Momentum to overhaul the AFPspensionsystems in the Andes has stalled amid dwindling public support for the ruling parties in Chile, Colombia, and Peru, fortifying opportunities for external managers. Asset managers with private equity or other alternatives will find opportunity to capitalize on pension fund appetite for long-term, low-volatility products with low correlation to existing benchmarks, according to Cerulli’s report, Latin American Distribution Dynamics 2023: Latin America’s Leftward Tilt and Its Impact on Retail and Institutional Asset Gathering.

According to the research, produced in conjunction with Cerulli’s research partner for Latin America, Latin Asset Management, Chilean AFP holdings of cross-border funds and ETFs total $73 billion, Colombian $40 billion, and Peruvian at $8.6 billion.

“Despite calls by recently elected left-leaning populists in Chile, Colombia, and Peru to limit the participation of privately owned managers in the pension sphere, broad-based drastic reforms are being rejected in the region”, the report added.

“There’s consensus in the Andes that the region’s pensionsystems need to be updated in order to improve payouts for retirees, as well as include others who did not contribute to the system during their working years, but there’s little appetite for eliminating the AFPs or returning pensionsystems to state control,” states Thomas Ciampi, director of Latin Asset Management and author of the report.

While government-mandated emergency withdrawals in Chile and Peru dissuaded AFPs from locking up assets in long-term vehicles such as a real estate development or infrastructure projects, they have since increasingly allocated to alternatives as the response to COVID-19 has ended.

Including Mexican Afores, alternatives penetration in the AFP/Afore pension fund segment jumped to $71 billion in mid-2023, from $46 billion at the close of 2020. Excluding Mexico, the increase was more moderate—to $36 billion from $27 billion over the same period. “Peruvian and Mexican private-pension managers are already allocating a larger percentage of their portfolios to alternatives than to cross-border mutual funds and ETFs,” remarks Ciampi.

External managers have secured their place in the AFP system for now, but the challenges they face in the pension segment—attractive yields on local, onshore fixed-income securities, and the uncertainty surrounding the future of the AFP—will continue to loom. Managers that offer exposure to alternatives such as private debt, private equity, and real estate will be better positioned for mandate wins.

Citi has led a strategic investment round in Supra. Far Out Ventures and H20 Capital also participated in the financing round.

Supra is a Colombian fintech that enables cross-border payments and treasury solutions for small and medium-sized businesses (SMBs) that participate in import and export activities.

The new capital will enable the growth of Supra’s Colombian operations to fulfil its payment aggregator role in partnership with Foreign Exchange Market Intermediaries (IMC) and licensed Payment Service Providers.

Diego Santoyo, Head of Corporate Sales and Solutions for the Andean region at Citi, said: “Citi’s best-in-class cross-border payments and FX technology will help enable Supra’s operations and expansion in Colombia.”

“At Supra, we are developing cutting-edge cross-border payment solutions that provide value-added services to our clients as well as transaction speed and highly competitive rates. Our technology is one of the first in the country that complies with the regulations issued by the Colombian Central Bank for payment aggregators,” said Emilio Pardo, CEO and co-founder of Supra.

In Colombia, more than 40,000 companies participate in import and export commercial activities and the market for business-to-business cross border payments in 2022 was approx. $134 billion according to data from the Colombian Tax Authorities (DIAN).

The investment was led by Citi’s strategic investments arm, which invests in innovative fintech companies that are aligned to Citi’s core businesses.

“We believe Supra’s product, business model and collaboration with Citi will allow them to create competitive moats in the multi-billion-dollar import and export cross-border payments market in Colombia,” said Aldo Alvarez, Lead for LatAm Strategic Investments in Citi’s Markets business.

H.I.G. Capital announced that one of its affiliates has completed the acquisition of Mainline Information Systems, a leading IT solutions provider. Mainline’s management team, headed by CEO Jeff Dobbelaere, will continue to lead the Company.

Headquartered in Tallahassee, FL, and with revenues in excess of $1 billion, Mainline is a leading, diversified IT solutions provider serving the infrastructure needs of blue-chip enterprises. Founded in 1989, the Company designs and implements custom IT solutions for enterprises and provides associated professional and managed services. Mainline has leveraged its technical data center expertise, diverse partner network, and consultative customer-centric approach to become a leading provider of enterprise server, hybrid cloud, cyber storage, and network & security solutions.

“Over the past 30 years, Mainline has developed strong and enduring relationships by providing our customers with some of their most complex and mission critical infrastructure solutions. Mainline has become a clear industry leader and is incredibly well positioned to continue to drive business outcomes for our clients as the technology landscape evolves,” said Jeff Dobbelaere. “I am very excited to partner with H.I.G. and look forward to investing in the significant growth opportunities which can take the company to new heights.”

Aaron Tolson, Managing Director at H.I.G., commented, “Mainline’s technical expertise, its status as a trusted advisor for its customers, and the value it brings to its Original Equipment Manufacturer partners are unmatched in the IT industry. We have been very impressed by what Jeff, and the rest of the management team have built and look forward to helping the Company further accelerate its significant growth potential through organic initiatives and acquisitions.”

H.I.G. was advised by Guggenheim Securities LLC, UBS, and Latham & Watkins LLP. The Company was advised by Highlander Advisors and King & Spalding.

Photo courtesyRobert M. Almeida, Global Investment Strategist at MFS

The inflation ambush of 2022 ended a decades-long downward trajectory for interest rates. While rates may fall a bit as the effects of tight financial conditions weigh on aggregate demand and economic growth, we don’t believe the cost of capital going forward will resemble anything like the levels of recent years when central banks artificially set market prices via quantitative easing. Just as water ultimately finds its own level, in my opinion, interest rates will find their own, higher level.

As a result of higher capital costs, companies will find it challenging to meet investor expectations. In past notes, we have argued this is part of a large paradigm shift from high and easy-to-earn returns on capital to something lower and harder. While higher borrowing costs are the most notable change, they are not the only factor driving the paradigm shift. This note focuses on one of the other factors: a secular increase in capital expenditures and what this may mean to profits.

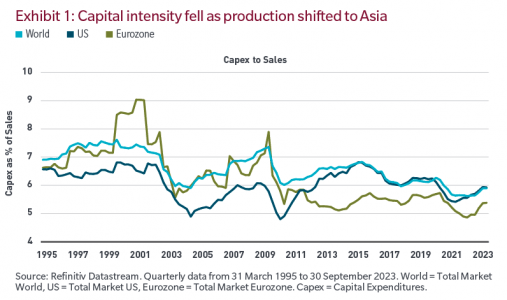

Falling capital intensity was the past

Globalization, in particular China’s emergence on the global scene in the mid-1990s as the low-cost manufacturer, was game changing. While it catapulted China from economic dormancy to the world’s second largest economy, its impact reached far beyond China as it allowed developed market companies to become de facto asset-light businesses by outsourcing their manufacturing to lower-cost locales.

Companies no longer needed to rebuild tangible capital because China, and Asia more broadly, did it for them. As a result, capital intensity (capital assets compared with revenues) steadily declined, as depicted below.

This matters because there is a long-term and inverse relationship between capital spending and return on capital. When capital intensity falls, all else equal, returns rise because less capital was deployed. Tangentially, the outsourcing of production also pressured operating expenses due to reduced need for human capital.

The combination of financial leverage by way of artificially-suppressed rates and falling fixed investment drove historic returns for shareholders. But that came at the expense of savers and labor, and exacerbated income inequality. Both trends have ended.

Rising capital intensity is the future

The pandemic, followed by the Russia-Ukraine war, exposed the risk of not having goods available for sale when customers want them. To make a car requires thousands of parts, but it only takes one missing part to halt production. For companies, having a product available on the shelf at a lower margin has become more important than an empty shelf at peak margin. While the building of semiconductor and electric vehicle factories has captured the bulk of the media attention, reshoring and added capacity has extended across electrical goods, chemicals, medical equipment and more. Companies outside of technology and the automotive industry are spending money too.

A brewing cold war between the US and China, and more recently a war in the Middle East, have made this risk even more acute. While the magnitude is uncertain, we can expect deglobalization to divert capital — which in recent years was returned to shareholders via dividends, stock buybacks and acquisitions — to fixed investment. That will likely become a drag on future returns.

Why this matters

While in the short run, trading impulses, such as monthly labor or inflation data, drive asset prices, in the long term, it’s return on capital that matters. Looking ahead, the shift from supply chain efficiency to resiliency will mean that companies that are short of tangible capital will need to make capital investments that will negatively impact returns.

Much like investors, companies are capital allocators. Their stock and bond prices are scorecards, voted on by the market. We’re exiting an environment where the consequences for bad decision-making were blunted by the tailwinds of artificially suppressed rates and globalization. And we’re entering one with a reduced margin for error.

Returns may prove resilient for companies led by great decision makers who understood that COVID-era cheap capital and stretched supply chains were unsustainable. However, companies with high capital needs and elevated debt burdens may disappoint. Since returns drive financial asset prices, this should also bring a paradigm shift in the importance of security selection and active management.

KKR, a global investment firm, has marked the beginning of 2024 with significant promotions within its ranks. The firm announced the elevation of 8 of its members to Partner status and 33 to Managing Director positions, effective from January 1, 2024. This move underlines KKR’s commitment to recognizing and nurturing talent as part of its growth and evolution strategy.

Joe BaeandScott Nuttall, Co-Chief Executive Officers at KKR, expressed their pride in this new chapter, highlighting the company’s nearly five-decade legacy of strengthening businesses and delivering consistent results to investors. They emphasized the importance of the firm’s culture and people, acknowledging the newly promoted individuals as embodiments of KKR’s values and dedication to client and portfolio company support.

The new Partners at KKR, recognized for their exemplary contributions, include Anne Arlinghaus from Capstone in New York, and James Gordon from the Infrastructure sector in London. Joining them are Franziska Kayser and Varun Khanna, both from London, with expertise in Private Equity and Credit & Markets, respectively. Keith Kim from Seoul, specializing in Infrastructure, and Prashant Kumar from Singapore, focusing on Private Equity, are also among the newly elevated. Completing the list of Partners are George Mueller from Credit & Markets in New York and Kugan Sathiyanandarajah from Health Care Strategic Growth in London.

In addition to the new Partners, KKR has also promoted a substantial number of professionals to the role of Managing Director. This diverse group brings expertise from various sectors and global locations, reflecting the firm’s wide-reaching influence. Among them are Mohamed Attar from Global Client Solutions in Dubai, Jonathan Bersch in Corporate Services and Real Estate from New York, and Rami Bibi from Global Impact in London. Also elevated are Ben Brudney, Zac Burke, and Daniele Candela, each with a strong background in Real Estate Equity, Global Macro, Balance Sheet & Risk, and Credit & Markets, respectively, all based in New York or London.

The promotions also span across various global locations such as Dublin, Houston, Tokyo, Sydney, San Francisco, and Mumbai, with professionals like Myles Carey, Todd Falk, Andrew Jennings, Gene Kolodin, Kensuke Kudo, and many others being recognized for their significant contributions to KKR’s diverse sectors including Infrastructure, Technology, Finance, and Real Estate.

This strategic move by KKR not only strengthens its global leadership but also signifies the firm’s dedication to fostering talent and expertise within its ranks. The promotions are a testament to the individual achievements of these professionals and KKR’s commitment to excellence in the investment sector. As KKR continues to navigate the complex global investment landscape, these leaders are poised to play pivotal roles in the firm’s ongoing success and growth.

Cerulli projections indicate that total passive mutual fund and exchange-traded fund (ETF) assets will surpass total active mutual fund and ETF assets by early 2024, according to U.S. Product Development 2023: Resource Reallocation Through Product Rationalization.

However, the flight toward passive may be slowing, as active management seeks ground in vehicles other than the mutual fund.

Approximately 10 years ago, passive mutual funds and ETFs were neck and neck in the asset race against each other, while they collectively held one-quarter of the marketshare of total mutual fund and ETF assets. Since then, passive assets in the two vehicles have stolen one to three percentage points of marketshare from actively managed assets each year, reaching 49% of marketshare as of the end of 2Q 2023, according Morningstar.

However, the gains in passive marketshare may not represent the full story. Passive management primarily exists only within mutual funds, ETFs, and collective investment trusts (CITs). According to the research, looking across mutual funds, ETFs, CITs, money markets, retail separately managed accounts (SMAs), and alternative structures, active management still holds 70% of marketshare as of the end of 2022 and the pace of outflows has slowed in recent years.

As the industry looks into the future, questions persist regarding how much marketshare passively managed assets will eventually control, and whether the trend toward passively managed assets will slow based on changing economic conditions and investor preferences. “Time will tell where the critical point exists upon which passive investing becomes a risk, where the mechanism of blindly buying securities based on their prices rather than their cash flow could blow back,” says Matt Apkarian, associate director.

Performance aside, the drivers of demand for active and passive are based on attitudes toward management styles, and the belief or lack of belief that active managers can outperform in various market environments or over full market cycles. Geopolitical shock (73%) and recession (69%) are the scenarios most believed to increase demand for active management, while a sustained equity bull market (50%) is the scenario most believed to decrease demand for active management.

“Expansion of strategies and allocations outside of the largest U.S.-based asset classes can stand to give support to active management, as assets appear to be on a path to continue moving into passively managed products within the portfolio core of U.S. equity and fixed income,” adds Apkarian.

“Asset managers must adapt to changing demand from financial advisors and end-investors to remain relevant in the industry. Increased focus on defined outcome products with better downside capture can serve to be the tool that meets advisor needs when attempting to provide their clients with a smooth ride toward their financial goals,” he concludes.

Insigneo has successfully completed the acquisition of the Latin American consumer brokerage and advisory accounts of PNC Investments, PNC Managed Account Solutions, and PNC Bank.

This strategic move, initially announced on August 22, 2023, represents an important milestone for Insigneo, as it expands its Mexican client base as well as its geographic footprint by establishing new offices in Texas.

This transaction underscores Insigneo’s commitment to international wealth management.

Insigneo has been gaining significant ground by emphasizing client service, leveraging state-of-the-art technology, and focusing on continuous innovation. Clients who were part of PNC’s Latin America brokerage and advisory business will now enjoy all the benefits of Insigneo’s focused global wealth management approach and international capabilities.

Raul Henriquez, Chairman, and CEO of Insigneo Financial Group, expressed his enthusiasm about the successful completion of the transaction, stating, “The acquisition of PNC’s Latin American brokerage and advisory business underscores Insigneo’s commitment to global wealth management. We recognize the importance and relevance of the Mexican market and see this as a strategic move to immediately establish a relevant presence in that market, while positioning Insigneo to harness new opportunities in the region.”

The closing of this transaction solidifies Insigneo’s leadership in the global wealth management industry. The company remains focused on its alternative business model while driving growth through successful strategic M&A activities, a commitment further underscored by the recent appointment of Carlos Mejia as Head of Mergers and Acquisitions.

Javier Rivero, President, and COO of Insigneo Securities and Insigneo International Financial Services, added, “Both parties worked diligently and efficiently during this time focused on a smooth transition. Insigneo welcomes all incoming employees, investment professionals, and their clients to our growing firm.”

In an increasingly overcrowded market, model providers are vying for shelf space. To succeed, providers will need to consider how their products are differentiated to fit into platform product lineups and whether they can deliver solutions at scale, according to The Cerulli Report—U.S. Asset Allocation Model Portfolios 2023.

81% of model providers indicate the most important criteria for selecting platforms and model marketplaces through which to distribute models are the placement and visibility for their strategies on the platform.

Given that overcrowding is a major issue, strategy placement and visibility are key factors in the success of a model on a platform. However, limited shelf space is overwhelmingly the most substantial barrier to placing models on distribution platforms, according to 48% of model providers.

“Models can be viewed as highly commoditized, particularly in target-risk/target-allocation products,” says Matt Apkarian, associate director. “In general, home offices do not like hosting substantially similar products on platforms and take only as many products on the platform as they can find gaps in the lineup needed to meet the portfolio objectives of their clients.

This creates extreme competition between model suites and a need for differentiation to achieve placement,” he adds.

At the same time, model providers selecting platforms must consider whether have they have the resources to deliver solutions at scale. Ongoing management of models on platforms can be an onerous process for model providers, as processes for model updates across platforms lack uniformity and create operational overhead for providers. For instance, the task of updating tickers and weights for each model is one of the top pain points listed by several model providers that discussed difficulties in working with various platforms.

Cerulli recommends model providers think strategically about the platforms they are considering and whether their solutions are aligned with the needs of advisors. “Even with proper placement, models do not sell themselves, so distribution efforts are essential to grow model assets under management,” says Apkarian. “Model providers should prioritize platforms preferred by advisors as a top priority for product placement.”

U.S. equities were lower in October, with the S&P 500 and Nasdaq dropping more than 10% from their July peaks. While the S&P is still up 10.7% year-to-date, nearly all the return has been driven by the so-called “Magnificent Seven” (NVIDIA, Apple, Microsoft, Meta, Amazon, Tesla, and Alphabet) amid enthusiasm for the prospects for Artificial Intelligence with mega-cap tech stocks being the main perceived beneficiaries.

Despite the encouraging reports of robust retail sales and a strong Q3 GDP growth, the relentless surge in Treasury yields was a notable headwind to equities during the month. Stocks now have more competition as higher returns for risk-free assets make stocks less appealing in the short term as an investment option. This market dynamic reflects the market’s growing acceptance of a more prolonged period of hawkish policies from the Federal Reserve. On November 1, the Federal Reserve made the decision to hold interest rates steady. This determination came against the backdrop of a flourishing economy and a robust labor market. It marked the second consecutive meeting in which the Fed opted to keep rates unchanged, following a series of 11 rate hikes, including four in 2023.

Headline news in Merger Arbitrage was primarily driven by the VMware/Broadcom deal, where the spread has widened as the companies await final signoff by Chinese antitrust regulator, SAMR. Spreads on other deals were volatile and generally wider in sympathy with VMware, as typically happens when there is volatility in widely held arbitrage positions. Deals such as Albertsons, PNM Resources, Capri Holdings, Sovos Brands and Amedisys were notably wider in October as well. Partially offsetting the wider spreads were deals that made significant regulatory progress in October, including Activision, Horizon Therapeutics, National Instrument and New Relic. We believe these mark-to-market declines will be recovered in the coming months as companies make continued progress towards completing their transactions.

The convertible market gave up some of the gains in October that we had seen earlier this year. Convertibles continue to outperform underlying equities in weak markets, but with over 40% of the market now fixed income alternatives, the move in interest rates has weighed on valuations. Market sentiment was quite negative this month as we waited for companies to report. Looking forward, we anticipate a majority of the negative interest rate impact has been priced into convertibles, and we are optimistic that low expectations from investors will set many companies up for positive performance.

Opinion article by Michael Gabelli, managing director at Gabelli & Partners

Portfolio management faces several complex challenges that require the constant attention of industry professionals. The 1st Annual Report of the Asset Securitization Sector, sponsored by FlexFunds, highlights the top 10 challenges facing portfolio managers when raising capital and acquiring clients.

Raising Capital and Acquiring Clients: A Competitive Battleground

Tightening regulations, which can increase costs and create barriers for new investors, is one of the first complications portfolio managers encounter. Intense competition to attract clients and capital adds to this challenge, especially when differentiation between financial products is minimal.

Lack of understanding on the part of investors and clients about investment strategies and financial products can generate fear and indecision, especially in environments of low returns or lack of liquidity.

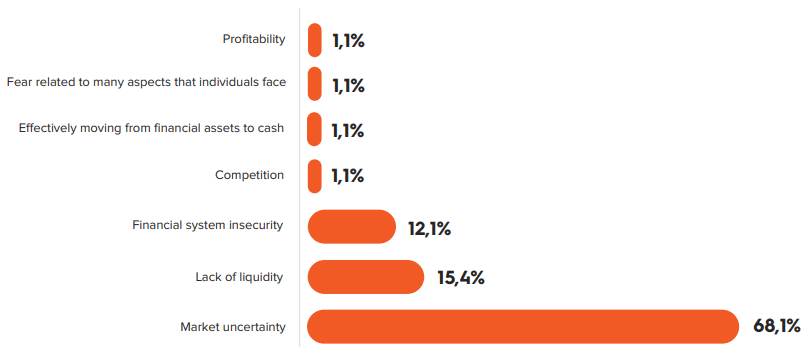

However, market uncertainty, arising from volatility or structural factors, stands out as the most problematic factor for acquisition.

FlexFunds’ report studies the main trends in asset management, which included the participation of more than 80 companies from 15 countries in LATAM, the United States, and Europe. This report reveals that 68.1% of participants consider uncertainty the most significant challenge, followed by lack of liquidity (15.4%) and financial system insecurity (12.1%). These factors accounted for 95.6% of the responses.

Market volatility undermines investor confidence and increases risk aversion, delaying investment decisions. Overcoming these challenges requires tactics that address uncertainty and improve client understanding of investment strategies.

Difficulties in Client Portfolio Management

According to the FlexFunds’ report, investment portfolio management faces several complex challenges, the top 10 of which stand out:

Client risk tolerance: Each client has a different risk tolerance, requiring careful balance in portfolio composition.

Market volatility: Financial markets are inherently volatile, requiring frequent adjustments to maintain portfolio balance.

Changes in economic conditions: Economic and market conditions impact asset returns, requiring adaptability in investment strategy.

Proper diversification: Achieving optimal diversification can be challenging, requiring in-depth analysis and specialized knowledge.

Asset selection and active management: Identifying strong asset investment strategies and actively managing the portfolio involves constant monitoring and informed decision-making.

Costs and fees: Balancing costs with the quality of services and results is essential to maintaining the client’s net return.

Effective communication: Clear and effective communication is crucial to understanding the client’s changing needs and ensuring trust over time.

Compliance and regulation: Keeping compliant with regulations and ethical standards is essential for asset managers.

Managing client emotions: Handling client emotions during volatility is crucial to avoid impulsive decisions.

Relative performance and expectations: Addressing client expectations and explaining relative performance is vital to maintaining trust.

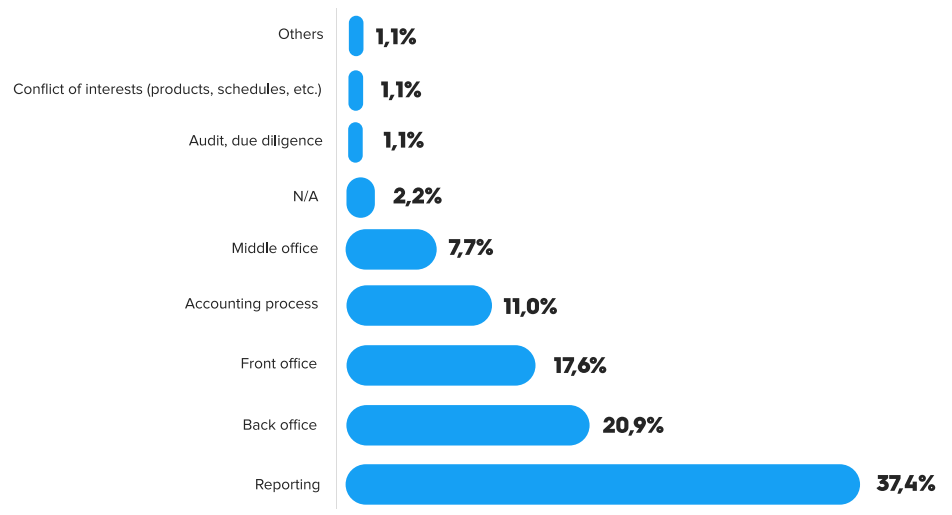

When industry professionals in more than 15 countries were asked, “What are the main difficulties you face in client portfolio management?” respondents identified reporting (37.4%), back-office (20.9%), front-office (17.6%), the accounting process (11%), and middle-office (7.7%) as the primary challenges in portfolio management.

Dive into a detailed analysis of the difficulties in portfolio management. From risk tolerance to emotional client management, FlexFunds’ 1st Annual Report of the Asset Securitization Sector reveals the daily complexities that portfolio managers face. Discover how industry leaders address market volatility, appropriate diversification, and regulatory challenges.

Download the full report to uncover innovative strategies, practical solutions, and exclusive insights on portfolio management in the competitive financial world 2024. Will the 60/40 model remain relevant? Which collective investment vehicles will be most utilized? What is the expected evolution of ETFs? What factors should be considered when building a portfolio? among others.