Powell indicated that the recent inflation overshoot is largely due to tariffs, which added up to half a percentage point to the cost of living. Without them, core PCE would already be just above 2%.

The message was clear: the bias is toward future rate cuts, although the bar for action remains high. Current conditions support holding rates steady for now, with markets no longer expecting a cut before June.

Fed succession: risk of a hawkish shift

On Friday, Kevin Warsh was named as Powell’s successor. A former Fed governor (2006–2011), Warsh is known for his critical stance on expansionary monetary policy. He has opposed QE programs beyond the initial post-subprime round, arguing that they distort markets, fuel inflation, and politicize the Fed.

His conservative approach and preference for orthodox monetary policy—emphasizing price discipline, a leaner balance sheet, and limited intervention—have raised concerns among investors. He has even questioned recent decisions such as the 50 basis point cut in September, which he views as politically motivated. His appointment could strain the current balance between growth and financial stability and may strengthen the dollar.

Inflation, productivity, and dollar dynamics

The disinflationary trend continues. Productivity growth is outpacing GDP, easing wage pressures. Oil prices are supportive, and rents are moderating, while the impact of tariffs on the CPI is expected to fade in the coming months.

Despite this favorable macroeconomic backdrop, the recent decline in the dollar, coinciding with a rally in real assets such as gold, silver, and copper, appears to reflect a narrative of eroding monetary credibility rather than underlying fundamentals.

Treasury Secretary Scott Bessent publicly defended a “strong dollar” policy, which helped stabilize the EUR/USD exchange rate after a technical oversold condition. However, the interest rate differential between the United States and the Eurozone suggests that a political risk premium is weighing on the pair, bringing it closer to April 2025 levels.

Earnings and Market Sentiment: Software in the Spotlight

The earnings season for the software sector reveals a technical capitulation. Companies like MSFT, NOW, and SAP have seen significant declines—not due to poor results, but rather their inability to justify previously high valuations. Adding to the pressure are concerns that AI solutions such as Anthropic Cowork could disintermediate major SaaS providers, threatening the traditional per-user licensing model.

The sector is clearly oversold. However, sentiment and technical damage will take time to recover. Key indicators to watch include upcoming data on Net Revenue Retention (NRR), cRPO, and company guidance. The market is looking for signs that renewals and workflow organization continue to hold up, and that AI has not yet had a structurally negative impact. Workday’s earnings on February 25 could be the catalyst to shift this narrative.

Circularity in the AI Ecosystem: Are Funding Rounds Inflated?

Another source of concern comes from the funding side. Reports of a potential $100 billion round for OpenAI, allegedly backed by its own partners (Nvidia, Amazon), have reignited fears over excessive circularity in the AI ecosystem. The perception that capital circulates within a closed loop of beneficiaries undermines the credibility of projected growth models.

AI Investment: Persistence and Barriers

Despite these concerns, AI investment shows no signs of slowing. The focus has shifted toward closed models with access to user data and reasoning capabilities—elements that could create durable barriers to entry.

While the market now demands tangible results, the disruptive potential and monetization opportunities continue to justify capital deployment. In 2026, AI-related CapEx will remain a key driver of corporate growth.

In conclusion, despite volatility and political risks, the macroeconomic backdrop remains constructive. The combination of robust growth, disinflation, and monetary prudence supports risk exposure. However, sector rotation, the evolving AI narrative, and the interpretation of post-Powell monetary policy will be critical to tactical portfolio construction in the first half of 2026. In the short term, there are also technical signals worth monitoring closely.

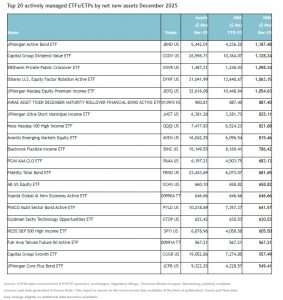

Global assets in actively managed ETFs reached a new all-time high of $1.92 trillion at the end of December, surpassing the previous record of $1.86 trillion set in November 2025. This means that, in 2025, assets grew by 64.5%, rising from $1.17 trillion at the end of 2024 to $1.92 trillion.

According to ETFGI’s analysis of the data, “during December, the global actively managed ETF industry recorded net inflows of $56.23 billion, bringing total net inflows for 2025 to a record $637.47 billion.” This flow activity was driven by globally listed, actively managed equity ETFs, which saw net inflows of $33.31 billion. “This brought total inflows for the year to $361.33 billion, significantly higher than the $211.34 billion accumulated in 2024,” they noted.

Actively managed fixed income ETFs also saw strong demand, with $18.56 billion in inflows in December and $237.93 billion year-to-date, well above the $139.69 billion recorded in 2024.

They note that “the substantial inflows can be attributed to the 20 top active ETFs by new net assets, which collectively gathered $15.89 billion during December.” Specifically, the JPMorgan Active Bond ETF (JBND US) attracted $1.19 billion, marking the largest individual net inflow.

The Financial & International Business Association (FIBA) announced the composition of its Board of Directors for 2026, bringing together top-level executives from international banking, law firms, compliance, fintech, cross-border payments, and businesses connected to digital assets. The new board reflects the diversity of the global financial ecosystem and the growing intersection between traditional banking and emerging financial service verticals.

The Chair of the 2026 Board will be Pablo Vallejo, General Manager of Banco Pichincha Miami Agency, who will assume leadership of the board as FIBA’s global agenda continues to expand. Vallejo succeeds Mónica Vázquez, who will remain involved as Immediate Past Chair.

“FIBA’s strength comes from the diversity and expertise of the community we bring together,” said David Schwartz, President and CEO of FIBA. “Our board of directors reflects the highest level of industry leadership and reinforces our commitment to providing exceptional education, meaningful networking opportunities, and industry-leading events. Among them is the FIBA Anti-Money Laundering (AML) Conference, one of the Association’s flagship events, which brings together the most respected voices in the industry for professionals navigating today’s evolving financial landscape,” he added.

“As Chair, I am honored to work alongside an exceptional group of professionals who share a deep commitment to excellence and collaboration,” said Pablo Vallejo, Chair of the FIBA Board of Directors 2026 and General Manager of Banco Pichincha Miami Agency. “FIBA has become a trusted platform for the financial community to learn, connect, and lead, and we will continue to elevate the quality of the Association’s education, member experience, and global industry offerings,” he added.

Headquartered in Miami, FIBA has established itself as a key meeting point for the international financial community, with a focus on regulation, compliance, AML, payments, and cross-border banking. Through its annual event agenda and Education Academy, the Association plays an important role in professional development, offering globally recognized certifications in partnership with Florida International University (FIU).

Looking ahead to 2026, FIBA will continue expanding its reach with a community that already includes more than 110 member organizations and over 10,800 certified professionals worldwide.

2026 FIBA Board Leadership:

Pablo Vallejo (Banco Pichincha) — Chair

Mónica Vázquez — Immediate Past Chair

Luis Navas (Insigneo Securities, LLC) — Chair-Elect

Susana Sierra (BH Compliance) — Vice Chair

Guillermo Benites (UDT) — Vice Chair

Harry Cupp (Sunwest Bank) — Vice Chair

Marina Olman (Greenberg Traurig) — Vice Chair

Wayne Shah (Wells Fargo) — Treasurer

Peter Rahaghi (Shutts & Bowen) — General Counsel

Teresa Foxx — Past Chair Representative

New 2026 Board of Directors:

The new board is rounded out by executives from financial institutions, law firms, and financial services companies with a strong regional and international presence:

Amerant — Shalako Weiner

Athena Bitcoin — Carlos Carreño

BANESCO — Norma Sabo

Banco Azteca — Alberto Bringas

Banco de Bogotá — Alfonso Garcia

Banco Popular Dominicano — Edward Baldera

Banco Santander International — Alfredo Aguila

Bradesco — Dulce Galindo

Diaz Reus — Javier Coronado

Facebank — Bernardo Velutini

Helm Bank — Mark Crisp

Holland & Knight — Andy Fernandez

Itaú — Erico Narchi

JPMorgan — Vinicius Furtado

Kaufman Rossin — Heidy Duarte

Republic Bank — Kimberly Erriah-Ali

SunState Bank — Fabricio Macastropa

TD Bank — Alexis Flores

Terrabank — Antonio Uribe

Truist — Luis Arango

U.S. Century Bank — Maricarmen Logrono

Winston & Strawn — Carl Fornaris

A growing association

FIBA emphasizes that the composition of the 2026 board reflects a phase of consolidation and growth, in a context where financial regulation, financial crime prevention, digital payments, and digital assets are gaining importance on the global agenda.

The association will continue to strengthen its role as a leading platform for international banking and compliance, supporting the evolution of the financial system in the United States and Latin America.

In the past twelve months, Japan has been responsible for some market volatility, something we are not accustomed to. A sign of this has been the recent sharp bond sell-off, which drove yields to record levels and attracted media attention. The combination of a weak yen, the rebound in long-term yields, the fiscal challenges that need to be addressed, and the Bank of Japan’s (BoJ) monetary policy normalization process are part of the elements behind these movements.

To this is added the fact that, over the weekend, the country will hold early elections, which were called earlier this year by Sanae Takaishi, Prime Minister and leader of the Liberal Democratic Party of Japan (LDP).

“This move by Takaishi aims to assert control over her own party and coalition, in order to implement her multi-year reflation strategy. The markets rightly fear that giving her more political capital means more fiscal deficits and inflationary pressures, hence the massive sell-off in the bond market and the jump in stocks. The yen reflects the fear that the Bank of Japan may be hindered by the executive from normalizing real interest rates quickly enough to contain inflationary pressures,” explains Raphael Gallardo, Chief Economist at Carmignac.

For now, the current expansive fiscal policy and uncertainty on the political front highlight the structural obstacles the country is facing, including negative real yields and an already high level of debt.

“The new prime minister wants to take advantage of her very high current popularity rating to win seats for the Liberal Democratic Party and regain control of the Lower House against a Democratic Party for the People, the opposition party, which is unprepared,” adds Martin Schulz, Head of the International Equity Group at Federated Hermes.

Moreover, stocks reacted positively, boosting the “Takaichi Trade,” which includes the aerospace and defense, nuclear, cyber, and domestic exposure sectors.

“Although we have observed some yen depreciation, the restrictions on Chinese exports and the increase in inflationary pressures could negatively affect the confidence of Japanese households and businesses in the short term, so ensuring internal political unity in the long term could help Japan’s negotiating position internationally, especially with the upcoming summit between Japan and the United States. Among the risks we are observing are internal political gridlock and a further unwanted depreciation of the yen,” notes Schulz.

Implication for the Markets

To understand why this weekend’s Japanese election is important, it is necessary to reflect on the role Japan plays in the markets. First, after several decades, it seems to be breaking out of economic stagnation. “Japanese equity valuations have been particularly affected by the persistent reflation scenario. In these environments, the relationship between interest rates and price-to-earnings (P/E) ratios tends to invert. This has caused the P/E ratios of Japanese companies to barely exceed 17 times over the past twenty years, compared to the nearly 20-times average over rolling 10-year periods recorded by U.S. equities,” explains Noriko Chen, Portfolio Manager at Capital Group.

Secondly, it should be remembered that Japan plays a significant role as a “major financier” in recent years through the large carry trade that many have taken advantage of as a technical strategy, and upon which much of today’s leverage has been built.

“By keeping interest rates at zero or even negative levels, the Bank of Japan allowed a large amount of trillions of dollars to flow into risk assets around the world, especially the United States. Today, that cycle appears to be ending with the normalization of monetary policy, which is forcing the unwinding of massive positions,” states Laura Torres, Chief Investment Officer at IMB Capital Quants.

In view of the early elections this weekend, Ray Sharma-Ong, Deputy Global Head of Bespoke Multi-Asset Solutions at Aberdeen Investments, explains that if the Liberal Democratic Party (LDP) were to secure a majority and move forward with its fiscal agenda, several macroeconomic repercussions could be expected in the markets.

“Growth and aggregate demand will increase, driven by considerable fiscal stimulus and targeted investment in strategic sectors such as defense and energy. In addition, inflation expectations and Japanese government bond yields will rise, reflecting the market’s anticipation of a larger fiscal deficit, increased public spending, and greater uncertainty regarding the long-term fiscal path. And finally, the Japanese yen will weaken, as markets price in a weaker fiscal position, a larger fiscal deficit, and the possibility of a slower consolidation of public finances,” argues Sharma-Ong.

Although all eyes are on the record highs gold is setting, the truth is that another precious metal is experiencing a true rally: silver. It posted a spectacular year-end surge that has continued into the early weeks of 2026. In fact, in 2025, the metal appreciated by nearly 150%, clearly outperforming gold.

So far, gold’s current bullish trend has been supported by falling real interest rates, a weaker dollar, and market concern over the implications of rising U.S. public debt levels, the cost of servicing that debt, and the impact on U.S. Treasury bonds. But what factors are driving silver’s performance?

According to Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, the silver market has recorded a structural supply deficit for five consecutive years. “However, this imbalance hadn’t triggered a significant price reaction until 2025, when the uptrend accelerated and took on a virtually parabolic pattern toward the end of the year,” he notes. Wewel attributes this sharp upward movement, which even surpassed the absolute price increases seen ahead of the peaks in 1980 and 2011, to the combination of several factors:

Decline in U.S. interest rate expectations: In the second half of 2025, the market began to focus on the appointment of a successor to Federal Reserve Chair Jerome Powell. “The expectation of a more accommodative Fed, which could implement several rate cuts in 2026, has weakened the U.S. dollar and increased the appeal of non-interest-bearing assets such as silver and gold,” he notes.

Inclusion on the U.S. critical minerals list: In early November 2025, the U.S. Department of the Interior added silver to its list of critical minerals. Thanks to its high electrical conductivity, this material is essential for manufacturing high-performance chips and for the development of infrastructure linked to artificial intelligence. Its inclusion on the list, along with fears of potential U.S. tariffs on silver, alerted the market to potential supply risks and prompted an advance in silver shipments to the U.S. As a result, the London market recorded physical outflows of the metal, reducing local reserves.

Chinese export restrictions: Since the beginning of the year, China has implemented stricter controls on silver exports. This decision is part of a broader strategy to secure access to critical minerals and limits silver exports during 2026 and 2027 exclusively to government-approved companies.

Growing relevance as a store of value: Finally, silver is gaining prominence as a monetary metal. Compared to other commodities, its storage cost is low, and it has a long historical track record as a key material in coinage. The high per-unit cost of physical gold purchases is excluding many low- and middle-income buyers in emerging markets, positioning silver as a more “affordable” alternative to gold in these countries. As a result, household demand has increased in India and China. In Shanghai, buyers are paying a premium of around $10 per ounce over the London market price.

“The sharp surge in the price of silver has brought the gold/silver ratio to around 50. Given that this indicator fell to levels near 40 in previous bullish cycles, silver could significantly surpass $100 per ounce in the current cycle. In principle, our positive view on gold supports this scenario, and speculative positions do not appear excessive,” states Wewel.

However, he warns that although the physical supply deficit should keep silver prices elevated in the short term, the metal tends to experience much deeper corrections than gold after a prolonged rally due to its higher volatility. “Since momentum is losing strength, the risk-return balance now seems less attractive for silver. This also implies that, from these levels, it should be difficult for silver to continue outperforming gold,” he concludes.

The possible nomination of Rick Rieder, Chief Investment Officer of Global Fixed Income at BlackRock, as the next chair of the U.S. Federal Reserve has reopened debate among investors, economists, and monetary policy analysts. At stake is not just a name, but the leadership profile the Fed needs at a time when its traditional policy framework is under scrutiny.

With Jerome Powell’s term coming to an end, Rieder has emerged as one of the most visible candidates, despite being clearly outside the central banking establishment. According to an analysis by EFG International, his potential appointment would be historic: Rieder would be the first Fed chair in decades without prior experience at the central bank or academic training as an economist.

An Outsider Versus the Traditional Model

In a note signed by Stefan Gerlach, Chief Economist at EFG, the bank highlights that while Powell is also not a career economist, he had a long track record within the Federal Reserve before assuming the chair. Rieder, by contrast, comes exclusively from the world of financial markets, having built his career at firms like Lehman Brothers and more recently, since 2009, according to his LinkedIn profile, at BlackRock, where he oversees approximately $2.7 trillion in global fixed income assets.

This unconventional background is precisely the heart of the controversy. For Bob Smith, President & Co-Chief Investment Officer at Sage Advisory, the contrast between “insider” candidates, such as Christopher Waller or former governor Kevin Warsh, and a clearly external figure like Rieder raises a key question: is institutional credibility more important today, or direct market experience?

One of the main concerns raised by both EFG and Sage Advisory is the reputational risk associated with the Fed’s independence. The fact that Rieder comes from the world’s largest asset manager could fuel perceptions of a central bank more closely aligned with private-sector interests, at a time when its autonomy has already been a subject of political and media debate.

EFG’s Chief Economist recalls that history offers discouraging precedents when the Fed has been led by figures lacking a strong technical foundation in monetary policy, citing the case of G. William Miller in the late 1970s, whose tenure coincided with a decline in the Fed’s credibility in the face of inflation.

Sage Advisory, meanwhile, notes that the Fed’s institutional design, with collegial decision-making within the FOMC and well-defined operating frameworks, serves as a natural check on any attempt at individual influence, although it acknowledges that market perception plays a central role.

Diego Albuja, market analyst at ATFX LATAM, points out that “Rieder’s profile is technically solid. His decades-long career in fixed income markets has allowed him to closely analyze inflation, interest rates, liquidity, and credit, precisely the core pillars on which monetary policy operates. This would give him a clear advantage in interpreting how markets react to each Fed decision and how those decisions are transmitted to the real economy.”

However, Albuja clarifies, unlike other chairs, Rieder does not come from academia or the internal structure of the central bank. “This means his main challenge wouldn’t be economic analysis itself, but rather managing institutional credibility, communicating with the market, and sustaining public confidence in an increasingly sensitive political and financial environment.”

“The fixed income investment chief at BlackRock, who has never held political office, would bring a perspective grounded in granular, data-driven corporate analysis, rather than in economic theories and models,” wrote Krishna Guha, head of global policy and central bank strategy at Evercore ISI, in a note quoted by CNBC. “Markets are likely to embrace Rieder as one of their own,” he added.

A Shift in the Approach to Monetary Policy?

From a macroeconomic perspective, analyses agree that Rieder would likely be seen as a chair more attuned to current financial conditions than to retrospective analyses of inflation and employment. EFG notes that this approach could translate into quicker responses to market changes, though it would also pose a challenge for maintaining coherence and predictability in monetary policy.

In that context, voices like that of macro analyst Nic Puckrin, co-founder of Coin Bureau, suggest that Rieder could soften the tone of the Fed’s communication and give more weight to financial stress indicators, without necessarily signaling an aggressive turn toward rate cuts.

ATFX LATAM’s market analyst believes that Rick Rieder has the technical capacity and market experience to lead the Federal Reserve, “but his true test would lie in preserving the central bank’s independence and credibility. If successful, he could usher in a more pragmatic era in monetary policy; if not, the cost could show up in greater volatility and reduced effectiveness of the Fed’s decisions.”

“Rieder is an unconventional candidate,” notes Puckrin, “but maybe that’s exactly what’s needed at a time when the market is questioning how effective traditional policy tools really are in fulfilling the Fed’s dual mandate.”

Beyond the candidate himself, the consensus among the sources cited is that the discussion around Rieder reflects a deeper tension within the U.S. financial system: the need to adapt monetary policy to a more complex environment, without eroding the central bank’s credibility or independence.

Photo courtesyPresentation of the alliance between Insigneo and Karta in Punta del Este

Insigneo announced in a statement a strategic alliance with Karta to launch a premium credit card for globally mobile, high-net-worth clients with assets in the U.S.

“Thanks to this alliance, Insigneo becomes the first wealth management firm to secure exclusive rights to a co-branded credit card with Karta, reinforcing its leadership in delivering innovative solutions for international clients,” the statement said.

The new Insigneo x Karta card addresses a long-standing gap in the market: international high-net-worth clients with assets in the U.S. have historically been underserved by traditional credit card offerings, often relegated to low-tier debit products with minimal benefits and inadequate service.

“Our clients don’t see limits in their financial lives, and their financial tools shouldn’t have them either,” said Raúl Henríquez, chairman of the board and CEO of Insigneo.

“This alliance with Karta allows us to complement our wealth management platform with a solution tailored to the sophistication and global lifestyle of our clients. It’s not just about managing wealth, but about empowering its daily use, aanywhere in the world,” he added.

The Insigneo x Karta credit card offers premium features designed for this demographic. Cardholders enjoy seamless spending across currencies and borders, with no foreign transaction fees, while Priority Pass Select provides complimentary access to more than 1,300 airport lounges worldwide.

The KARTA Points rewards program offers flexible redemption options with major airlines, hotels, and premium partners. Upon approval, clients receive instant digital access, with immediate availability on Apple Pay and Google Pay. The 24/7 multilingual customer service via WhatsApp ensures personalized assistance in the client’s preferred language, while the fast, fully digital onboarding process delivers a streamlined approval experience designed to meet modern expectations.

“The clients Insigneo serves are exactly the ones we created Karta for,” said Freddy Juez, CEO and founder of Karta.

“They expect a premium experience in their investments; now they’ll have that same quality of experience when they spend, travel, and seek assistance anywhere in the world. This alliance validates our vision and brings it to a community that truly values innovation and excellence in service,” Freddy Juez added.

This partnership was officially presented in early January 2026 at Insigneo’s Sunset event in Punta del Este, Uruguay.

Insigneo is a wealth management firm that provides services and technologies empowering investment professionals. Insigneo serves more than 300 investment professionals and 68 institutional firms supporting over 32,000 clients.

Karta is a next-generation financial services company focused on serving high-net-worth individuals (HNWIs) and globally mobile clients who do not reside in the U.S. and whose assets are held at U.S. banking and brokerage institutions.