The independent and hybrid registered investment advisor (RIA) channels are growing at a faster pace than other brokerage channels. To capitalize on this opportunity, asset managers are expanding their coverage models and the depth of their resources for larger RIAs, according to the latest Cerulli Edge-U.S. Advisor Edition report.

The total number of independent and hybrid RIAs has surged in the past decade, rising from 18% to over 27%, and is expected to exceed 30% within the next five years.

Advisors with varying levels of experience and assets have made the switch, but RIAs with more than $1 billion in assets under management have experienced the greatest expansion.

With this growth, asset managers are enhancing their coverage models, expanding their service menus to better cater to these massive RIAs.

Currently, more than two-thirds of asset managers offer or plan to offer dedicated key account coverage, institutional pricing, and client-facing marketing materials to the largest RIAs.

At least 75% of asset managers are using or planning to use dedicated key account coverage to aid in distribution efforts with the largest RIA firms. However, these resources are no longer sufficient compared to the more complex resources advisors now expect from the industry.

“It is no longer a competitive advantage to simply provide key account coverage or make client-facing marketing materials more user-friendly,” says Kevin Lyons, senior analyst.

Advisors are seeking more intricate resources that can truly benefit their practice by making it more efficient, he added.

As a result, distribution executives at asset managers have also begun to focus on other services: nearly 70% currently offer or plan to offer portfolio construction/model construction services or investment analysis tools.

More than half (52%) offer or plan to offer business consulting resources (e.g., succession planning, growth strategies, team structuring).

“Wave after wave of advisors is joining the independent channel, coming from firms and channels that often provided portfolio analysis tools, consulting expertise, and investment analysis as part of their advisor affiliation. Asset managers understand the need to prioritize coverage in the RIA space and help fill any gaps in research or even administrative services that their former firms provided,” says Lyons.

As more experienced advisors migrate to independent and hybrid RIA channels, asset managers can seize the opportunity by deepening their competitive positioning through the quality of the resources they offer, making themselves more attractive potential partners for advisors, concludes the expert.

BlackTORO Global Wealth Management and SORO Wealth announced this Wednesday a strategic alliance to jointly offer comprehensive investment and wealth management solutions to Mexican individuals and families.

SORO Wealth, based in Monterrey, “is defined by its excellence and innovation in providing wealth management advice to Mexican individuals and families, including corporate legal services, family governance definition, and legal advice on private equity and venture capital structures and transactions,” according to the statement accessed by Funds Society.

“This agreement marks an important step in our efforts to provide high-quality, value-added services to our clients in Latin America. The combination of our strengths will enable us to offer differentiated and long-term investment solutions to Mexican investors from the U.S.,” said Gabriel Ruiz, partner and president of BlackTORO.

BlackTORO has fiduciary responsibility and aims to provide independent, globally aligned investment advice that meets the high standards sought by Latin American individuals and families when investing their wealth. Their personalized services include investment portfolio advice and management and access to leading U.S. financial entities for custody and execution, with preferential conditions and costs, according to the firm’s statement.

The BlackTORO team has an “extensive track record in the financial industry, bringing essential experience and knowledge to the success of this strategic alliance,” the statement adds.

“This alliance will allow us to cross our borders and provide comprehensive and efficient wealth management services to our clients,” commented Mario Sosa, partner of SORO Wealth.

Latin America and the Caribbean have seen a greater share of U.S. development assistance during Joe Biden’s administration, which has had a notable impact on the environmental sector, elevating it from third to second place in budget allocation, according to a BBVA report.

While the government and civil society sector has held the top spot for assistance to Latin America and the Caribbean under both Donald Trump and Joe Biden, environmental assistance has risen from third to second place in terms of the proportion of funding allocated during Biden’s administration.

Differences can also be seen between the Trump and Biden administrations regarding the purposes for which environmental assistance has been allocated.

Trump focused more on agricultural policy activities, rural development, and water, whereas Biden has placed greater emphasis on biodiversity.

For instance, environmental protection policies were dominant in both administrations, but this focus is more pronounced under Biden, who has allocated 59.4% of environmental assistance to this area, over 10 percentage points higher than his predecessor. Under Trump administration, environmental protection policies received 48.5% of environmental assistance, the bank adds.

Another noteworthy point is that during Trump’s presidency, agricultural policy and rural development (including activities such as promoting agroforestry systems and food security) had a larger share of environmental assistance, with 38.2% allocated to this purpose. Along with water and sanitation activities, which accounted for 8.9% of environmental aid, these two areas together comprised 47.1% of assistance in this sector.

Under Biden, the share of agricultural policy and rural development has decreased to 18.1% of environmental assistance. In contrast, funding for biodiversity, which was in fourth place under Trump, has risen to third place under Biden, accounting for 9.6% of environmental assistance. Multisectoral aid has also gained more importance under Biden, representing 6.6% of environmental assistance, while the proportion focused on water and sanitation has decreased from 8.9% under Trump to 4.1% under Biden.

Regarding the distribution by country in Latin America and the Caribbean, during Donald Trump’s administration, four countries accounted for two-thirds of the aid in this sector: Haiti (20.2%), Colombia (16.2%), Guatemala (14.3%), and Honduras (7.4%).

Under Biden, six countries now represent two-thirds of environmental assistance: Colombia, which has risen to first place with 17.6%; Guatemala, which has moved from third to second place with 11.6% of aid; Haiti, which has dropped from first under Trump to third under Biden with 11.5%; Honduras, which remains in fourth place with 10.2% of assistance in this sector; Brazil, which under Trump was in seventh place, now rises to fifth with 6.9%; and finally Mexico, which has moved from eighth place under the Republican administration to sixth, representing 6.4% of aid for the sector.

Overall, U.S. aid to the region is distributed as follows: 29.7% for Government and Society sectors, 18.6% for Environmental Assistance, 12.1% for Emergency Response, and 11% for Conflicts, Peace, and Security.

Countries Receiving the Most Aid Across All Sectors

Donald Trump provided the most assistance to Colombia, with 33.2% of aid received, followed by Haiti with 15.5%, and Mexico in third place with 10.4% of the total received. Hemispheric projects, those involving participation from Latin American and Caribbean countries along with counterparts in North America, accounted for 7.3%, while Peru ranked fifth with 5.9% of the assistance received.

Biden, on the other hand, has prioritized hemispheric projects in general, with 31.5% of aid provided so far by his government to the region. Colombia follows in the next position, with a 17.7% share, ahead of Haiti (9.6%), Guatemala (5.3%), and Honduras (4.7%).

Thus, Mexico has dropped from third place in aid received under Trump to sixth place during Biden’s administration, mainly due to increased focus on Central America, with Guatemala and Honduras in the current administration. Another point to highlight is the reduction in Colombia’s share, which under Trump represented 33.2% of the aid received in the region, while under Biden, it has almost halved to 17.7% of the total disbursed to Latin America and the Caribbean.

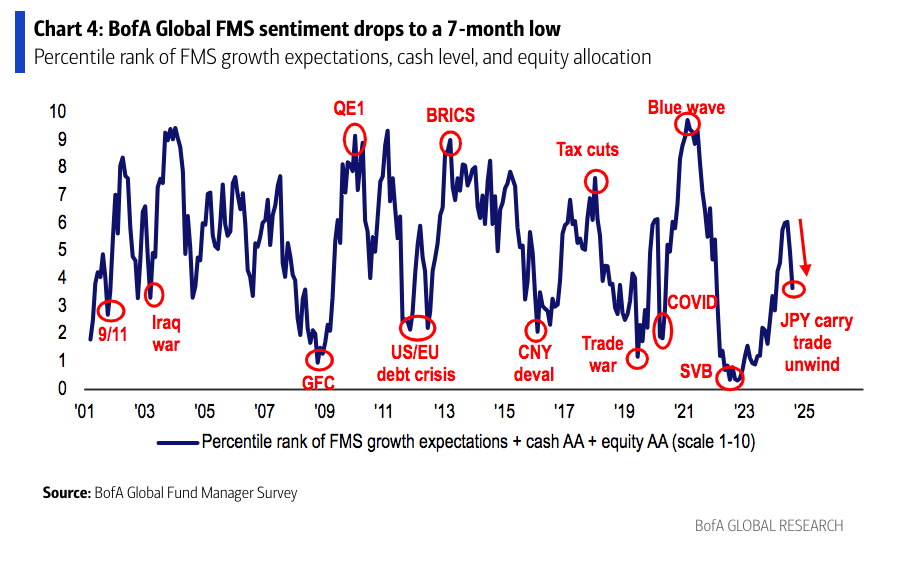

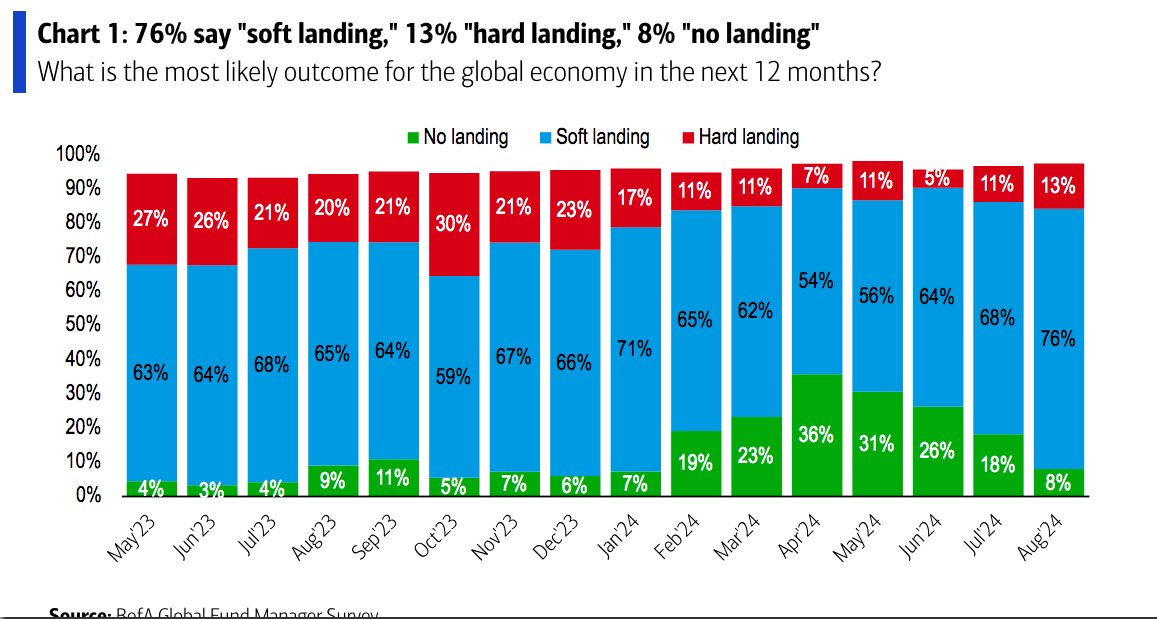

Despite the market correction in early August, investor optimism has not been affected. According to BofA’s monthly manager survey, 76% continue to expect a soft landing and a Fed action, now, of four or more cuts to ensure that this expectation of a soft landing is met.

However, the survey picks up that global growth expectations in the August survey fell sharply by 20% compared to July, in fact a net 47% of respondents expect a weaker global economy in the next 12 months. “Growth expectations and risk appetite declined in recent weeks due to the yen volatility shock and weak July employment data,” notes the BofA survey.

As a result, investors increased cash levels again for the second consecutive month, rising from 4.1% to 4.3%. “Our broader measure of FMS sentiment, based on cash levels, equity allocation and economic growth expectations, fell to 3.7 from 5.0 last month,” the firm notes.

As for monetary policy, 55% of investors believe that globally it is too restrictive, the highest figure since October 2008. In this regard, they point out that investors’ belief that policymakers should ease quickly is driving expectations of lower rates, which is why 59% expect lower bond yields, the third highest figure on record (after November and December 2023). Bond yield expectations are also lower, a sentiment that has been increasing month-over-month.

Coupled with monetary policy expectations is the conviction that a “soft landing” of the economy will be achieved, a conviction driven by the likelihood of lower short-term interest rates. Specifically, 93% of FMS investors expect lower short-term rates 12 months from now, the highest figure in the past 24 years.

Asset Allocation

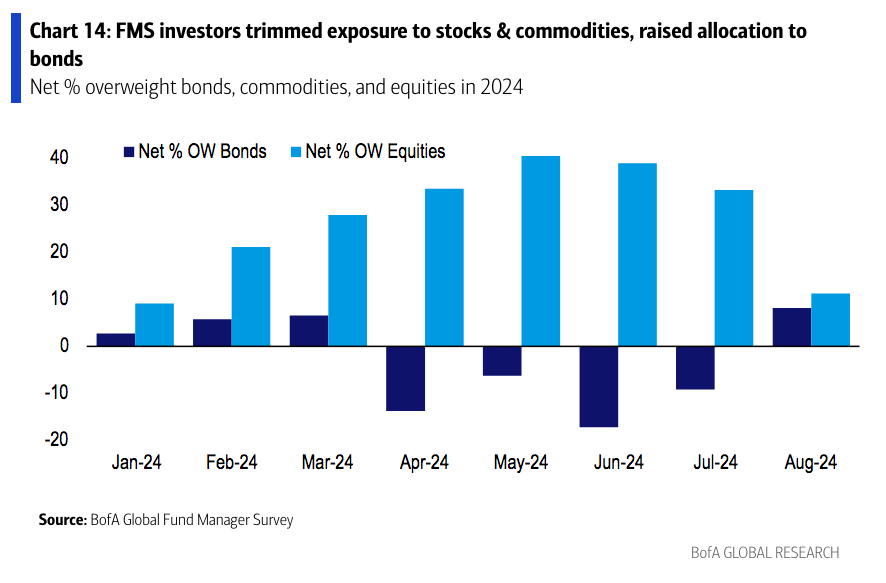

When it comes to talking about allocation within investors’ portfolios, the survey shows that in August investors rotated into bonds and out of the equity market. “The allocation to bonds increased to 8% overweight from 9% underweight. This is the highest allocation since December 2023 and the largest monthly increase since November 2023. In contrast, the allocation to equities fell by 11%, which is the lowest allocation since January 2024 and the largest monthly decline since September 2022. Notably, in absolute terms, 31% of FMS investors said they were overweight in equities, down from 51% who said so in July.

“In August, investors increased allocation to bonds, cash and health care and reduced allocation to equities, Japan, the Eurozone and materials. Investors are more overweight in healthcare, technology, equities and the U.S., and more underweight in REITs, consumer discretionary, materials and Japan. Relative to history, investors are long bonds, utilities and healthcare and are underweight REITs, cash, energy and the Eurozone,” BofA notes.

Finally, two curious tidbits of information left by this month’s survey is that the largest regional equity allocation was to the U.S., while the allocation to Japanese equities experienced the largest one-month drop since April 2016. “As a result, global managers’ allocation to U.S. equities relative to Japanese equities increased to the highest level since November 2021,” the survey concludes.

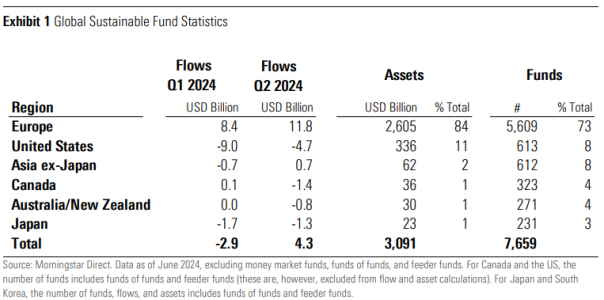

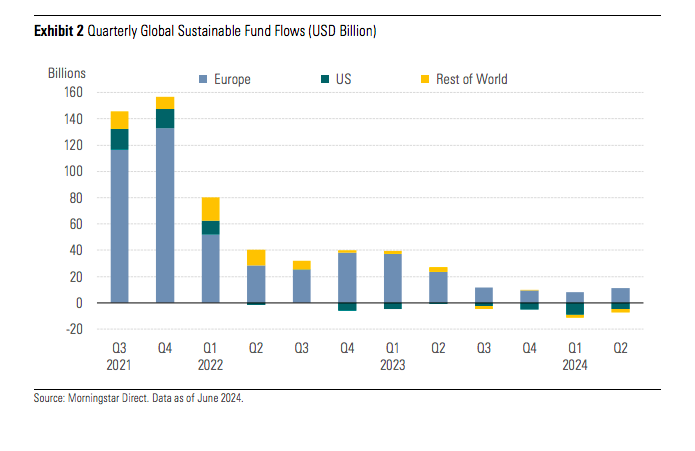

In the second quarter of 2024, the global universe of sustainable funds—which includes open-end funds and ETFs—received $4.3 billion in inflows, compared to the $2.9 billion in outflows experienced in the first quarter of the year. Does this mean that investors are returning to sustainable funds?

“The outlook for global ESG fund flows is starting to improve. We began the year with outflows, but this has since changed, with money returning to the sector. European ESG funds have gathered more than $20 billion so far this year. Across the pond, investor appetite for ESG funds remains moderate, with continued outflows, but these were smaller than those seen in the previous two quarters,” explains Hortense Bioy, Head of Sustainability Research at Morningstar Sustainalytics.

The report indicates that calculated as net flows in relation to total assets at the beginning of a period, the organic growth rate of the global sustainable fund universe was 0.14% in the second quarter, a slight improvement from the 0.01% rate in the previous quarter. “However, the aggregate growth of sustainable funds lagged behind the broader fund universe, which with $200 billion in inflows, recorded an organic growth rate of 0.4%,” the report notes.

To put this in context, the Morningstar Global Markets Index achieved a 2.6% gain in the second quarter, while fixed-income markets, represented by the Morningstar Global Core Bond Index, fell 1.2%. “Europe represents 84% of global sustainable fund assets, and the United States maintained its status as the second-largest market. With total assets of $336 billion, it held 11% of global sustainable fund assets, reflecting the distribution observed three months ago,” the report states.

Specifically, European sustainable funds raised $11.8 billion, compared to the $8.4 billion recorded in the previous quarter. The report also noted a reduction in outflows in Japan, while sustainable funds in Asia continued to attract new net money.

Lastly, it highlights that product development continued on a downward trajectory, with only 77 new sustainable fund launches in the second quarter of 2024, “confirming the normalization of sustainable product development activity after three years of high growth during which asset managers rushed to build their sustainable fund ranges to meet the growing demand from investors,” the report indicates.

Asset managers now know how to navigate their way into the portfolios of Zest and XP, the strategic alliance between two brands aiming to conquer the Latin American Wealth Management client segment. The two firms held their first Investment Committee meeting on Monday, August 12.

According to a statement sent to Funds Society, “the purpose of the Committee is to analyze the global economy to define an investment thesis in line with current conditions. This investment thesis is expressed in model portfolios, according to the different risk profiles defined by the Committee’s policy.”

Jonathan Kleinberg, Asset Management Manager at Zest, emphasized the importance of this alliance and the added value it brings to the analysis and decision-making process.

“This committee is fundamental to our alliance with XP. Incorporating diverse perspectives and knowledge on the global economic situation is crucial to recommending the best positioning to our clients, always aligned with their investment objectives and risk profiles,” Kleinberg stated.

Together, the combined Zest and XP teams have 50 analysts focusing on global trends and the situation in Latin America. The committee meets quarterly and monitors investment theses with a focus on wealth preservation.

During the inaugural Committee meeting, the current and future dynamics of the U.S. monetary situation were analyzed, a crucial factor influencing global markets and, consequently, the economies of Latin America.

It was highlighted during the meeting that, following a very strong economic cycle in the U.S., characterized by a rapid increase in prices, the economy has begun to slow down. The risks of a potential recession have increased, although if it materializes, it is expected to be mild and allow for a subsequent recovery. The Federal Reserve could begin a cycle of rate cuts starting in September, with a possible aggressive decrease of 50 basis points, followed by more cuts in November.

Alberto Bernal, Chief Global Strategist at XP, clarified that “although the slowdown is evident, we do not see structural signs suggesting a deep recession. We expect the Federal Reserve’s monetary policy to act as a necessary relief for the U.S. economy, which will directly impact Latin American markets.”

Zest powered by XP is a financial services platform that provides access to international capital markets. It currently manages over 5,000 clients and 80 financial advisors. The group’s business focus is on financial education and high-tech solutions.

XP Inc. comprises one of Brazil’s largest investment platforms, with a presence in major financial centers around the world. XP owns brands such as XP, Rico, Clear, XP Educação, InfoMoney, among others. XP Inc. has 4.6 million active clients and more than 200 billion dollars in assets under custody. For 23 years, the group has been transforming the Brazilian financial market to improve people’s lives. A pioneer in the market with its network of investment advisors, which is now the largest in the country, with more than 14,000 professionals. For more information, visit the website.

Janus Henderson Group announced that it has entered into a definitive agreement to acquire a majority stake in Victory Park Capital Advisors, a global private credit manager.

With a nearly two decade-long track record of providing customized private credit solutions to both established and emerging businesses, “VPC complements Janus Henderson’s highly successful securitized credit franchise and expertise in public asset-backed securitized markets, and further expands the Company’s capabilities into the private markets for its clients”, the statement said.

VPC invests across industries, geographies, and asset classes on behalf of its long-standing institutional client base. VPC has specialized in asset-backed lending since 2010, including in small business and consumer finance, financial and hard assets, and real estate credit. Its suite of investment capabilities also includes legal finance and custom investment sourcing and management for insurance companies.

In addition, the firm offers comprehensive structured financing and capital markets solutions through its affiliate platform, Triumph Capital Markets. Since inception, VPC has invested approximately $10.3 billion across over 220 investments , and has assets under management of approximately $6.0 billion, according the firm information.

Janus Henderson expects that VPC will complement and build upon Janus Henderson’s $36.3 billion in securitized assets under management globally, the press release adds.

“As we continue to execute on our client-led strategic vision, we are pleased to expand Janus Henderson’s private credit capabilities further with Victory Park Capital. Asset-backed lending has emerged as a significant market opportunity within private credit, as clients increasingly look to diversify their private credit exposure beyond only direct lending. VPC’s investment capabilities in private credit and deep expertise in insurance align with the growing needs of our clients, further our strategic objective to diversify where we have the right, and amplify our existing strengths in securitized finance. We believe this acquisition will enable us to continue to deliver for our clients, employees, and shareholders,” said Ali Dibadj, Chief Executive Officer of Janus Henderson.

This acquisition marks another milestone in Janus Henderson’s client-led expansion of its private credit capabilities following the Company’s recent announcement that it will acquire the National Bank of Kuwait’s emerging markets private investments team, NBK Capital Partners, which is expected to close later this year, the firm says.

“We are excited to partner with Janus Henderson in VPC’s next phase of growth. This partnership is a testament to the strength of our established brand in private credit and differentiated expertise, and we believe it will enable us to scale faster, diversify our product offering, expand our distribution and geographic reach, and bolster our proprietary origination channels,” said Richard Levy, Chief Executive Officer, Chief Investment Officer, and Founder of VPC.

The acquisition consideration comprises a mix of cash and shares of Janus Henderson common stock and is expected to be neutral-to-accretive to earnings per share in 2025 and is expected to close in the fourth quarter of 2024 and is subject to customary closing conditions, including regulatory approvals.

Artificial Intelligence made headlines in 2023, but where is it headed now? ChatGPT and other generative AI tools have directly benefited a handful of stocks so far. According to Allianz GI, the next wave of AI advancements should expand opportunities to other companies within the ecosystem.

“This initial buildout of AI infrastructure lays the critical foundation for further disruptions as companies across various sectors leverage generative AI capabilities,” they argue.

According to Allianz GI’s latest report, the next phase of generative AI adoption and growth should benefit a broader ecosystem, including AI applications and AI-enabled industries in the coming years. “We are still in the early stages of AI infrastructure buildout and generative AI adoption. Unlike previous innovation cycles, where agile startups disrupted larger incumbents, this time, tech giants have been the initial beneficiaries. These tech giants have more resources, unique data sources, and significant infrastructure capabilities to train large language models (LLMs) and seize early opportunities with generative AI,” the manager notes.

So far, they believe that much of the outperformance in stocks has been concentrated in a select group of AI infrastructure and tech giant companies in this initial phase. Specifically, a handful of semiconductor companies whose accelerated computing chips are crucial for AI training, and major hyperscale internet and cloud providers who quickly leveraged generative AI and showed some early monetization.

“Continued developments in generative AI and large language models (LLMs) have driven much stronger demand for AI infrastructure so far, causing some supply constraints as hyperscale cloud platforms invest heavily to meet the rising demand from corporations and governments worldwide. Demand is expanding into other areas like next-generation networks, storage, and data center energy infrastructure to support the explosive growth of new AI workloads,” the report comments.

Allianz GI also observes a new wave of AI applications incorporating generative AI capabilities into their software to drive more value and automation opportunities. “Many companies in AI-enabled industries are also increasing investments in generative AI to train their own industry-specific models on proprietary data or insights to better compete and innovate in the future,” they state.

However, they warn that many of these new AI use cases are still in the pilot development phase and are not yet monetizing or contributing to earnings. They explain that, along with higher interest rates for a longer period in 2024, there has been greater dispersion in stock performance between infrastructure, software/applications, and other sectors so far this year. The market is taking a wait-and-see approach to valuing the benefits of generative AI in the broader ecosystem at this time. Allianz GI expects more clarity on the impact in the coming year as new applications and use cases emerge with each generation of better AI chips and as these AI models become smarter.

“In general, the AI innovation cycle is just beginning. The initial buildout of AI infrastructure sets the stage for more companies across various industries to leverage generative AI capabilities and catalyze the next phase of adoption and growth. In this next phase of disruption and change, there will be significant opportunities to generate alpha through active stock selection in AI applications and AI-enabled industries,” they conclude.

Photo courtesyAlberto Silva, Director of Multifamily Office at BTG Pactual Chile

Today, given the economic context marked by high levels of uncertainty, wealth management has gained relevance among managers, as it allows them to maximize and preserve the value of their clients’ assets through personalized financial and investment strategies. This includes protecting wealth by mitigating risks through diversification and selecting assets resistant to fluctuations. Additionally, it focuses on ensuring sufficient resources for retirement and facilitating efficient wealth transfer to future generations. Wealth management also involves continuous adaptation to personal and market changes, always maintaining alignment with clients’ long-term goals and safely leveraging financial innovations.

Alberto Silva, a Chilean native, is the new Director of Multifamily Office at BTG Pactual Chile. With over 18 years of experience in the financial industry, he was a portfolio manager in fixed income, equity, and structured products. His transition to wealth management was driven by a desire to develop commercial and soft skills, in addition to his active management experience.

What are the biggest challenges you currently face as Director of Multifamily Office at BTG Pactual Chile?

The main challenge is to provide highly personalized and comprehensive service to high-net-worth families while maintaining a solid track record in an increasingly volatile and complex financial environment. Additionally, we face growing competition due to the emergence of advisors and small offices, along with technological advances that have intensified competition and reduced fees in the industry.

What strategies do you consider key for growth and sustainability in the asset and wealth management sector, especially in Chile?

It is essential to understand the changing needs of clients in a complex geopolitical and demographic environment. At BTG Pactual Chile, we focus on developing business in the region, leveraging local investment opportunities, and benefiting from a robust team in major financial centers worldwide.

What are the key trends in the wealth management industry?

There is a growing trend toward greater diversification of portfolios, especially with increased international exposure. The internationalization of portfolios, increased exposure to dollars, and the use of international platforms are key trends in an environment of rising uncertainty, demographic changes, and technological advancements affecting both the industry and markets. In this regard, BTG Pactual’s international platform has been crucial in providing Latin American clients access to markets in Europe and the United States.

Regarding the growth of the industry, do you think it will lean more towards separately managed accounts or collective investment vehicles?

There is room for both types of products. In our experience, institutional clients prefer separately managed accounts, while high-net-worth families tend to opt for collective investment vehicles. Throughout my experience, I have managed all kinds of assets, with a greater emphasis on fixed income strategies. At BTG Pactual, we use an open-architecture platform to invest with the best global managers, providing consistent value to our clients.

Do you allocate a certain percentage of a client’s portfolio to alternative assets, and how do these vary in terms of geographic location?

Yes, we have developed an alternative assets program with exposures ranging from 25% to 35% in products like private equity, private debt, and real estate. We have also been active in club deals, offering investments with higher returns and lower volatility, though with less liquidity. The underlying assets of these alternative investments vary geographically. Our open-architecture strategy allows us to invest with the best local and international managers, consistently identifying those who deliver high returns.

What is the biggest challenge in capital raising or client acquisition?

The biggest challenge is understanding the client’s needs to create a value proposition that combines their financial goals, expected returns, risk, liquidity, and the family’s values and legacy.

What factors do you think a client prioritizes when investing?

Clients prioritize expected returns relative to perceived risk, the efficiency and cost of investment strategies, and, increasingly, family values and the purpose of the wealth.

How is technology transforming the wealth management sector, specifically artificial intelligence?

Technology is democratizing investment opportunities through platforms and virtual assistants. Artificial intelligence facilitates rapid analysis of large volumes of information and the automation of administrative tasks, allowing us to focus on client relationships and identifying investment opportunities.

What are the most important skills a wealth management director should develop, and how do you personalize investment strategies to meet each client’s needs?

A wealth management director should develop essential skills such as analytical ability, effective communication, teamwork, and adaptability to change, especially in a volatile and challenging financial environment. To personalize a client’s investment strategies, at BTG Pactual, we have a highly qualified team both locally and internationally. In Chile, we are 12 professionals dedicated to the Multifamily business, supported by a team of 35 in the United States, Brazil, and Luxembourg, and backed by over 8,000 professionals worldwide.

Future of Wealth Management

In the next 5 to 10 years, Alberto forecasts a significant generational shift in investment decision-making. New generations are inclined toward alternative investments, venture capital, and strategies addressing technology and climate change impacts. This shift occurs in an environment of decreasing expected returns, driving a greater search for opportunities that offer both financial performance and positive social impact. The integration of advanced technology and the personalization of investment strategies will also play a crucial role in adapting to these new priorities and meeting emerging investor expectations.

Interview conducted by Emilio Veiga Gil, Executive Vice President at FlexFunds, in the context of the “Key Trends Watch” initiative by FlexFunds and Funds Society.

Photo courtesyVíctor Piña, BBVA Global Wealth Solutions (GWA) CIO in Miami

Latin Americans have put a significant focus on ETFs when structuring their investment portfolios, BBVA Global Wealth Solutions (GWA) CIO in Miami, Victor Piña, told Funds Society.

“In terms of investor trends, especially among Latin Americans, we have seen a lot of inclination toward ETFs. In general, many ETFs in UCITS format,” Piña explained in an exclusive interview with Funds Society.

I believe that the growing divide between beta and alpha and the search for greater efficiency finds ETFs as a trend that “is here to stay” because they are products with a very low cost.

On the other hand, Piña added that within GWA’s wealth management business, especially in the Ultra High Net Worth segment, there is a particular interest in alternative products.

“In the higher segments we see an appetite for alternative instruments and they are also combining their portfolios between ETFs and alternatives.”

With regard to alternatives, BBVA GWA takes into account liquid alternatives with daily or bi-daily liquidity but deploys more complex strategies which are more difficult to structure through ETFs.

“These funds do have a niche because they can serve to diversify the portfolio and it is something that we at BBVA GWA want to offer,” explained the CIO.

On the other hand, illiquid alternative products are something that the investment team is working on and could enter in the coming months.

At BBVA GWA they agree with the analysis of most experts that inflation in the US is already beginning to ease and will ease a little more and that should bring a drop in rates in the short term, according to Morningstar. For this reason, Piña said that they remain positive on debt instruments with terms of one to three years.

“I think we believe that rates will go down, and to put it simply: we want to lock in rates to do the lock in based on the drop we expect,” he said.

Political context

In recent days, US politics has experienced episodes that altered the presidential race for November. The resignation of the current president Joe Biden and the possible replacement by his vice president, Kamala Harris, for the moment, strengthen the expectations of former president Donald Trump to return to the Oval Office.

When asked about the possibility of the expectations of the polls and bets being met, the CIO of BBVA WGA responded that some scenarios can be seen.

On the one hand, more protectionist policies are implemented and in that sense a tax reduction that could lead to a greater fiscal deficit. This scenario, according to Piña, could generate a contraction in the decline of the consumer price index.

In addition, Piña highlighted that there was a lot of differentiation between the returns of the technology sector, which as Trump’s chances increase, has been normalizing.

“The valuations in the US are very different in the technology sector than in the rest. Before, we had invested at the S&P 500* level and now we are evaluating the possibility of discriminating and concentrating more on the most attractive valuation companies that, generally, are not the mega caps,” described the executive.*

On the other hand, the types of infrastructure sectors are beginning to look attractive compared to technology, he added.

As for emerging countries, mainly in Latam, the region has had challenges recently that have generated volatility in the markets. To name an example, Piña commented that the election of the new president of Mexico, Claudia Sheinbaum, had caused some political uncertainty, however, since the messages she has sent, in the appointment of her economic team, for example, the markets have been stabilizing. The same is happening in Peru, “where we are beginning to see stabilization” and Argentina “which has had an impressive rally in its valuations.”

“So, in my opinion, this issue of noise or political volatility at the end of the road will be rewarded by the fundamentals of the countries, for example Mexico and nearshoring,” he commented.

Finally, he clarified that the valuations of emerging markets tend to be more attractive with a view to the medium and long term.

The portfolio creation process

The advisory process at BBVA GWA consists of three defined steps that for Piña “are fundamental to provide a service adapted to each client and strive to optimize investment opportunities.”

It begins with a profiling questionnaire that seeks to find out the goals and the level or tolerance to risk of investors. “The know your customer (KYC) client phase is very important to provide good advice,” he said.

Once this information is available, investment guides are prepared and these are a portfolio at the asset class level based on long-term models with a five-year horizon.

However, that does not mean that the strategic model is complemented by a tactical model where investment ideas for a period of no more than one year are also included.

After concentrating the ideas, they are processed in an optimizer “in which we indicate the level of risk that our clients tolerate, and what we aim to be an optimal portfolio is established.” Later, the best investment solutions or the best products are selected. “For each type of asset we select what we deem to be the most efficient for each one of them,” he emphasized.

Finally, our investment counselors “counselors support our financial advisors who in the creation of proposals” meet with clients, bringing them investment portfolios.

The interview was conducted prior to the massive stock market crash of the past “Black Monday” of August 5, 2024.