Assets invested in the U.S. ETF sector reached a new record of $9.74 trillion at the end of August, according to a report by ETFGI.

The sector recorded net inflows of $66.31 billion during the month of August, bringing year-to-date net inflows to a record $643.52 billion, surpassing July’s $9.49 trillion, according to the August 2024 report.

Additionally, assets have increased by 20.1% year-over-year in 2024, rising from $8.11 trillion at the end of 2023 to $9.74 trillion, marking 28 consecutive months of net inflows, the report adds.

“The S&P 500 index rose by 2.43% in August and is up 19.53% year-to-date in 2024. The developed markets index, excluding the U.S., increased by 2.78% in August and 11.13% in 2024. Israel (+7.47%) and Singapore (+5.59%) posted the largest gains among developed markets in August. The emerging markets index rose by 2.01% in August and 10.89% in 2024. Indonesia (+10.79%) and Thailand (+8.62%) recorded the highest increases among emerging markets in August,” said Deborah Fuhr, managing partner, founder, and owner of ETFGI.

In the U.S., the ETF sector had 3,669 products by the end of August, with assets worth $9.74 trillion from 337 providers listed on three exchanges.

On the fixed income side, ETFs saw net inflows of $25.61 billion in August, bringing year-to-date net inflows to $129.54 billion, exceeding the $109.87 billion in net inflows in 2023.

Commodity ETFs registered net inflows of $715.56 million in August, putting the year-to-date net outflows at $1.73 billion, lower than the $5.8 billion in net outflows for the same period in 2023.

Active ETFs attracted net inflows of $20.67 billion during the month, bringing year-to-date net inflows to $180.4 billion, significantly higher than the $74.2 billion in net inflows in 2023.

The substantial inflows can be attributed to the top 20 ETFs by new net assets, which collectively gathered $46.13 billion in August. The Vanguard S&P 500 ETF (VOO US) gathered $7.88 billion, the largest individual net inflow, the report explains.

Miami currently holds the highest bubble risk, according to this year’s edition of the UBS Global Real Estate Bubble Index.

Driven by the luxury market boom, prices in Miami have increased by nearly 50% in real terms since the end of 2019, with 7% of that rise occurring in the last four quarters, the report adds.

The U.S. homeownership market is becoming increasingly unaffordable, as the monthly mortgage payment as a percentage of household income is now much higher than during the peak of the 2006–2007 housing bubble.

In Los Angeles, real housing prices have barely increased since mid-2023. Due to the decline in economic competitiveness and the high cost of living, the population of Los Angeles County has been shrinking since 2016. As a result, rents have not kept pace with consumer prices, the study explains.

Despite its low affordability, New York housing prices have not corrected significantly. They are only 4% below 2019 levels and have even increased slightly in the last four quarters.

The Boston housing market has seen a 20% price increase since 2019, outpacing both the local rental market and income growth. However, the local economy has recently taken a hit, particularly due to layoffs in the tech and life sciences sectors, which could signal a shift in this trend.

Globally, real estate bubble risk has decreased in the cities analyzed. In addition to Miami, Tokyo and Zurich also saw their index rise.

However, cities like San Francisco, New York, and São Paulo present a low bubble risk.

The SEC announced charges against 12 firms, including broker-dealers, investment advisers, and a dual-registered broker-dealer and investment adviser, for widespread and prolonged failures in the maintenance and preservation of electronic communications, violating the recordkeeping provisions of federal securities laws, according to the regulator’s statement.

The firms admitted to the facts outlined in their respective SEC orders, acknowledged that their conduct violated the recordkeeping provisions of federal securities laws, agreed to pay combined civil penalties totaling $88,225,000, and have begun implementing improvements to their compliance policies and procedures to address these violations.

The sanctioned firms are as follows: Stifel, Nicolaus & Company, which agreed to pay a $35 million fine; Invesco Distributors, along with Invesco Advisers, with a $35 million fine; CIBC World Markets, along with CIBC Private Wealth Advisors, which will pay $12 million; Glazer Capital with $2 million; Intesa Sanpaolo IMI Securities with $1.5 million; Canaccord Genuity with $1.25 million; Regions Securities will pay $750,000; Alpaca Securities with $400,000; Focused Wealth Management agreed to pay $325,000, and Qatalyst Partners will not pay any fine.

“Today’s enforcement actions reflect the range of consequences that parties can face for violating the recordkeeping requirements of federal securities laws. Widespread and long-standing failures, especially when they potentially impede the Commission’s investor protection function by compromising a firm’s response to SEC subpoenas, can result in substantial civil penalties,” commented Gurbir S. Grewal, Director of the SEC’s Division of Enforcement.

The SEC’s investigations into all the firms, except Qatalyst, uncovered widespread and long-standing use of unapproved communication methods, known as “off-channel communications,” within these firms.

On the other hand, firms that self-report and otherwise cooperate with the SEC’s investigations may receive significantly reduced penalties. In this case, despite recordkeeping failures involving senior management communications that persisted even after the SEC’s first recordkeeping matters were announced in 2021, Qatalyst took significant compliance steps, self-reported, and remedied the situation, resulting in a no-penalty resolution.

As outlined in the SEC’s orders, the firms admitted that during the relevant periods, their personnel sent and received off-channel communications that should have been retained as required under securities laws. The failure to maintain and preserve these records deprived the SEC of key communications during its investigations.

With the goal of expanding access to real estate investment, U.S. real estate investment manager Black Salmon completed its first tokenization of a real estate project in Florida. The transaction, carried out through Chilean fintech Wbuild’s technology, was valued at nearly one million dollars.

According to a joint statement, the two firms partnered to distribute a share of one of Black Salmon’s projects: the development of a 23-story multifamily building located in the heart of St. Petersburg, in Tampa, Florida. The building is situated next to Tropicana Field Stadium and the area’s main commercial districts and entertainment zones.

The companies hailed the operation as a success. The tokenized share was sold in just one week, for a total of nearly one million dollars. This portion represents 10% of the total project, which has an estimated annual return of between 17% and 20%.

Tokenization allowed investors to acquire a token starting at $50,000. Without this technology, the minimum external investment would have been $500,000.

As a result of this success, Black Salmon—managing over $2.1 billion in assets (AUM)—is preparing to launch another project using this method. This second asset is located in the heart of the Medical District in Miami, Florida, and involves the construction of two multifamily buildings.

The tokenization of real estate assets has become a growing trend, allowing property ownership to be divided into small digital tokens, thereby lowering the investment amounts required to access this class of alternative assets.

Jorge Escobar, co-CEO of Black Salmon, highlighted the partnership with Wbuild. The fintech’s expertise, he said in the press release, “enables high-value real estate projects from the United States to be brought closer to Latin American investors.”

Daniel Pardo, CEO of Wbuild, emphasized that the partnership enables direct participation in high-quality investment opportunities. “More family offices, companies, and individuals will be able to access diversified and flexible investment portfolios through our platform,” he commented.

Wbuild offers real estate investments in the U.S., structured as tokens. According to Pardo, in an interview with Funds Society a few months ago, these tokenized assets function as “digital shares” of a company holding the real estate assets.

Patria Investimentos announced the creation of the Reforest Fund, in partnership with Pachama, with the goal of raising up to $100 million for reforestation and degraded land restoration projects in Brazil and other Latin American countries.

The fund aims to promote the ecological recovery of these areas by using both native and unconventional exotic species, while also encouraging the bioeconomy through the sale of carbon credits, reforestation timber, and agroforestry products.

According to the announcement, the fund will be structured around two types of projects: ecological restoration, aimed at selling carbon credits, and productive restoration, which includes the sale of timber and other products like cacao and coffee, along with carbon credits. The initiative also focuses on generating social benefits, such as job creation and economic development for local communities.

“Productive ecological restoration, in addition to promoting biodiversity and ecosystem services, generates social benefits for local communities,” the company stated.

The first projects of the Reforest Fund will concentrate on the Atlantic Forest (Mata Atlântica), a highly degraded biome with significant recovery potential. Future plans include expanding to other biomes across Latin America.

The partnership between Patria Investimentos and Pachama leverages the complementary strengths of both companies. Patria contributes “best governance practices, local presence, and the ability to mobilize long-term capital,” while Pachama brings “credibility to access high-quality carbon credit buyers and proprietary technology for project origination and monitoring,” according to the statement.

José Augusto Teixeira, a partner at Patria Investimentos, stated that “this new fund is part of our strategy to expand our product portfolio, complementing our offering with an alternative asset class in which we do not yet operate.” He emphasized that the fund’s projects combine differentiated returns with a positive impact on society and the environment. “The projects respect the environment while delivering positive social and economic impacts for communities,” he added.

The fund marks Patria’s entry into a new segment of sustainable investments, aligning with the growing interest in long-term environmental and social solutions in Latin America.

Brookfield Oaktree Wealth Solutions, a global provider of alternative investments, is expanding its presence in the wealth management sector in Latin America, with DAVINCI Trusted Partner leading support and marketing efforts for private placement in Argentina and Uruguay, both firms announced in a statement.

DAVINCI Trusted Partner announced its strategic alliance with Brookfield Oaktree Wealth Solutions to offer alternative investment solutions to financial advisors and private banking in Argentina and Uruguay. Brookfield Oaktree Wealth Solutions’ parent company, Brookfield, manages approximately $1 trillion in assets, with a distinguished track record and notable expertise in Real Estate, Infrastructure, Private Equity, Credit, and Renewable Power & Transition.

“We view DAVINCI as an extension of our support team in Latin America. We are fortunate to partner with them as they share our commitment and passion for serving our clients in the region,” said Oscar Isoba, Managing Director and Head of LatAm at Brookfield Oaktree Wealth Solutions.

“The combination of Brookfield Oaktree Wealth Solutions’ global scale with DAVINCI’s local expertise will enable us to offer our investment capabilities to wealth advisors and private banks in the region, with a focus on education about alternative investments and how advisors can position these unique strategies in their clients’ portfolios. We are very excited to bring these solutions to Argentine and Uruguayan investors, and we look forward to expanding our reach to other countries in the region,” Isoba added.

Santiago Queirolo, Managing Director of DAVINCI Trusted Partner, highlighted: “We are fully committed to our clients, and our main objective is to help financial institutions assess the best investment solutions available in the market. There is growing interest in alternative investments in the wealth management sector, seeking to diversify traditional portfolios and enhance long-term returns. With this strategic alliance with Brookfield Oaktree Wealth Solutions, we will help financial institutions navigate the alternative investment universe with the goal of educating while introducing the best alternative investment solutions.”

“We are very excited about this alliance with Brookfield Oaktree Wealth Solutions, one of the most prominent firms in the credit and private assets market. This agreement will allow us to offer the best alternative investment solutions to intermediaries in Argentina and Uruguay,” said James Whitelaw, Managing Director at DAVINCI TP.

DAVINCI Trusted Partner specializes in the independent distribution of investment funds in Latin America, providing access to investment solutions from leading global managers. With a highly experienced team and deep knowledge of the regional regulatory framework, it offers specialized consulting to financial intermediaries, establishing itself as a trusted partner in the region.

Brookfield Asset Management is a global alternative asset manager. It invests clients’ capital for the long term, with a focus on real assets and essential service businesses that form the backbone of the global economy. It offers a wide range of alternative investment products to clients worldwide, including public and private pension plans, endowment funds and foundations, sovereign wealth funds, financial institutions, insurance companies, and private wealth investors.

Photo courtesyAlberto Burs, Offshore Vice President at Inviu

Asset management has undergone substantial transformations in recent decades, driven by technological advancements, globalization, and the evolution of financial markets. Today, the industry faces an increasingly dynamic environment, with investors demanding not only attractive returns but also sustainable and responsible strategies. In this context, adaptability and innovation are key to addressing future challenges.

As part of the Key Trends Watch, a joint initiative by FlexFunds and Funds Society, the aim is to provide insight into the changes and challenges in the asset management industry through the perspective of leading professionals. This time, we spoke with Alberto Burs, Offshore Vice President at Inviu, about emerging trends, sector challenges, and opportunities.

Alberto Burs was appointed Offshore Vice President at Inviu in March 2024, where he leads the development of the international business and provides services to financial advisors in several Latin American countries. With over a decade of experience in the sector, he was previously Sales Manager at Compass Argentina and worked as an independent financial advisor. He holds a degree in Public Accounting and Business Administration from the Pontifical Catholic University of Argentina and a master’s degree in Finance from the University of Torcuato Di Tella.

For Burs, Inviu is a project that has redefined his professional career. “I was invited to join and discovered a completely new vision of the industry. At Inviu, we are doing something unique. Perhaps XP in Brazil has developed something similar, but there is nothing like this in the region.” He highlights that, thanks to the backing of Grupo Financiero Galicia and an innovative technological platform, Inviu has positioned itself as a leader within its industry in Argentina, and its next goal is to expand this offering to the rest of Latin America.

Regarding the main challenges he faces as VP Offshore at Inviu, Burs emphasizes that one of the most important is the resistance of advisors to change their traditional platforms. “The main challenge is convincing advisors, who have been working with the same broker for 10 or 15 years, to try something new. We know that once they try our platform, the service they offer their clients will improve significantly.”

The Inviu platform is the core of their offering. Burs explains that integration with Pershing and Interactive Brokers allows them to offer advisors unified access to both local and offshore markets, something that in countries like Argentina provides great added value. “Technology is our differentiator. It not only enables the integration of markets and the various investment banks we have agreements with but also prepares the platform to include new trends like crowdfunding and cryptocurrencies.”

Main trends

The expert points out that alternative assets are gaining prominence, especially after the challenging year of 2022, when both stocks and bonds fell without offering any refuge. “The alternative world has solidified as a key asset class for diversifying portfolios. Today, the correlation between bonds and stocks is high, so having alternatives is essential.”

While he acknowledges that retail market allocation to alternative assets is still low, he believes it could increase to as much as 20-30% without affecting portfolio liquidity. “Private credit is one of the strategies with the most appetite due to the attractive risk-return it offers compared to public fixed income.”

“I believe there are two key factors that clients prioritize today: risk and liquidity. However, the importance of liquidity is gradually decreasing, which is leading to the resurgence of the world of alternative assets,” he adds regarding the factors most important to clients.

When asked about the future of the industry, Burs highlights the growing relevance of separately managed accounts (SMAs) over collective investment vehicles. “Managed accounts allow advisors to delegate decisions to professionals, with a more personalized and flexible approach than mutual funds or ETF portfolios.”

He also firmly believes that technology will transform the way small investors access global markets. “Technology will allow any investor, regardless of size, to invest in assets such as bonds, stocks, SPVs, real estate, or cryptocurrencies. This is the future of asset management: a platform that integrates all investment options. This is where we want to go with Inviu.”

The role of artificial intelligence in the sector

Burs is also optimistic about the impact of artificial intelligence on the sector. “I believe AI will be useful, but it will not replace advisors. It will be key for investment strategies and, above all, for helping to accurately identify clients’ risk profiles, avoiding unpleasant surprises during times of volatility.”

The asset management sector continues to evolve rapidly, driven by technological innovation and the growing demand for diversified and accessible investment products. Burs and his team at Inviu are at the forefront of this transformation, leading with a platform that promises to integrate all investment alternatives in one place and with a clear vision that the future lies in adapting to new trends and investor needs.

Interview conducted by Emilio Veiga Gil, Executive Vice President of FlexFunds, as part of the Key Trends Watch by FlexFunds and Funds Society.

Pixabay CC0 Public Domain rus-burkhanov from Pixabay

Since the end of 2021, the high yield bond markets have weathered an unprecedented storm. The sudden change in the interest rate regime left its mark, and the ICE BofA BB-B Global High Yield Index saw its value plummet by $654 billion, reducing its size by more than a quarter, from $2,510 billion to $1,856 billion[1].

Why such a contraction? There are three main factors that explain this earthquake in the high yield space.

Firstly, rising interest rates have prompted many companies to reduce their debt levels, preferring to focus on stability rather than expansion through mergers and acquisitions or share buy-backs. This caution has led to a reduction in the supply of new bonds.

Secondly, the best-rated companies in the high yield segment have sought to improve their ratings in order to move into the investment-grade category and thus benefit from more advantageous debt costs.

Thirdly, rate hikes have increased default rates, as some indebted companies are no longer viable in the current environment.

Looking ahead, we expect this trend to continue, albeit at a slower pace. Businesses, though less inclined to take on debt, are beginning to adopt behaviors that could generate a positive net credit supply. However, private debt, offering higher rates, is increasingly competing with high yield bonds, exacerbating the scarcity of supply. In Europe, some companies shine like “rising stars”, but in the United States, opportunities are more limited, requiring greater selectivity. Default rates are likely to remain high, as companies face higher refinancing costs.

How can investors navigate this tumultuous environment? We recommend three rules:

Focus on fundamentals: in an uncertain macroeconomic environment, it’s crucial to stay focused on fundamentals and prepare for greater dispersion.

Move from beta to alpha: as credit spreads tighten, now is the time to focus on active, alpha-seeking strategies, rather than passive ones.

Favoring a global approach: in a contracting market, investors should broaden their investment universe and favor a global approach, enabling greater diversification and more opportunities.

Candriam Bonds Global High Yield: Our tailor-made solution

Our fund, Candriam Bonds Global High Yield, is designed to exploit the unique opportunities offered by high yield bonds. Through sector and maturity diversification, this fund aims to outperform investment grade bonds. Faced with higher default rates, the expertise of our dedicated team of analysts is essential to navigate this complex market.

Our strategy is based on three pillars:

Global vision: we cover the two largest markets (USA and Europe) and a wide range of instruments (high yield, investment grade, fixed and floating rate bonds, derivatives).

Active management: our positions are actively managed, with strong convictions based on in-depth fundamental, legal and quantitative analysis.

Prudent risk management: we apply rigorous risk management, closely monitoring liquidity, sovereign, extreme, volatility and credit risks. We also use asymmetrical products, such as options, to hedge our positions.

Our selection of issuers is based on rigorous fundamental research incorporating ESG factors. Each issuer receives an internal credit rating, enabling us to assess its creditworthiness and default risk, with particular attention paid to extra-financial criteria.

We go beyond traditional investor boundaries by exploring opportunities between the investment grade and high yield segments. This flexibility enables us to dynamically adjust the overall duration of our portfolio to suit different market conditions.

In times of uncertainty, our in-house legal expertise and understanding of the intricacies of contractual provisions are essential to managing risk. The important thing is not to take any ill-considered risks. The result of our risk approach is a zero default rate.

The world is increasingly dominated by key trends, such as digitalization, bipolarization and decarbonization, which are profoundly transforming economic relationships and are likely to significantly disrupt financial markets. Combined with the interventions of central banks that may be pursuing policies counter to the fiscal policies of governments, these trends are a source of concern for investors and are creating volatility in the money and bond markets.

In such a context, outperformance will depend on diversification, selectivity and active management to maintain a controlled and calibrated investment risk . We remain focused on finding promising opportunities, supported by rigorous fundamental research that integrates ESG factors. The harmonious collaboration between our portfolio managers, ESG analysts and credit analysts has been key to our success in managing high yield bond strategies over the past twenty years.

Opinion article by Nicolas Jullien,Head of High Yield & Credit Arbitrage at Candriam.

Fed Rate Cuts Will Ease Pressure on U.S. Real Estate Market, but Mortgage Rates Unlikely to Fall Below 5% Before 2027, According to Fitch Ratings

The 30-year fixed mortgage rate and the 10-year Treasury yield have already priced in the Federal Reserve’s 50 basis point rate cut. Even with additional rate cuts, a decline in the 30-year mortgage rate to around 5% depends on the spread with the 10-year Treasury bond returning to the pre-pandemic average of 1.8 percentage points.

Fitch analysts note that the 10-year yield has less room to fall following rate cuts, especially after this summer’s declines in anticipation of monetary policy easing. They expect the 10-year yield to end 2026 around 3.5%, down slightly from its current level of around 3.7%. A 3.5% 10-year Treasury yield plus the historical average spread of 1.8 percentage points results in a mortgage rate of around 5.2%.

The spread between the 30-year mortgage rate and the 10-year Treasury yield has widened relative to the historical average since the Fed began raising policy rates in March 2022. This reflects a higher prepayment risk and the Fed’s reduction in its holdings of mortgage-backed securities (MBS). The spread peaked near 3% in November 2023 when the average 30-year fixed mortgage rate reached a cycle high of 7.8%. It has since narrowed slightly, averaging 2.6 percentage points since January 2024.

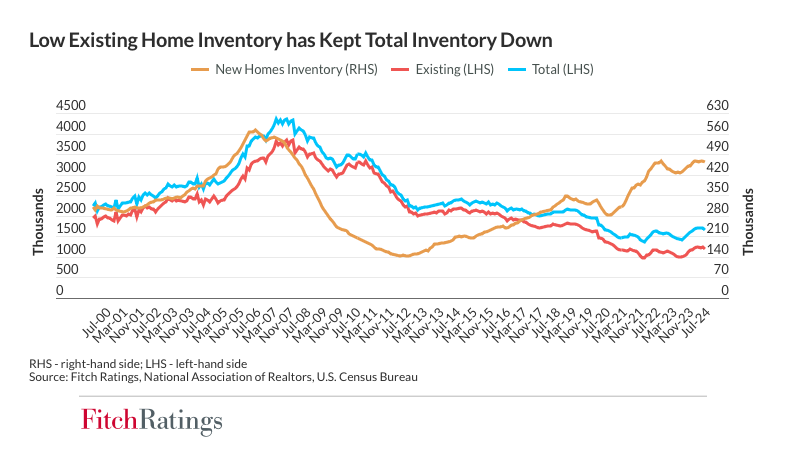

Demand Remains Above Averages

Housing demand, as measured by homes sold above the list price and the average sale price relative to the list price, has softened since August 2023 but remains above long-term averages. A further decline in mortgage rates will help improve affordability and support demand, but low inventory will likely constrain home sales until rates approach 5%.

Around 24% of outstanding mortgages have rates above 5%. As mortgage rates approach that figure, likely by 2026, homeowners with these higher-rate mortgages, along with those with rates between 4% and 5% (around 19% of outstanding mortgages), should become more willing to sell their homes and take on a new mortgage, according to Fitch Ratings.

Housing Supply Needs to Improve

According to Fitch, “Total U.S. inventory has broadly increased this year, but it remains below pre-pandemic levels, driven by a 27% drop in existing home supply since February 2020. While the new home inventory has grown by 29% since the start of the pandemic, the supply of existing homes, which accounts for roughly 80% of home sales, needs to improve in order to enhance pricing and market activity.”

Mortgage originators are already benefiting from higher volumes as refinancing activity has gradually recovered with the decline in mortgage rates. Homeowners with mortgage rates above 6%, representing 14% of outstanding mortgages or roughly $1.5 to $2 trillion, are in a prime position to refinance as the average 30-year rate approaches 6%.

BNP Paribas has announced the signing of an agreement with HSBC to acquire its private banking activities in Germany. The deal aims to position BNP Paribas Wealth Management among the leading players in Germany and raise the amount of assets under management to over 40 billion euros (around 45 billion dolars).

Germany, a key geography for BNP Paribas, offers significant growth potential for wealth management activities, particularly within the “mittelstand” segment (German SMEs), as well as with entrepreneurial clients and German families. Leveraging BNP Paribas’ diversified and integrated business model, BNP Paribas Wealth Management aims to provide these entrepreneurial clients with a comprehensive service offering, ranging from investment and corporate banking to asset management, drawing on BNP Paribas’ well-established franchises.

HSBC’s private banking activities, primarily focused on HNW and UHNW clients, and with a complementary regional presence, especially in North Rhine-Westphalia, fit perfectly within BNP Paribas Wealth Management’s model. This will allow BNP Paribas to rank among the top wealth managers in the country, according to the statement from the French firm.

BNP Paribas Wealth Management, part of the Investment and Protection Services division, is the leading private bank in the eurozone, with global assets of 446 billion euros (498 billion dolars) as of the end of June 2024.

The transaction is expected to close in the second half of 2025, pending regulatory approvals.

“This acquisition is a crucial step in positioning BNP Paribas Wealth Management among the leading players in Germany, where we believe our model is best suited to meet the long-term needs of entrepreneurial clients, leveraging the Group’s strong franchises to meet both their personal and corporate needs. It will, therefore, contribute to consolidating our position as the leading wealth management player in the eurozone,” said Vincent Lecomte, CEO of BNP Paribas Wealth Management.

Lutz Diederichs, CEO of BNP Paribas Germany, added, “Germany is a key strategic market for BNP Paribas, with a local presence of over 75 years. Our twelve business lines make our business model one of the most diversified and resilient in the German banking sector. Developing our wealth management franchise is an integral part of our growth plan in the German economy. Wealth Management in Germany serves as a gateway for our clients to the full range of services offered by the BNP Paribas Group, particularly in Corporate & Institutional Banking, Real Estate, Asset Management, and Securities Services.”