GPTAdvisor, a financial advisory firm powered by artificial intelligence, has announced its expansion into the Americas with the addition of Camila Rocha as Co-founder & General Manager for the region, according to a statement.

“This strategic move marks the beginning of a new phase for the company, strengthening its presence in the region and bringing its artificial intelligence platform to more businesses and professionals,” the firm stated.

GPTAdvisor already has clients in the region, such as the Uruguayan firm AIVA, and highlights that the opening of its office in Mexico reinforces its commitment to the American market. The company aims to offer solutions tailored to local needs, optimizing financial decision-making through advanced artificial intelligence.

With extensive experience in the technology and financial sectors, Camila Rocha will lead GPTAdvisor’s expansion and localization strategy in the Americas.

“The hot topic today is artificial intelligence, but companies still don’t know how to integrate it into their daily operations. GPTAdvisor offers a proven solution that addresses precisely this need, providing the AI applicability layer that is key to business success today,” said Rocha.

“The Americas represent a strategic opportunity for GPTAdvisor. With Camila leading this expansion, we are confident that we can understand and respond to the specific needs of the local market, offering a truly relevant solution for our clients,” stated Salvador Mas, CEO of GPTAdvisor.

Currently, GPTAdvisor serves well-known clients in Europe, including Santander, Bankinter, and ANDBANK, among others. With its expansion into the Americas, the wealthtech aims to add the region’s leading financial institutions to its client portfolio, further solidifying its leadership in AI-driven financial advisory.

Operations in the Americas began in February 2025, and the company is already working on adapting its platform to provide closer and more efficient support to users in the region.

The election result in Germany has been clear: the Christian Democratic Union/Christian Social Union (CDU/CSU) won the legislative elections on Sunday, receiving 28.6% of the votes, according to preliminary and official results. Based on investment firms’ interpretation of this outcome, the most likely scenario is a coalition with the SPD, despite the challenges of reaching an agreement. For this reason, they warn that the greatest risk for the markets is that the debate over the governing coalition drags on.

“The centrist parties failed to retain a constitutional majority, which complicates the prospects for a decisive shift in fiscal policy. In fact, any modification of the debt brake reform will need support from either the Left or the AfD. The latter opposes reforming the debt brake, while the former might support it to increase investment—but not defense spending. Therefore, complex political agreements and fiscal creativity would be required. Looking at the bright side, one could argue that the reduced room for maneuver in national defense spending could be positive for the EU, with Merz potentially supporting more joint EU borrowing,” notes Apolline Menut, an economist at Carmignac.

Lastly, as Moëc points out, “a shift toward sovereignty in defense matters for Germany and Europe implies a strong sense of political direction in Berlin.” The economist highlights the “profound change in Germany’s strategic defense doctrine” under the next German Chancellor, Friedrich Merz, of the CDU, a party that, as Moëc notes, “has historically been the strongest advocate for alignment with the United States on defense matters.”

According to Ebury, since the formation of a majority government is not expected, perhaps the biggest risk for financial markets is the possibility that coalition negotiations will be prolonged, potentially lasting weeks or even months. “In 2017, the grand coalition government took office almost six months after the elections, following the failure of coalition talks between the CDU/CSU, the Greens, and the Free Democrats. Similarly, after the 2021 elections, the ‘traffic light’ coalition government was formed after 73 days. Markets do not react favorably to uncertainty, and as usual, a prolonged period of political uncertainty could weigh on the euro, as it would delay the necessary reforms to lift the economy out of its slump,” they state in their latest report.

Germany’s Challenges

What will happen with the other challenges facing Germany? According to Stefan Eppenberger, senior strategist, and Michaela Huber, cross-asset strategist at Multi-Asset (a Vontobel boutique), when it comes to much-needed reforms, the decisive factor for the German economy (and financial markets) will be whether the new government alters the debt brake. According to Article 115 of the Grundgesetz, the federal government has a “strictly limited structural borrowing margin, meaning it is independent of economic conditions.” Specifically, this means that the “maximum net borrowing allowed” is limited to 0.35% of GDP.

“In addition to greater fiscal policy stimulus, financial markets expect a corporate tax cut, a reduction in bureaucracy, lower electricity costs through reduced grid and energy tariffs, and labor market liberalization. However, much of these measures are likely to be difficult to implement under the new coalition government,” explain the two experts.

Meanwhile, David Kohl, chief economist at Julius Baer, adds: “A new conservative-led government will have the opportunity to address some of Germany’s economic challenges, such as investment shortages and high labor costs.” However, he believes the political shift’s impact may easily prove disappointing, as challenges such as an aging workforce, a skilled labor shortage, and regulatory burdens persist. “We expect a return to economic growth in 2026, and moderation in wage agreements should lead to disinflationary forces,” Kohl adds.

According to Pedro del Pozo, director of financial investments at Mutualidad, “Germany’s economic woes would make much more sense to be addressed with a more active fiscal policy, including allowing for higher borrowing for investment—something that, given the country’s fiscal health, is perfectly feasible.” He also believes that “the main reason that will lead the ECB to cut rates remains the improvement in inflation data, especially considering the ECB’s own projection for price developments in Europe, which should stabilize at a 2% increase by the end of the year.”

Implications for Assets

Given this context, DWS believes that the policies outlined in the final coalition agreement—and, more importantly, their eventual implementation—will be decisive for the markets. “For German and, indeed, European public debt, we foresee a limited impact, though the swift formation of a new government and subsequent reforms would be seen as positive for long-term growth prospects. Similarly, the impact on currency markets appears moderate. Regarding corporate credit, we do not see a significant impact, whether or not a government is formed quickly. Germany represents 14% of the iBoxx Euro Corporate Index, which is well-diversified in terms of sectoral exposure,” they state in their latest report.

Regarding the impact on equities, they note that there may be some disappointment that the Christian Democrats did not secure a stronger mandate for greater deregulation and reduced wealth redistribution. “But even such reforms would have had little immediate impact on earnings expectations. In any case, and especially for European equities in general, the most important question will likely be how quickly the continent’s largest economy can form an effective government amid, for example, U.S. tariff threats,” they add.

In this regard, BlackRock Investment Institute shares a similar assessment. “European stocks have outperformed their U.S. counterparts this year and are much cheaper relative to historical valuations than they have been in decades. With much bad news already priced in, even the prospect of good news could help push them higher. German fiscal stimulus may still be a long way off, but regional markets will welcome greater political clarity,” they state in their latest report.

Additionally, they recall that a de-escalation of the war in Ukraine could lower energy prices and stimulate European growth. “The EU now has a sense of urgency that typically drives action: an extraordinary defense summit will be held next week. The European Central Bank is expected to further cut rates this year, as eurozone growth remains sluggish and inflation has declined. We maintain our relative preference for eurozone bonds over U.S. Treasuries, especially long-term bonds,” they indicate.

Finally, DWS asserts that for private infrastructure, a quickly formed government focused on project execution would be crucial. “In the real estate sector, we highlight the restrictions on how quickly residential rents can rise in high-demand areas. The outgoing government had already planned to extend these restrictions until 2029 under relatively favorable conditions for landlords. Given the significance of rent control as an election issue—especially in terms of mobilizing support for The Left—we would not be surprised to see slightly stricter regulations than previously planned,” they conclude.

For Gilles Moëc, chief economist at AXA IM, a bipartisan coalition between the center-right CDU and the center-left SPD is in a position to govern. “CDU and SPD share a common interest in increasing defense spending and supporting Ukraine, as well as a strong pro-European perspective.”

The growth of the European active ETF market continues. This time, Schroders joins other asset managers and takes a further step by registering such a vehicle in Ireland.

It is worth noting that the firm already operates with active ETFs in the U.S. and Australia, and now aims to bring its expertise to the European market.

As explained, this active ETF has been launched as an Irish collective asset management vehicle under the Irish Collective Asset-Management Vehicles Act of 2015.

Regarding the registration of the new active ETF, Schroders states, “As the industry evolves and the range of fund structures expands, we constantly review what our clients demand and which structures are most effective for managing their investments. With the growth of the active ETF market across Europe, we are assessing where offering these new fund structures can add value for our clients.”

The U.S. SEC announced last week a regulation on so-called “emerging technologies” that includes both digital currencies and artificial intelligence. Countries like Brazil, Mexico, or Chile already have advanced legislation on cryptocurrencies, but AI is being addressed separately.

What do cryptocurrencies have to do with AI? If we read the SEC‘s statement, U.S. authorities seem concerned with fraud prevention as well as promoting the technology sector.

Brazil, a Pioneer in Cryptoasset Regulation, in the Midst of AI Debate

The National Congress of Brazil is currently debating AI legislation, seeking to balance innovation and the protection of fundamental rights. In December 2024, a bill was passed that proposes a regulatory framework and whose main mission is to protect the intellectual property of creators. On the other hand, cryptoasset regulation has been in place for several years; the first law was passed in 2022 and defines virtual assets as a regulated category. The Central Bank must take on the role of regulatory body, ensuring greater oversight of exchanges and transactions. However, the market is still waiting for secondary measures to clarify aspects such as regulatory compliance and investor security. Brazil is the country with the highest adoption of cryptoassets in Latin America, a sector growing in e-commerce, remittances, and cross-border payments. Traditional Brazilian banks have started offering digital asset services.

Chile and Its National Center for Artificial Intelligence

The case of Chile is somewhat similar to that of Brazil: cryptocurrency regulation dates back to 2022, and parliament is currently debating artificial intelligence. However, the Andean country already has a slight advantage as since 2021 it has had a National Center for Artificial Intelligence (CENIA). The Chilean regulation on digital assets—or Fintech Law—defines a cryptoasset as “a digital representation of units of value, goods, or services, with the exception of money, whether in national currency or foreign exchange, which can be transferred, stored, or exchanged digitally.” The Comisión para el Mercado Financiero (CMF) is responsible for regulating the sector.

The Chilean government published its first national AI policy in 2021. Since then, the country has created CENIA, promoted AI-focused PhD scholarships through the National Agency for Research and Development (ANID), launched 5G networks, developed the first AI doctorate in Chile and Latin America, and implemented the Ethical Algorithms Project, among other initiatives. This policy remains in effect, and according to the institutional portal of the Chilean Ministry of Science, it is anchored in three pillars: enabling factors, development and adoption, and governance and ethics. These definitions resulted from a participatory process conducted in 2019 and 2020. More recently, in May 2024, the government took another step and presented a bill aimed at regulating and promoting the development of this technology. This initiative is still in its first constitutional process in the Chamber of Deputies at the time of this report.

Mexico Awaits the AI Debate

In Mexico, the Fintech Law recognizes cryptocurrencies as digital assets and allows their use as a payment method within the financial system. It also regulates electronic payments, crowdfunding, and digital assets. There are two types of ITFs (Financial Technology Institutions): crowdfunding institutions and electronic payment fund institutions (digital wallets). The law defines virtual assets (cryptocurrencies) as “the representation of value recorded electronically and used among the public as a means of payment for all types of legal acts, whose transfer can only be carried out through electronic means.” The Bank of Mexico (Banxico) supervises processes, and Banxico must authorize virtual assets before ITFs and other financial entities can use them. Regarding AI, there is no regulation in the Mexican financial system.

The Situation in Uruguay and Argentina

In Uruguay, the first Virtual Assets Law was passed in 2024. The regulation equates cryptoassets with securities, meaning they are now under the regulatory framework of the Central Bank of Uruguay (BCU).

In Argentina, before the Milei scandal, there was great anticipation regarding the regulation of digital assets, with a law expected to be approved this year. The South American country ranks second in the region in stablecoin adoption (cryptocurrencies pegged to a fiat currency, in this case, the U.S. dollar) and has a highly developed industry with major projects ahead. Amid a tense political climate, in the coming months, we will see how the discussion progresses in a country that had aspired to regional leadership in the field.

María Fernanda Magariños, Executive Director of Investment Management at Sura Investments

FlexFunds and Funds Society, through their Key Trends Watch initiative, share the vision of María Fernanda Magariños, the newly appointed Executive Director of Investment Management at Sura Investments, a company within Grupo SURA, an investment management firm with 80 years of experience and a presence in Mexico, Colombia, Peru, and Chile, in addition to investment vehicles in the United States and Luxembourg.

A qualified actuary, Magariños is strongly motivated to channel global resources toward Latin America’s sustainable development, bridging economic and social gaps through investment. In her new role, she is responsible for designing investment solutions for pension fund managers, insurance companies, and family offices.

In a challenging and volatile economic environment, her strategy focuses on building long-term, trust-based relationships and ensuring operational excellence—key aspects for institutional clients who must balance profitability and stability when managing third-party assets.

To achieve this, she considers three essential factors: a straightforward client-focused approach, strong talent management to enhance investment strategy execution, and the ability to operate within strict regulatory frameworks without losing flexibility—crucial in maintaining confidence in diverse Latin American markets.

Trends in portfolio and investment vehicle management

Magariños highlights the increasing inclusion of alternative assets in investment strategies. Alternative assets have become an essential diversification tool for institutional investors, who typically manage portfolios with a long-term investment horizon. Traditional assets in Latin American markets do not always offer the depth or returns needed to meet investors’ objectives.

She mentions infrastructure, private debt, and real estate, among the most popular alternative assets. These assets enable greater diversification and contribute to economic development and regional strengthening, adding extra value for investors. In this sense, alternative assets balance risk and return, which is key to meeting institutional clients’ investment profiles.

Another crucial aspect of asset management is the proper selection of investment vehicles. Magariños emphasizes that each client type requires tailored solutions. While insurers may benefit from direct or structured vehicles that optimize capital and reduce regulatory requirements, pension funds find more value in collective investment funds aligned with their operational structures.

The key is not to apply a one-size-fits-all solution but to design customized strategies that balance profitability and risk for efficient and sustainable investment management.

According to Magariños, success in asset management in Latin America depends on a long-term strategic vision centered on client needs and trust-based relationships. The key lies in portfolio diversification, incorporating alternative assets that provide greater stability and returns. Moreover, investment solutions must be flexible and adaptable, with a strong local presence that ensures compliance with regulations without compromising efficiency.

Thus, capital optimization, effective talent management, and the ability to adapt to a constantly changing environment will be fundamental in strengthening asset management in the region, where alternative assets will play a key role in ensuring the growth and sustainability of institutional portfolios.

Which assets will dominate the future?

Looking ahead, María Fernanda identifies a key financial instrument for investors in 2025: private debt. This instrument diversifies portfolios and offers attractive returns in an environment with a limited supply of traditional options. The growing interest in alternative assets also reinforces their role in risk management and returns optimization.

Separately managed accounts (SMA) vs. collective investment vehicles

According to Magariños, separately managed accounts and collective investment vehicles play a crucial role and must coexist in the market. This flexibility allows investment solutions to be tailored to specific investor needs. Sura Investments, for example, offers a wide range of investment solutions, from Latin American alternative assets to third-party funds investing in global assets, adapting to the demands of insurance companies, pension funds, and family offices alike.

When asked about the most important factors investors prioritize when making decisions, Magariños highlights two key elements: the quality of the manager and operational excellence.

Investors increasingly focus on manager profiles, seeking proven experience and a strong track record in investment strategies. In this regard, a firm’s performance is measured not only by returns but also by its ability to deliver efficient operations and timely reporting, which are essential to meeting institutional investors’ regulatory requirements and expectations.

In this context, Magariños underscores the key skills an advisor should have: active listening,effective communication, and a genuine interest in learning. At Sura Investments, these skills are highly valued, as providing expert advisory services to clients is central to their value proposition and a fundamental way to achieve clients’ financial goals.

However, Magariños adds that one must not overlook the advancement of artificial intelligence, which is becoming the new driving force in asset management. AI’s data analysis capabilities have enhanced the personalization of investment solutions and optimized decision-making, enabling the creation of products tailored to client needs making them more competitive and efficient.

The interview was conducted by Emilio Veiga Gil, Executive Vice President of FlexFunds, as part of the Key Trends Watch initiative by FlexFunds and Funds Society.

The recent challenges facing the private equity market could be overcome as rate cuts and lower inflation set the stage for an improvement in multiples. According to Rainer Ender, Global Head of Private Equity at Schroders Capital, although 2024 saw a significant slowdown in deal activity, signs of recovery are emerging, suggesting that the private equity market could be more dynamic in 2025.

“Just like in 2023, we have seen wide bid-ask spreads and reduced liquidity. When interest rates rise, so do the financing costs for acquisitions, which lowers the EV/EBITDA. Buyers pay more to secure fewer loans, reducing the amount they are willing and able to offer for assets,” says Ender.

In his view, rising interest rates have put downward pressure on cash flows, while inflation has increased costs for companies that lack proper pass-through mechanisms. Meanwhile, sellers have tried to exit assets when leverage was cheap and multiples were rising. Ender believes this dynamic has created a mismatch between the price buyers are willing to offer and the price sellers are willing to accept. Even amid these challenges, he sees several developments suggesting that 2025 may bring more favorable conditions.

“Although EV/EBITDA multiples for large acquisitions have declined, the global value of deals is increasing, a trend driven by the preference for larger investments in established companies. Exit prices in the global market have stabilized, and there has been a recent uptick in sponsor-to-sponsor exits (where one PE fund sells to another PE fund). However, a significant valuation gap persists, as small and mid-sized company acquisitions are trading at a steep discount compared to their larger counterparts, a trend that suggests a perceived value discrepancy in the market,” Ender points out.

Secondly, he believes that many of the factors putting downward pressure on multiples will dissipate, and the decline in interest rates and lower inflation should lay the foundation for an improvement in multiples. “We also believe that investors could benefit by following the money and considering GP-led secondary transactions. Nearly half of the record-high secondary transaction volume in the first half of the year came from these vehicles, also known as continuation funds. These funds align the financial incentives of GPs and LPs, creating potential benefits for all stakeholders: the original sponsor, new and existing investors, and the company or companies within the new fund structure,” he emphasizes.

Finally, Ender notes that conditions will also favor a focus on small and mid-cap markets, which are diversifying. “Recent history has demonstrated their potential to perform well in periods of volatility, and the law of large numbers (probability theory) makes it inherently easier to generate higher multiples in smaller companies. Operating in small and mid-cap markets also reduces dependence on the still-stagnant IPO market for exits. Moreover, after successfully helping a small or mid-sized company grow into a large-cap company, exits can be larger in the market, where a significant amount of dry powder—capital already raised and seeking opportunities—remains available. If we combine the recent period of volatility with the dot-com crash, the global financial crisis, the eurozone crisis, and the COVID-19 pandemic, we see that the Global Private Equity Index outperformed the MSCI ACWI Gross Index by an average of 8%,” argues the Schroders Capital expert.

Additionally, he highlights that, structurally, the nature of committed capital allows firms to retain ownership of assets during crises and sell them when market conditions are favorable, avoiding the kind of “fire sales” at low valuations. “The generally more rigid nature of private equity also prevents people from falling into psychological investment traps, such as panic selling at the worst possible moment. From a fundamentals perspective, private equity firms tend to have a different sector mix compared to public markets, focusing on less cyclical industries such as healthcare and technology while maintaining lower exposure to banks and heavy industry. Additionally, private equity tends to favor growth and disruption, seeking companies with high expansion potential. They also prefer business models with recurring cash-generating revenues, as these tend to be less volatile,” he concludes.

Exchange-traded products (ETPs) have become an essential tool for portfolio managers, as highlighted by FlexFunds, offering flexibility, accessibility, and cost efficiency for asset repackaging and management. These financial instruments enable asset managers to efficiently diversify their portfolios, implement tailored investment strategies, and seamlessly adapt to changing market conditions.

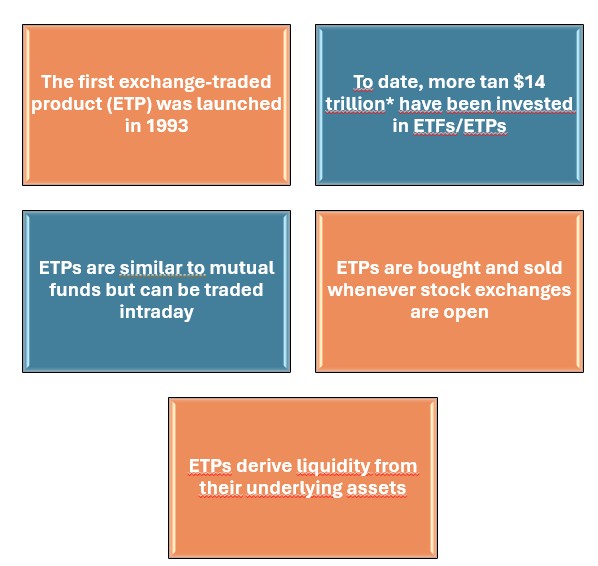

What Is an ETP?

An ETP is a financial instrument traded on a stock exchange, similar to equities. It provides access to a benchmark index or a specific asset class, making it easier for managers to construct diversified portfolios with a single transaction. Most ETPs are passive investments designed to track the performance of an underlying index or asset, generally with lower operating costs than actively managed investment funds or mutual funds.

Characteristics of ETPs

Passive management: A cost-efficient and transparent option for gaining exposure to an index or asset without the need for constant active management.

Simplified diversification: Enables managers to access a broad range of assets through single trade.

Liquidity and ease of trading: Can be bought and sold during market hours, with real-time pricing.

Flexibility for managers: Can issue shares or debt securities based on demand, adapting to portfolio needs.

Transparency: ETP components are published daily, providing managers with a clear view of portfolio holdings.

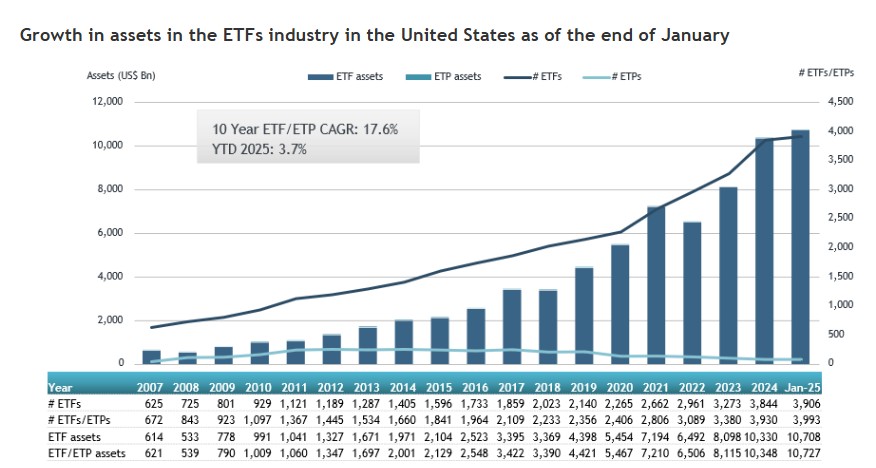

The growing ETP market

The ETP industry has experienced significant growth since the launch of the first product in 1993. According to independent research and consulting firm ETFGI, as of January 2025, over $14 trillion was invested globally in ETFs/ETPs. In the United States, the market reached a record $10.73 trillion in January 2025, surpassing the previous peak of $10.59 trillion recorded in November 2024. These figures reflect the growing interest in and adoption of ETPs as a key portfolio management vehicle, as illustrated in the following chart:

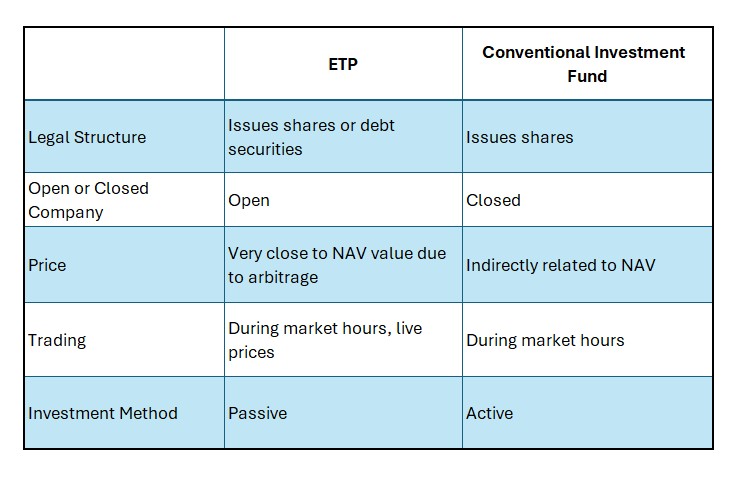

ETPs vs. traditional investment funds

Today, portfolio managers have a wide range of investment vehicles to optimize their strategies. This article focuses on comparing ETPs with traditional investment funds, highlighting their key differences in the table below.

FlexFunds: A global leader in ETP solutions

FlexFunds is an internationally recognized service provider for the issuance and administration of ETPs covering listed assets and alternative investments. These solutions are tailored for investment advisors, hedge fund managers, private fund managers, and real estate fund managers.

FlexFunds’ ETPs stand out for their efficiency and versatility, allowing asset managers to design customized strategies and create exchange-listed products with a unique ISIN code listed on the Vienna Stock Exchange and Bloomberg. Among their key advantages:

Efficient subscription via Euroclear

Flexible portfolio composition: Enables the securitization of multiple asset classes, both liquid and alternative.

Cost-efficient structure: Enhances portfolio profitability and optimizes operational expenses.

Global access: Products can be acquired from any brokerage account worldwide, facilitating international distribution.

Integrated administration: Supported by renowned institutions such as Interactive Brokers and Bank of New York, ensuring security and trust.

Direct reporting and transparency: Pricing is calculated and displayed directly on Bloomberg, Six Financial, and investors’ accounts.

With FlexFunds’ investment vehicles, asset managers can access solutions that securitize multiple asset classes, both liquid and alternative. To learn how these solutions can enhance your investment strategy, feel free to contact one of our experts at info@flexfunds.com.

Private credit was one of the most in-demand assets among private market investors in 2024. Not only did it gain popularity, but European market operations rebounded over the past twelve months, reinforcing its appeal. According to experts at Pictet AM, this trend is expected to continue in 2025.

“It is important to note that this is a growth asset class, starting from an approximate value of €400 billion, which is only a third of the size of this market in the U.S. It is also expanding into small and medium-sized enterprises, which are increasingly turning to direct loans, as traditional bank financing is difficult to obtain,” explain Andreas Klein, Head of Private Debt, and Conrad Manet, Client Portfolio Manager, both from Pictet AM, in their latest analysis.

They argue that smaller transactions, especially those aimed at growth or transformational capital—where direct loans are the primary alternative to banks—are largely shielded from competitive dynamics. This contrasts with the larger-volume end of the market, where renewed competition from syndicated and high-yield loans generates excess capital, lower interest rates, and weaker protective clauses.

“In fact, yield-to-maturity spreads in European direct loan operations have declined by nearly 1% since early 2023 in the core and upper-middle segments, falling below 6% for the first time. Some loans have even been issued at 4.5% and 5%, often without creditor covenants. This has coincided with historically high levels of investment capacity, to the point that private equity and private debt funds now hold a record $2 trillion available for investment. A weak mergers and acquisitions market has contributed to this, creating a scarcity of opportunities. As a result, loan transaction margins have shrunk, with a relaxation of protective clauses,” the experts highlight.

However, they clarify that the reduction in margins in the lower-middle market—defined as transactions with companies generating up to €15 million in operating profit—has been more modest, around 0.2%. This is because there are fewer private debt funds competing in this segment, and banks have a limited presence due to capital constraints, particularly regarding credit lines. “In this lower-middle segment, yield spreads remain stable, and risk parameters are more controlled, leading to an improved risk-adjusted return premium compared to the more traditional, higher-volume segment. Specifically, leverage is decreasing in the lower-middle market, with more transactions closing at less than four times debt/EBITDA. Additionally, strong protective clauses for investors prevail in this segment,” Pictet AM analysts emphasize.

Another factor investors value in direct loans is their relatively low default rate. According to the experts, default rates have risen to around 6% in syndicated loans but remain below 2% on average in direct loans. However, they caution that default rates could rise due to lingering inflationary pressures and a potentially slower pace of interest rate cuts by European central banks compared to previous cycles. This could create tensions, particularly in more cyclical and leveraged segments, such as high-yield and leveraged loans.

“However, in 2025, we expect the lower-middle segment of direct loans to benefit from improving economic conditions and a rebound in M&A activity. That said, Europe’s economic recovery may not be uniform, and volatility is possible. Therefore, we are focusing on less market-sensitive and less volatile sectors such as medical technology, software, and business services. These sectors provide diversification, more stable income, and better capital preservation. On the other hand, we are avoiding more cyclical segments within the industrial and consumer sectors. Additionally, while most of the market continues to issue loans with light protective clauses, we hold single-lender positions, allowing us to structure customized agreements that better protect capital,” add the experts at Pictet AM.

They acknowledge that smaller companies can be riskier but emphasize their focus on businesses operating in and dominating niche markets with high entry barriers and limited competition. “Often, these companies exhibit the defensive qualities of major industry leaders—sometimes even better. Moreover, private equity funds tend to overweight loans to private equity-owned businesses, where transaction volume is higher, though potentially offering less value. However, maintaining a significant proportion of loans to company founders can be a strength if the right network is in place. That’s why our portfolio balances loans to private equity-owned companies with direct loans to founders, providing an additional layer of diversification,” they note.

Overall, Pictet AM expects that in 2025, the lower-middle segment of direct loans will remain a superior and more stable source of income and capital preservation. It can complement more traditional allocations to the upper-middle segment, special situation debt, and private equity debt. “It can serve as a strategic component in any private credit portfolio, both for investors taking their first steps into this asset class and for more sophisticated investors looking to diversify their portfolios,” the experts conclude.

In recent years, Spain has solidified its position as a highly attractive destination for wealthy Latin Americans. A growing number of high-net-worth Latin American families are settling in the country, driven primarily by significant political changes in their home countries. They seek, among other things, both physical and economic security for their assets in Spain.

Madrid, in particular, has recently experienced such a significant influx of investment from Latin America that it has come to be known as the “new Miami.” The numbers speak for themselves. For instance, 17% of residents in the affluent Barrio de Salamanca are wealthy Latin Americans, and nearly 15,000 Latin American students attended Madrid universities during the 2022-23 academic year.

Why Is Spain So Attractive to High-Net-Worth Latin Americans?

Spain offers significant opportunities with a business-friendly environment and strong cultural and linguistic ties to Latin America. Additionally, it is an appealing country from a family perspective, thanks to its top-tier public and private universities, pleasant climate and lifestyle, high-quality healthcare, relatively low crime rates, easy access to the rest of Europe, and good connections to Latin American countries.

For all these reasons, Spain is an obvious choice for Latin Americans looking to emigrate. But what has truly triggered the current high levels of wealth migration?

Many high-net-worth Latin American families began considering investment and/or relocation to Spain following the rise of left-wing governments across the continent, which generally created a less favorable fiscal and regulatory climate for the wealthy. Other recent events, such as Mexico’s 2024 judicial reform or the redefinition of private property in Mexico City’s constitution, have also spurred these movements.

Spain’s luxury real estate market has been another key factor drawing the attention of affluent Latin Americans, as these properties offer better value per square meter compared to what they might find elsewhere in Europe or much of the United States.

Recognizing the economic opportunity this trend presents, certain administrations have taken specific measures to foster and accelerate these wealth flows. For example, Isabel Díaz Ayuso, President of the Community of Madrid, announced last year that tuition fees at public universities for Latin American students would be reduced to match those paid by Spanish and European students starting in the 2024-25 academic year.

More importantly for this segment of the population, the recent approval of the so-called “Mbappé Law” in Madrid, which took effect on January 1, 2025, introduces a 20% regional deduction on personal income tax for non-residents who establish tax residency in Madrid and make certain investments as stipulated by the law.

Finally, it is important to note that many will still be able to benefit from the well-known “Beckham Law,” allowing them to be taxed as non-residents during their first years of residence in Spain, offering clear tax advantages. However, eligibility will depend entirely on the professional activities they undertake while in the country.

Will Recent Changes Affect Latin American Wealth Migration?

However, it is not all smooth sailing. It is undeniable that housing prices have risen significantly as more high-net-worth families have moved to or invested in Spain, particularly in major cities. While this reflects the strong interest in the country among foreign buyers, it has also priced many local residents out of the market, generating growing discontent over measures aimed at attracting international investment.

To ease tensions surrounding the impact of wealthy foreigners on Spain’s real estate market, the Socialist government voted in 2024 to eliminate the Golden Visa, which allowed individuals to obtain permanent residency through the purchase of properties valued at €500,000 or more.

Golden Visa applications will only be accepted until April 3, 2025, prompting some foreign investors to rush their purchasing decisions. However, other pathways for non-EU nationals to obtain residency in Spain, such as the non-lucrative residence visa, will remain available.

Additionally, and more controversially, Prime Minister Pedro Sánchez has recently introduced several proposals, including the potential implementation of a 100% tax on property purchases by non-EU residents. The aim is to curb foreign real estate investment and make housing more accessible to Spanish residents.

However, there is significant uncertainty regarding whether these measures will gain the necessary support from key government allies to move forward, which is crucial in a highly fragmented political coalition.

Moreover, it remains to be seen whether such measures (if ultimately approved) could be considered discriminatory and in violation of EU law by relevant authorities, including the European Commission or the Court of Justice of the European Union. This is particularly relevant given recent case law on inheritance and gift taxes and the rental of properties by non-EU residents.

Madrid Will Likely Cement Its Status as the “New Miami”

Ultimately, despite recent developments, Spain and its capital are well-positioned to continue attracting high-net-worth Latin American families.

The strong historical, cultural, and linguistic ties make Spain a natural destination for these individuals to establish their new home. And while there may be some political instability surrounding this issue at present, Latin American wealth migration is almost certain to continue in the coming years.

Opinion piece by Nerea Llona, Tax & Legal Counsel for Spain and Latin America at Utmost Wealth Solutions.

Catastrophe bonds, whose returns have consistently outperformed high-yield debt markets in recent years, are about to become accessible to a broader segment of investors.

Next month, the Brookmont Catastrophic Bond ETF, based on a portfolio of up to 75 of the 250 so-called “catastrophe bonds” in circulation, could begin trading on the New York Stock Exchange (NYSE)—a global first.

“It’s an asset with a lot of nuances, and our goal is to demystify it,” said Rick Pagnani, co-founder and CEO of King Ridge Capital Advisors Inc, which will manage the ETF, in an interview cited by Bloomberg. The fund will be overseen by Brookmont Capital Management LLC, based in Texas.

Pagnani, who until last year led Pimco’s insurance-linked securities division, stated that “it is difficult to create a diversified catastrophe bond portfolio for a typical individual investor.” By packaging catastrophe bonds into an ETF, “we aim to lower some of the barriers to entry,” he said.

The market, dominated by U.S. issuances, is currently valued at approximately $50 billion, according to Bloomberg.

According to Pagnani, the pipeline of projects remains “strong and growing,” which could help push the market to $80 billion by the end of the decade.

Brookmont and King Ridge are still finalizing the lineup of partners involved in launching the ETF. They aim to raise between $10 million and $25 million in initial capital. The ETF is registered with the SEC.

The fund will cover risks ranging from Florida hurricanes and California earthquakes to Japanese typhoons and European storms, according to the prospectus filed with the U.S. market regulator.

As outlined in the prospectus, it is an actively managed ETF that, under normal circumstances, will invest at least 80% of its net assets in catastrophe bonds. It will not have restrictions on specific issuances, risks, or geographic exposure. However, the document notes that at times, the fund may have a relatively higher exposure to U.S.-related risks.

Additionally, it may occasionally have a greater concentration in Florida hurricane-related catastrophe bonds than in other regions or risks due to the higher availability of such investments relative to the global market.