Altrata, the global data-driven intelligence on the wealthy and influential, released the 11th edition of the World Ultra Wealth Report 2023. The report reveals a 5.4% decline in the ultra high net worth (UHNW) population in 2022, the first annual decrease of this population in four years and the most substantial contraction since 2015.

The World Ultra Wealth Report 2023leverages Wealth-X data and sheds light on the state of the global UHNW population; those with a net worth of $30 million or more. Despite the annual decline in population, the ultra wealthy still hold more than $45 trillion in assets, with median wealth of $51 million per person.

Leveraging Wealth-X’s proprietary Wealth and Investible Assets Model, the global ultra wealthy population is expected to total 528,100 people by 2027, an increase of 133,000 on 2022 levels. UHNW wealth is projected to rise to $60.3trn, implying an additional $14.9trn of newly created wealth over the next five years.

The recent decline impacted global regions and cities differently. Among the numerous findings, the World Ultra Wealth Report 2023reveals that North America remains the leading ultra wealth region by far but saw a 4% decline in population in 2022; this was the biggest annual fall in a decade.

However, Asia experienced the largest fall of any region with a 10.9% decrease in ultra wealthy individuals and a 10.6% decrease in their overall wealth.

Europe’s wealth assets were hit hard by an inflationary spike and energy crises stemming from the Russia-Ukraine war, and the region experienced a 7.1% decline in its ultra-wealthy population, while the Middle East, Latin America and the Caribbean saw strong gains in ultra-wealthy individuals and total net worth.

The report goes on to examine different ultra wealthy archetypes, namely entrepreneurs, corporate executives, and sole inheritors. These archetypes highlight the similarities and differences among these demographics by wealth source, asset allocation, industry affiliation, luxury asset ownership trends and more.

“Whether by chance or design, the turbulent backdrop of 2022 provided wealth-creation opportunities for some among the ultra wealthy class,” said Manuel Bianchi, head of global sales for Altrata.

The Securities and Exchange Commission announced charges against five investment advisers for failing to comply with requirements related to the safekeeping of client assets.

Three of the firms were also charged with failing to timely update SEC disclosures regarding audits of their private fund clients’ financial statements. All five advisory firms have agreed to settle the SEC’s charges and to pay more than $500,000 in combined penalties.

The advisory firms are Lloyd George Management (HK) Limited; Bluestone Capital Management LLC; The Eideard Group, LLC; Disruptive Technology Advisers LLC and Apex Financial Advisors Inc.

According to the SEC’s orders, the five firms failed to do one or more of the following: have audits performed; deliver audited financials to investors in a timely manner; and/or ensure a qualified custodian maintained client assets. In addition, according to the SEC’s orders, two of the firms failed to promptly file amended Forms ADV to reflect they had received audited financial statements, and one of the firms did not properly describe the status of its financial statement audits for multiple years when filing its Form ADV.

“The Custody Rule and the associated Form ADV reporting obligations are core to investor protection,” said Andrew Dean, Co-Chief of the SEC Enforcement Division’s Asset Management Unit. “We will continue to ensure that private fund advisers meet their obligations to secure client assets.”

Without admitting or denying the findings, the firms agreed to be censured, to cease and desist from violating the respective charged provisions, and to pay civil penalties ranging from $50,000 to $225,000.

This is the second set of cases that the Commission has brought as part of a targeted sweep concerning violations of the Investment Advisers Act’s Custody Rule and Form ADV requirements by private fund advisers after charging nine advisory firms in September 2022.

Following two months of year-over-year declines, home prices rose in August (+0.7%) as the number of homes on the market decreased for the second month in a row, down -7.9% year-over-year, according to the Realtor.com® August Monthly Housing Trends Report.

Active inventory remained -47.8% below typical 2017 to 2019 levels, although an unseasonable increase in newly listed homes from July to August (+3.5%) this year provides more options for home shoppers as the fall buying season approaches.

“While the uptick in new listings is good news for home shoppers, inventory remains persistently low, even with record-high mortgage rates putting a damper on demand,” said Danielle Hale, Chief Economist for Realtor.com®. “The inventory crunch continues to put upward pressure on home prices, amplifying affordability concerns and shutting some potential buyers out of the market. However, we anticipate mortgage rates will gradually ease through the end of the year and, despite this month’s bump in home prices, we’ll be unlikely to see a new price peak this year.”

What it means for homebuyers, sellers, and the housing market Although home sellers were less active in August compared to last year, the increase in newly listed homes for sale from July to August creates a nice boost for shoppers heading into fall, which is typically the best time to buy a home. Homeowners who have been on the fence about selling will likely find eager buyers looking for fresh listings.

“As fall buying activity heats up, the newly available homes for sale aren’t likely to remain on the market long, so sellers and hopeful homebuyers will need to be prepared to move quickly,” said Realtor.com® Executive News Editor Clare Trapasso. “Home shoppers can save searches on Realtor.com® to receive real-time alerts, receive mortgage pre-approvals, and pore over their budgets to determine what they can realistically afford with today’s higher mortgage rates.”

Affordability remains a significant concern. Although sales of new homes are on the rise, construction activity isn’t sufficiently robust to offset the inventory shortage and ease prices, which are up nearly 38% from August 2019 levels. Additionally, elevated mortgage rates have raised the monthly financing cost of the average home by about $417, up 21.7% from August 2022. This greatly exceeds both wage growth (4.4%) and inflation (3.2%).

Newly listed homes improve from July, but inventory crunch continues While the market saw an unusual bump in newly listed homes for sale between July and August this year, the overall number of homes actively for sale shrank for the second consecutive month, reversing the consistent growth trajectory seen since April 2022. Some of this drop can be attributed to an off-season surge in inventory during a market slowdown last summer. Although active inventory still remains below typical pre-pandemic levels seen between 2017 and 2019, the modest rise in new homes listed for sale this summer could give buyers grappling with affordability issues more options.

As inventory shrinks, homes in several large markets sell faster compared to last year The time homes spend on the market is approaching last year’s quicker figures, with buyers again vying for fewer available options than the prior year in most parts of the country. Should this pattern continue, by the coming month homes in every region except the South are likely to sell faster than they did during the same period last year.

The US high yield market delivered strong returns in the first half of 2023, with the ICE BofA US High Yield Constrained Index gaining 5.42%. Solid economic data to start the year helped credit spreads tighten in the initial weeks of 2023. However, a round of bank failures including Silicon Valley and First Republic triggered a flight to quality later in 1Q23.

After the market digested another manufactured debt ceiling crisis in the US, signs of deflation and improving odds of a “softish” landing for the economy drove a vigorous rally in risk assets to end the first six months. Continued year-over-year growth of high yield issuers’ operating earnings in the first quarter and supportive market technicals also helped to lift high yield bond prices.

While high yield has delivered robust performance thus far in 2023, yields remain close to 8.5%, and Nomura maintains a constructive outlook for the asset class in the second half of the year. Key drivers of our favorable perspective include:

An Attractive Entry Point

Looking back on 30 years of data, when investors have put money to work with market yields between 8-9%, the median 12-month forward return for high yield was better than 11%. Similarly, the end of a tightening cycle has been an excellent time to deploy capital to risk assets, including high yield bonds. There have been five tightening cycles in the US over the last 30-years. High yield’s average 12-month forward return from the date of the last rate increase was over 12%. The Fed will likely hike one more time in July, but the end of the tightening cycle is rapidly approaching.

Solid Fundamentals

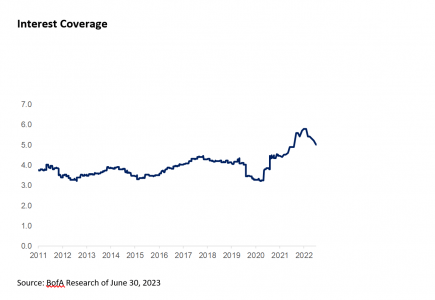

While it is too early to gauge second quarter results, operating earnings continued to grow in 1Q23, and more high yield issuers have guided 2023 earnings higher vs. those who revised expectations lower. High yield companies continue to generate cash flow, and they are using those resources to prepare for a slower economy. Leverage is close to a decade low. Interest coverage, arguably the best harbinger of the future default rate, is holding above 5x, the first instance in over 30 years of historical data that coverage has breached that threshold. BB-rated bonds currently represent close to 50% of the high yield market, while CCCs weigh in at just above 10%. Given the market’s healthy cash flows and higher quality tilt, Nomura expects the default rate to increase but not spike as the economy slows, rising from 1.6% over the last 12 months to a peak near the 3.2% long term average default rate.

Supportive Technicals

In 2022 the US high yield market contracted by roughly $200bil, a sizeable reduction relative to total market cap of close to $1.5tril. In the first half of 2023, the market saw more than $70bil of calls, tenders and maturities, and nearly $65bil of net rising star upgrades out of high yield. New issuance totaled about $95bil, thus the market contracted by approximately $40bil in 1H23, bolstering the supply/demand dynamic that drives prices. We expect the market to continue contracting over the balance of 2023, as a greater volume of high yield bonds are rising star candidates relative to investment grade issues that could drop to high yield. With less than $75bil of high yield bonds maturing before the end of 2024, we expect issuance to remain relatively light.

Flows Improving

According to Lipper data, high yield mutual funds and ETFs saw net outflows in excess of -$10bil in the first half of 2023. June net flows were positive $2.5bil, as investors perceived a favorable opportunity to add exposure to high yield. Nomura has experienced a comparable flow pattern in 2023. Net flows were relatively flat in the first five months of the year, masking a host of large subscriptions and redemptions, before flows turned meaningfully positive in June. Clients added to high yield for a variety of reasons including a more favorable tactical outlook for the asset class and portfolio rebalancing back to fixed income as a result of the heady equity returns in 1H23.

Favorable Outlook vs. Investment Grade

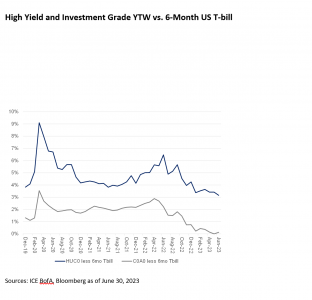

Based on our conversations with clients and prospects around the world, we believe that many investors have parked cash on the sidelines, enjoying T-bill yields approaching 5.5% while accepting reinvestment risk. A moderating growth and inflation outlook could prompt investors to re-risk portfolios by adding credit and duration exposure. When faced with the option of transitioning fixed income allocations into investment grade or high yield credit, we expect more clients to opt for the latter. Due to the steep inversion of the US Treasury yield curve, investors moving from 6-month T-bills to investment grade corporates (as proxied by the ICE BofA US Corporate Index – C0A0), picked up only 13bps of additional yield as of June 30. Investors would increase yield by more than 300bps moving from 6-month T-bills to the ICE BofA US High Yield Constrained Index (HUC0).

As of June 30, high yield (HUC0) offers a yield to worst of 8.6% with a duration less than 4 years. Investment grade (C0A0) yields 5.6% with a duration of 6.9 years. In a sideways market, high yield’s carry will likely help the asset class outperform. In a rising rate environment, shorter duration will advantage high yield relative to investment grade. High yield’s credit spread close to 400bps is not excessively cheap, but there is room for spread tightening if the US manages to avoid recession and land softly. Investment grade would likely outperform in a harsher than expected recession. However, we view that scenario as unlikely given the strong economic growth ongoing in sectors like travel & leisure, energy, and infrastructure, and the continuing imbalance between labor demand and supply supporting today’s robust job market.

Given these tailwinds, Nomura believes the current environment offers investors a favorable opportunity to increase portfolio allocations to high yield bonds.

Photo courtesyHéctor Grisi, CEO of Banco Santander, y Ana Botín, President.

Santander has been named the Most Innovative Bank in the world by The Banker. The magazine has given the bank its highest recognition at their Innovation in Digital Banking Awards because of the bank’s successful deployment of Gravity – the bank’s home-grown digital cloud-native core banking platform, which is being implemented worldwide to help the bank become a fully digital company. The Banker describes Gravity as a “massive and ambitious project”.

“Santander is the first major bank in the world with in-house software that digitalizes core banking, which is the most critical part of a bank’s IT infrastructure and where the main financial transactions, such as money transfers, deposits or loans are processed, and has already migrated more than 90% of its IT infrastructure to the cloud,” according to the firm’s statement.

This transformation is allowing easier and faster access to data, more simplicity and faster time-to market, making it possible to deliver new capabilities for customers in hours, instead of days or weeks, and more frequent app updates. It also helps the bank improve greatly its customer experience, products and services, and drive value using real-time analytics, the memo added.

This change will also bring significant efficiencies through cutting-edge end-to-end automation and other savings.

Ana Botín, Banco Santander executive chair, said: “Innovation is at the heart of our transformation, helping us serve customers better while delivering profitable growth and value creation. Gravity, and many other examples across the group, are testament to this. World-class innovation is only possible with top talent, so huge congratulations to all the Santander Group colleagues building these global solutions as a team. We are extremely grateful to the Banker magazine for this recognition.”

Santander’s core banking digital journey started in 2022 and will be completed between the end of 2024 and the first half of 2025. The transition has already been completed successfully in several businesses in UK and Chile without any service interruption, and is also well advanced in Brazil. Atthe completion of the programme, more than 1 trillion technical executions will be managed every year by the Gravity platform within Santander’s systems.

Gravity allows parallel processing, meaning the bank can simultaneously run workloads on its existing core banking mainframe and on the cloud, allowing it to perform real-time testing with no disruption to its businesses. Once satisfied with the stability and performance, the bank can then transition from the mainframe system to the cloud.

In October 2022, Google Cloud announced that it would be commercializing a service to help other companies transition from mainframe to cloud called Dual Run, which was developed on top of Santander’s Gravity software.

Santander’s successful cloud-native core banking platform is built upon world-class capabilities thanks to the knowledge transfer of a large team of IT professionals, some of whom created the legacy system 20 years ago and are now moving it to the cloud, as well as young developers and engineers. This gives Santander’s 16,500 software developers and engineers a modern, high-performing environment to create customer-centric applications and increase the bank’s ability to attract top talent. Santander has also reduced the bank’s energy consumption from its IT infrastructure by 70%, contributing to its responsible banking targets.

As part of Santander’s innovation initiatives, the bank is also in the middle of a transformation to bring its 164 million customers onto a common operating model supported by a cutting-edge technology platform. This project, named One Transformation, is based on proven group operating models and proprietary technology like Gravity. For example, Santander Portugal has taken most of its operational activities out of its branches, freeing up branch employees so that they can spend more time supporting customers and on commercial activities, and Openbank has implemented process automation and made every product available digitally end to end, with simple products. The bank is now implementing One Transformation in the US, Spain and Mexico.

The abrdn distribution team in charge of Brazil and Leonardo Lombardi, from CSP

Global asset manager abrdn announced today in Sao Paulo the completion of a new partnership with Capital Strategies Partners, the Madrid-based third party marketer firm, which will see Capital Strategies scale the delivery of abrdn funds in the Brazilian market, as well as bespoke solutions to pension funds and other institutional investors.

Working with Capital Strategies, abrdn will increase access to Brazil’s growing yet still underserved onshore market. Building on a wider push into South America’s largest wholesale market in 2023, the partnership follows the successful launch of two Brazilian Depository Receipts (BDRs) on B3 that mirror abrdn precious metal ETFs and will continue to drive interest in abrdn’s differentiated offerings from Brazilian accredited investors

The latest tie-up also builds on solid distribution foundation in South America, having secured a similar 2021 partnership in Spanish-speaking LatAm markets with Excel Capital supporting fund access in Argentina, Uruguay, Chile, Colombia and Peru. In combination, these partnerships now enable abrdn to cover a wide swath of the LatAm wholesale market and quickly and holistically address investor needs as they evolve.

“Capital Strategies has become well respected as a marketer leader in Latin America, especially in Brazil, and their platform delivers wide and efficient access to sophisticated investors and advisors,” said Menno de Vreeze, Head of Business Development for International Wealth Management – Brazil at abrdn. “abrdn’s capabilities are becoming well known in Latin America’s wealth circles, and as we further grow our presence, this is another big step that will add immediate scale and value. We’re very excited to discover the fruits of this relationship.”

Pedro Costa Felix, Partner at Capital Strategies, added: “We are now proud to be working with several of the world’s largest asset managers to deliver valuable exposure in Brazil, and are very pleased to add abrdn to that growing circle. Even as it continues to mature, it is clear that the Brazilian market already offers a compelling opportunity for abrdn and its funds, with their distinctive risk profile and specialization. We are keen to enable their successful growth in Brazil, helping to build regional reputation in LatAm and flowing in new global assets to their funds through these channels.”

61 percent of US companies surveyed expect ESG backlash to continue or increase over the next two years, according to a report issued by The Conference Board.

The report recommends that corporate boards and management view backlash as an opportunity to clarify their ESG strategy and communications.

The Conference Board also found that most companies are staying the course when it comes to their ESG commitments. Of the firms affected by backlash, just 11% are changing the substance of their ESG programs, while a majority are focusing more on the link between ESG and core business strategy. And nearly half are changing terminology to use terms such as “sustainability.”

“ESG backlash is an umbrella term that encompasses a range of positions from healthy skepticism to philosophical opposition to various forms of opportunism,” said Paul Washington, Executive Director of The Conference Board ESG Center. “While backlash is often fueled by people’s emotions, companies should respond objectively.

The most effective response is to ensure the company’s ESG positions align with company’s core business strategy, are supported by empirical data, and serve the long-term welfare of the company, its stakeholders, and society.”

These insights and others are featured in a new report, How Companies Can Address ESG Backlash, developed by The Conference Board in collaboration with the global CEO advisory firm Teneo.

The findings come from 1) a roundtable by The Conference Board that brought together more than 200 corporate leaders, and 2) a survey of 125 corporations, about half of which have annual revenue of over $10 billion.

U.S. Bank announced several updates to previously shared leadership changes that will be effective Sept. 1.

“Our succession planning efforts have enabled us to move quickly and prudently to ensure continuity of leadership and service as senior executives have made personal and professional choices in their careers,” said Andy Cecere, chairman, president and CEO of U.S. Bank.

Terrance Robert Dolan, currently vice chair and chief financial officer, and John Stern, senior executive vice president and head of Finance, will assume new titles effective Sept. 1.

Dolan will serve as vice chair and chief administration officer overseeing the company’s combined Chief Administration Office. Stern will become senior executive vice president and chief financial officer.

The company had indicated earlier this year that these promotions were expected this fall, and both leaders have been effectively prepared for their new roles. Dolan will continue to report to Cecere, with Stern reporting to Dolan.

At the same time, Jeff von Gillern, vice chair of Technology and Operations Services, will retire on Sept. 1.

The company previously announced his intention to retire last November, and he has been gracious to stay on board to guide the company through the systems integration related to its MUFG Union Bank acquisition.

Von Gillern will remain on hand as an advisor to the CEO through the end of the year, but his remaining day-to-day responsibilities will shift to Dilip Venkatachari effective the first day of September. Venkatachari, senior executive vice president and chief information and technology officer, will then report directly to Cecere and serve as an executive officer of the company.

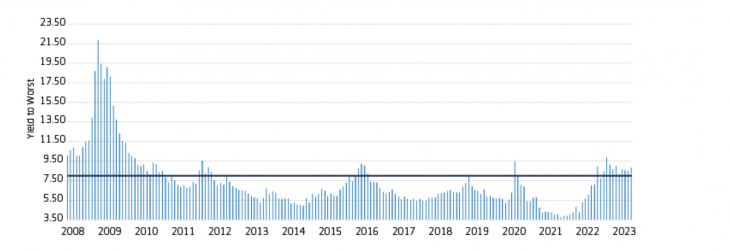

As rates have shifted higher, high yield is now living up to its name.

Since 2008, there have been relatively few opportunities to invest in high yield at yields above 8%. Many investors who allocated to the asset class during these times, benefited from double-digit total returns over the subsequent one-, three- and five-year periods.

Since 2008, the average annualized forward return for the Bloomberg US Corporate High Yield index ranged from approximately 11% to over 18% when the starting yield to worst was higher than 8%. The results are similar for the global high yield market.

Exhibit 1: Yields above 8% are relatively rare, and can present above-average total return potential Yield to worst for the Bloomberg US Corporate High Yield Index

Exhibit 1: Past results are not a reliable indicator of future performance.Source: Aegon AM and Bloomberg. Based on monthly Bloomberg. US Corporate High Yield Index data from January 1, 2008 to May 31, 2023. One-, three- and five-year returns are based on the forward annualized index return for months where the starting yield to worst was above 8%. Three-and five-year returns based on 44 months and 43 months, respectively, that had starting yields of more than 8%. Data is provided for illustrative purposes only. Indices do not reflect the performance of an actual investment. It is not possible to invest directly in an index, which also does not take into account trading commissions and costs. All investments contain risk and may lose value.

Assessing spreads and future return potential

While all-in yields are attractive, spreads remain around historical averages, leaving many investors grappling with the right time to increase their high yield allocation. Given the macro uncertainty, it is unlikely that we will see sustained spread tightening in the near term, although relatively tight market technicals can exert positive pressure.

Although spreads could be biased toward widening in the short term, we expect this could be more contained than during previous downturns given the higher-quality composition of the high yield market today relative to prior downturns.

Previous recessions have resulted in spreads widening above the 800 to 1,000 basis-point (bps) level. However, many of these periods were also during times of much lower risk-free rates. For example, the spread widening witnessed during 2020 occurred when rates were at historically low levels.

As a recession becomes more imminent, it is feasible that spread widening is more contained to around 600 to 700 bps given the higher-quality composition of the market and the solid fundamental starting point. Additionally, periods of spread widening could be short-lived, depending on the macro backdrop.

We believe that the majority of the Federal Reserve’s rate hikes have already occurred and that when the economy turns, rates are likely to decline, which could help offset some of the spread widening.

Additionally, after massive outflows from the high yield asset class in 2022, we may well witness a wave of inflows as opportunities arise and investors shift toward overweight, which could in turn provide supportive technicals and potentially result in swift spread tightening.

While it can be challenging to time the bottom or top of the market, we believe current yields can provide appealing long-term total return potential. In addition, we expect dislocations to emerge, presenting opportunities to capitalize on bouts of spread widening.

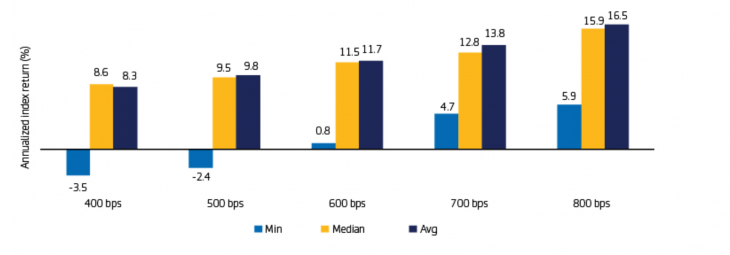

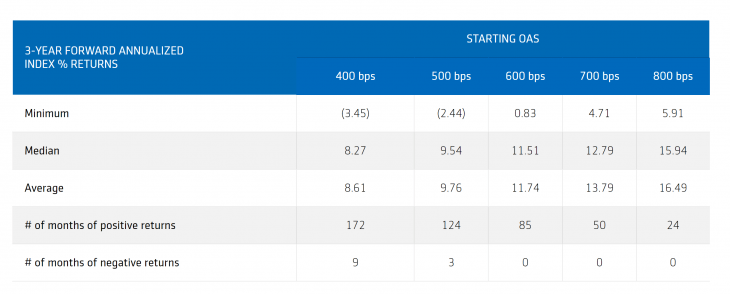

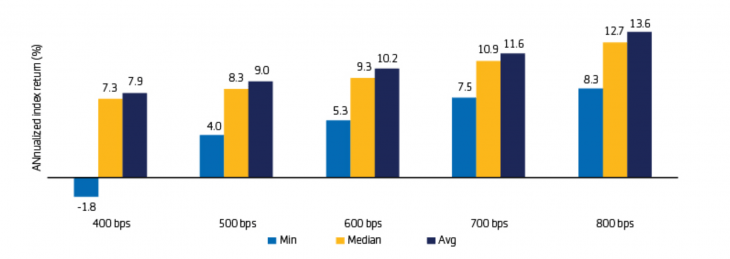

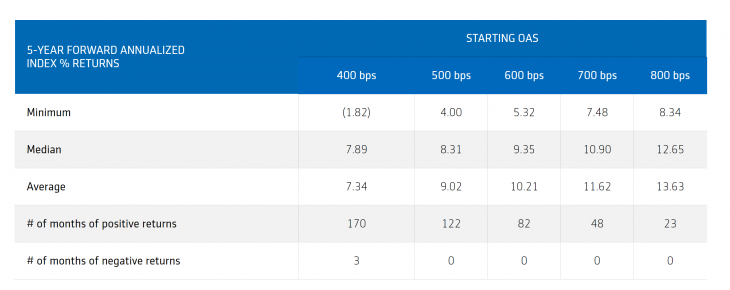

As shown below, the high yield index has historically generated average returns over 7% during the subsequent three- and five-year periods based on a starting OAS of 400 to 800 bps. The results are similar for US and global high yield indices.

Exhibit 2: 3-year forward high yield index returns based on starting OAS Bloomberg US Corporate High Yield Index (monthly data from January 1994 through May 2023)

Exhibit 3: 5-year forward high yield index returns based on starting OAS

Bloomberg US Corporate High Yield Index (monthly data from January 1994 through May 2023)

Exhibit 3: Past results are not a reliable indicator of future performance.Source: Aegon AM and Bloomberg. Based on monthly Bloomberg US Corporate High Yield Index data from January 31, 1994 – May 31, 2023. The 3- and 5-year returns are based on the forward annualized index return for months where the starting OAS was at or above the level shown. Data is provided for illustrative purposes only. Indices do not reflect the performance of an actual investment. It is not possible to invest directly in an index, which also does not take into account trading commissions and costs. All investments contain risk and may lose value.

Time in the market, not timing the market

Overall, we believe yields around 8% can present attractive opportunities for long-term investors. Depending on your appetite for volatility, this may not be the environment to stretch for unnecessary risk in lower-quality CCC bonds, particularly when there are interesting opportunities to generate solid returns in higher-quality high yield bonds.

In this environment, we think there is a case to be made for long-term investors to consider gradual increases to high yield in an effort to capitalize on attractive yields, provided they can weather some short-term market swings. Spread widening may present opportunities to further increase allocations, however timing the bottom or top of the market can be challenging. After all, it is time in the market, not timing the market, that matters in high yield.

Over the long term, high yield has tended to deliver competitive risk-adjusted returns compared to many other fixed income assets, and even equities. As such, we believe the structural case for high yield remains very much intact. And throughout the remainder of the year, we expect high yield has the potential to generate attractive carry and solid coupon-like returns.

Article written by Kevin Bakker, CFA and Co-head of US High Yield; Ben Miller, CFA and Co-head of US High Yield; Thomas Hanson, CFA and Head of Europe High Yield; and Mark Benbow, Investment Manager. All of them of Aegon Asset Management.

Los precios de la vivienda en Estados Unidos volvieron a aumentar por cuarto mes consecutivo en los 20 principales mercados metropolitanos en junio, según los últimos resultados de los índices S&P CoreLogic Case-Shiller, publicados esta semana.

“El índice S&P CoreLogic Case-Shiller U.S. National Home Price NSA, que abarca las nueve divisiones censales de EE.UU., registró una variación anual del 0,0% en junio, frente a la pérdida del -0,4% del mes anterior. El índice compuesto de 10 ciudades registró un descenso del -0,5%, lo que supone una mejora respecto al descenso del -1,1% del mes anterior. El compuesto de 20 ciudades registró una pérdida interanual del -1,2%, frente al -1,7% del mes anterior”, dice el comunicado al que accedió Funds Society.

En cuando la información interanual, Chicago se mantuvo en el primer puesto con un aumento interanual del 4,2%, Cleveland en el segundo con un 4,1% y Nueva York en el tercero con un 3,4%.

Nuevamente hubo una división equitativa de 10 ciudades que informaron precios más bajos y aquellas que informaron precios más altos en el año que finaliza en junio de 2023 en comparación con el año que finaliza en mayo de 2023; 13 ciudades mostraron una aceleración de precios en relación con el mes anterior.

En la comparación mes a mes, antes del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,9% en junio, mientras que los Índices Compuestos de 10 y 20 ciudades también registraron aumentos similares del 0,9%.

Después del ajuste estacional, el Índice Nacional de EE.UU. registró un aumento intermensual del 0,7%, mientras que los Índices Compuestos de 10 y 20 Ciudades registraron aumentos del 0,9%.

“Los precios de la vivienda en Estados Unidos siguieron aumentando en junio de 2023”, afirmó Craig J. Lazzara, director general de S&P DJI. “Nuestro National Composite subió un 0,9% en junio, y ahora se sitúa sólo un -0,02% por debajo de su máximo histórico de hace exactamente un año. Nuestros Composites de 10 y 20 ciudades ganaron asimismo un 0,9% cada uno en junio de 2023, y se sitúan un -0,5% y un -1,2%, respectivamente, por debajo de sus máximos de junio de 2022”.

La recuperación de los precios de la vivienda es generalizada, según el índice. Los precios subieron en las 20 ciudades en junio, tanto antes como después del ajuste estacional. En los últimos 12 meses, 10 ciudades muestran rentabilidades positivas. Dicho de otro modo, la mitad de las ciudades de la muestra se sitúa ahora en precios máximos históricos, agrega el informe.

Acerca de S&P Dow Jones Indices

S&P Dow Jones Indices es la mayor fuente mundial de conceptos, datos e investigación esenciales basados en índices, y el hogar de indicadores icónicos de los mercados financieros, como el S&P 500® y el Dow Jones Industrial Average®. Se invierten más activos en productos basados en nuestros índices que en productos basados en índices de cualquier otro proveedor del mundo.

S&P Dow Jones Indices es una división de S&P Global (NYSE: SPGI), que proporciona inteligencia esencial para que particulares, empresas y gobiernos tomen decisiones con confianza.