Frederick Shaw, Country Head – United States at Apex Group

Apex Group announces the appointment of Frederick Shaw as Country Head – United States, responsible for overseeing the delivery of Apex Group’s single-source solution to clients in the geography.

Shaw brings two decades of experience in the financial services industry, joining Apex Group from private markets investor, Hamilton Lane, where he held the role of Chief Risk Officer and Global Head of Operations.

During his tenure, Shaw led teams overseeing the company’s domestic and international regulatory compliance and risk management frameworks along with its global operations complex. Prior to joining Hamilton Lane in 2011, Shaw held senior compliance and operational roles in international banks and alternative asset management.

In his new role, Shaw will oversee Apex Group’s rapidly expanding US business, which now employs over 600 people across 15 local offices.

The Group’s domestic US clients, as well as international clients investing into the US, benefit from the efficiency of a single-source solution, including access to a broad range of services including Digital Banking, Depositary, Fund Raising Services, and pioneering ESG Ratings and Advisory Solutions, offered globally and delivered locally, the firm said.

In addition to strong organic growth, Apex Group has also recently completed the integration and rebrand of theacquisition of Greenhough Consulting Group, bolstering its corporate and business services offering for funds and corporates, the company added.

Shaw will work closely Apex Group’s experienced regional leadership team, including recently appointed Group President, Samir Pandiri, Georges Archibald, Chief Innovation Officer and Regional Managing Director, Americas and Elaine Chim, Global Head of Closed Ended Products.

Georges Archibald, Chief Innovation Officer and Regional Managing Director, Americas, comments: “We are thrilled to welcome an executive with Fred’s knowledge and outstanding market reputation to our senior leadership team. His extensive buy side experience will provide valuable insights into the requirements of our current and future clients and enable us to further enhance their operational efficiency and performance. Fred shares our commitment to maintaining regulatory standards while embracing new ideas and approaches as we evolve to become the service provider of the future.”

Frederick Shaw, Country Head – US adds: “I am excited by the opportunity to join Apex Group, drawing on my client-side experience to drive continued service excellence, innovation and growth for clients. Apex Group has successfully disrupted the US market, as an independent provider of a compelling single-source solution which supports the entire value chain of a business. I look forward to playing a part in the business’ continued success, by leveraging Apex Group’s technology and solutions to better address the priorities of our clients.”

The COVID-19 pandemic has impacted us in numerous ways, setting off a cascade of dramatic changes to our lifestyles, and amid the unique circumstances of the lockdown environment, many turned to pets for companionship. The American Pet Products Association estimates that pet ownership increased from 56% of households in 1988, to 67% in 2019 and 70% post pandemic, mostly driven by millennials. Dogs comprise 57% of pet ownership, followed by cats at 27%.

Households across the U.S., Europe and Asia are shrinking due to a combination of lower birth rates, delayed marriages and overall rising costs of living and having children. In the U.S., for example, the average number of people per household dropped from an average of 3.5 in the 1960s to roughly 2.5 by 2020. As family formation has taken a back seat, and as many employees were told to work remotely during the pandemic, many millennials have chosen to have “fur babies” over children, especially during the COVID-19 pandemic. According to census data as of July 2019, millennials have overtaken baby boomers as the largest generation with 72 million members, and they experienced the highest increase in pet ownership among all age groups.

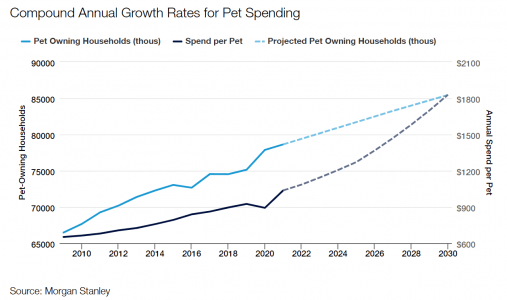

Millennials (born from 1981 to 1996), as well as Gen Z (1997 to 2013), are also the age groups that are most likely to consider their pets to be part of the family. Their desire to humanize their pets means they’re more willing than any other age group to spend a larger portion of their incomes on keeping their pets healthy and happy. More important, these two age groups are also expected to own roughly 60% of U.S. dogs by 2025, exceeding the pet ownership of the boomer generation. We believe this increase, and these age groups’ stronger attachment or “humanization” of their pets, will together provide a durable tailwind for the pet sector for many years to come. As seen below, Morgan Stanley predicts an acceleration to an 8% compound annual growth rate for U.S. pet expenditures by 2030, one of the largest rates of return in any retail segment.

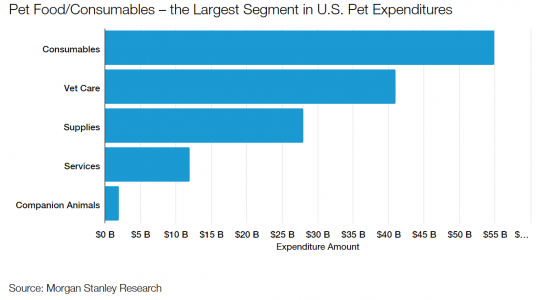

In addition, while emerging-markets countries such as India, Mexico, China and Brazil are currently lagging developed nations in pet ownership per capita, there is broad-based growth. In fact, according to a pet industry report by Bloomberg Intelligence, the global pet industry is expected to reach $493 billion by 2030, representing a drastic 54% increase from current levels. Although the U.S. will likely continue to be the largest market, emerging markets countries are also expected to deliver growth due to under-penetration of packaged dog food. Under-penetration and premiumization should continue to drive the largest consumables segment, while the basic need for pets to eat reduces cyclicality.

With a growing number of Americans regarding their pets as essentially a member of their family, the “pet humanization” trend has spawned an explosion of new businesses that focuses on providing better pet nutrition and care. Pet “parents,” especially in the developed world, have become increasingly educated about pet diets, and they are willing to devote more of their hard-earned money on premium, natural or branded pet foods. The “premiumization” of pet food has accelerated in popularity, particularly among millennials, who are more willing than other age groups to make financial trade-offs here and invest in their pets’ health.

More to the point, U.S. millennial consumers are moving away from highly processed and lower-quality dry food (i.e., kibble) to pet foods that are minimally processed or so-called “raw” or “gently cooked” with human-grade ingredients. Gourmet-level dog and cat food is one of the fastest-growing areas in the pet food market due to its superior nutrition and lack of additives. Fresh pet food is believed to provide benefits like more energy, shinier coats, less stinky breath and healthier skin. Moreover, for consumers, cost seems to matter less and less in today’s landscape.

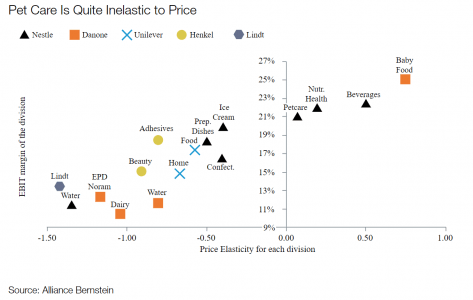

The premium pet food category appears to be one of the last areas where consumers are making “trade-down” decisions — that is, where they are willing to substitute for cheaper products — even despite high inflation eating away at household incomes. And once pet parents find high-quality foods that work for their pets, they’re unlikely to switch. As a result, pet food — and especially premium pet food — is proving to be one of the most resilient areas compared to other spending categories. As seen below, the price elasticity of the pet care category, which includes pet food, is almost as inelastic as those of baby food.

Lastly, adoption and acceleration of e-commerce have helped further bolster the pet food sector. Pet food e-commerce was already growing at a healthy pace before the pandemic, but digital paths to purchasing pet food have gained even more traction in recent years. Carrying home heavy boxes of dog food, or other pet products, like cat litter, isn’t appealing. And pet owners, especially those in the younger generations, are seeing the value of online shopping as well as direct and auto-shipping to their doorsteps. According to a 2021 report from Packaged Facts, pet food e-commerce will account for 55% of total U.S. pet food sales by 2025. That is up from approximately 30% today, above the 20% average for all U.S. retail.

The culture shift around pets has helped propel a rising demand for natural and premium pet goods. We believe the pet food industry is one of the most recession-resistant defensive plays, but also a structural growth story in the market.

Analysis by Mustafa Arikan, equity research analyst for Thornburg Investment Management.

Wipfli, a top 20 advisory and accounting firm, published the results of two industry surveys from the wealth management and asset management sectors to gain insights into their current economic challenges and how they’re positioning themselves for long-term market stability.

Ongoing rate hikes, uncertain market performance, geopolitical tensions, and increased competition all contribute to overall cautious economic predictions in both the new State of the wealth management and State of asset management industry reports.

“Our research indicates common themes uniting wealth management and asset management firms’ priorities,” said Anna Kooi, financial services and institutions practice leader at Wipfli. “Employee retention and recruitment, client engagement, and technology integration are all crucial for future success, and firms have to balance budget allocations and investments in each area appropriately.”

Both wealth management and asset management firms anticipate shifting economic times ahead, with 62% of wealth management firms and 72% of asset management firms expecting a U.S. recession in the next 12 months. Accordingly, the majority of survey participants for each industry estimate conservative market growth of five to eight percent over the next 12 months (55% wealth, 65% asset). Less than a third for both industries anticipate standard growth of eight to ten percent.

Recruiting top talent and implementing technology are key concerns for both industries. About two-thirds of both industries (66% wealth, 69% asset) list employee recruitment as one of their top concerns, and asset management firms note that talent management is their most important strategic focus. Also, asset management firms are ahead of the curve in recognizing how technology can assist and automate tasks for employees, while wealth management firms are also focused on new client acquisition and cultivation.

“Wealth management firms need to focus on targeted strategies that will help them foster long-term stability and viability,” said Paul Lally, wealth and asset management industry leader, principal at Wipfli. “In today’s uncertain economy, it’s critical for firms to adapt and constantly reassess their growth strategies.”

For example, most wealth management firms surveyed listed new client demographics as a key priority, but the majority also reported making no changes to their client acquisition strategies. In addition, offering employee flexibility was seen as key to addressing recruiting concerns, yet 64% of wealth respondents also expected employees to work in the office five days a week. Workplace flexibility and increased employee benefits will be key for firms to attract new talent, and wealth management firms should ensure that their growth plans align with their overall goals and initiatives to avoid contradictions in their strategies.

Asset management respondents are experiencing a massive shift in how technology is applied in their day-to-day operations. Three-quarters of asset firms surveyed named “managing and implementing change” as the top factor driving their goal achievement. With the onset of industry-changing technologies like artificial intelligence enhancing their work, asset management firms know they are on the precipice of a new era.

“Asset management firms recognize the important role technology will need to play due to the ever increasing complexity of investment opportunities and client demands.” said Ron Niemaszyk, partner for Wipfli’s wealth and asset management practice. “New and older generations of clients are increasingly comfortable with technology, and expect firms to provide a level of reporting on metrics well beyond that of monthly returns. Investors are now looking for insights into their portfolios’ risks and exposure to ESG initiatives. Firms who begin offering this type of reporting now can establish an edge in client acquisition over less progressive competitors.”

Technological integration is transforming how wealth management and asset management firms do business. In both industries, some firms are already using technology to support more efficient client onboarding and account management processes, as well as using data analytics to inform business decisions. Eighty-three percent of asset management firms are using business analytics to support data-driven decisions, and 58% of wealth management firms have increased their use of analytics in key business strategies.

The wealth management survey was based on responses from 102 wealth management firms across 28 states, and the asset management survey had 99 firms respond across 31 states. Both the State of the asset management report and the State of the wealth management report can be found on Wipfli’s website.

Ocorian has strengthened its financial crime and anti-money laundering support for clients with a key appointment. It has promoted Joe French to Managing Director and Head of its Financial Crime and Consulting Services.

Joe French is promoted to his new role having previously worked for Ocorian’s Newgate Compliance Limited for over six years. His experience includes 13 years with HM Revenue & Customs leading intelligence teams which developed domestic and international criminal and civil cases in relation to money laundering, fraud and cyber-crime. Prior to this he worked for the Financial Conduct Authority, after starting his career with Royal Bank of Scotland.

This comes as recent international research with more than 130 family office professionals, commissioned by Ocorian, said growing regulatory pressures are a key driver behind 91% expecting their outsourcing to grow over the next three years.

Ricky Popat, Director – Regulatory & Compliance at Ocorian said: “Joe’s appointment and our growing financial crime team emphasises our focus on excellence in this area. We know that many clients including family offices struggle to source regulatory support, so we’re delighted to be able to enhance our services to clients with particular emphasis on digital assets.”

Joe French added: “Regulatory demands are increasing rapidly across all jurisdictions and businesses often find it difficult to ensure they remain compliant on a continuous basis and financial crime is a major focus for regulators worldwide. I’m excited to be part of a growing team at Ocorian who can offer clients the very best advice and continue and to supporting clients with pragmatic and flexible solutions building on the wide range of services provided by Ocorian.”

Investors Trust announces the launch of ITA University, its innovative online educational platform. In alliance with IE University and CFA Institute, Investors Trust continues its commitment to provide the financial advisor of the future with the best resources available.

This educational platform will be available only for financial advisors working with Investors Trust and aims to deliver a one-of-a-kind approach to higher education for IFAs looking to expand their skills and professional knowledge.

ITA University will provide tailor-made courses, certifications, and other educational resources in collaboration with Investors Trust’s strategic partners IE University and CFA Institute. By joining efforts with these prestigious institutions, financial advisors working with Investors Trust will have access to top-rated personalized training in order to deliver the best service to their clients.

“We believe education is key to keep growing in an evolving and always changing industry. ITA University is another representation of Investors Trust’s commitment to the development and success of our financial advisors,” said Ariel Amigo, Chief Marketing & Distribution Officer.

Investors Trust is excited for the launch of this powerful educational platform and to work alongside top-rated institutions in order to keep providing excellence in the insurance and investments industry.

The income necessary to buy a starter home has risen most in Florida, according to a new report from Redfin.

In Miami buyers need to earn $79,500 (up 24.8%) to afford the typical $300,000 starter home. Rounding out the top three is Newark, NJ, where buyers need $88,800 (up 21.1%) to afford a $335,000 home. Fort Lauderdale, Miami and Newark also had the biggest starter-home price increases, with prices up 15.8% year over year, 13.2% and 9.8%, respectively.

In addition, Fort Lauderdale buyers need to earn $58,300 per year to purchase a $220,000 home, the typical price for a starter home in that area, up 28% from a year earlier. That’s the biggest uptick of the 50 most populous U.S. metros.

Even though starter-home prices have risen most in Florida, they’re still less expensive than a place like Austin or Phoenix, where home prices skyrocketed during the pandemic and have since come down some.

Prices are rising in Florida because despite increasing climate risks, out-of-town remote workers and retirees are flocking in. That’s largely due to warm weather and relative affordability; even though prices there soared during the pandemic, homes are still typically less expensive than a place like New York, Boston or Los Angeles. Five of the 10 most popular metros for relocating homebuyers are in Florida.

The U.S. Average

A first-time homebuyer must earn roughly $64,500 per year to afford the typical U.S. “starter” home, up 13% ($7,200) from a year ago.

The typical starter home sold for a record $243,000 in June, up 2.1% from a year earlier and up more than 45% from before the pandemic. Average mortgage rates hit 6.7% in June, up from 5.5% the year before and just under 4% before the pandemic.

Prices for starter homes continue to tick up because there are so few homes for sale, often prompting competition and pushing up prices for the ones that do hit the market. New listings of starter homes for sale dropped 23% from a year earlier in June, the biggest drop since the start of the pandemic. The total number of starter homes on the market is down 15%, also the biggest drop since the start of the pandemic. Limited listings and still-rising prices, exacerbated by high mortgage rates, have stifled sales activity. Sales of starter homes dropped 17% year over year in June.

“Buyers searching for starter homes in today’s market are on a wild goose chase because in many parts of the country, there’s no such thing as a starter home anymore,” said Redfin Senior Economist Sheharyar Bokhari. “The most affordable homes for sale are no longer affordable to people with lower budgets due to the combination of rising prices and rising rates. That’s locking many Americans out of the housing market altogether, preventing them from building equity and ultimately building lasting wealth. People who are already homeowners are sitting pretty, comparatively, because most of them have benefited from home values soaring over the last few years. That could lead to the wealth gap in this country becoming even more drastic.”

Home prices shot up during the pandemic due to record-low mortgage rates and remote work, and now rising mortgage rates are exacerbating the affordability crisis, especially for first-time buyers. A person looking to buy today’s typical starter home would have a monthly mortgage payment of $1,610, up 13% from a year ago and nearly double the typical payment just before the pandemic. Average U.S. wages have risen 4.4% from a year ago and roughly 20% from before the pandemic, not nearly enough to make up for the jump in monthly mortgage payments.

Many prospective first-time homebuyers are between a rock and a hard place because rents remain elevated, too. The typical U.S. asking rent is just $24 shy of the $2,053 peak hit in 2022.

Over the last few years, inflation, rising interest rates and high costs for just about everything have impacted nearly everyone – but for Gen Z, the economic environment has had a profound impact, a new U.S. Bank survey found.

Members of this generation, who range in age from 18 to 26, are overwhelmed by recent economic news, are unsure how to start investing, compare their financial progress to others – including their parents, people they see on social media, and people better off than they are – and are highly motivated by experiences and the pursuit of personal interests and opportunities. Members of the Millennial generation, aged 27-42, share many of these same feelings.

“Younger generations are dealing with inflation, high interest rates, and high prices, but they also inherited a much different world than older generations: since 1980, college tuition has increased by 169%; the average price of a home is up 540%; and average student-loan debt now sits at $37,000,” said Gunjan Kedia, vice chair of Wealth, Corporate, Commercial and Institutional Banking at U.S. Bank. “It’s no wonder they are unsure about beginning an investing journey. But despite these headwinds, they are passionate about investing in causes they believe in and are seeking financial guidance.

“We did this survey to better understand the challenges the younger generation is facing, how they are (or aren’t) investing and why, and how we can help them start investing before they lose too much time. Some of the findings that really stood out for me are that financial worries and decision fatigue are impacting young investors’ confidence, they are overwhelmed and unsure how to begin investing, and nearly 80% of investors responded to the economic climate by changing their investment strategies in some way in the past three months.”

Among the highlights of the report are the search for a better quality of life, personal interests and new experiences drive the investment decisions of younger generations.

In addition, Gen Zers view wealth differently than older generations and will sacrifice returns to invest in causes they believe in.

Finally, younger generations compare themselves to others and social networks.

The new data is from a proprietary U.S. Bank survey of 3,000 active investors and 1,000 aspiring investors of all generations. The survey was conducted May 12-24, 2023.

To read the full report, please click on the following link.

The Securities and Exchange Commission charged Richard Heart (aka Richard Schueler) and three unincorporated entities that he controls, Hex, PulseChain, and PulseX, with conducting unregistered offerings of crypto asset securities that raised more than $1 billion in crypto assets from investors. The SEC also charged Heart and PulseChain with fraud for misappropriating at least $12 million of offering proceeds to purchase luxury goods including sports cars, watches, and a 555-carat black diamond known as ‘The Enigma’ – reportedly the largest black diamond in the world.

According to the SEC’s complaint, Heart began marketing Hex in 2018, claiming it was the first high-yield “blockchain certificate of deposit,” and began promoting Hex tokens as an investment designed to make people “rich.”

From at least December 2019 through November 2020, Heart and Hex allegedly offered and sold Hex tokens in an unregistered offering, collecting more than 2.3 million Ethereum (ETH), including through so-called “recycling” transactions that enabled Heart to surreptitiously gain control of more Hex tokens.

The complaint also alleges that, between at least July 2021 and March 2022, Heart orchestrated two additional unregistered crypto asset security offerings that each raised hundreds of millions of dollars more in crypto assets. As alleged, those funds were intended to support development of a supposed crypto asset network, PulseChain, and a claimed crypto asset trading platform, PulseX, through the offerings of their native tokens, respectively, PLS and PLSX.

Heart also allegedly designed and marketed a so-called “staking” feature for Hex tokens, which he claimed would deliver returns as high as 38 percent. The complaint further alleges that Heart attempted to evade securities laws by calling on investors to “sacrifice” (instead of “invest”) their crypto assets in exchange for PLS and PLSX tokens.

“Heart called on investors to buy crypto asset securities in offerings that he failed to register. He then defrauded those investors by spending some of their crypto assets on exorbitant luxury goods,” said Eric Werner, Director of the Fort Worth Regional Office. “This action seeks to protect the investing public and hold Heart accountable for his actions.”

The SEC’s complaint, filed in U.S. District Court for the Eastern District of New York, alleges that Heart, Hex, PulseChain, and PulseX violated the registration provisions of Section 5 of the Securities Act of 1933.

The complaint also alleges that Heart and PulseChain violated the antifraud provisions of the federal securities laws. The complaint seeks injunctive relief, disgorgement of ill-gotten gains plus prejudgment interest, penalties, and other equitable relief.

Investors around the world are aware that the asset growth and the prolonged period of low interest rates that defined the decade-plus bull run are unlikely to return any time soon, according to Cerulli Associates’ latest report,Global Markets 2023: A Changing World. Product development and innovation will be vital for asset managers seeking to retain and win business in the coming years.

“The mutual fund industry demonstrated resilience last year, achieving growth despite the volatile market environment,” says André Schnurrenberger, managing director, Europe at Cerulli Associates. “We believe the best opportunities for asset managers exist in specialist areas such as responsible investment and alternatives, as well as the wealth management channel.”

In the highly competitive U.S. market, product strategy and innovation are driven by the fact that many investment products are viewed as lacking differentiation. Cerulli believes that, to satisfy the unique needs of investors, asset managers need to deliver more solutions across a broader range of vehicle structures and provide scalable solutions that can be customized at the individual investor level. Firms that have built their businesses on the backbone of the mutual fund structure over several decades need to determine which direction to pivot their offerings to retain assets.

In Hong Kong, product innovation has been seen in the exchange-traded fund (ETF) segment, with developments in virtual asset; technology; and environmental, social, and governance (ESG) ETFs, among others. Korea has also seen developments in the ETF space, where regulation has been eased since the end of 2022, allowing product diversification.

This has led to innovations such as ETFs tracking new underlying indices that are not usually tracked or customized, hybrid ETFs centered on a single stock, and maturity-matching bond ETFs with a lifespan.

In China, the assets of ETFs, excluding money market ETFs, increased by 19.8% to RMB1.3 trillion (US$200 billion) last year as innovative products such as bond, index enhanced, cross-border, and themed ETFs boomed. Meanwhile, in the U.S., where the ETF has historically been linked to index strategies, there has recently been increased product development in actively managed ETFs, including mutual fund conversions.

In Singapore, Cerulli believes there is scope for innovation in ESG and alternatives, particularly in the high-net-worth (HNW) segment. For example, Abrdn has launched an ESG-focused Asian high-yield bond fund targeting retail investors. In the investment-linked product (ILP) space, local insurers are not only putting emphasis on sustainability and looking for related investment solutions, but also continuing to launch new and innovative ILPs and search for underlying funds.

The importance of ESG criteria to Swedish institutional investors means opportunities exist for asset managers that can demonstrate a clear, transparent, and repeatable sustainable investment process. Those that can support innovative and forward-looking approaches to environmental themes will be particularly in demand among smaller pension funds seeking efficient exposures.

“Climate and environment-themed funds have so far dominated ESG product development, but we are seeing plenty of activity in impact investing,” says Schnurrenberger. “In Singapore, for example, the DBS Asia Impact First Fund, which was launched in August 2022, seeks to provide capital to social enterprises that focus on social and environmental issues in Asia.”

S&P Dow Jones Indices (S&P DJI) today released the latest results for the S&P CoreLogic Case-Shiller Indices, the leading measure of U.S. home prices. Data released today for May 2023 show all 20 major metro markets reported month-over-month price increases for the third straight month. More than 27 years of history are available for the data series and can be accessed in full by going to following link.

YEAR-OVER-YEAR

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a -0.5% annual decrease in May, down from a loss of -0.1% in the previous month. The 10-City Composite showed a decrease of -1.0%, which is a tick up from the -1.1% decrease in the previous month. The 20-City Composite posted a -1.7% year-over-year loss, same as in the previous month.

Chicago, Cleveland, and New York reported the highest year-over-year gains among the 20 cities in May. Chicago moved up one to the top spot with a 4.6% year-over-year price increase, while Cleveland came in at number two with a 3.9% increase, and New York entered the top three in third with a 3.5% increase. There was an even split of 10 cities reporting lower prices and those reporting higher prices in the year ending May 2023 versus the year ending April 2023.

MONTH-OVER-MONTH

Before seasonal adjustment, the U.S. National Index posted a 1.2% month-over-month increase in May, while the 10-City and 20-City Composites both posted increases of 1.5%.

After seasonal adjustment, the U.S. National Index posted a month-over-month increase of 0.7%, while the 10-City Composite gained 1.1% and 20-City Composites posted an increase of 1.0%.

ANALYSIS

“The rally in U.S. home prices continued in May 2023,” says Craig J. Lazzara, Managing Director at S&P DJI. “Our National Composite rose by 1.2% in May, and now stands only 1.0% below its June 2022 peak. The 10- and 20-City Composites also rose in May, in both cases by 1.5%.

“The ongoing recovery in home prices is broadly based. Before seasonal adjustment, prices rose in all 20 cities in May (as they had also done in March and April). Seasonally adjusted data showed rising prices in 19 cities in May, repeating April’s performance. (The outlier is Phoenix, down 0.1% in both months.) On a trailing 12-month basis, the National Composite is 0.5% below its May 2022 level, with the 10- and 20-City Composites also negative on a year-over-year basis.

“Regional differences continue to be striking. This month’s league table shows the Revenge of the Rust Belt, as Chicago (+4.6%), Cleveland (+3.9%), and New York (+3.5%) were the top performers. If this seems like an unusual occurrence to you, it seems that way to me too. It’s been five years to the month since a cold-weather city held the top spot (and that was Seattle, which isn’t all that cold). Since May 2018, the top-ranked cities have been Las Vegas (12 months), Phoenix (33 months), Tampa (5 months), and Miami (9 months).

“At the other end of the scale, the worst performers continue to cluster near the Pacific coast, with Seattle (-11.3%) and San Francisco (-11.0%) at the bottom. This month the Midwest (+2.7%) unseated the Southeast (+2.1%) as the country’s strongest region. The West (-6.9%) remains weakest.

“Home prices in the U.S. began to fall after June 2022, and May’s data bolster the case that the final month of the decline was January 2023. Granted, the last four months’ price gains could be truncated by increases in mortgage rates or by general economic weakness. But the breadth and strength of May’s report are consistent with an optimistic view of future months.”