Santander Bank announced that it has closed a transaction with the Federal Deposit Insurance Corporation (FDIC) to participate in a joint venture that consists of a $9 billion portfolio of New York based multifamily real estate assets retained by the FDIC following the failure of Signature Bank.

The Bank acquired a 20 percent equity stake of the joint venture for $1.1 billion at an attractive basis and will service 100 percent of the assets in the portfolio.

“This transaction underscores our strength and scale, leveraging our considerable expertise in the sector,” said Ana Botín, Banco Santander executive chair. “We are a major participant in the U.S. multifamily space and this transaction plays to our strengths.”

The Bank has a $13.5 billion multifamily real estate portfolio, is a leading multifamily bank real estate lender in the United States and holds an Outstanding Community Reinvestment Act (“CRA”) rating.

“Santander US is a top-ten multifamily bank real estate servicer and lender and this transaction will leverage that industry expertise while also deepening our franchise in the New York metro market,” said Tim Wennes, Santander US country head and Santander Bank president and CEO.

The U.S. remains a strategic market for Banco Santander, as demonstrated by this transaction. The portfolio of loans in the joint venture consists of three pools of rent-controlled and rent-stabilized multifamily loans. The transaction will be accretive starting in 2024 and consume approximately two basis points of Santander Group CET, to be paid back within three years.

Santander was advised in this transaction by Wachtell, Lipton, Rosen & Katz, Davis Polk, and Chain Bridge Partners.

In the latest issue of The Cerulli Edge—U.S. Monthly Product Trends, a detailed analysis of product trends up to October 2023 is presented, focusing on mutual funds and exchange-traded funds (ETFs).

The report delves into the shifting advisor allocation to alternatives in the context of a rising rate environment, providing a comprehensive overview of current market dynamics.

As of the end of October, mutual fund assets were valued at $16.6 trillion, marking a significant decrease from the July 2023 peak of $18.2 trillion.

The month saw a 2.9% decline in mutual fund assets, primarily due to net negative flows amounting to $79.1 billion, translating into an organic growth rate of -0.5% for October. In a similar vein, ETF assets experienced a downturn amidst the fluctuating equity and fixed-income markets during October.

The total value of ETF assets fell by 2.4% to just under $7.0 trillion. However, this decrease was somewhat offset by positive net inflows totaling $30.4 billion throughout the month. The current rising rate environment poses challenges for advisor engagement with alternative investments, as it renders a variety of other exposures more appealing.

Nevertheless, the industry is set to maintain its momentum, propelled by significant advancements in product structures and a deepening understanding of alternatives among advisors. Over recent years, these aspects have seen considerable improvement, and many managers are actively promoting these exposures.

To navigate this landscape effectively, managers are advised to concentrate not only on distributing alternatives but also on ensuring transparent communication regarding the risks associated with the rate environment. Prioritizing the development and strategic positioning of product lines, rather than focusing solely on specific high-performing exposures (e.g., consultative sales processes), is likely to yield long-term benefits for asset managers.

What will 2024 bring? To answer this question, Pictet AM recently invited Luca Paolini, its chief strategist, to give his analysis to the firm’s Spanish clients. At the event, Gonzalo Rengifo, head of distribution for Iberia and Latam at Pictet Asset Management, summed up the firm’s main conviction: “We are entering a market cycle of some moderation, in which developed countries will continue to grow and emerging countries will grow more”.

Rengifo explained that in 2024 the disinflation process will continue, “if geopolitical events allow it”, although he warned that, at least in developed countries, that process will not be immaculate: “We believe that, from now on, every release of inflation data will entail volatility”. “Although interest rates may have peaked, the cuts may come later and be slower than expected by the market. Indeed, by 2024, we expect interest rates to be cut in both the eurozone and the US, but not aggressively. The Fed may cut them more than other central banks. In addition, the Bank of England, with its economy in recession, may cut rates earlier than expected,” he adds.

Third, Rengifo highlighted the importance of income as a new player in investments, offering returns of 3% to 5% across asset classes: “The good news is that, for the first time in a long time, we expect bonds, equities and cash to generate positive real returns. The new normal is lower expected returns in bonds and equities, lower correlations, a return to fundamentals and lower growth. Inflation will slow, but not enough.”

Inflation: the last mile will be the hardest one

During his speech, Paolini insisted on the need to put the current market situation into perspective. Thus, although he notes that the market is currently dominated by pessimism and bearishness, he appeals to realism: “We believe that next year’s returns will not be fantastic, but they will be better than those seen in the last decade”.

Pictet AM’s chief strategist gives two pieces of advice for 2024: first, take consensus expectations with caution; second, that the entry point for accessing different asset classes is key. In this regard, he has good news: “Equities, fixed income and cash are for the first time since 2002 where they should be: equity multiples are aligned with fundamentals, cash remunerates in line with inflation and rates are at normal levels, in line with nominal growth.”

The expert gave as an example of the caution to be taken when pricing in expectations how the two big stories that were to mark 2023, the US entering recession and the post covid recovery in China (which has disappointed markets) have played out: “We didn’t think the US was going to be so strong in 2023. By 2024 we expect a rebalancing with a big change, because it is still possible that the US will disappoint, that the consumer will weaken more than expected.” Instead, Paolini believes Europe could surprise positively.

On inflation, Paolini stated that “the last mile will be the hardest”, in the sense that the most painful thing will be to get inflation from 3% to 2%, because it will mean that “central banks will have to take the blame for causing a recession”. Therefore, the strategist says that any surprise in the inflation trajectory will be one of the main risks for next year, as it will condition the Fed’s response in a very sensitive year, as the US will hold elections in the last quarter of the year.

Another possible scenario is that inflation will stagnate at around 2.5%-3%, and US GDP will not grow, posing a new dilemma for the Fed. Should this materialize, Paolini believes that the Fed “will react, albeit not as quickly as we expect, to get growth back to 2%”.

Paolini believes that the situation will be more complicated for the ECB: “Inflation is a bit higher, but it will be more difficult for it to cut rates because inflation is more persistent”.

For these reasons, Pictet AM has a preference for fixed income, particularly U.S. and U.K. debt in the year ahead. “For the first time in 20 years, US IG bonds are offering higher yields than the S&P 500 dividend,” adds the strategist. On the other hand, he is cautious about high yield debt: “It is too early to invest, except for the very short term”. The expert indicated that the firm was also positive on emerging fixed income. He explained that the dollar is currently “overvalued, it should retreat and that would be positive for the global economy”.

Europe could surprise

In equities, the expert says that right now the key lies in determining “where we are in the cycle”. He says that “all the relevant indicators are very high”, so he asserts that the US is “closer to a recession than a recovery” and that if it has not fallen into recession this year it is because the economy is still taking the impact of the stimuli applied to the economy to counteract the pandemic. Instead, he predicts that Chinese assets will remain muted: “Investors want to see real estate stabilize, in our experience it is best to wait”.

Pictet AM has a positive view on Europe. “European equities may be the positive surprise of 2024,” says Paolini. He lists several reasons: sentiment is very pessimistic, European companies are trading at a lower P/E than they were during the Global Financial Crisis, and growth is improving because of rising disposable income, due to the impact of inflation. “There are still savings in Europe and there is still some fiscal expansion to come,” the expert concludes.

2022 will be remembered as a challenging period for financial markets, characterized by the ineffectiveness of traditional strategies and notable losses in global stock indices. Amidst this scenario, portfolio managers were forced to face the sale of positions backed by illiquid assets, highlighting the critical need for adaptability in investment management.

The rapid rise in interest rates in the United States and the Eurozone, driven by the urgency to curb runaway inflation, became a fundamental trigger for financial challenges. Additionally, the threat of recessions in major developed economies and geopolitical uncertainty created a landscape full of uncertainties for portfolio managers.

In this context, the 1st Report of the Asset Securitization Sector, sponsored by FlexFunds, serves as a tool to understand how financial advisors in different regions deal with the complexities of the current financial environment. The report analyzes short-term expectations, challenges in portfolio management, and key trends in the asset securitization sector through a series of questions directed at industry experts from over 80 companies in 15 countries in LATAM, the United States, and Europe.

In situations of uncertainty and volatility, portfolio management must seek the redistribution of financial resources to minimize risks and maximize returns. Portfolio diversification among different assets, sectors, and industries is a traditional strategy, but it is crucial for clients to understand the risks associated with each financial product. A delicate balance between risk and return, along with periodic rebalancing, becomes essential to maintain long-term goals and strategies.

Macroeconomic variables play a fundamental role in investment decision making. Economic growth, interest rates, inflation, the labor market, and government policies directly impact the health and performance of an economy. In this regard, the study conducted in this area has been broken down into four questions:

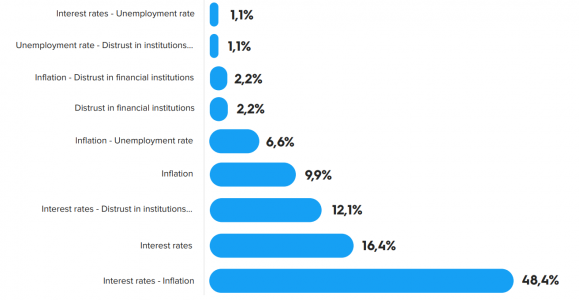

What variables will have the greatest influence on the markets in the next 12 months?

The results in Figure 1 show that almost half of the respondents believe that the main variables influencing the markets in the coming months will be interest rates and inflation, with interest rates being the primary variable considered by 78% of the sample, followed by inflation at 64.8%. Distrust in financial institutions is a factor considered by 17.6% of respondents.

Thus, the main variables to watch in the coming months are inflation and the evolution of interest rates until the end of their upward cycle.

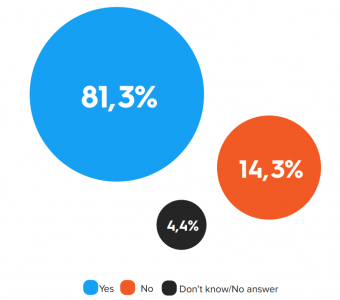

Considering that uncertainty is an inherent characteristic of financial markets, experts were asked if they believe investors are demanding more conservative positions. 81.3% of respondents believe that their clients are indeed demanding more conservative positions, compared to 14.3% who disagree with this statement, as seen in the following graph:

The situation in the financial markets during the year 2022/23, with losses in major indices and returns on stocks, investment funds, and assets, has generated an increase in perceived risk, increasing aversion to it. Both portfolio managers and investors are more inclined to modify their investment strategies to redistribute their portfolios towards more conservative positions.

The 1st Report of the Asset Securitization Sector provides portfolio managers with insights based on the survey results from nearly a hundred industry experts, where their expectations about interest rates and a possible recession in the United States over the next 12 months are also addressed. Download it now to learn their response and the main trends within the sector: Will the 60/40 model continue to be relevant? Which collective investment vehicles will be more used? What is the expected evolution for ETFs? What factors to consider when building a portfolio?

Members of the Group of Boutique Asset Managers (GBAM) are operating on five continents, and all are squaring up to 2024 by focusing on their usual ‘bottom up’ approach. But regardless of where they are on the globe, it’s clear that consistent themes are emerging at the macro level as well as some distinctly local ones in their 2024 outlooks.

Continued retreat from peak inflation and interest rates are central to expectations. The uncertainty element around rates is whether they may be held at levels that spark a soft landing, if not a recession in certain developed markets. But at the same time there is a sniff of opportunity: Emerging Markets could be winners from US Fed rate cuts alongside local elections leading to policy changes and economic reform.

The political factor looms large, with more than half the World’s population going to the polls through 2024, while ongoing conflicts in Europe and the Middle East in particular pose threats to food and energy prices.

The continued march of technology, digitisation and Artificial Intelligence notwithstanding, the reduced likelihood of the Magnificent Seven accounting for such a large share of stock market returns will put the spotlight on active management amid recognition of valuations in traditional asset classes and opportunities in diversification into alternatives and convertible bonds.

In Edinburgh, Scotland, Andrew Ward, Chief Executive Officer at Aubrey Capital Management, the specialist global manager, says: “The three global factors that will most likely affect our business in 2024 include a normalising of global inflation and interest rates, putting cash back in the pockets of ordinary consumers, thereby boosting the revenues of the sorts of companies in which we invest; the ratcheting back of inter-state conflict and the threat of such, creating more stability for trade to flourish and ordinary humans to live their lives, travel and spend hard-earned cash as they wish; and the sensible development and growth of AI (and other appropriate tech) that benefits modest businesses like ours, allowing us the scope to do more routine data processing (of various types) inhouse, thereby depending less on expensive near-monopolistic ‘providers’, ultimately allowing us to dramatically reduce fees and improve net returns to our clients.”

In Stavanger, Norway, The Chairman of GBAM and Chief Executive of SKAGEN Funds, Tim Warrington, opines that: “This year, in contrast to last, the consensus seems to be a soft-landing over recession; albeit with most hedging, noting that much needs to continue to go right to both deliver and sustain it.”

Putting aside elections on both sides of the Pond, where Tim sees too much at stake to expect significant policy changes, he says: “The narrow basis to success in 2023 – the AI-charged Magnificent Seven delivering more than half the market gains – will not endure ad infinitum. And interest rate tops in the developed markets will be supportive to emerging markets. So active managers should have advantage, especially those investing in small- to mid-caps and further afield.”

Also in the Europe region, MAPFRE’s Chief Investment Officer José Luís Jimenez in Madrid, Spain, and Co-Founder of GBAM, echoes the points of both of politics and uncertainty when he says: “History, like economics, is cyclical and bearing in mind that next year more than half of the population of the World will go to the polls, despite many of the ballot results being already known, uncertainty is all over the place However, most investors are suffering somekind of Peter Pan Syndrome: ‘A soft landing lies ahead, and it will be excellent for stocks and bonds’; ‘Interest rates cuts are around the corner next year and thanks to a strong labour market, Covid´s savings and cheaper finance, the World economy will do well’. But all experienced economists know that predictions are one thing and reality another. Many things could go wrong next year.”

Shifting the spotlight away from developed to emerging markets, there are signs that investors may come to appreciate this sector more than has been the case in recent years.

Reflecting on the relative opportunities for emerging markets, Ladislao Larraín, Chief Executive Officer at LarrainVial AM, the largest non-banking asset manager in Chile, based in Santiago, says: “The shift in the Federal Reserve’s monetary policy cycle is key to improving asset returns in emerging economies. The accelerating decline in inflation in the United States and globally has made it likely that the Fed’s rate cutsare likely to materialize before mid-2024. In this context, we are highly optimistic about political and macroeconomic developments in Latin America, where recent elections have been won by pro-free-market forces. This, coupled with very negative poll standings for most of the leftwing coalitions in power, promises to reverse the pink tide in the region. Additionally, the region’s countries have favourable macroeconomic stories such as the agro- and oil export boom in Brazil and nearshoring in Mexico.”

Charles Ferraz, Chief Executive Officer at the New York-based investment boutique Itaú USA Asset Management says: “Looking ahead to 2024, the US markets remain influenced by interest rates fluctuations, government spending, and potential election-related volatility. Caution is advised for the US equity markets, but emerging market equities should benefit from the scenario. In Brazil, the markets anticipate potential gains as global interest rates fall, combined with the ongoing local adjustments. With a robust current account, favourable geopolitical positioning, and growing capital markets, Brazil becomes an attractive destination for investments. However, the fiscal deficit continues to be a challenge. Overall, this dynamic sets the stage for optimism in both the stock market and the local currency (BRL).”

From another emerging market region, Hlelo (Lo) Nc. Giyose, Chief Investment Officer & Principal at First Avenue Investment Management, the long only equities specialist manager based in Johannesburg, South Africa, spots similarities in that that local developments in policy could have a significant impact on return expectations, as the country’s GDP has been in decline since 2011 even as it faces a rampant public service wage bill funded by debt that has reached a limit.

“It is time for the 33% of unemployed South Africans to go back to work (productively) to drive both pension fund flows and economic growth per capita. The reason we are pointing this out is that 2024 is a watershed year where the governing party, the African National Congress, is projected to lose its majority in government. The country can now focus on reforms from parties that have been critical of the economic malaise of the past 13 years.”

Over in Hong Kong, Ronald Chan, Chief Investment Officer and Founder of Chartwell Capital, the independent asset manager focused on China’s Greater Bay Area and the Asia-Pacific region, identifies elections next year in Taiwan and the US presidential election as particularly important events affecting the local business environment, along with rates decisions by the US Fed affecting asset prices and stock markets in Asia. The possibility of a global economic slowdown “could pose challenges for companies in Hong Kong, however, it’s important to note that challenges are often accompanied by opportunities, and businesses that can adapt to changing market conditions may find new avenues for growth and innovation.”

The local market faces specific conditions: valuations of Hong Kong local stocks are at their lowest in 30 years; dividend yields are in many cases at their highest, ranging from 8%-11%; and while foreign capital has been cautious due to concerns around China, mainland Chinese capital may be overlooking local businesses.

Another way to approach uncertainty is to consider asset class allocations. Members of GBAM have identified a number of opportunities emerging into 2024 despite identified risks stemming from the ongoing macro environment, particularly uncertainty around the pace of change in interest rates.

Paulo Del Priore, Partner at Farview, the global multi-strategy investment manager with offices in London, UK andSão Paulo, Brazil, highlights that amid a global investment landscape still marked by increasing complexity, heightened geopolitical tensions, and volatility, there is a shift in the correlation between equity and bonds, which, he says: “Challenges traditional investment approaches, such as buy-and-hold, underscoring the importance of incorporating alternative risk premia strategies into traditional portfolios. In 2024, we anticipate wider spreads in absolute returns, contributing to a more positive outlook.”

In Zurich, Switzerland, Dr. Pius Fisch, Chairman of Fisch Asset Management, a global leader in convertible bonds, says that amid a “tug-of-war” between increasing risk of recession and simultaneously falling interest rates “we believe that 2024 will be a promising year for fixed income, and for EM corporates in particular.”

“Investment-grade corporate bonds should be able to benefit strongly from an easing of monetary policy, but high-yield companies should also stand to gain from potentially lower refinancing rates. In addition, solid fundamentals and continued low default rates represent a robust backdrop. In the emerging markets complex, we also see very attractive carry for higher-quality companies with strong balance sheets and short maturities.”

And from Francisco Rodríguez d’Achille, Partner & Director of Lonvia Capital, the small- and mid-cap company specialist based in Paris, France, comes thoughts that: “Like in 2022, so far this year 2023 has left a significant de-rating in our portfolio in terms of valuation. A pause in the interest rate policy by the central banks will bring a return to fundamentals and with it a strong revaluation of companies that are growing structurally without depending on exogenous factors, despite the fact that they have been heavily punished in terms of price and valuation.”

Andreina Nicolosi, AML Compliance Director at Snowden Lane

Andreina Nicolosi has joined Snowden Lane from Morgan Stanley, industry sources informed Funds Society.

The lawyer, who joins as the Director of AML Compliance, has about twenty years in the industry.

Throughout her extensive career, Nicolosi has worked for the OAS, the World Bank, Citi, and HSBC. In the British bank, she worked for five years as a Financial Crime Compliance Officer, where she “brought experience in anti-money laundering operations to provide influential guidance to businesses and local compliance officers in order to avoid reputation risks and ensure compliance with laws and guidelines,” among other activities detailed inher LinkedIn profile.

In 2017, she joined Morgan Stanley, where she served as a compliance officer to assess the money laundering risk of Latin American clients, a position she held until her move to Snowden Lane.

This appointment adds to a large number of international advisor exits from Morgan Stanley after the warehouse announced in June of this year that it would close international accounts that did not meet certain requirements demanded by the company.

Among the firms that have captured the most advisors are Snowden Lane, Insigneo, Bolton, Raymond James, and UBS.

PIMCO has named Mohit Mittal, Managing Director and Portfolio Manager, as Chief Investment Officer – Core Strategies.

In this role, he will oversee fixed income portfolios across PIMCO’s core suite of strategies – including Low and Moderate Duration, Total Return and Long Duration – and lead the core portfolio management team. Mittal will report to Dan Ivascyn, Managing Director and Group Chief Investment Officer.

Mittal is a longstanding leader on the trade floor, a member of PIMCO’s Investment Committee and has a strong track record across a broad range of portfolios. He joined the Total Return portfolio management team five years ago and has contributed to PIMCO’s multi sector portfolios including Long Duration, Dynamic Bond, Stable Value and Investment Grade Credit.

“Mohit is the rare talent who brings deep quantitative expertise with macro insights to investing while embracing a collaborative approach that harnesses the best investment ideas generated by a team of portfolio managers,” said Ivascyn. “He’s a welcome addition to PIMCO’s highly experienced group of CIOs and his focus on core strategies further strengthens our leadership in fixed income markets.”

PIMCO’s other CIOs include Andrew Balls, Managing Director and CIO – Global Fixed Income, Mark Kiesel, Managing Director and CIO – Global Credit, Marc Seidner, Managing Director and CIO – Non-traditional Strategies, and Qi Wang, Managing Director and CIO – Portfolio Implementation.

Despite slower home price growth, affordability will be the biggest challenge for homebuyers in 2024, according to the Bright MLS 2024 Housing Forecast. However, more buyers and sellers will return to the market in the coming year as interest rates fall from 22-year highs, and homeowners begin to loosen their grip on 3% mortgage rates as life events prompt more people to move. The result will be more options for home shoppers and a rise in home sales, though market activity is still projected to remain well below typical levels.

As we look towards the real estate market in 2024, there are several key trends and predictions outlined by the Bright MLS forecast that buyers and sellers should be aware of. Firstly, a significant change is anticipated in mortgage rates. These rates are expected to establish a new normal, dropping below 7% in the first quarter of the year.

As the year progresses, they are predicted to fluctuate between 6-6.5%, eventually settling at around 6.2% by the end of the year. This shift in mortgage rates is crucial for both buyers and sellers as it directly impacts affordability and the overall cost of purchasing a home.

Another important aspect to consider is the expected movement in the housing market regarding sales and inventory. The forecast suggests a rebound in existing home sales, which are projected to conclude the year at 4.6 million. This marks a significant 12.1% increase from the low numbers recorded in 2023, though it’s still below the sales numbers typically seen in a regular year. Furthermore, the market is likely to witness more sellers entering due to changing family and financial circumstances. This influx of sellers is anticipated to boost the inventory by 7.6% by the end of 2024. An increase in inventory, coupled with a rise in the number of buyers, is expected to maintain stability in home prices.

Finally, the forecast addresses the dual aspects of affordability challenges and the impact of new home supplies on the market. Despite a general trend of stability in home prices, with the median price in the U.S. expected to rise marginally by 1.5% to $394,200, there are nuances to be aware of.

The growing affordability issues, combined with an increase in the supply of new homes, are likely to lead to a decrease in home prices in specific markets. This trend will be particularly evident in areas like California and Florida. Therefore, both buyers and sellers in these regions need to be particularly mindful of these localized market dynamics when making their real estate decisions in 2024.

“After a very difficult market for buyers who have had to contend with an atypical housing market in 2023, home shoppers will find more listings to choose from in 2024, ” Lisa Sturtevant, Bright MLS Chief Economist said. “At the same time, both buyers and sellers will have to reset expectations next year for persistently higher mortgage rates and more negotiations during the transaction.”

Key 2024 housing trends and the wildcards

A slower start to the spring homebuying season:Although home sales are expected to increase in 2024, Bright MLS’ forecast calls for home sales to remain low in the first quarter of the year, as rates remain around 7% and some prospective buyers will wait, holding out for lower rates later in the year.

“Life happens” will force homeowners out of their sub-3% loans: With nearly two-thirds of U.S. homeowners holding onto a mortgage rate below 4% and rates currently well above 7%, there has been little incentive to sell. However, as rates begin to fall and move closer to 6.5%, homeowners who have been characterized as being “locked in” to their mortgage will increasingly find that changing family and financial circumstances outweigh their low rates. This will lead to more new listings over the course of the year. Inventory will still be below pre-pandemic levels, though the gap will have narrowed so that nationally year-end 2024 inventory will be at 92% of the year-end 2019 level.

Affordability will continue to challenge buyers: Several factors will push and pull at home prices in 2024. More inventory will be generally offset by more buyers in the market. This will keep home prices stable in many markets. But affordability, which worsened significantly over the past year as both mortgage rates and home prices were rising, is going to continue to be a challenge in 2024, particularly for first-time homebuyers. Sellers looking to attract these buyers may need to offer closing cost assistance or other financial incentives to make the numbers work for those in the market for the first time.

Buyers waiting for a major price correction should not hold their breath: There is no evidence to suggest that there will be major, widespread home price corrections in 2024. However, in markets where home prices escalated during the pandemic or where new single-family construction is adding significantly to inventory, buyers could see home prices fall below 2023 levels. Conversely, markets where home prices have been rising in line with wages and inventory remains low, prices will continue to rise in 2024 (see the lists of markets with the largest forecasted increases and decreases below).

Wildcards that could shake up the housing market: The housing market has been anything but predictable in recent years, and there is a risk that political or economic factors could bring the unexpected to the housing market in 2024. Right now, the outlook is for a mild and short recession in 2024, which will not have a major impact on the housing market. However, ongoing global conflicts could increase the U.S. recession risk. Government standoffs and political discord at home can also lead to more consumer anxiety.

J.P. Morgan Private Bank released its 2024 Global Investments Outlook, After the Rate Reset: Investing Reconfigured, which defines five important considerations for investors as they navigate the dynamics of today’s new interest rate environment.

“Markets have entered an entirely new interest rate regime,” said Grace Peters, Global Head of Investment Strategy at J.P. Morgan Private Bank. “Three years ago, nearly 30% of all global government debt traded with a negative yield. It seemed the era of super-low interest rates might never end, but it did.”

“As we head into a new year, it’s time for investors to think about their investing goals and how they must adapt to – and even capitalize on – this market environment,” said Clay Erwin, Global Head of Investments Sales & Trading at J.P. Morgan Private Bank. “The rise in global bond yields is not just historic—it may mark a once in a generation entry point for investors that might not be available a year from now.”

To harness the new dynamics of a 5% rate world, J.P. Morgan Private Bank’s 2024 Investment Outlook explores five important themes.

Inflation will likely settle – you should still hedge against it.

“Compared to this time last year, the inflationary outlook is far less bleak. However, we think that 2% mandate will become the inflation floor, not the ceiling. Therefore, investors still need to prepare for a higher inflation world, just not as high as we’ve experienced recently,” said Erwin.

To grapple with the prospect of more meaningful inflation in 2024 and beyond, investors might first look to equities. Public companies may continue to maintain both pricing power and their margins.

Moreover, while investors used bonds to help insulate portfolios from slower growth in the previous cycle, the 2024 Outlook notes that investors should consider an allocation to real assets as an inflation hedge for the cycle ahead.

The cash conundrum: the benefits and risks of holding too much.

Low volatility and 5% yields on cash have been a magnet for J.P. Morgan Private Bank’s clients, who are holding significantly more cash than they did two years ago, having added at least $120 billion more in more in short term money market funds and treasury bills. This trend is global, but particularly powerful in the U.S. where clients have over twice the allocation to short-term treasuries and money markets as their peers outside the U.S.

“It feels good to hold cash when rates are high and other markets are this volatile,” said Jacob Manoukian, U.S. Head of Investment Strategy at J.P. Morgan Private Bank. “Cash works best relative to stocks and bonds in periods when interest rates are rising quickly, and investors question the durability of corporate earnings growth. But we think this is as good as it gets for cash.”

Bonds are competitive with stocks – adjust the mix according to your ambitions.

While there has been a painful stretch for bondholders this year, the new rate regime represents a reset in bond market pricing, and core bonds may now be poised to deliver strong forward-looking returns. Relative to stocks, bonds haven’t looked this attractive since before the Global Financial Crisis. Despite this, four out of every five J.P. Morgan Private Bank clients have not materially increased their allocation to fixed income over the last two years.

“We look to bonds to provide stability and income. Given the recent increase in yields, from our view bonds are now well positioned to deliver on both fronts,” added Manoukian.

With AI momentum, equities seem to be on the march to new highs.

Equities offer the potential for meaningful gains in 2024. Even as economic growth slows amid higher rates, large-cap equity earnings growth should accelerate and may propel stock markets higher over the next year.

“We believe the U.S. large-cap corporate sector has gone through an earnings recession already, with eight of the eleven major sectors in the S&P 500 having reported negative earnings growth for two or more consecutive quarters over the last two years. These companies have emerged leaner and resilient to potential challenges that 2024 could present,” noted Christopher Baggini, GlobalHead of Equity Strategy at J.P. Morgan Private Bank.

Investors don’t seem to have missed the valuation opportunity. While the S&P 500 trades at an above average valuation, there is a substantial discount to be found in U.S. mid and small-caps as well as European and emerging market stocks. Additionally, the promise of artificial intelligence and the potential upside in the stocks of drug makers with a growing share of the weight loss market also provide an attractive opportunity for investors looking into next year.

On regional opportunities, Alex Wolf, Asia Head of Investment Strategy at J.P. Morgan Private Bank, considers Indian equities a bright spot for 2024.

“In India, corporate earnings have kept pace with GDP growth – a rarity in emerging economies. Indian company profits, and thus stock returns, have tended to grow in line with nominal GDP,” notes Wolf. “Data over the past twenty years show that India has one of the closest relationships between economic growth and market returns.”

Pockets of credit stress loom, but they will likely be limited.

The next year could see stress in certain sectors of the credit complex. For example, commercial real estate loans, leveraged loans, and some areas of consumer credit – like autos and credit card – and high yield corporate credit could be vulnerable.

“An inescapable fact of the business cycle is that higher interest rates make credit harder to come by. We think these stresses will be manageable, and not enough to cause a recession in 2024,” added Peters.

Learn more about J.P. Morgan Private Bank’s 2024 Global Investments Outlook and download the full report here.

iBusiness Funding announced the launch of LenderAI Prodigy which introduces an innovative collection of AI chatbots inside their flagship end-to-end SBA software solution, LenderAI.

The first chatbot iBusiness Funding has implemented helps users navigate the SBA’s Standard Operating Procedures (SOP) quickly and accurately. A user can ask the chatbot any SBA-related question, and the bot will respond with the correct answer as per the SOP. It also cites the specific section it is referencing in the SOP for the user. Originally developed for and successfully utilized internally by iBusiness Funding, it is now available to all LenderAI clients within the new Prodigy feature.

This functionality showcases iBusiness Funding’s expertise with AI as well as their commitment to testing and refining technology internally before bringing it to the market, the firm said.

“The SOP chatbot was a game changer for our internal teams, enabling us to navigate the complexities of the SBA’s SOP with ease. Seeing its impact, we knew it was essential to adapt and offer this powerful tool to our clients,” said Justin Levy, CEO of iBusiness Funding. “You can ask the bot things like ‘How do I release collateral in loan servicing,’ ‘Please chart the maximum rates of SBA loans,’ or a myriad of other questions that commonly come up when processing SBA loans and get an accurate answer instantly.” With its ability to provide fast, reliable answers, this tool significantly reduces the time and effort it takes financial institutions to find information. It is also updated frequently to reflect any updates or changes to the SOP.

First in Market and Future Developments

As the first AI tool of its kind in the market, LenderAI Prodigy underscores iBusiness Funding’s role as an innovator in the financial technology and artificial intelligence spaces. The next chatbot to be released will provide lenders using LenderAI with a customized chatbot reflecting their own specific credit policies and guidelines that their staff can use internally. This will make it easier than ever for lenders to ensure their employees can quickly and easily understand their own guidelines and policies by relying on a single source of truth. Additional chatbots are in development, promising to further enhance LenderAI’s capabilities.

“Our goal with the first chatbot inside the Prodigy feature is to empower banks and credit unions with a tool that not only saves time but also ensures accuracy and compliance with the latest SOP updates. Our chatbot is future-proof and updated as changes are introduced to the SOP, ensuring our clients have peace of mind knowing that the answers they receive to their questions are always correct,” added Mr. Levy.