Once again, Monaco will become the meeting hub for asset and wealth management leaders during IMpower FundForum, taking place from June 23 to 25, 2025. As the only specialized event dedicated to investment managers across active, passive, and private markets—with a focus on private wealth management—it is a must-attend for senior executives in the industry.

Join 1,400+ senior leaders, including 500+ asset managers, 400+ fund selectors, and asset owners, for three dynamic days of networking and collaboration. Year after year, the event is the preferred choice for CEOs, CIOs, COOs, and partners from leading asset managers and GPs worldwide. With a 35-year track record, it delivers unparalleled industry insights.

With the highest concentration of fund buyers and LPs from private banking and wealth management, this is the only event where you can connect with over 500 influential professionals. According to the event organizers, “One-third of attendees are fund selectors and asset owners.” Stay ahead in the asset and wealth management community at IMpower FundForum, the ultimate event for meaningful connections and valuable industry insights.

Fund selectors attend for free, while asset and wealth managers benefit from discounted rates. Register now and save 10% with code: FKN3972FUNDSOC.

Hernández, former executive director at J.P. Morgan Wealth Management, serves high-net-worth and ultra-high-net-worth families, as well as entrepreneurs, corporate executives, and institutional investors.

Through NewEra Wealth, Hernández is creating a highly personalized, family office-style experience that offers clients exclusive access to carefully selected private investment opportunities while leveraging cutting-edge technology to enhance outcomes, Bolton stated in a press release.

“NewEra Wealth is built on the principles of integrity, independence, and innovation. By partnering with Bolton Global Capital, we can provide our clients with top-tier resources and a truly independent platform that allows us to focus solely on their best interests,” said Hernández.

“Partnering with Bolton Global allows me to focus on gathering and managing assets without the high costs, risks, and operational complexities of running an RIA. They handle those responsibilities in a more cost-effective way,” he added.

As part of Bolton Global Capital‘s network of independent advisors, NewEra Wealth will offer comprehensive wealth strategies tailored to each client’s unique financial situation, according to the firm’s statement. The company’s offerings include investment management, corporate and retirement cash management, capital markets advisory, and sophisticated estate planning solutions.

“Víctor has an outstanding track record of delivering exceptional value to his clients. His leadership and expertise make him an ideal partner for Bolton Global Capital, and we are excited to support NewEra Wealth in redefining the client experience in independent advisory services,” said Steve Preskenis, CEO of Bolton Global Capital.

With a degree in finance from Bentley University, Hernández most recently ran his own registered investment advisory firm, has over 20 years of experience, and brings extensive knowledge in investment management. During his tenure at J.P. Morgan, he managed over $600 million in assets, according to Bolton. He also holds an international MBA from IE Business School in Madrid, Spain.

His achievements have been recognized by the industry, earning him multiple Forbes rankings as the top wealth advisor in the state, recognition as one of the best next-generation wealth advisors in the U.S., and features in Fortune magazine.

Insigneo continues expanding its New York team with the addition of Jason Jimenez as Senior Investment Portfolio Associate, as announced on LinkedIn by Alfredo Maldonado, managing director and market head of the firm in that city and the northeastern United States.

“Welcome, Jason Jimenez, to our expanding Insigneo team in NYC!” wrote Maldonado. He added that Jimenez will bring “his exceptional talent to our team. At Insigneo, our goal is to strengthen our franchise by welcoming top-tier professionals.”

Jimenez held the position of Senior Associate Director of Wealth Strategy at UBS for less than a year and previously spent nearly five years at J.P. Morgan Chase as a Client Service Associate. He is a graduate of the Tandon School of Engineering at New York University.

Dynasty Financial Partners announced that Sam Anderson and Harris Baltch have been appointed co-heads of Dynasty Investment Bank as part of the bank’s development and the “ongoing dynamic growth” of the Dynasty Wealth Management platform, according to the firm’s statement.

Anderson and Baltch will report to Justin Weinkle, Dynasty’s Chief Financial Officer, who has also been named Chairman of the company’s Capital Committee.

“This expansion of the executive leadership team will provide Dynasty Investment Bank with greater focus, talent, and resources necessary to pursue the best opportunities and deliver optimal results for its investment banking clients,” the company stated.

Before joining Dynasty, Anderson and Baltch covered complementary sectors of the financial services industry as investment bankers at Goldman Sachs and UBS, respectively. Over their combined careers, they have executed more than $50 billion in M&A transaction value and over $100 billion in financing, according to information provided by Dynasty.

During their three years with the company, they have collaborated on numerous transactions on behalf of the Dynasty Network.

“Similar to many areas of our business, the official launch of Dynasty Investment Bank two years ago and this expanded leadership team we are announcing today naturally evolved from our ongoing support activities for our network firms,” said Shirl Penney, founder and CEO of Dynasty Financial Partners.

“We are proud of how our business has progressed thanks to the alignment and close collaboration we maintain with our clients. It is that same partnership mentality that Sam and Harris will embody as they expand Dynasty Investment Bank and execute on behalf of our clients. The potential for this area of our business is limitless,” he added.

Officially launched in 2023, Dynasty Investment Bank provides specialized services to both wealth management and asset management firms, including M&A advisory and execution for both buyers and sellers, capital underwriting, valuations, and succession planning.

In 2024, Dynasty Investment Bank advised on 15 M&A and capital-raising transactions, including cross-border mergers and acquisitions of publicly traded companies, domestic sell-side transactions, strategic recapitalizations, valuations, and capital-raising mandates. Dynasty currently has 57 partner firms in its network, representing over 500 advisors and more than $105 billion in platform assets.

In today’s investment landscape, alternative assets have become a compelling portfolio and risk diversification strategy. Real estate has proven to be an attractive option within this category due to its ability to generate recurring income and preserve value over time. However, liquidity has historically been one of its limitations. This is where asset securitization plays a crucial role, allowing real estate to be converted into tradable securities accessible to a broader base of investors.

Real estate securitization generally involves creating a special purpose vehicle (SPV), a legal entity that isolates and manages properties. This SPV issues securities backed by the property’s income flows, such as bonds or notes, which institutional investors can acquire in capital markets. For asset managers, this mechanism improves portfolio liquidity, optimizes capital allocation, and enables structuring attractive financial products for different investor profiles.

Real estate securitization can take many forms; among the main ones are:

Residential Mortgage-Backed Securities (RMBS): These are securities backed by pools of residential mortgages. Banks or financial institutions typically originate mortgages and then sold to an SPV. The SPV bundles the mortgages and issues securities backed by the underlying loans.

Commercial Mortgage-Backed Securities (CMBS): These securities are backed by pools of commercial real estate mortgages. Commercial property owners, such as office buildings, shopping centers, or industrial properties, take out the loans. The SPV pools these loans and issues securities backed by the underlying mortgages.

Real Estate Investment Trusts (REITs): These investment vehicles own and operate income-generating real estate assets. REITs allow investors to gain exposure to real estate without directly owning the underlying properties. REITs must distribute at least 90% of their taxable income to shareholders as dividends, making them attractive for investors seeking regular income.

Securitized real estate assets offer multiple advantages for asset managers and their clients, including:

Diversification: Exposure to a broad spectrum of real estate assets across various regions and sectors.

Professional Management: Assets are managed by experienced real estate and finance specialists.

Optimized Returns: Securitized real estate can offer an attractive return profile compared to traditional investments.

However, securitized real estate assets also carry certain risks, including:

Market Risk: The value of securitized instruments may fluctuate based on real estate market conditions.

Credit Risk: The underlying assets may fail to meet payment obligations, affecting the instrument’s profitability.

Liquidity Risk: Changes in market conditions may impact the ease of buying or selling these securities at fair prices.

Success story: CIX Capital

CIX Capital is a firm specializing in real estate investments in Brazil and the U.S., focusing on structuring and managing tailored strategies for institutional investors, asset managers, and family offices. With over R$7.3 billion in transactions, CIX sought an efficient investment vehicle to access international private banking swiftly and cost-effectively.

In this context, FlexFunds‘ solutions enabled CIX Capital to structure a customized issuer for exchange-traded products (ETPs), transforming real estate assets into tradable securities with access to international markets. Thanks to this solution, CIX has securitized over $200 million, optimizing costs and timelines compared to traditional structures in jurisdictions such as the Cayman Islands, the British Virgin Islands, and Luxembourg.

Carlos Balthazar Summ, CEO of CIX Capital, highlights: “FlexFunds’ investment vehicles are ideal for real estate. In a record time, we set up and launched our Bond (ETP), quickly accessing private banking channels via Euroclear, broadening our international capital raising ability, and successfully acquiring 358 multifamily units in Florida, USA. The simplicity in the onboarding of investors and its accompanying savings in the back-oce make FlexFunds’ your ideal partner to create internationally accredited investment structures. It is also a state-of-the-art solution that was well perceived by the private and asset management industries in Brazil and abroad.”

Key benefits achieved by CIX Capital with FlexFunds:

Simplify the investor onboarding and underwriting process

Reduced the administrative costs of fund management.

Facilitate the raising of capital from international investors.

Enable access to international private banking channels.

Real estate securitization provides asset managers an efficient tool to optimize portfolios, enhance liquidity, and attract institutional investors. However, conducting a thorough risk analysis and structuring vehicles tailored to each investment strategy is crucial.

FlexFunds serves as a strategic partner in the repackaging of real estate assets, offering accessibility and management optimization through securitization and as a bridge to multiple private banking platforms. If you are interested in securitizing your real estate investment fund, contact the experts from FlexFunds at info@flexfunds.com.

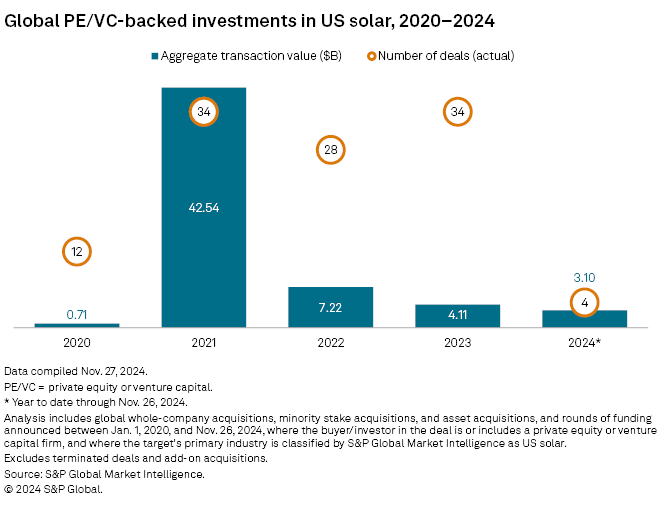

Private equity and venture capital activity in the U.S. solar industry is on track to reach its lowest level in the past four years. This contrasts with significant global private equity inflows into the sector during 2024, according to a new global report by S&P.

According to the report, private equity investments in residential and utility-scale solar energy in the U.S. from January 1 to November 26 totaled $3.1 billion, approximately 24.6% lower than the total reached in 2023 and representing only 7.3% of the $42.54 billion accumulated in 2021. So far, only four private equity deals in U.S. solar energy have been announced in 2024.

Globally, the value of transactions in residential and utility-scale solar energy reached $25.04 billion, an increase of approximately 52% from the $16.46 billion recorded for the entire year of 2023, according to data from S&P Global Market Intelligence.

This rise in global investment comes amid China’s dominance in solar panel production, which has led to oversupply levels. According to a report by Wood Mackenzie, the Asian country will continue to hold more than 80% of global solar manufacturing capacity through 2026.

Europe, including the United Kingdom, attracted the majority of private equity investments in residential and utility-scale solar energy, with 23 deals exceeding $20 billion. The value of private equity transactions involving UK-based renewable energy companies has already surpassed private investments in the U.S. renewable energy sector this year.

Additionally, the U.S. and Canada ranked second in transaction value, with $3.25 billion across seven solar energy deals. The Asia-Pacific region, including China, followed closely with 20 deals worth over $795 million.

European Mega-Deals Drive Private Equity Financing Growth

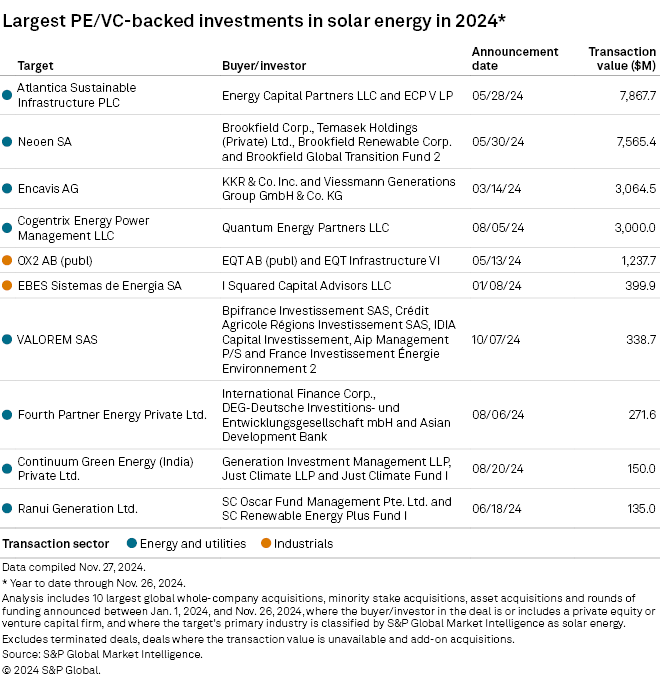

Several multibillion-dollar transactions have contributed to the total value of solar sector deals so far this year. The largest private equity-backed solar energy deal announced in 2024 is Energy Capital Partners LLC’s planned $7.87 billion acquisition of Atlantica Sustainable Infrastructure PLC, a UK-based company. Its ECP V LP fund is set to purchase Atlantica from Algonquin Power & Utilities Corp., which decided to sell after conducting a strategic review of its renewable energy business.

The second-largest deal is Brookfield Asset Management Ltd. and Temasek Holdings (Pvt.) Ltd.’s proposal to acquire 53.32% of Neoen SA, a Paris-based company, for $7.57 billion. The buyers are expected to eventually acquire full ownership of the company and take it private.

Private investments in the industry can help pave the way for the development of new solar technologies. The shorter development timeline, lower capital costs, and compatibility with battery energy storage systems have kept solar energy more attractive than other alternative energy sources, such as wind or nuclear, according to Benedikt Unger, director at consulting firm Arthur D. Little.

“By financing next-generation solar technologies, such as bifacial modules and perovskite cells, private equity investments can accelerate innovation,” Unger wrote in an email to Market Intelligence.

The technical explanation is that bifacial modules capture light on both sides of the solar panel, while perovskite cells are high-performance, lower-cost materials compared to those currently used in solar technology. Unger also sees opportunities for private equity in emerging local solar technology supply chains and the growing solar panel recycling industry.

“Photovoltaic recycling is an emerging industry, but its development is crucial, especially in more mature markets like Europe or the United States. Localized supply chains will be needed in many regions, including Africa and Southeast Asia,” Unger concludes.

Two new professionals have joined Pinvest, the investment advisory arm of Ecuadorian financial group Pichincha in Miami. Francisco Badiola and Diana Zumaran were added to the firm’s roster this week, according to sources familiar with the matter who spoke with Funds Society.

Badiola comes from Citi, where he spent nearly eight years, according to his LinkedIn profile. During his time at Citi, he held several positions, including Investment Counselor—his last role before moving to Pinvest—and VP Investment Associate at Citi Private Bank.

Previously, he worked at Mercantil Bank as a Wealth Management Operations Specialist and at Ocean Bank, where he rose to the position of Treasury Specialist. In total, he has a decade of experience in the financial industry.

Also coming from Citi, where she worked as an AML Compliance Analyst, Zumaran has joined the Miami-based firm as operations & compliance officer. She spent nearly four years at the investment bank, following her role as a personal banker at Wells Fargo. Before that, she worked in various non-financial industries.

Both professionals will report directly to Esteban Zorrilla, CEO of Pinvest. Zorrilla leads the Miami-based firm and also serves as head of private banking at Pichincha Corp.

Pinvest is a SEC-registered investment advisory firm. Its parent company, Grupo Financiero Pichincha, operates in the United States, Ecuador, Peru, Colombia, and Spain.

Across Europe, women are less likely than men to participate in financial markets, leading to what experts call the gender investment gap. The numbers are striking: on average, women own 30% to 40% less in investments and private pensions than men, putting them at a long-term financial disadvantage (OECD, 2023).

While structural factors such as the gender pay gap—which stands at 12.7% in the EU (European Commission, 2024)—and career interruptions due to caregiving responsibilities contribute to this disparity, another key factor is confidence and perception. Many women feel that investing “is not for them,” often due to financial jargon, a natural aversion to risk, and a lack of female role models in finance.

However, the reality is clear: without investing, women risk greater financial insecurity and accumulate less wealth over time. Beyond personal finances, the gender investment gap is an economic issue, costing Europe an estimated €370 billion* annually in lost potential.

Why Aren’t Women Investing Enough?

Despite increasing financial independence, women across Europe are less likely to invest in stocks, funds, and pensions than men. A 2024 ING survey found that only 18% of women invest regularly, compared to 31% of men. In Germany, the disparity is even more pronounced, with only 30% of women actively investing their savings, a significantly lower rate than their male counterparts (DWS, 2024).

In the UK alone, the gender investment gap is estimated at €687 billion (Portfolio Adviser, 2024), with a similar trend across the EU. Women are more likely to hold their savings in cash, missing out on the long-term growth potential of financial markets.

One of the main reasons? Fear of risk. The European Banking Authority (EBA) reports that women are far more likely to keep their money in cash savings accounts, even as inflation erodes their value, rather than investing in diversified portfolios that offer higher growth potential (EBA, 2023).

Another factor is the representation of finance in media and culture. A 2025 study from King’s Business School in London analyzed 12 finance-related movies and 4 television series and found that 71% of male protagonists held senior executive roles, while none of the female characters did (Baeckstrom et al., 2025). More often, women were portrayed as wives or assistants rather than investors or decision-makers.

From Monopoly to the Markets

The fight for women’s financial empowerment is not new. Consider Lizzie Magie, the often-overlooked inventor whose game later became Monopoly. In 1904, she designed The Landlord’s Game to highlight wealth inequality and promote economic education. Yet, years later, Charles Darrow adapted and commercialized her idea, taking full credit and reaping financial rewards (Women’s History Museum, 2024). Her story reflects a broader issue—women’s contributions in finance are often undervalued.

The Cost of Not Investing

Women’s reluctance to invest is not just a financial literacy issue—it is a direct threat to their long-term financial security. On average, women live five years longer than men (Eurostat, 2024), meaning they need larger retirement savings. However, they are more likely to invest in “safe” but low-yield products, such as low-interest savings accounts or government bonds, rather than diversified stock portfolios that generate long-term growth.

The risk of staying on the sidelines is clear: if a woman holds €50,000 in cash for 30 years, inflation could cut its purchasing power in half. Meanwhile, a diversified stock portfolio with an average annual return of 7% could grow to €380,000 over the same period.

Breaking the Cycle: How to Close the Gender Investment Gap

To ensure that women are better represented in financial markets, we need structural changes, cultural shifts, and targeted initiatives to make investing more accessible and inclusive. The financial education plays a crucial role, with programs that simplify investment strategies and address women’s specific concerns.

The representation in media is key: currently, only 18% of financial experts quoted in the press are women, reinforcing the outdated perception that investing is a male-dominated field (Baeckstrom et al., 2025). Normalizing women as financial experts and investors can help dismantle stereotypes and encourage participation.

Additionally, more financial institutions recognize the need for tailored investment products. An example is Female Invest in Denmark, which offers investment courses and community-based support (Female Invest, 2024).

The workplace pension policies must evolve to reflect the reality that women take more career breaks than men. Sweden, for example, has introduced state-matching pension contributions to help women save more for retirement (Pensions Europe, 2024).

By addressing these systemic barriers, we can create an environment where women have both the opportunity and the confidence to invest, ensuring their financial security and independence for future generations.

If history has taught us anything, it’s that when women take control of their finances, they change the game—just as Lizzie Magie did with Monopoly.

This time, let’s make sure they receive both the credit and the financial rewards. By breaking down barriers, increasing confidence, and making investing more accessible, we can help more women build a strong and lasting financial future.

On International Women’s Day, we envision a future where every woman feels empowered to invest, grow her wealth, and take control of her financial destiny. Because when women invest in themselves, they invest in a stronger and more prosperous society for all.

Opinion Piece by Britta Borneff, Chief Marketing Officer (CMO) of the Association of the Luxembourg Fund Industry (ALFI).

Note: The European Investment Bank (EIB) estimates that the gender investment gap results in an annual economic loss of approximately €370 billion, equivalent to 2.8% of the EU’s GDP (2016). This figure highlights the severe economic consequences of gender inequalities in the financial sector.

72% of female clients of U.S. financial advisors specifically sought recommendations from other women, and 64% of advisors understand that their ability to provide personalized and tailored financial advice is one of the main reasons clients choose to work with them.

These findings come from a new survey of 405 financial advisors from the financial services firm Edward Jones, conducted in collaboration with Morning Consult between August 22 and September 6, 2024.

“Considering that two-thirds of American women see themselves as the Chief Financial Officers of their families, it’s clear that women are taking an increasingly important role in their financial future, and there is a growing opportunity for financial advisors to serve them,” the report states.

According to the Edward Jones study, when looking for a financial advisor, women turn to their networks. To establish a genuine connection with clients, financial advisors report that they focus primarily on being transparent and honest about outcomes, fees, and services (72%), actively listening to their needs and concerns (68%), and regularly following up to track progress and involve them in every step of the decision-making process (66%).

“Authenticity and transparency are essential for building meaningful client relationships. All investors value a financial advisor who takes the time to understand their unique financial needs,” said Jasmine Butler, a financial advisor at Edward Jones.

When it comes to converting women investors into clients, financial advisors highlight three key factors: providing clear communication and education (65%), being empathetic toward their financial situations (64%), and maintaining regular and transparent communication (63%).

According to the surveyed financial advisors, more than three-quarters of female clients prioritize long-term investing over short-term investing (77%). Their top financial goals include contributing to their retirement plan (63%), working toward financial independence (61%), and building personal retirement savings (56%).

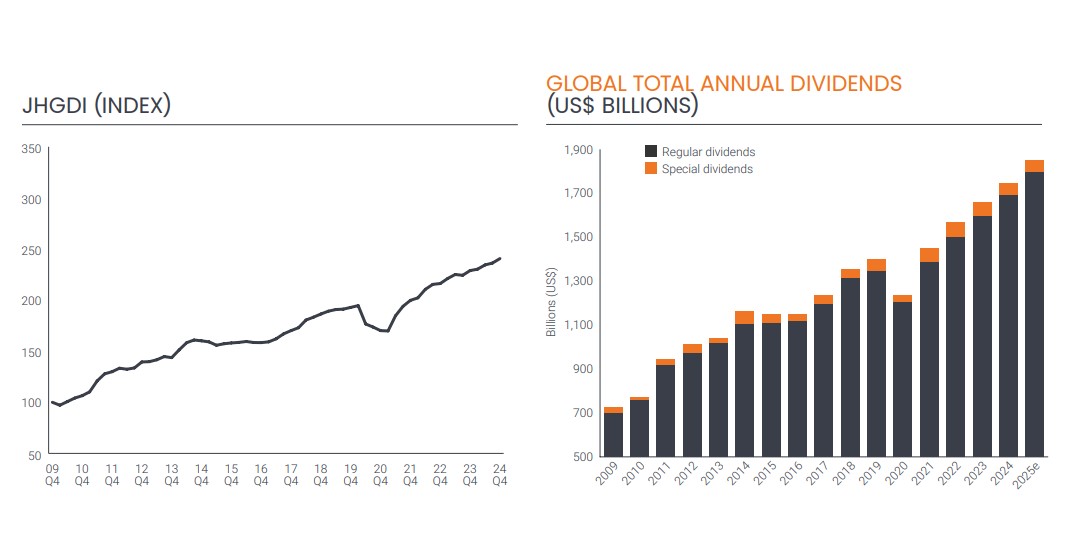

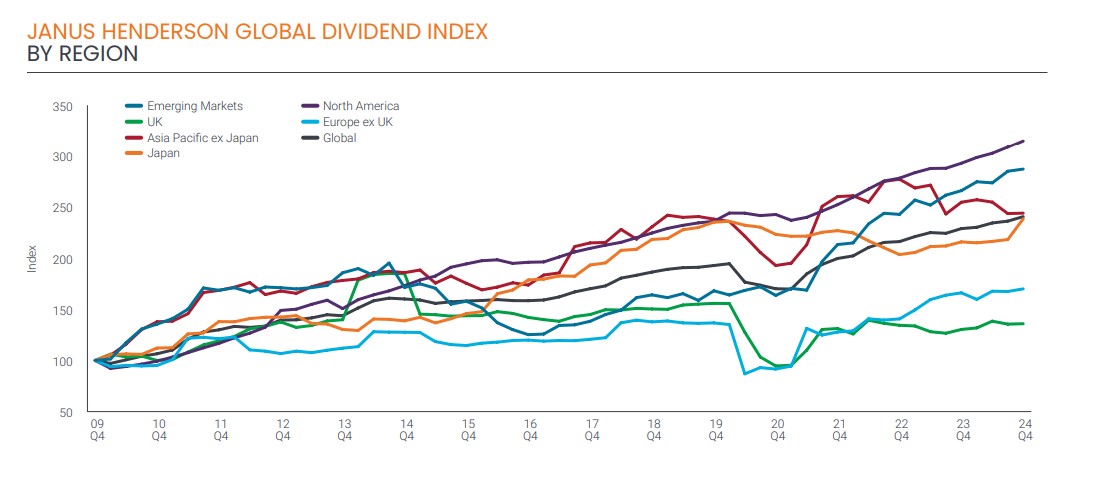

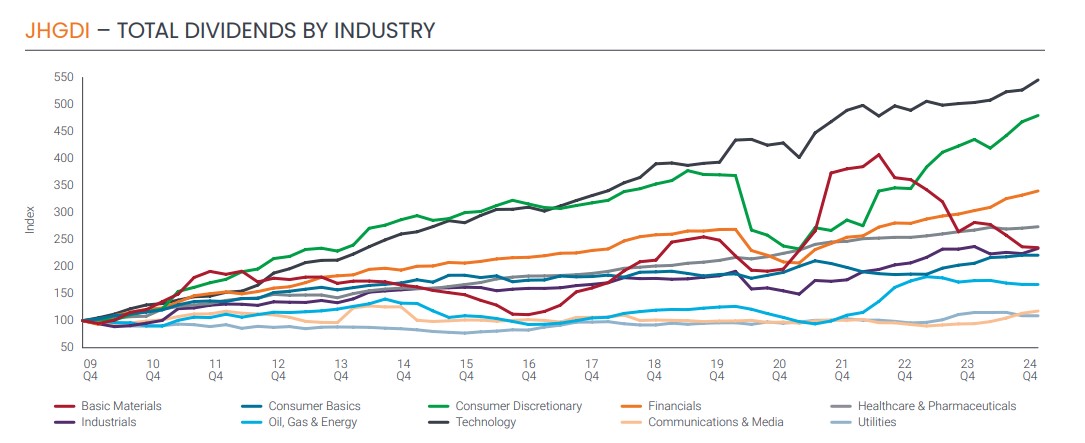

Global dividend payouts reached a record $1.75 trillion in 2024, representing underlying growth of 6.6%, according to the latest Janus Henderson Global Dividend Index. The asset manager explains that, at a general rate, growth was 5.2%, driven by lower special dividends and the strength of the dollar.

The year’s results slightly exceeded Janus Henderson’s forecast of $1.73 trillion, mainly due to a better-than-expected fourth quarter in the U.S. and Japan. In Q4, dividend payouts increased by 7.3% on an underlying basis.

According to their assessment, overall growth was strong across Europe, the U.S., and Japan throughout the year. Some key emerging markets, such as India, and Asian markets like Singapore and South Korea, also recorded decent growth. In 17 of the 49 countries included in the index, dividend payouts hit record levels, including some of the largest distributing nations like the U.S., Canada, France, Japan, and China.

When analyzing the source of this growth, the Janus Henderson report highlights that several major companies distributing dividends for the first time had a disproportionate impact.

“The largest payouts came from Meta and Alphabet in the U.S. and Alibaba in China. Together, these three companies distributed $15.1 billion, representing 1.3% of total dividends or one-fifth of global dividend growth in 2024,” the report states.

Another key finding is that 88% of companies either increased or maintained their payouts globally, while the median dividend growth—or typical growth rate—stood at 6.7%.

By sector, nearly half of the dividend increase in 2024 came from the financial sector, primarily banks, which saw underlying dividend growth of 12.5%.

According to Janus Henderson, dividend growth in the media sector was also strong, doubling on an underlying basis, largely due to payouts from Meta and Alphabet. However, the increase was broad-based, with double-digit growth in telecommunications, construction, insurance, durable consumer goods, and leisure.

In contrast, mining and transportation were the worst-performing sectors, paying a combined $26 billion less than in 2023.

The report also highlights that, for the second consecutive year, Microsoft was by far the world’s largest dividend payer. Meanwhile, Exxon, which expanded its portfolio with the acquisition of Pioneer Resources, climbed to second place—a position it hadn’t held since 2016.

For the year ahead, Janus Henderson expects dividends to grow by 5% on a general basis, pushing total payouts to a record $1.83 trillion. Underlying growth is projected to be closer to 5.1% for the full year, as the strong U.S. dollar against multiple currencies is expected to slow overall growth.

Janus Henderson’s Assessment of the Index Data

Commenting on these figures, Jane Shoemake, portfolio manager at the Global Equity Income team of Janus Henderson, highlights that several of the world’s most valuable companies—particularly those rooted in the U.S. tech sector—are now starting to distribute dividends. This contradicts previous assumptions that these firms would avoid returning capital to shareholders through dividends.

“In doing so, they are following the path of other successful companies before them. As they mature, they start generating cash surpluses that can be returned to investors. These companies are currently providing a significant boost to global dividend growth,” says Shoemake.

2025: An Uncertain Year for the Global Economy

Overall, Shoemake sees 2025 as a potentially uncertain year for the global economy.

“The world economy is expected to continue growing at a reasonable pace, but the risk of tariffs and potential trade wars, along with high public debt levels in many major economies, could lead to greater market volatility in 2025. In fact, fixed-income yields in some markets have risen to levels not seen in years,” she explains.

She also points out that higher interest rates impact investment, slow long-term earnings growth, and increase financing costs, all of which affect corporate profitability.

“That said, the market still expects corporate earnings to increase this year, with consensus forecasts projecting growth above 10%. While this may seem overly optimistic given the current economic and geopolitical challenges, the good news for income-focused investors is that dividends tend to be more resilient than profits throughout the economic cycle.

Companies decide how much to distribute to shareholders, meaning dividend income streams are far less volatile than corporate earnings. For this reason, we expect dividends to reach a new record this year,” concludes Shoemake.