The U.S. venture capital market displayed a sharply divergent pattern during the first five months of 2026: investors completed slightly fewer transactions but deployed substantially more capital than during the same period a year earlier.

According to GlobalData, the total number of venture capital deals announced in the United States declined by 2% year over year between January and May 2026, while total funding value more than tripled.

“This divergence reflects a clear trend toward larger funding rounds and highly selective megadeals. It reinforces the United States as the undisputed epicenter of global venture capital value creation, even amid a modest slowdown in overall deal activity. It is also worth noting that much of this increase in funding value was driven by multibillion-dollar investments secured by a handful of artificial intelligence startups,” said Aurojyoti Bose, Lead Analyst at GlobalData.

Why the U.S. Remains the Global Leader

Among the most notable U.S. financing rounds during the January–May 2026 period were OpenAI’s $122 billion fundraising, Anthropic’s consecutive funding rounds of $65 billion and $30 billion, and xAI’s $20 billion capital raise, among others.

Analysis of GlobalData’s financial deals database shows that despite the decline in transaction volume, the United States maintained its global leadership, accounting for approximately 30% of all venture capital deals announced worldwide between January and May 2026.

At the same time, the sharp increase in deal value propelled the U.S. to capture an overwhelming 81% of global venture capital investment, underscoring the country’s outsized influence in shaping international capital allocation trends.

According to Bose, “the substantial gap between the U.S. share of deal volume and its share of funding value highlights a market characterized by larger average check sizes and a high concentration of capital in high-conviction investment opportunities.”

Other Venture Capital Hotspots

Compared with other major markets, the United States continues to outperform its competitors by a wide margin.

China, the world’s second-largest venture capital market, experienced a strong rebound. The number of transactions increased by approximately 41% year over year, while total deal value surged by around 220%. As a result, China accounted for 23% of global venture capital deal volume and 7% of global funding value. Although these figures point to renewed momentum, China’s share of total investment value remains only a fraction of that of the United States.

The United Kingdom accounted for 7% of global deal volume and 3% of total funding value, while India represented 8% of global transactions but just 1% of worldwide funding value.

“Compared with the U.S., venture capital activity in these markets points to considerably more cautious investor sentiment and a lower frequency of large-scale financing rounds during the period,” GlobalData noted.

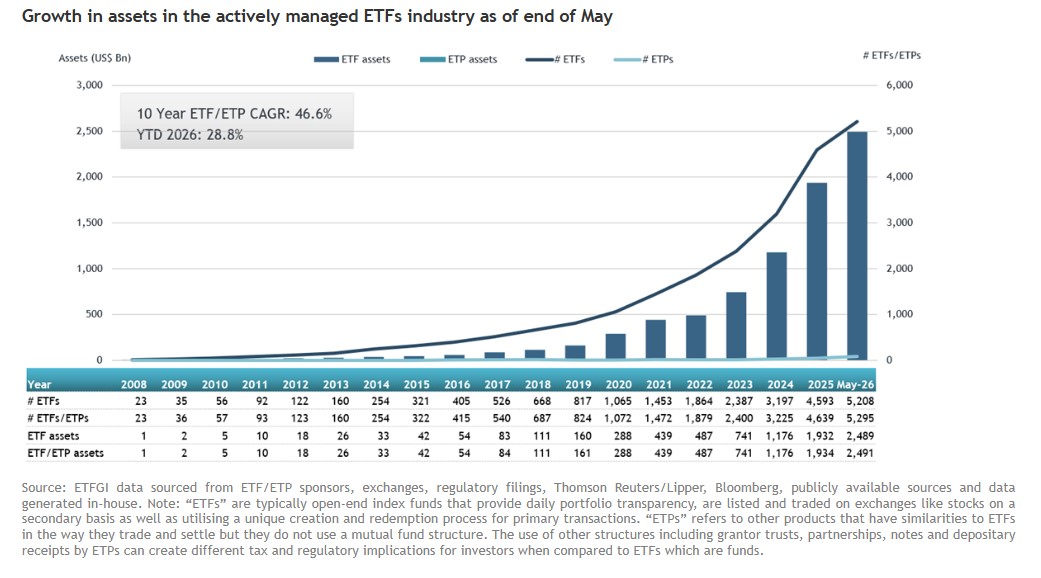

Assets in active ETFs reached a new all-time high of $2.49 trillion at the end of May, driven by a record $412 billion in year-to-date net inflows. According to ETFGI’s latest monthly report, the global active ETF industry attracted $100.08 billion in net inflows during May alone, bringing total inflows for the first five months of 2026 to $411.75 billion.

According to the report, assets have increased 28.8% year to date, up from the $1.93 trillion recorded at the end of 2025, reflecting the increasingly strong and accelerating adoption of active investment strategies in the ETF format.

“Year-to-date net inflows through May—$411.75 billion—are the highest ever recorded, shattering the previous record of $220.53 billion during the same period in 2025. With this performance, the industry has now posted 74 consecutive months of net inflows, reinforcing a sustained structural shift toward these investment solutions worldwide,” ETFGI noted.

A breakdown of the flows shows that active equity ETFs led subscriptions, attracting $60.97 billion in net inflows during May. Year to date, they have gathered $242.18 billion, significantly higher than the $124.28 billion recorded during the same period in 2025.

Meanwhile, active fixed income ETFs posted $26.12 billion in net inflows in May. Total year-to-date inflows reached $136.73 billion, compared with $82.09 billion through May 2025, underscoring investors’ continued appetite for income generation and portfolio diversification.

Leading Asset Managers

Dimensional remains the world’s largest active ETF provider by assets under management, with $296.82 billion and an 11.9% market share. It is followed closely by J.P. Morgan Asset Management, with $291.38 billion in assets (11.7% market share), while iShares ranks third with $168.64 billion (6.8% market share).

According to ETFGI, these three firms—out of 717 providers operating in the market—collectively account for 30.4% of global active ETF assets, while none of the remaining 714 providers individually holds a market share of more than 6%.

For decades, sports sponsorship was viewed primarily as a marketing tool. That has long ceased to be the case when it comes to the FIFA World Cup. Today, the tournament has become a platform for corporate geopolitics, where energy, technology, financial, aviation and consumer companies compete for something far more valuable than visibility: global influence.

The reason is simple. No other sporting event combines such a vast audience, geographic diversity and cultural reach. FIFA’s figures are compelling: the 2022 Qatar World Cup generated engagement with approximately 5 billion people across television, digital platforms and social media, while the final between Argentina and France attracted an estimated 1.42 billion viewers worldwide—the largest audience in the tournament’s history.

With the 2026 FIFA World Cup, hosted by Mexico, the United States and Canada, the phenomenon will become even larger. The tournament has expanded from 32 to 48 teams, increased from 64 to 104 matches, and will be played in North America—the world’s most lucrative advertising market.

The World Cup has become a $13 billion business, and the tournament’s expansion is reshaping FIFA’s own finances. The organization projects $11 billion in revenue for the 2023–2026 cycle, a 70% increase over the previous cycle, driven primarily by the commercialization of the North American World Cup.

The expected revenue breakdown illustrates the scale of the event: $4.264 billion from broadcasting rights, $3.097 billion from hospitality and ticket sales, $2.693 billion from marketing and sponsorship rights, $669 million from licensing, and $277 million from other revenue streams, according to FIFA. However, several estimates place the tournament’s total economic impact at $13 billion, making it the most profitable sporting event in history.

Energy: From oil to corporate diplomacy

The presence of energy companies in football is no longer coincidental. Oil and gas producers increasingly seek to associate their brands with innovation, sustainability and global connectivity, particularly as the energy transition reshapes the industry. Sports sponsorship has become a form of corporate and national soft power.

The clearest example was Qatar’s strategy during the 2022 World Cup, where international exposure helped reinforce both the country’s geopolitical position and that of its energy companies in Western markets. For hydrocarbon producers and state-owned energy firms, football offers something traditional advertising cannot buy: global legitimacy and emotional connections with consumers and investors.

Technology: Competing for the digital ecosystem

For technology companies, the World Cup represents the ultimate showcase for their data ecosystems, artificial intelligence capabilities and digital services.

The opportunities extend far beyond stadium advertising, encompassing AI-enhanced broadcasting, cloud infrastructure for data processing, real-time analytics, programmatic advertising, cybersecurity, immersive experiences, augmented reality and e-commerce linked to sports broadcasts, among many other applications.

According to FIFA’s post-tournament report, the Qatar World Cup generated 2.7 billion digital and streaming interactions, along with 2.2 billion social media engagements—figures that surpassed those recorded during Russia 2018 and were validated by many of the world’s leading technology companies.

For major technology firms, the tournament is arguably the only event capable of simultaneously delivering global scale and highly sophisticated digital audience segmentation.

Payments: The World Cup as a financial laboratory

The payments industry is arguably the sector that derives the greatest strategic value from these partnerships.

Every fan represents a potential cardholder, digital wallet user, cross-border consumer and future retail investor.

Sponsorship allows companies to transform a sporting event into a platform for accelerating the adoption of digital payments and financial services. It is no coincidence that global payments giants invest hundreds of millions of dollars in sponsorship agreements before committing even larger sums to activation campaigns across dozens of countries.

Some estimates suggest that top-tier global sponsors may spend more than $100 million solely for association rights with the tournament, excluding additional expenditures on marketing campaigns and brand activations.

Aviation: Capturing the growth of global tourism

Airlines use football for far more than selling tickets.

Air connectivity has become strategic infrastructure for international trade and tourism. For airlines, the World Cup represents opportunities to expand route networks, strengthen international hub positioning, enhance loyalty programs, increase premium passenger traffic and attract corporate travelers.

The 2026 edition will span 16 host cities across three countries, generating tens of millions of passenger journeys during just over one month of competition.

Consumer goods: The final frontier of mass marketing

Few industries understand the value of the World Cup better than consumer goods companies.

The tournament remains the only event capable of simultaneously driving impulse purchases, family consumption, higher spending on food and beverages, official merchandise sales and e-commerce growth.

The Qatar World Cup generated more than 15 billion social media impressions and over 3.6 billion video views, extraordinary levels of engagement for consumer-facing brands.

What does this mean for investors?

From the perspective of financial markets and investment funds, the World Cup acts as a catalyst for multiple sectors.

Historically, major sporting events generate temporary spikes in revenue and brand visibility. However, the real value for investors lies in companies’ ability to convert that exposure into long-term customer growth and geographic expansion.

The World Cup has evolved from a competition among national teams into a contest among economic models, global brands and national strategies of influence.

Companies no longer sponsor football simply to sell more soft drinks, airline tickets or credit cards.

They do so because, for one month, the World Cup commands the attention of a large share of the world’s population and offers something extraordinarily scarce in today’s digital economy: a truly global, simultaneous and emotionally engaged audience.

From a geopolitical and financial perspective, few investments provide such significant potential returns in terms of global visibility and strategic positioning.

LinkedIn / Kathleen M. Hutchinson, Director of the SEC Office of International Affairs.

The U.S. Securities and Exchange Commission (SEC) has announced the appointment of Kathleen M. Hutchinson as the new Director of the Office of International Affairs (OIA). The OIA is the department responsible for advising the Commission on international policy, coordinating with regulatory authorities around the world to facilitate cross-border oversight and enforcement, and providing technical assistance.

Hutchinson had served as Acting Director of the OIA since January 2025. Her career at the SEC began in 2003 as a staff attorney in the Office of Compliance Inspections and Examinations (now the Division of Examinations), before joining the OIA in 2008. Within the office, she has held several leadership positions, including Associate Director and Deputy Director, and has served twice as the office’s Acting Director.

“Kathleen has demonstrated a deep commitment to public service and to our mission for more than two decades. I greatly appreciate her willingness to take on the permanent leadership of the Office of International Affairs. She has successfully led numerous international initiatives alongside our counterparts abroad, and I have complete confidence in her continued leadership and guidance on international policy and cooperation,” said Paul S. Atkins, Chairman of the SEC.

For her part, Kathleen Hutchinson said: “The extraordinary talent of the team in the Office of International Affairs makes it a true privilege to work every day in service of investors and our markets. Advancing the SEC’s international priorities through collaboration with foreign counterparts—on policy and supervisory matters, as well as enforcement and technical assistance—is essential to enabling the SEC to fulfill its mission. I am grateful to Chairman Atkins for this opportunity and look forward to continuing to work with the Commission, my colleagues at the SEC, and international authorities to address the regulatory challenges facing global markets today.”

Hutchinson holds a Juris Doctor and a master’s degree in International Relations from the Washington College of Law and the School of International Service at American University, as well as a bachelor’s degree from Binghamton University. She began her legal career in private practice at law firms in Washington, D.C., and New York.

After years of operating without a physical headquarters, CFA Society Brasil has entered a new phase of expansion. The association, which brings together professionals in the country certified by the CFA Institute, reopened its office in São Paulo this year. The goal is to use the new facilities as a base for expanding its influence in the financial market, strengthening its presence beyond the Rio–São Paulo corridor, and increasing the number of events and educational initiatives it offers.

“The Society remained active over the past few years, but we believe we can do much more with the return of the office,” says Lucas Dolabela Barcellos Correa, President of CFA Society Brasil, in an interview with Funds Society conducted at the institution’s new headquarters. The office opened on May 27 on Fidêncio Ramos Street, in the Vila Olímpia neighborhood. “We want to attract new candidates, create value for our members, and positively influence the market,” he says.

The decision to close the previous office was made during the pandemic. Because the CFA exams required in-person attendance and there was uncertainty about how long the health crisis would last, both the CFA Institute and local societies implemented cost-cutting measures. The Brazilian headquarters, located in the Faria Lima district, closed in 2020.

According to the president, the lack of a physical headquarters somewhat limited the organization’s ability to coordinate and integrate its activities, even though the Society continued promoting events and initiatives throughout that period.

“When you dismantle an office, it may seem like you’re only losing a physical space, but it involves much more than that. It’s about having the team together and having a central location for activities. We lost some of that,” he says. CFA Society Brasil currently has 1,822 members and plans to use the new office to expand its role in discussions on the development of Brazil’s capital markets.

“We remain very focused on broadening the reach of our initiatives and strengthening our presence among the market’s key players,” Correa says.

Part of this strategy involves strengthening ties with higher education institutions and training new professionals. The organization continues to run initiatives such as the Research Challenge—a global equity research competition for university students—and seeks to expand its presence at educational institutions outside the traditional hubs for training financial market professionals.

“We need to have a stronger presence at universities,” he says. According to Correa, the idea is to introduce students to the profession early in their careers and present the CFA designation as an option for professional development.

The expansion also includes an institutional engagement agenda. The Society regularly participates in public consultations organized by the Brazilian Securities and Exchange Commission (CVM), maintains dialogue with organizations such as Anbima and Previc, and seeks to contribute to discussions on financial market regulation and best practices.

“We try to be present and express our views in ways that help guide the market in the right direction,” he says.

Another initiative to broaden the organization’s reach is the introduction of specialized certifications developed by the CFA Institute. In addition to the traditional CFA Program, the Institute has been creating credentials aimed at specific market niches, such as ESG, private markets, and Investment Foundations.

A key development is that some of these certifications are expected to be translated into Portuguese over the next few years, reducing one of the main barriers to entry for Brazilian professionals.

“Translating these certifications into Portuguese will be very beneficial in attracting more people to our community,” Correa says.

However, the change has sparked internal discussions among CFA societies worldwide. Since these programs do not require candidates to complete the full CFA Program, it has not yet been decided whether professionals who earn these new credentials will be eligible for membership in local societies.

“For now, it’s an open question. We’re seeing a different audience profile from the traditional CFA Charterholder, and we’re still discussing how this fits within the Society,” he says.

According to Correa, this is a strategic issue for the organization. On the one hand, these certifications could significantly broaden the reach of the CFA brand; on the other, they introduce a new type of professional into the organization’s ecosystem.

Expansion Beyond São Paulo

Although nearly 80% of its members are concentrated in São Paulo, the organization aims to expand its regional reach. Plans include holding events in state capitals such as Belo Horizonte, Porto Alegre, Brasília, and Curitiba, as well as fostering closer ties with universities and professionals in other parts of the country.

“We need to have more influence outside this region as well. It makes sense to have a stronger presence beyond the traditional financial hub,” the executive says.

In addition to geographic expansion, the Society aims to increase the prominence of its events and strengthen relationships with members throughout the country. The plan is to use the new office as a meeting place for discussions on investments, regulation, financial education, and the development of the capital markets.

Attracting New Professionals

The growth strategy also includes training new CFA candidates. The organization runs university programs—such as the Research Challenge, a global equity research competition—and initiatives aimed at integrating women into the financial sector.

One highlight is the Women in Investment Management (YouWIM) program, which selects female university students for an immersive experience in the financial market and seeks to connect them with internship opportunities at banks, asset managers, and other financial institutions.

“We want to bring more women into the financial market,” Correa says.

According to him, the initiative seeks to increase female representation in a sector historically dominated by men while introducing future professionals to the CFA ecosystem during their university years.

Correa emphasizes that the goal is to expand the reach of the certification without compromising the technical rigor that defines the program. Today, only a small fraction of Brazilian financial market professionals hold the designation.

“We’re talking about roughly 1,800 people in a market that may have between 500,000 and 700,000 professionals. It’s an extremely powerful differentiator,” he says.

He also notes that the CFA Program requires approximately 900 hours of study spread across three exam levels, and only a portion of candidates complete the entire process without failing an exam.

Ethics as a Core Value

Although the market often associates the certification with technical investment expertise, Correa says the organization’s primary mission remains promoting the highest ethical standards of the profession.

“Here we’ve talked a lot about valuation, discounted cash flow, and technical skills. But the CFA was founded, to a large extent, on ethics. It’s a recurring subject in every exam and one we reaffirm every year,” he says.

In his view, the Society’s role extends beyond professional education; it also involves participating in public consultations, regulatory debates, and discussions about the future of Brazil’s financial market.

“We want to be the industry’s benchmark and the gold standard for ethics,” he concludes.

Who Is Lucas Dolabela Barcellos Correa?

The current President of CFA Society Brasil, Lucas Dolabela Barcellos Correa, built his career in the financial market before moving into the corporate sector. A graduate of IBMEC, he began his career at Itaú BBA, where he spent several years working in product- and client-related roles. He earned the CFA charter in 2015 and soon afterward joined the organization’s board of directors.

After completing an MBA abroad, he returned to Brazil to launch Horizonte Capital, an investment vehicle focused on acquiring small and medium-sized businesses. He later transitioned to the real economy and currently serves as Chief Financial Officer (CFO) of Dome Serviços Integrados, a logistics company associated with the Port of Açu that specializes in supporting offshore operations for the oil and gas industry.

Correa’s own professional trajectory reflects one of the changes that CFA Society Brasil seeks to communicate to the market: the certification is no longer limited exclusively to investment managers and analysts.

According to him, an increasing number of professionals in the real economy—such as CFOs, corporate finance executives, and specialists in mergers and acquisitions (M&A) and financial planning—are pursuing the program to deepen their technical knowledge and advance their careers.

“More and more people within companies are seeking this knowledge to set themselves apart. Today I’m a CFO, and I still see tremendous value in the CFA,” he says.

On the morning of June 25, 2025, the Mexican financial system discovered that, in certain circumstances, the difference between an accusation and a sentence can be nothing more than a press release. Unbeknownst to anyone at the time, that day would be etched into the history of the country and of finance in the region, while CI Banco, Vector Casa de Bolsa, and Intercam Banco would never again see another day without the shadow of suspicion hanging over them. It was the beginning of the end.

What happened that day was historic for two reasons:

It was the first time the United States used the powers granted under legislation stemming from the fight against fentanyl to act directly against Mexican financial institutions.

Although it was technically not a traditional sanction by the Office of Foreign Assets Control (OFAC), it did impose restrictions on certain transfers and transactions involving the U.S. financial system, which in practice triggered a severe erosion of market confidence.

The fate of the accused institutions had been sealed. There were no handcuffs, raids, or court orders. Nor was there a final ruling from Mexican or U.S. courts. A document issued in Washington by the Financial Crimes Enforcement Network (FinCEN) of the United States Department of the Treasury was enough for three Mexican financial institutions—CI Banco, Intercam, and Vector Casa de Bolsa—to begin the path toward their disappearance as participants in the national financial system.

The accusation was devastating: facilitating money laundering operations linked to fentanyl trafficking and Mexican criminal organizations. The tool used was equally significant. For the first time, Washington invoked powers granted under legislation specifically designed to combat the financing of the synthetic opioid trade.

From that moment on, it no longer mattered whether judicial proceedings had been initiated, whether additional evidence would emerge, or whether the institutions would be able to defend themselves. In financial markets, the presumption of innocence rarely survives the loss of access to the U.S. financial system.

Clients began withdrawing funds, international correspondent banks reviewed business relationships, and counterparties, trustees, investment funds, and service providers activated contingency protocols. The question was no longer whether the three institutions could prove their innocence, but how long they could continue operating under suspicion.

The Mexican government responded by demanding evidence and defending the strength of the national financial system. Authorities insisted there was insufficient evidence to substantiate illicit activities and opted for temporary interventions aimed at preserving stability and protecting clients. But the market had already delivered its own verdict.

Because in global finance, there are institutions too big to fail, but there are also institutions too heavily accused to survive.

One year later, the cases of Vector, Intercam, and CI Banco left an uncomfortable lesson for Mexico and for any economy integrated into the international financial system: the U.S. dollar is not only the world’s reserve currency; it is also a foreign policy instrument and a mechanism of financial discipline capable of crossing borders without the need for judicial rulings.

This story is not merely about three Mexican institutions. It is about the immense power the United States continues to wield over the global financial infrastructure and how, under certain circumstances, an accusation issued from Washington can have deeper and faster consequences than any judicial decision handed down in another country. One year ago, the Department of the Treasury made the accusation, while the market, clients, and counterparties did the rest.

Financial Death

On June 25, 2025, the United States Department of the Treasury reminded the world of a truth that financial markets have known for decades but that is rarely seen so starkly: in global finance, it is possible to survive a bad investment, a liquidity crisis, or even a recession, but it is virtually impossible to survive being shut out of the U.S. financial system.

With the designation by the Financial Crimes Enforcement Network (FinCEN) of Mexico’s CI Banco, Intercam, and Vector Casa de Bolsa as institutions of “primary money laundering concern” in connection with fentanyl trafficking and Mexican criminal organizations, the new powers derived from U.S. legislation specifically designed to combat the financing of the fentanyl trade were officially deployed against financial-sector companies in a partner country.

Formally, it was not a judicial sentence. In practice, it was. Because within the international financial system there exists an unwritten but unmistakable concept: financial death. With the Department of the Treasury’s announcement alone, the fate of CI Banco, Vector, and Intercam had been sealed, and their disappearance became only a matter of time.

Financial death does not mean the immediate closure of offices or the automatic revocation of a banking license. Nor does it require a liquidation order or a final judicial ruling. Instead, it occurs when counterparties stop returning calls, correspondent banks terminate relationships, clients begin withdrawing funds, and the rest of the market decides that the reputational cost of continuing to do business has become too high.

That is exactly what happened. Within hours, questions began coming from institutional clients, trust settlors, exporting companies, fund managers, and corporate treasuries. The issue was not whether the allegations were true or false. The issue was much simpler: what happens if tomorrow this institution loses access to U.S. dollars?

In a globalized financial system, that question alone is enough to trigger a stampede. Mexican authorities responded by defending the strength of the national financial system and demanding that Washington provide concrete evidence supporting its allegations. The official response was clear: if crimes had been committed, Mexico would act, but the accusations had to be supported by verifiable evidence.

However, financial markets rarely wait for the courts. The financial business operates on an extremely scarce commodity: trust.

Trust has one uncomfortable characteristic: it takes decades to build and only hours to disappear. The administrative intervention of the three institutions by Mexican authorities sought to contain systemic risk and protect depositors and investors, while confirming something many market participants understood from the very first day: the problem was no longer legal, but reputational and operational.

Over the following months, there was a slow but steady migration of clients, assets, and business from the accused institutions to other firms in the sector. Deposits declined, business relationships deteriorated, and the dismantling of much of the business the three entities had built over decades began.

The question that remains one year later is an uncomfortable one for Mexico: Can a foreign government effectively destroy Mexican financial institutions without a judgment issued by the country’s own courts? The answer over the past year appears to be yes.

Not because the United States has jurisdiction over Mexico, but because it possesses something arguably even more powerful: control over the world’s reserve currency, the international payments system, and access to the U.S. dollar. For many institutions, being shut out of the U.S. financial system is equivalent to losing access to oxygen.

The paradox is evident. For decades, financial globalization was described as a process of integration and efficiency. The cases of Vector, Intercam, and CI Banco revealed the other side of the phenomenon: the concentration of global financial power in a handful of critical infrastructures controlled directly or indirectly by the United States.

SWIFT, correspondent banking, dollar clearing, and international markets form a network whose main gateway remains in Washington and New York. And whoever controls the gateway largely controls who gets in and who stays out. That is why this case will likely be studied for years in schools of economics, law, and international relations.

Not only because of the money laundering allegations, and not only because of the fight against fentanyl, but because it demonstrated in practical terms the geopolitical reach of the U.S. dollar in the twenty-first century. One year ago, the Department of the Treasury issued an accusation, but the market delivered the sentence—and that may well be the most important lesson of the entire story.

Photo courtesyJuan Hernández, Head of the Americas (Ex-U.S.) at Vanguard

Five years after taking charge of Vanguard’s Latin American operations, Juan Hernández continues to strengthen his profile within the firm. Vanguard has now announced an expansion of his leadership responsibilities, elevating him from Head of Latin America to Head of the Americas (Ex-U.S.).

In this role, the firm said in a statement, Hernández will oversee operations in both Canada and Latin America, continuing to cover the region from Vanguard’s offices in Mexico City.

According to the company, the appointment builds on a career that has steadily gained prominence within the organization. Hernández joined Vanguard in 2017 to lead the firm’s business in Mexico and went on to assume responsibility for the broader Latin American business in 2021. During this period, Vanguard noted, he has strengthened the firm’s presence and relationships with institutional investors, intermediaries and clients across the region.

In addition, earlier this year Hernández took on responsibilities related to the distribution of UCITS products, assuming the role of Head of Global Distribution Outside Europe for these vehicles. “The confidence placed in him is nothing new,” Vanguard emphasized, noting that UCITS represent “one of the asset manager’s key global growth initiatives.”

Now, with the Canadian market also under his supervision, Hernández becomes one of the most influential figures within Vanguard’s international leadership structure. The move reflects the growing importance of the Americas to the asset manager, one of the largest investment firms in the world.

“It remains to be seen whether this commitment to an integrated continental vision will be accompanied by new expansion plans and a deeper engagement with investors across the region,” Vanguard added in its press release.

Amundi recently held its World Investment Forum 2026, titled “Age of Empires?”, where several leading figures from the worlds of economics and finance explored the major macro trends currently shaping the global landscape, as well as the investment opportunities they present.

The event opened with Valérie Baudson, CEO of Amundi, who shared her outlook for the coming year and discussed the firm’s strategic plan. Baudson highlighted the accelerating fragmentation of the multilateral order and the “evident” competition for critical resources, technological supremacy and the race to develop AI capabilities.

On the economic front, she pointed to the resilience of the global economy, which is becoming increasingly diversified; reaffirmed Europe’s resilience and the slowdown in U.S. growth; and noted the divergence within the Chinese economy. In this context, according to Baudson, “fiscal and monetary policy, both in developed and emerging markets, has become increasingly important,” while markets “continue to offer opportunities, provided you know where to look.”

As a result, “in the age of empires, geopolitics has regained primacy over economics.” The relationship between the United States and China will continue along a path of uneasy coexistence, but Europe “can act as a balancing force,” and as the world adapts to the energy crisis, “we are entering a new geoeconomic regime.”

Overall, Baudson believes the U.S. economy is likely to remain strong, although inflationary pressures will persist, “testing the monetary policy of the new Federal Reserve Chair.” In Europe, she expects growth to remain moderate this year, but over the longer term the agenda will revolve around “greater spending on defense and infrastructure, more resilient supply chains and progress in the energy transition.” Asia, meanwhile, will continue to display “multiple pillars of growth,” with Baudson highlighting China and India in particular, while paying special attention to countries dependent on oil and gas imports.

“Markets will adapt to this new reality while continuing to offer opportunities for investors. Artificial intelligence, which was once primarily a technological phenomenon, is now an energy phenomenon that is transforming the competitive landscape,” she said, adding that cybersecurity “will remain a risk we must keep firmly in mind, as will the cost of usage.”

Baudson also emphasized the “quiet but persistent questioning” of U.S. sovereign assets as a pillar of global stability. As “regional dynamics matter increasingly,” diversification “must also take into account currency, region and sector, as well as supply chain exposure and energy security.”

In this environment, Baudson said Amundi’s mission “is clear: to provide clients with resilient portfolios capable of capturing the transformative opportunities ahead.”

From a business perspective, the CEO detailed that retirement solutions and the digitalization of savings are the firm’s two priority growth drivers. To achieve this, Amundi has set two objectives: supporting new digital players and helping banks accelerate their digital transition, with the goal of doubling the number of digital partners by 2028.

Geographically, the firm is focusing on Asia, where it aims to reach €150 billion in investment inflows by 2028. It also plans to “significantly increase market share in Northern Europe, from the UK to Germany,” while noting that its strategic plan also calls for “a stronger presence in high-potential regions such as Latin America.”

According to Baudson, achieving these goals will require innovation in securitization. She highlighted the launch of the first tokenized money market fund and reaffirmed Amundi’s commitment to remaining a leader in responsible investing. She also referenced innovation in both passive and active ETFs, as well as the expansion of technology and digital services through Amundi Technology.

Janet Yellen

Following her opening remarks, Baudson held a conversation with Janet Yellen, former Chair of the Federal Reserve and former U.S. Treasury Secretary, who admitted that the most challenging period of her career was the phase of financial instability, during which she felt like a true “firefighter” dealing with problems created by an “unregulated shadow banking system.”

Yellen acknowledged that concerns about the energy shock “are dominant,” but said the Fed is monitoring inflation appropriately and does not expect an interest rate hike in the coming months, while the possibility of a rate cut has “virtually disappeared.”

She also stated that she had “never before seen threats to central bank independence that come close to those we have witnessed over the past year,” noting that central banks were granted independence so they could focus on price stability and resist pressure from elected political leaders seeking interest rate policies that help manage public debt. In the United States, she said, the interest burden has become “genuinely problematic.”

Regarding the labor market, Yellen said that those who understand AI best “are very optimistic about productivity gains,” but she also noted that productivity improvements often take time to materialize.

“Sometimes it can take decades. AI may move faster, but there could still be a lag,” she said.

Bullard and Trichet

James Bullard, former President of the Federal Reserve Bank of St. Louis, and Jean-Claude Trichet, former President of the European Central Bank, completed the lineup of prominent speakers at the forum, focusing on the evolving monetary order.

Bullard argued that governments appear reluctant to raise taxes or control spending, which in his view will eventually create “problems at some point in the future,” with implications for central bank independence.

“We are approaching an unfavorable policy mix similar to what we saw in the 1970s, when undisciplined governments and central banks, lacking a coherent plan and inflation targets, combined with extensive exchange-rate manipulation, generated substantial volatility and ultimately numerous recessions across many countries,” he said.

At the same time, he encouraged policymakers to “do everything possible” to promote technological progress and rising living standards, while avoiding political developments that “take us back to a past that did not work.”

Bullard also addressed central bank projections. While he described scenario analysis as “useful” and helpful in “visualizing possible paths, pricing markets and calculating returns under different conditions,” he emphasized its limitations and argued that assessing future risks requires collaboration between central banks and the private sector.

For his part, Trichet described Europe’s role in today’s fragmented geopolitical landscape as “very important.”

“Perhaps I am too optimistic, so I should be cautious,” he said, before noting that the four currencies issued by the major central banks of the advanced economies—the U.S. dollar, euro, yen and pound sterling—share the same definition of price stability.

“In my view, this is extremely important,” he said, arguing that since the explosion of retail finance, “this represents the most dramatic change in the international monetary system since the end of the modern era.”

“That makes me somewhat more optimistic about our ability, despite all the challenges, to preserve both price stability and financial stability,” Trichet concluded.

Amid a global environment marked by macroeconomic volatility, trade tensions and tighter financial conditions, Latin America remained attractive to investors and closed 2025 with double-digit growth in mergers and acquisitions (M&A) activity.

According to “Unlocking Potential: Latam M&A and PE Activity in FY 2025,” a report published by Marsh, the global leader in risk, reinsurance, capital, people, investments and management consulting, the total value of transactions involving Latin American assets reached $114.3 billion, representing a 16% increase compared with 2024. The number of transactions, however, declined slightly to 1,345 deals, reflecting a global trend toward larger and more complex transactions.

Brazil remained the region’s leading market, recording 850 transactions with an aggregate value of $55.1 billion. Mexico and Colombia completed the group of most active countries, supported by strategic infrastructure and energy deals that continue to attract international capital.

The primary driver of growth was the energy, mining and utilities sector, which generated $42.6 billion in transaction value, representing a 25% year-over-year increase. Rising energy demand linked to the expansion of artificial intelligence, data centers and the transition to cleaner energy sources fueled investor interest in renewable energy assets, power transmission and electrical grid infrastructure.

The largest transaction of the year was GE Vernova’s acquisition of the remaining 50% stake in Prolec in Mexico for $5.3 billion, underscoring the growing strategic importance of energy infrastructure across the region.

Private equity also experienced one of its strongest rebounds of the year. Private equity transactions totaled $19.8 billion, representing a 106% increase from 2024, although the number of deals declined to 189 transactions.

Activity was driven primarily by investments in infrastructure and renewable energy, including Actis and GIC’s acquisition of a controlling stake in Serena Energia for $2.8 billion, as well as the acquisition of Orygen in Peru.

The technology, media and telecommunications (TMT) sector also remained highly active. With 278 transactions, TMT was the most active segment by deal count, supported by consolidation among telecommunications operators and the need to accelerate investment in fiber-optic networks and 5G technologies.

Among the most notable transactions was Millicom’s acquisition of Telefónica’s Colombian subsidiary, highlighting the sector’s ongoing consolidation as operators seek greater scale to meet growing demand for digital services.

At the same time, the nearshoring trend continues to strengthen demand for logistics infrastructure and data centers, creating new opportunities across both the real estate and infrastructure sectors.

Despite this momentum, the market faces significant challenges. Inflationary pressures, shifting tariff policies and a more restrictive financing environment have widened valuation gaps between buyers and sellers, increasing the complexity of negotiations.

In response, investors and financial sponsors are increasingly turning to transactional risk transfer solutions such as Representations & Warranties (R&W) insurance to reduce uncertainty and facilitate deal completion.

Felipe Escallón, Head of Private Equity and M&A for Florida and Latin America at Marsh, noted that the region has remained resilient despite macroeconomic volatility and geopolitical and regulatory challenges.

“Investors and sponsors are increasingly relying on transactional risk solutions to reduce uncertainty, bridge valuation gaps and facilitate faster and more secure execution of cross-border transactions,” he said.

Looking ahead to 2026, expectations point to a continuation of the trends observed last year, with investment increasingly concentrated in renewable energy, power grids, infrastructure and telecommunications, alongside growing participation from private equity funds.

However, industry experts agree that access to capital alone will no longer be sufficient. The ability to structure transactions effectively and manage associated risks will be a critical factor in turning investment opportunities into successful deals.

Franklin Templeton has announced the completion of its acquisition of 250 Digital, an active cryptocurrency investment management firm led by digital asset industry veterans Christopher Perkins and Seth Ginns. According to the firm, the transaction includes 250 Digital’s investment team as well as all liquid cryptocurrency strategies previously managed by CoinFund. As part of the agreement, Franklin Templeton will invest in those strategies.

The completion of the acquisition reflects Franklin Templeton’s long-term commitment to building infrastructure within the digital asset ecosystem and its conviction in the technologies that, according to the firm, will shape the next generation of institutional investing.

Business Division

With the completion of the transaction, Franklin Templeton has formally established Franklin Crypto, its dedicated active digital asset management division. Perkins will serve as Head of Franklin Crypto, while Ginns will assume the role of Chief Investment Officer (CIO), working alongside Tony Pecore, a long-time digital asset investment specialist at Franklin Templeton. Franklin Crypto will report directly to Sandy Kaul, Franklin Templeton’s Head of Innovation.

Franklin Crypto will provide institutional investors with actively managed cryptocurrency strategies, combining the investment expertise of the former 250 Digital team with Franklin Templeton’s global distribution platform. The new division complements Franklin Templeton’s existing digital asset capabilities, which already include a fully dedicated team focused on fundamental research, active portfolio construction and institutional risk oversight.