For investors, determining their asset allocation this year will be especially challenging. One of the main uncertainties is whether the new president of the United States, Donald Trump, will raise export tariffs and potentially spark a trade war.

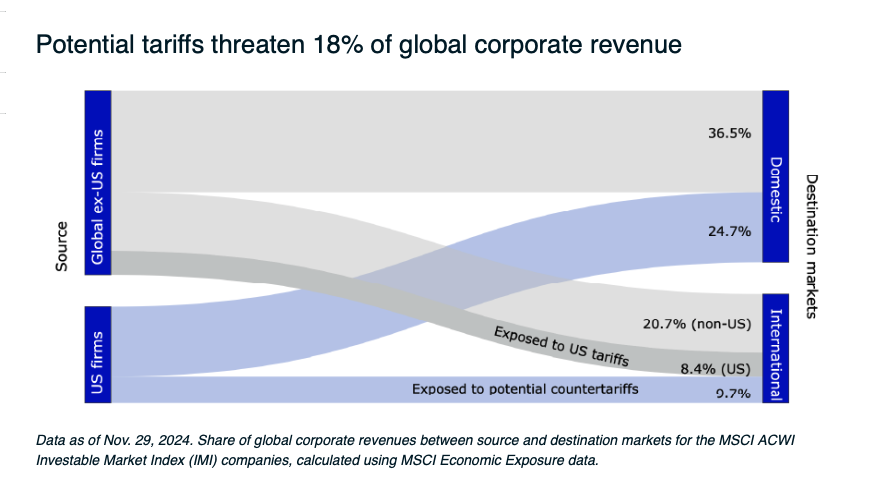

Abhishek Gupta, Executive Director of MSCI Research, analyzes the situation with data from his firm and explains in a report that “nearly 40% of global corporate revenues are generated in international markets, and 18% may be at risk due to the tariffs proposed by the U.S. and potential counter-tariffs. Furthermore, the risk was evenly split between non-U.S. companies selling in the United States (8.4%) and U.S. companies selling internationally (9.7%).”

Tariff Risk by Country and Sector

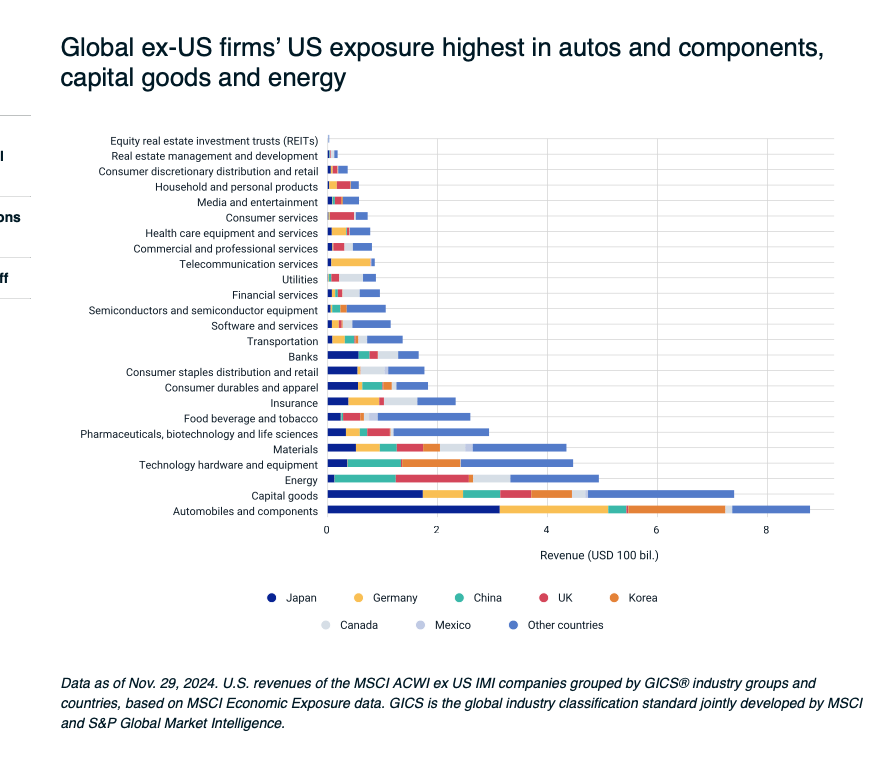

Japan, Germany, the United Kingdom, China, and Canada are the top five countries (by revenue in U.S. dollars) that sell in the U.S. market. Among them, Japanese, German, and Korean automakers dominate automobile and component imports, while Chinese, U.K., and Canadian companies lead energy imports.

Capital goods and materials also make up a substantial portion of total U.S. imports, but these are more fragmented among exporting nations. Other industries, such as pharmaceuticals, food and beverages, and durable consumer goods, have accounted for a smaller share of total U.S. imports but could be at risk due to their dependence on U.S. demand.

Beyond revenue exposure, the location of a company’s production facilities can add another layer of risk. For example, several Japanese automakers produce vehicles in Mexico. Higher U.S. tariffs on Mexican imports could have a disproportionate impact on these companies compared to those that manufacture in Japan.

The following heat map analysis combines data from MSCI Economic Exposure and MSCI GeoSpatial Asset Intelligence to highlight the number of companies economically tied to the United States (defined as deriving more than 10% of their revenue from the U.S.) that have production facilities in Canada, Mexico, or China—all of which could be subject to higher tariffs.

Approximately 390 non-U.S. companies meet these criteria (of which 90 are Canadian, Mexican, or Chinese companies). Japanese companies appear to be the most exposed, with 91 at risk, including 28 in the capital goods industry and 18 in the automotive sector. Many European companies may also be at risk due to overlapping revenue dependencies and production locations.

Japanese and Chinese Companies Top the List of Those Most Exposed to Higher U.S. Tariffs

If U.S. trade partners facing higher tariffs choose to impose their own tariffs on goods imported from the U.S., American companies will suffer, as they collectively derive a quarter of their revenue from international markets. China, for example, was the largest end market for U.S. goods in November 2024, with an export value to the U.S. more than double that of the United Kingdom, the next largest importing market. U.S. exports in technology, semiconductors, energy, capital goods, and other industries are the most exposed to such potential retaliatory measures.

However, in practice, corporate supply chains can be extremely complex, and intermediate inputs may cross national and regional borders multiple times before reaching final production. The tariff impacts on companies are more complicated than they might appear.

After five iterations, specialized asset manager Blue Owl is in the process of raising capital for its sixth GP Stakes fund. This strategy aims to cover the spectrum of alternative assets by investing in a variety of prominent specialized fund managers. As part of its commercial push, the firm is focusing intently on Latin America, targeting institutional investors in the region.

“This is a very unique way to invest in private markets,” says Michael Rees, Co-President of Blue Owl, in an interview with Funds Society. From the institutional investor’s perspective, Rees highlights three key pillars of the strategy’s appeal: an “extremely” diversified portfolio, capital efficiency, and cash flows.

Sources familiar with the process reveal that GP Stakes VI is targeting $13 billion in capital. The fundraising process is approximately halfway through, with expectations that the fund will close during 2025.

Rees confirms that the strategy will begin deploying capital in early 2025. “We’ve already raised significant capital, so we can start deploying it as soon as possible,” he explains.

Latin America Roadshow

The firm’s commercial effort in Latin America has included multiple visits to the region in recent months. “We have a strong focus on Mexico, but also on Chile and Colombia,” says Philippe Stiernon, CEO and Managing Partner of Roam Capital, the firm distributing Blue Owl’s products in the region.

In 2024, Blue Owl made two trips to Mexico—in March and November—to participate in the Encuentro Amafore, one of the key events for the pension fund industry (Afores). Additionally, the firm visited Chile and Colombia during the second week of January.

“We’re very excited about this,” says Rees. “Throughout 2025, we’ll conduct more roadshows and ensure we’re accessible to our clients,” he adds.

According to Rees, there are two types of investors who will find the fund particularly attractive. On the one hand, there are clients with well-established private markets portfolios seeking a product that generates alpha and outperforms the industry. On the other hand, there are investors just beginning to explore private assets who are looking for broad exposure through a single structure.

Stiernon explains that the institutional markets in Chile and Colombia align more with the first type of investor, while Mexico falls closer to the second. Although the Afores are not new to alternative investments, their growth has been more recent. “Many Afores are gaining momentum, with positioning limits increasing. That opens up opportunities for some institutions there to make significant moves into private markets,” Rees adds.

Even in jurisdictions with pension reform challenges—such as Colombia, Peru, and potentially Chile—the executives see room for interest. “Even in countries facing regulatory challenges, this product works seamlessly. It’s truly an all-weather product,” says Stiernon.

The GP Stakes Formula

The sixth fund in the series, like its predecessors, will span all major categories of alternative assets. Its portfolio is expected to follow the same pattern as earlier versions, reflecting the broader industry.

Rees anticipates the fund will invest approximately 60% in buyout managers, with the remaining 40% split across growth capital, venture capital, infrastructure, private credit, and real estate.

This diversification is at the core of GP Stakes VI’s pitch. Rees emphasizes that the fund isn’t just diversified by the underlying assets of the managers it invests in or by GP but also by geography and vintage year.

“When we invest in a GP, our clients gain exposure to their older funds, which are still active, and also to the funds they’re likely to launch in three, five, or ten years,” Rees explains.

Another critical component is the fund’s cash flow. GP Stakes, Rees notes, is a “yield strategy” that generates returns without needing to sell its stakes in alternative managers since it invests in profitable firms. “As we invest, we’re generating cash flow and yield almost immediately. So, while you’re putting money to work, you’re also taking money out,” he says.

The Profile of GPs

As for the type of asset managers Blue Owl targets, Rees stresses that the strategy seeks industry leaders with decades-long operational horizons. “We’re looking for private market firms that are building valuable franchises we can hold a stake in for a very long time,” he explains.

While the selection of GPs serves the fund’s diversification goals, Rees says the analysis process is entirely bottom-up. The priority is determining whether the manager ranks among the best in its category. “When you think about the top 100 or 200 GPs in the industry, that’s our fishing pool,” he notes, adding that “there are real benefits to being big in today’s market.”

Size, according to Rees, filters access to the client segments driving growth. “The new capital isn’t coming from U.S. state pension funds like it did a decade ago. It’s coming from the wealth channel and geographies that are increasing their positioning,” he says, citing Mexico, Australia, the Middle East, and Asia.

“If you’re a small firm and rank 5,000th in the industry, you won’t have access to those types of clients. That’s why we’re seeing this growth phase favor the larger, branded firms,” he concludes.

Amerant Bancorp and its subsidiary, Amerant Bank, have announced the appointment of Lisa Lutoff-Perlo and Odilon Almeida Junior to its Board of Directors.

Lutoff-Perlo, a leader in the global hospitality industry, has nearly 40 years of experience. Most recently, she served as President & CEO of FIFA World Cup 2026 Miami Host Committee. She also serves as a board member of AutoNation and chair of Hornblower Group’s Board of Directors.

Almeida Junior brings over a decade of experience on public and private company boards. He is the Managing Principal of AJ. Holdings Co. and Operating Partner at Advent, with prior roles as CEO of ACI Worldwide and President of Western Union’s Global Money Transfer division. He also serves on the Board of Directors for NCR Atleos.

“Their expertise, connections, and strategic vision will guide Amerant toward continued growth and success,” said Jerry Plush, Chairman and CEO of Amerant Bancorp.

Morgan Stanley Wealth Management’s latest quarterly retail investor pulse survey has revealed that investor sentiment remains stable as 2025 begins. The survey found that 58% of investors started the year with a bullish outlook, similar to the 59% recorded in the previous quarter.

Additionally, 64% of investors expect the market to rise by the end of the first quarter.

Inflation remains the top concern for investors, with 45% of respondents citing it as the main risk to their portfolios, consistent with the previous quarter’s 46%. Market volatility was the second most significant concern, with 24% of investors mentioning it, a slight increase from 23% in the last survey.

Concerns regarding the new administration decreased by 13 percentage points since the previous quarter.

The survey also showed that 59% of investors believe the U.S. economy is strong enough to allow the Federal Reserve to cut interest rates in the first quarter. However, this percentage is nine points lower than the previous quarter’s 68%.

The survey results suggest a consistent level of optimism among investors, with a continued focus on inflation, market volatility, and the performance of key sectors as 2025 continues.

Stonepeak has finalized the acquisition of Boundary Street Capital, LP. Boundary Street is a specialist private credit manager with a strong track record in digital infrastructure, enterprise software, and technology services sectors.

Stonepeak executives shared their enthusiasm about the deal.

“The teams represents a strong cultural fit for our firm, and their addition will enable us to bring an even broader set of offerings to our limited partners and borrowers across the infrastructure landscape,” said Jack Howell, Co-President of Stonepeak.

“With expertise in digital infrastructure and technology services and extensive experience in the lower middle market, Boundary Street complements our existing credit investing capabilities well,” said Michael Leitner, Senior Managing Director at Stonepeak.

“We are excited to start capitalizing on the many investment opportunities we’re seeing driven by digitalization and AI in ways we could not have done before,” said Rashad Kawmy, Partner and Co-Founder of Boundary Street.

Paul, Weiss, Rifkind, Wharton & Garrison, and Simpson Thacher & Bartlett LLP acted as legal counsel to Stonepeak, while Hogans Lovells provided legal support to Boundary Street.

CMEGroup has begun making its future products eligible for Robinhood customers in the U.S. The expansion will enable retail traders using the platform to access various futures across five major assets, including equity indexes, foreign exchange, cryptocurrencies, metals, and energy.

The platform includes future contracts for the S&P 500, Nasdaq-100, Russell 2000, and Dow Jones Industrial Average, as well as bitcoin and ether. Additionally, traders will have access to foreign exchange futures for significant currency pairs, metals such as gold, silver, and copper, and energy contracts for crude oil and natural gas.

“Expanding retail access to futures trading is an integral step in educating and empowering this new crop of investors, and we look forward to working with Robinhood to continue providing the products and resources needed to tap into today’s most important markets,” said Julie Winkler, Chief Commercial Officer at CME Group.

Robinhood has introduced a new mobile trading interface to support its launch, including a streamlined trading ladder for faster order execution.

“This reimagined experience, coupled with some of the lowest fees in the industry, makes trading futures at Robinhood an easy decision,” said JB Mackenzie, VP and GM of Futures and International at Robinhood.

The companies offer educational resources to help their traders navigate futures markets. CME Group offers courses, webinars, and market insights through the CME Institute and Futures Fundamentals. Robinhood is supplementing these efforts with futures-focused content on Robinhood Learn and an upcoming series of YouTube videos.

The launch reflects retail investors’ increasing demand for futures as more traders seek diversified investment opportunities and risk management tools.

The Conference Board Consumer Confidence Index fell by 5.4 points in January to 104.1, a dip from December’s revised reading of 109.5. The revision marked a 4.8-point increase from the preliminary December figure but still reflected a decline of 3.3 points from November.

The Present Situation Index, which gauges consumers’ views of current business and labor conditions, plummeted by 9.7 points to 134.3 in January. Meanwhile, the Expectations Index, measuring short-term outlooks for income, business and labor market conditions, dropped 2.6 points to 83.9. Despite this decline, the Expectations Index remained above the key threshold of 80, which typically signals recession concerns.

“All five components of the Index deteriorated, with the largest drop in consumers’ assessments of the current labor major,” said Dana M. Peterson, Chief Economist at The Conference Board.

Inflation expectations ticked up slightly, rising from 5.1% in December to 5.3% in January. Over half, 51.4%, of consumers expect higher interest rates in the next 12 months. Consumer buying intentions remained stable for homes and cars, while services spending, particularly dining and streaming, showed continued growth.

Edouard Carmignac had the opportunity to have lunch with the now-president Donald Trump 20 years ago. It was a business lunch where the founder, president, and CIO of Carmignac Gestion gained a good understanding of the character of the then-businessman, which has helped him assess how his second, non-consecutive term as U.S. president might unfold: “Donald Trump, for his flaws, can be criticized, but we must acknowledge that he has a formidable instinct. In a world seeking growth but that is globalized and where traditional models no longer work, his approach has an impact.” Although the president and CIO admitted that some of Trump‘s promises “include extreme proposals that may sometimes seem radical,” he also stated that “boldness and leadership are needed because the old paradigms are no longer sustainable.”

These remarks were made by Carmignac at the annual forum organized by his firm in Paris for clients and the media, which this year also marked the 35th anniversary of the firm and its flagship fund, Carmignac Patrimoine.

One of the major investment-related topics Edouard Carmignac addressed in his speech was the shift in the global political order, where he was particularly critical of countries with left-wing governments: “The classic redistribution models, which worked well in the past, are now exhausted. Resources cannot continue to be redistributed if there is no way to generate them. That is why European models face resistance and need to reinvent themselves with efficient governance.” However, despite these challenges, Carmignac maintained an optimistic outlook, asserting that “there is potential” for greater growth in Europe, and expressed confidence that European governments would gradually shift towards more conservative and right-wing positions, beginning with Germany after the elections scheduled for February.

Carmignac cited another example of a global leader, Javier Milei, with whom he had a one-hour meeting. Among the topics they discussed were economics and their shared views on the Austrian School of Economics. “I was impressed by his intelligence and his knowledge of economics. He has an unwavering determination to change Argentina and move it forward, which will have an impact not only on his country but also on South America,” Carmignac emphasized.

Among the investment themes for 2025 that Carmignac Gestion is monitoring, Edouard Carmignac highlighted that “a technological revolution is underway,” though he preferred to call it “augmented intelligence” rather than artificial intelligence. “We are witnessing a transformation that is just beginning, and those who invest in it will find great opportunities.” Regarding cryptocurrencies, he took a more cautious stance, instead emphasizing the importance of “continuing to invest in projects with real value and long-term sustainability.”

Outlook for 2025

Raphaël Gallardo, chief economist at Carmignac Gestion, provided a more detailed and specific analysis of key themes the firm is monitoring this year, positioning their funds accordingly. He began by discussing the current situation in the U.S., particularly the difficult paradox facing the new Trump administration, which has promised continued economic growth while avoiding inflationary pressures.

Specifically, Gallardo identified three factors affecting U.S. growth: the high deficit (above 6%), which will constrain budget decisions; the sustainability of the wealth effect experienced by households in recent years, driven by rising financial asset prices, which Gallardo questioned; and, related to the previous two, the evolution of interest rates, which he believes “will determine the budgetary margin,” as each movement in the cost of money directly impacts stock market valuations and real estate assets while also absorbing up to 20% of U.S. household incomes.

According to the chief economist, Trump has four key levers to navigate this challenge: reducing public spending through the newly created Department of Government Efficiency (DOGE), led by Elon Musk; promoting deregulation, particularly in artificial intelligence; implementing tariffs; and lowering oil prices by flooding the market with more barrels, which would require negotiations with Saudi Arabia and even Russian authorities, potentially leading to a resolution of the war in Ukraine.

On the other side of the world, Gallardo discussed China’s “obsession with trade surpluses,” arguing that its export figures are inflated due to the country ramping up shipments in 2024 ahead of new U.S. tariffs. Gallardo believes Xi Jinping‘s government is currently at an “impasse,” as it attempts to mitigate the negative impact of the real estate sector on the economy while trying to “set a consumption floor without altering the economic model.”

Regarding a potential new trade war between the U.S. and China, Gallardo sees multiple factors at play. He anticipates another shift in trade rules between the two nations—though he notes that Trump, unlike in 2018, is not being as aggressive with tariffs this time. He also cites other influences, such as the war in Ukraine and the ongoing fentanyl trade between the two countries.

Finally, Gallardo argues that the EU can play a key role in this historic rivalry in three ways: first, by becoming a better client for the U.S., particularly by increasing demand for American goods and services in the defense and gas sectors; second, by coordinating with the U.S. to decouple China’s technological advancement, creating a competitive advantage; and third, by leveraging deregulation within Europe to impact U.S. companies, such as enforcing stricter regulations on digital giants.

A new report from S&P Global Market Intelligence reveals how alternative data and AI can be used to assess the effects of U.S. tariffs on businesses. The report, ‘Three Tools for Trump Tariffs 2.0,’ provides insights into how tariffs impact companies at both the product and company levels.

The analysis highlights that companies with substantial international operations and high U.S. sales are particularly vulnerable. From 2017 to 2019, equity investors in these firms saw stock prices lag behind peers by 3.9%. On the other hand, companies with a higher U.S. workforce but lower U.S. revenue enjoyed an 11% equity premium over competitors.

Using Advanced AI and alternative data, including social media job profiles, business relationship algorithms, and natural language processing from the recently acquired ProntoNLP, the report allows businesses to track the real-time impact of tariffs.

The report shows that tariff–targeted firms altered their supply chain strategies by 17% from 2017 to 2019, with certain industries, like Autombiles & Components, seeing up to 37% shifts. Additionally, executives have increasingly emphasized supplier diversification in response to tariffs, with 57% of earrings call reponsesn in Q3 2024 focusing on this strategy.

As tariff discussions surge, companies can use these tools to better anticipate future impacts on their operations.

The growth of the ETF segment in the European fund market has raised a new question: Is a simple average sufficient to compare the sectoral performance of active versus passive UCITS equity funds? This is the question that the European Fund and Asset Management Association (EFAMA) has sought to answer in its latest edition of Market Insights, titled “The Sectoral Performance of Active and Passive UCITS: Is a Simple Measure Enough?”

Although past performance does not guarantee future returns, recent literature has shown that funds with better historical performance attract more capital inflows. In recent years, passive funds have gained popularity due to their lower costs and their tendency to report higher average net returns than active funds. “However, the debate over which group of funds delivers better performance is more complex than it seems,” EFAMA acknowledges.

According to EFAMA, fund performance is typically reported by showing a simple or weighted average of the gross or net returns of all funds within a given category. “This is generally measured within a broad fund category, such as all active or passive funds, or the total universe of funds. This approach does not take into account the diversity of funds in terms of issuers, types of securities, geographical exposure, currency, and industry sectors, and consequently, the diversity in fund performance,” EFAMA explains.

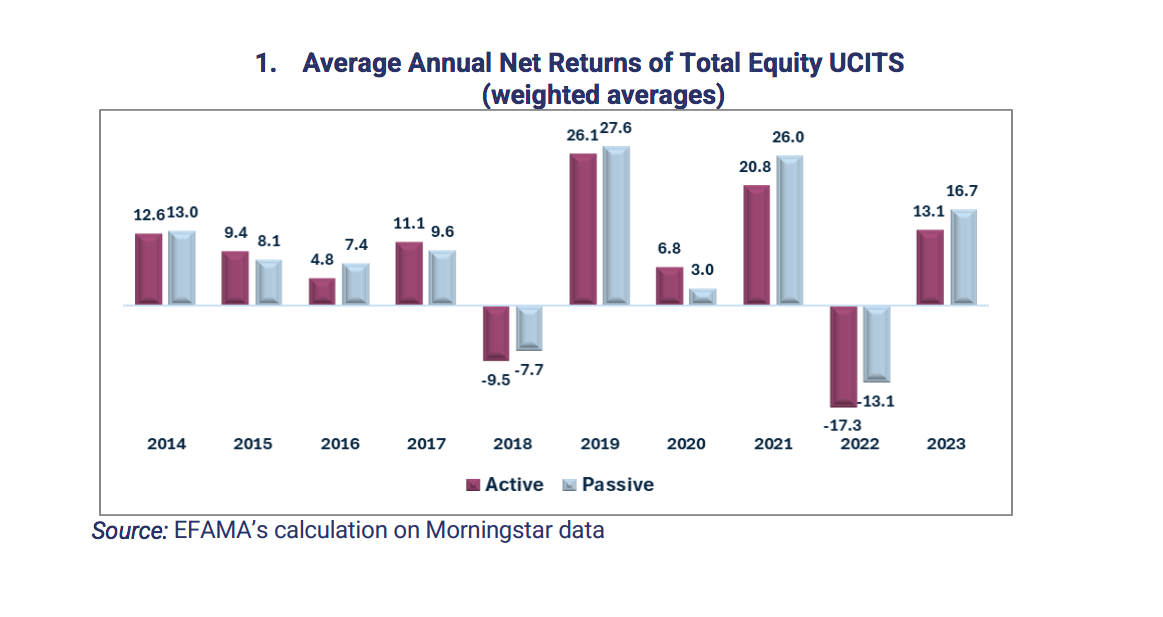

To address this, EFAMA analysts have compared the net performance of different categories of UCITS equity funds over the past ten years (2014–2023). The analysis shows that in 2023, the average net return of active UCITS equity funds was 13.1%, while that of passive UCITS equity funds reached 16.7%, “suggesting that passive UCITS outperformed,” EFAMA states in its report.

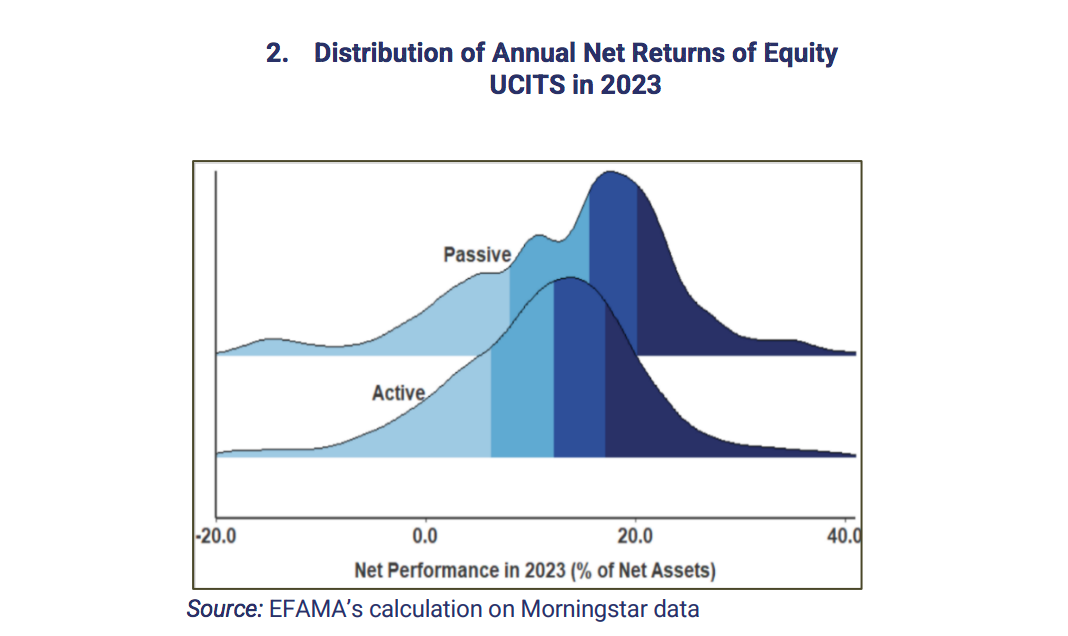

When analyzing the distribution of average annual net returns of active and passive UCITS equity funds in 2023, it is observed that two years ago, in 2023, many active funds achieved returns as strong as passive funds, while many passive funds had lower returns than active ones. According to EFAMA, “the observed returns depend on various fund characteristics, such as the industry sector or geographical exposure, regardless of whether a fund is active or passive.”

Key Findings

“Our analysis reveals significant differences in the average net performance of sectoral equity funds, with neither active nor passive funds consistently outperforming the other,” says Vera Jotanovic, Senior Economist at EFAMA.

Meanwhile, Bernard Delbecque, Senior Director at EFAMA, explains that given the high diversity among investment funds, “retail investors should seek professional advice before allocating their savings to specific equity funds, ensuring that their choices align with their individual investment goals and preferences.”

In this regard, one of the main conclusions reached is that “significant differences in net performance are observed among UCITS equity funds across various industry sectors, for both active and passive funds.”

Additionally, it is concluded that while passive equity funds generally outperform active equity funds when comparing net returns across the entire universe of equity funds, this pattern does not consistently hold across all sectors.

It is also extrapolated that some active funds outperform passive funds, and vice versa, depending on the industry sector, the year, and the time horizon, “demonstrating that no category consistently delivers superior performance,” EFAMA notes. Finally, the report warns that its findings remain robust even after accounting for return volatility.