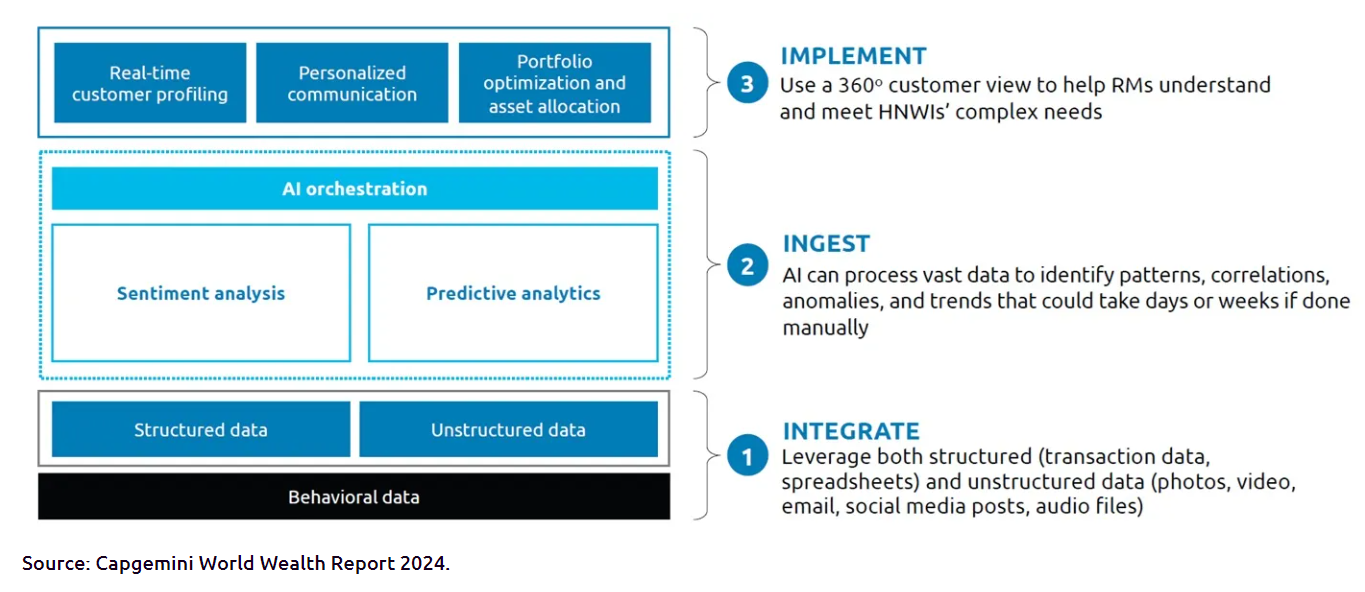

Building scalable AI-driven behavioral finance solutions requires a structured approach, according to a Capgemini study. This involves integrating diverse data sources by leveraging both artificial intelligence and generative AI capabilities. Additionally, the integrated data must be ingested using sentiment and predictive analysis based on AI, and the derived insights should be implemented to drive real-time customer profiling, portfolio optimization, and hyper-personalized experiences for high-net-worth individuals, as noted in the study.

This holistic approach not only enhances customer experiences but also empowers advisors by automating mundane tasks, optimizing their time, and minimizing errors. For example, the study cites firms like RBC Wealth Management U.S., which are already utilizing Salesforce’s “Personalized Financial Engagement” solution to integrate disparate data systems, create unified client profiles, and offer intelligent, automated customer journeys using generative AI.

However, executing a structured approach successfully is a significant challenge. To ensure that a company can efficiently integrate, ingest, and implement data to achieve necessary business value, Capgemini recommends six critical steps:

1. Make internal data accessible: For banks, the key question is not whether they have valuable data, but whether that data can be located and accessed by AI applications in real time. Isolated, hidden, and poorly labeled datasets need to be connected, cleaned, and standardized across business units and acquired entities.

2. Incorporate external data: While retailers commonly use third-party data to gain deep insights into customers, banks have lagged behind. To fully realize the promise of behavioral finance, banks must identify and integrate appropriate external sources with internal data repositories.

3. Set up robust AI infrastructure: Data must be delivered quickly to AI applications, as latency can severely limit AI’s ability to derive relevant insights. Banks need to design and deploy the appropriate computing, storage, networking, and cloud infrastructure to support AI foundations.

4. Adopt AI and generative AI solutions for finance: Understanding customer psychographics, creating hyper-personalized financial plans, and offering high-level client experiences requires adopting robust, purpose-built AI applications. Capgemini’s “Augmented Advisor Intelligence” solution, for instance, helps relationship managers make informed decisions and generate client-oriented communications.

5. Prepare to expose AI insights to clients: While AI for behavioral finance and customer communications is currently an internal function, high-net-worth individuals will eventually seek self-service capabilities alongside personal interactions with their relationship managers. To meet this future demand seamlessly, banks must design the architecture of technology and application bases with foresight.

6. Address regulatory concerns: As with any new technology, implementing AI solutions must comply with regulations to minimize risks of deviations or losses caused by AI applications. In addition to properly designing, deploying, and monitoring AI applications, banks should maintain human oversight between AI applications and customers, at least for now.

This comprehensive strategy is essential for financial institutions to maximize the benefits of AI-driven behavioral finance solutions while mitigating risks and preparing for future innovations.

BlackRock and Global Infrastructure Partners (GIP) have announced the “successful completion” of BlackRock’s acquisition of GIP, following its announcement in January of this year. According to the asset manager, “this combination creates a leader in the infrastructure industry, covering capital, debt, and solutions, while providing a diverse range of expertise and exposure in the infrastructure sector across both developed and emerging markets.”

The firm explained that the combined infrastructure platform will carry the Global Infrastructure Partners (GIP) brand, as part of BlackRock. GIP will continue to be led by Bayo Ogunlesi and the Office of the Chairman. Additionally, with approximately $170 billion in assets under management, the platform will have a global team of 600 people managing a diversified portfolio of over 300 active investments, operating in more than 100 countries.

With this combination, BlackRock consolidates over $100 billion in assets under management in private markets and approximately $750 million in annual management fees, increasing its private market assets by about 40% and expanding its recurring revenue.

“Infrastructure represents a generational investment opportunity. With the combination of BlackRock and GIP, we are well-positioned to capitalize on long-term structural trends that will continue to drive infrastructure growth and offer superior investment opportunities for clients worldwide. We are thrilled to welcome Bayo and the talented GIP team to BlackRock, and we look forward to delivering this combined infrastructure investment expertise to our clients,” highlighted Larry Fink, Chairman and CEO of BlackRock.

Meanwhile, Bayo Ogunlesi, Chairman and CEO of Global Infrastructure Partners, added, “We are excited to begin this new chapter as Global Infrastructure Partners (GIP), part of BlackRock, with the goal of creating the world’s leading infrastructure investment firm. The combination of our institutional intellectual capital, investment and business enhancement capabilities, global presence, and corporate and governmental relationships will allow us to offer attractive investments for our investors and innovative solutions for our clients.” For now, BlackRock plans to appoint Bayo Ogunlesi to its Board of Directors at its next meeting.

Amundi has announced the expansion of its fixed income offering in emerging markets with the launch of the Amundi JP Morgan INR India Government Bond UCITS ETF, with management fees of 0.30%.

According to the asset manager, the ETF replicates the JPM India Government Fully Accessible Route (FAR) Bonds Index, which covers Indian government bonds denominated in Indian rupees that have been made accessible to foreign investors, opening up investment routes for international participants in India’s bond market. This new launch highlights Amundi’s commitment to offering investors solid and accessible investment options with potentially attractive returns and diversification benefits.

India’s growth story, both at the macroeconomic level and within its fixed income market, presents an interesting investment case for investors, according to Amundi. “Furthermore, the recent inclusion of Indian government debt in the J.P. Morgan GBI-EM Global Series indices is driving increased demand and liquidity in the country’s fixed income markets. This, in turn, should strengthen the case for these securities, which can serve as a diversifying element in a global portfolio allocation,” the asset manager adds.

Following the launch of this new fund, Benoit Sorel, Director of Amundi ETF, Indexing & Smart Beta, emphasized: “India’s economic momentum and the recent inclusion of its government bonds in major global indices present a unique opportunity for international investors. With the launch of this ETF on Indian government debt, we are enabling our clients to access an enhanced portfolio diversification tool at a competitive market price.”

Jupiter Asset Management has announced the proposed acquisition of the investment team and assets managed by Origin Asset Management, a London-based global investment boutique, as part of a broader review of the firm’s emerging markets franchise.

Under the terms of the deal, more than 800 million pounds of predominantly institutional assets currently managed by Origin will be transferred to Jupiter AM, subject to customary approvals and consents. These assets are primarily held in long-standing segregated institutional mandates for a globally diversified client base, spanning Europe, Canada, and Australia.

The acquisition aligns with Jupiter’s growth strategy, particularly in strategically important areas such as the institutional client channel and the group’s international business. Jupiter notes that Origin brings additional scale to its Global Emerging Markets strategy and provides investment capabilities in International ex-US and Global Smaller Companies, areas of identified demand that will expand Jupiter’s ability to attract a wider range of clients.

Origin invests using a quantitative stock selection approach, combining proprietary algorithms and data with qualitative due diligence by its experienced investment team. The team consists of five investment professionals, all of whom will move to Jupiter upon completion of the acquisition, ensuring that their investment process remains intact. Origin’s strategies in Global Emerging Markets, International ex-US, and Global Smaller Companies have consistently outperformed their benchmarks over both the short and long term.

“I believe that the addition of the Origin team offers an attractive option for clients of both firms on the Jupiter platform as we look to broaden our offering. In addition to strengthening our global equity range and adding new global small-cap capabilities, the acquisition is a key part of our efforts to scale our emerging markets capabilities as we aim to build truly differentiated investment propositions. Origin’s rigorous and robust investment process, which combines both fundamental and quantitative elements, is unique and has delivered strong long-term results for clients,” commented Kiran Nandra, Head of Equities at Jupiter AM.

Meanwhile, Tarlock Randhawa, Managing Partner at Origin, added: “We are excited to join Jupiter, whose philosophy and culture of truly active and differentiated investment management aligns with our own, and whose strong client-centric approach is very clear. The transition for our existing clients will be seamless, and we believe they will benefit from Jupiter’s commitment to excellence in the client experience. In addition to the benefits for current clients, we are well positioned to grow our client base and assets over time.”

Additionally, Jupiter AM announced that Nick Payne, lead portfolio manager of Global Emerging Markets Equities, will leave the company at the end of 2024 to pursue other opportunities.

Alfonso del Castillo, global head at Santander Private Banking.

Changes in the structure and leadership of Santander Private Banking teams, led by Alfonso del Castillo, the global head, who has established his office in Madrid, moving from his previous position in Miami. The entity has made new appointments and a new addition, with the aim of accelerating its international growth.

The new addition to the team is Carmen Gutiérrez, the new head of the Global Family Office, who will lead the entity’s value proposition across all geographies. She has developed her career in institutions such as Julius Baer and Credit Suisse, in countries like Mexico and Switzerland.

The other positions have been filled with professionals from within the company. Antonio Costa, who was CEO in Switzerland (BSISA) for many years, has been appointed as the Global Head of Commercial, a newly created position in which he will be responsible for strengthening the entity’s business dynamics in all countries. His previous role will be assumed in 2025, pending the relevant regulatory approvals, by Frans Von Chrismar, who will be the new head of BSISA, the Swiss unit.

Verónica López-Ibor, previously head of Products and Private Wealth at BPI, will be the new Global Head of Products and Investments.

Javier Martín-Pliego has been appointed Global Head of Strategy, a position from which he will develop, coordinate, and implement the entity’s growth projects.

Additionally, Beltrán Usera will be the new Global Head of the UHNWI segment, which serves the group’s high-net-worth clients. Usera will relocate from New York to Madrid to take on this new role, where he will lead local and global teams serving ultra-high-net-worth clients to implement a coordinated global strategy in this area.

The Global CIO for Santander Private Banking will be Kamran Butt. He has been the CIO for the Middle East and will now hold both roles.

Meanwhile, Víctor Moreno will lead the Strategic Solutions unit globally, which he had previously co-led from Miami.

Javier Rodríguez Hergueta, in turn, expands his current role at BPI by taking on global leadership over Private Banking Platforms.

Additionally, the entity has appointed a new Global Head of Transformation, which will be Carlos Rengifo.

Klosters Capital, a multi-family office based in Florida, United States, and Capital Advisors, an independent Chilean financial advisor, have entered into a collaboration agreement to jointly serve the Latin American wealth management market from Miami. Klosters Capital has been operating in Miami since 2016 under a Registered Investment Adviser (RIA) license, serving clients from the United States and Latin America. Since 2022, it also has an office in Madrid, Spain, where it operates as a financial advisory entity (EAF).

For Javier Rodríguez Amblés, Managing Partner of the company, “this agreement represents a strategic alliance that allows us to extend our services to several countries in the region where we had little presence, such as Chile, Peru, and Argentina, where Capital Advisors has established experience.”

With 25 years of experience, Capital Advisors is a recognized independent financial advisor that advises clients in Chile, Argentina, and the United States.

Pablo Solari, a partner at the firm, adds that “this agreement allows us to consolidate our presence in the United States by supporting our clients through Klosters Capital’s platform, with which we share a strategic business vision and the same values in the management and advisory of our clients.”

Capital Advisors is a member of the Global Association of Independent Advisors (GAIA), where all members must remain certified by CEFEX (Center for Fiduciary Excellence). This entity, headquartered in Pittsburgh, aims to “promote and verify excellence by evaluating and certifying compliance with high professional standards of conduct,” according to its website. In 2018, Capital Advisors Family Office became the first Latin American investment advisor to receive this recognition.

Both companies share a business model in which they are compensated exclusively by their clients, ensuring and guaranteeing their independence and rigor in management, always prioritizing the interests of their clients.

Bitpanda, a platform specializing in digital assets, has announced a collaboration with Societe Generale-FORGE (SG-FORGE), an integrated and regulated subsidiary of Société Générale Group. Through this partnership, Bitpanda will offer the EUR CoinVertible (EURCV) stablecoin, managed by SG-FORGE and compliant with MiCA1 regulations, to the entire European market. This agreement stems from the commitment of both companies to increase accessibility and adoption of digital assets across Europe.

Thanks to Bitpanda’s reputation and its extensive user base, European investors will have access to a stable, secure, and accessible digital currency. As a dedicated issuer of a reliable stablecoin, SG-FORGE focuses on delivering seamless financial experiences to its users.

Regulated stablecoins, such as EURCV, aim to bridge the gap between traditional finance and new digital economy products. They provide a stable and reliable store of value, particularly given the inherent volatility of cryptocurrencies.

With this collaboration, EURCV can expand across Europe and be used for cross-border payments, remittance transfers, or daily transactions, thanks to the ease and security offered by Bitpanda’s ecosystem.

Lukas Enzersdorfer-Konrad, Deputy CEO of Bitpanda, stated that euro-based stablecoins “are essential for the future of digital assets in Europe. The landscape is changing, the integration with traditional finance is increasing, and fully regulated stablecoins are the key to making this possible. We will work with Societe Generale-FORGE to bring that future closer.”

Jean-Marc Stenger, CEO of Societe Generale-FORGE, explained that this partnership “is a crucial step toward realizing our vision of making stablecoins a central component of the global financial system. Together with Bitpanda, we are confident in our ability to offer European users a stable, secure, and accessible digital currency.”

BlackRock and Santander have announced the signing of a memorandum of understanding under which funds and accounts managed by BlackRock will invest up to $1 billion per year in specific financing projects, energy financing, and infrastructure debt investment opportunities with Santander through structured transaction formats.

The agreement continues a previous one in which funds and accounts managed by BlackRock agreed to provide financing for a diversified $600 million infrastructure credit portfolio of Santander.

“We are thrilled to extend our long-standing relationship with Santander through this agreement, which will provide long-term, flexible capital on a recurring basis to support the growth of their project finance franchise. At the same time, this collaboration will provide greater access to attractive and differentiated investment opportunities for our clients now and in the long term,” said Gary Shedlin, Vice Chairman of BlackRock.

“This framework agreement with BlackRock will allow us to continue proactively rotating our assets, further strengthening our financial position, and enabling us to generate capital for additional profitable growth. We look forward to working with BlackRock through this expanded partnership,” said José García Cantera, CFO of Santander.

BlackRock’s private debt franchise, valued at $86 billion, offers differentiated, flexible, and scalable financing solutions to a wide network of financial institutions and global corporate relationships. The company has developed one of the leading infrastructure debt franchises in the market, sourcing, structuring, and managing client assets with revenue-generating potential.

To mark New York Climate Week, the global technology platform Clarity AI has presented its new study, “Carbon Reporting Trends: Has Global Progress Stalled?” The report shows that greenhouse gas (GHG) emissions disclosure by companies has reached a point of stagnation: 80% of companies in the MSCI ACWI index report their Scope 1 and 2 emissions, but only 60% disclose at least part of their Scope 3 emissions. The study also highlights significant regional disparities and ongoing challenges in the quality of Scope 3 data.

“Despite advancements in emissions disclosure in recent years, our results show a concerning stagnation,” said Nico Fettes, Director of Climate Research at Clarity AI. “With increasing disclosure requirements for financial institutions regarding financed emissions, the demand for detailed and accurate corporate emissions data continues to grow. However, many companies still do not provide the comprehensive information necessary for effective climate risk analysis. This lack of transparency not only hampers informed decision-making by investors and stakeholders but also limits the public’s ability to understand and respond to climate risks, thereby affecting efforts towards a more sustainable future.”

Only 60% of Companies Report Scope 3 Emissions

While nearly 80% of companies in the MSCI ACWI index have disclosed their Scope 1 and 2 data, only 60% report any of their Scope 3 emissions, leaving a significant gap. This result reflects a slowdown in the growth of Scope 3 disclosure, particularly in emerging Asian markets, where only 41% of companies report these emissions, compared to nearly 90% in Europe and Japan.

Scope 3 Data Quality Improves by 130%, but Gaps Persist

Since 2019, the quality of Scope 3 emissions data has improved by more than 130%, according to Clarity AI’s internal reliability models. This improvement is largely due to more companies reporting both a greater number of categories and more relevant Scope 3 categories. However, the overall quality of these data still falls short of what should be considered sufficiently high-quality disclosure, highlighting the need for more robust reporting practices.

U.S. Companies Are Closing the Gap in Scope 1 and 2 Disclosure

Companies in Europe and Japan lead in Scope 3 emissions disclosure, with nearly 90% reporting this data. In contrast, emerging markets in Asia are falling behind, with only 41% of companies disclosing Scope 3 emissions. However, the growth rate of disclosure has stabilized across all regions.

In the United States, significant progress has been made. Since 2019, when the disclosure rate was much lower, U.S. companies have reached a 90% disclosure rate for Scope 1 and 2 emissions, almost matching their European and Japanese counterparts. Nevertheless, like the global trend, only 60% of U.S. companies report any of their Scope 3 emissions, underscoring the ongoing challenge of achieving comprehensive emissions disclosure, even in regions where Scope 1 and 2 reporting has improved significantly.

BBVA and global investment firm KKR have formed a strategic alliance to support the decarbonization of the economy. As part of this partnership, BBVA will invest $200 million (€187 million) in KKR’s global climate strategy, which focuses on large-scale investments in solutions that drive the transition to a low-carbon economy.

Both companies made this announcement during Climate Week held in New York this week. The agreement aims to identify new investment opportunities related to climate infrastructure, particularly those supporting the energy transition and electrification. It will also leverage the complementary strengths of both companies, facilitate knowledge exchange, and advance shared goals to accelerate the energy transition.

“We believe that in the second half of this decade, we will see strong growth in new low-carbon infrastructure. The opportunity is immense, and BBVA aims to become a leader in advising and financing to support our clients in the U.S. and Europe in building this future infrastructure across key transition sectors—Energy, Construction, and Mobility, among others. This ambitious alliance with KKR will be a key component of our sustainability strategy. Both teams will work together to seize this growth opportunity for our businesses,” said Javier Rodríguez Soler, BBVA’s Global Head of Sustainability and CIB.

“To tackle the major decarbonization projects the world needs, it’s essential to have top global investors and financial institutions. Large asset managers and international banks are needed to finance this transition and accompany all sectors on their respective decarbonization paths in an orderly manner. With KKR’s proven expertise in this field, we will share knowledge and combine teams, capabilities, and efforts in this strategic alliance to multiply investment in infrastructure and climate projects,” added Rodríguez Soler.

Emmanuel Lagarrigue and Charlie Gailliot, co-heads of KKR’s Global Climate Strategy, added, “We are still in the early stages of what will be a multi-decade transition to net-zero emissions, representing one of the greatest investment opportunities of our time and requiring the full participation of the financial sector. We are thrilled to collaborate with BBVA, given their leadership in the renewable energy sector and their deep commitment to mitigating climate change impacts.”

BBVA aims to support and help its clients transition to a more sustainable world. To this end, sustainability is at the core of its business and is one of its six strategic priorities. The bank has identified decarbonization and ‘green’ technologies as two of its priority investment areas. To support this, it has created a global financing unit specialized in clean technology or ‘cleantech’ innovation. The team, based in New York, London, Madrid, and Houston, offers financing and advisory services.

BBVA is actively investing in some of the most cutting-edge and innovative climate action funds, with the goals of achieving financial returns, participating in disruptive projects, and gaining knowledge of these technologies to better advise companies affected by these innovations and in need of financing.

On September 12, BBVA announced the creation of a sustainability hub in Houston, aimed at leading the financing of the energy transition in the United States.