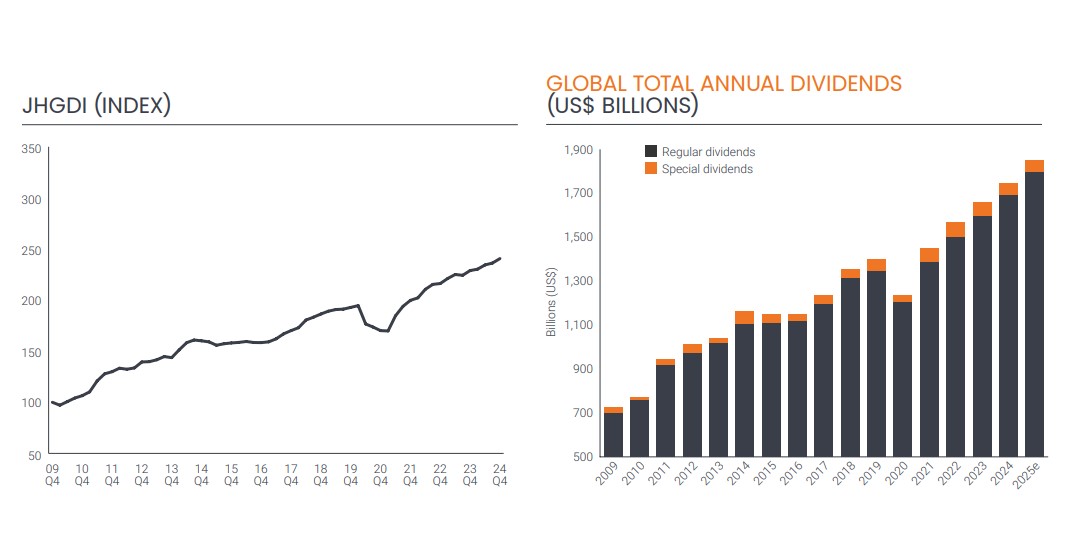

Global dividend payouts reached a record $1.75 trillion in 2024, representing underlying growth of 6.6%, according to the latest Janus Henderson Global Dividend Index. The asset manager explains that, at a general rate, growth was 5.2%, driven by lower special dividends and the strength of the dollar.

The year’s results slightly exceeded Janus Henderson’s forecast of $1.73 trillion, mainly due to a better-than-expected fourth quarter in the U.S. and Japan. In Q4, dividend payouts increased by 7.3% on an underlying basis.

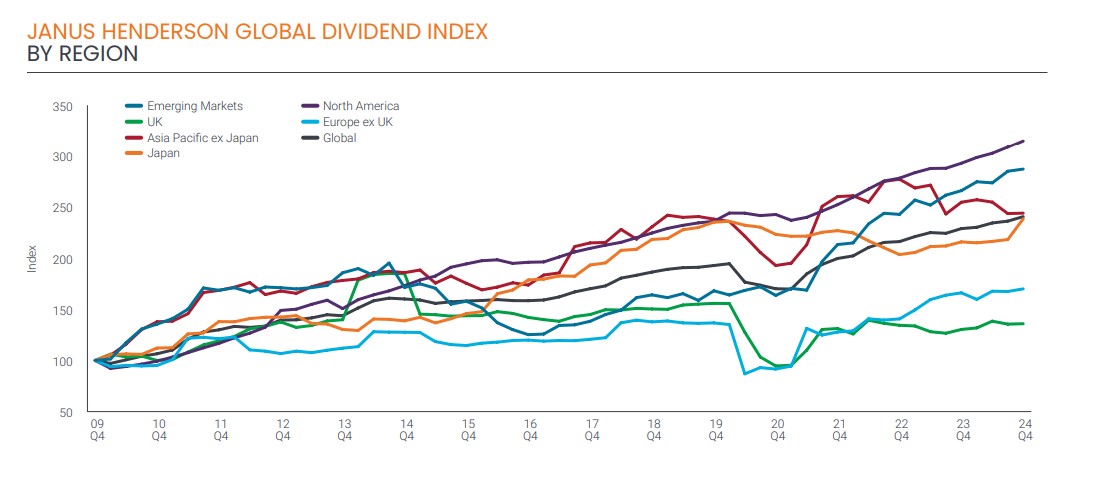

According to their assessment, overall growth was strong across Europe, the U.S., and Japan throughout the year. Some key emerging markets, such as India, and Asian markets like Singapore and South Korea, also recorded decent growth. In 17 of the 49 countries included in the index, dividend payouts hit record levels, including some of the largest distributing nations like the U.S., Canada, France, Japan, and China.

When analyzing the source of this growth, the Janus Henderson report highlights that several major companies distributing dividends for the first time had a disproportionate impact.

“The largest payouts came from Meta and Alphabet in the U.S. and Alibaba in China. Together, these three companies distributed $15.1 billion, representing 1.3% of total dividends or one-fifth of global dividend growth in 2024,” the report states.

Another key finding is that 88% of companies either increased or maintained their payouts globally, while the median dividend growth—or typical growth rate—stood at 6.7%.

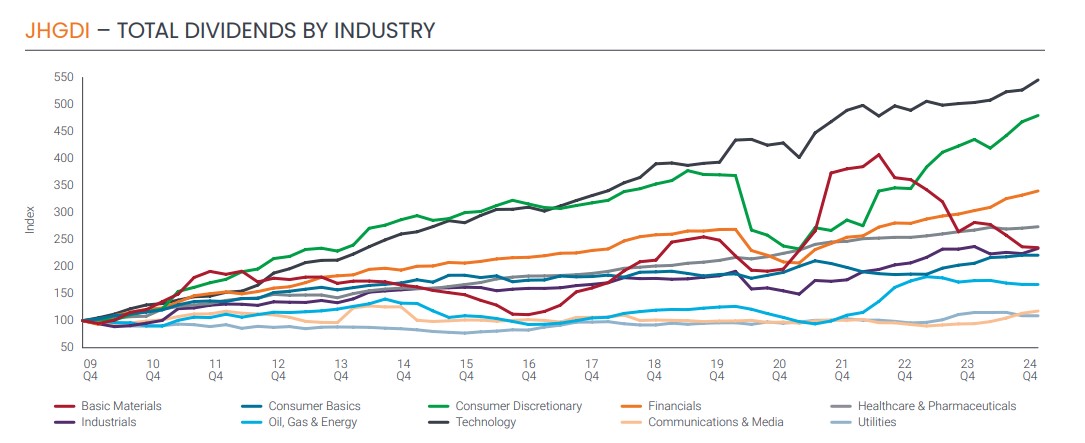

By sector, nearly half of the dividend increase in 2024 came from the financial sector, primarily banks, which saw underlying dividend growth of 12.5%.

According to Janus Henderson, dividend growth in the media sector was also strong, doubling on an underlying basis, largely due to payouts from Meta and Alphabet. However, the increase was broad-based, with double-digit growth in telecommunications, construction, insurance, durable consumer goods, and leisure.

In contrast, mining and transportation were the worst-performing sectors, paying a combined $26 billion less than in 2023.

The report also highlights that, for the second consecutive year, Microsoft was by far the world’s largest dividend payer. Meanwhile, Exxon, which expanded its portfolio with the acquisition of Pioneer Resources, climbed to second place—a position it hadn’t held since 2016.

For the year ahead, Janus Henderson expects dividends to grow by 5% on a general basis, pushing total payouts to a record $1.83 trillion. Underlying growth is projected to be closer to 5.1% for the full year, as the strong U.S. dollar against multiple currencies is expected to slow overall growth.

Janus Henderson’s Assessment of the Index Data

Commenting on these figures, Jane Shoemake, portfolio manager at the Global Equity Income team of Janus Henderson, highlights that several of the world’s most valuable companies—particularly those rooted in the U.S. tech sector—are now starting to distribute dividends. This contradicts previous assumptions that these firms would avoid returning capital to shareholders through dividends.

“In doing so, they are following the path of other successful companies before them. As they mature, they start generating cash surpluses that can be returned to investors. These companies are currently providing a significant boost to global dividend growth,” says Shoemake.

2025: An Uncertain Year for the Global Economy

Overall, Shoemake sees 2025 as a potentially uncertain year for the global economy.

“The world economy is expected to continue growing at a reasonable pace, but the risk of tariffs and potential trade wars, along with high public debt levels in many major economies, could lead to greater market volatility in 2025. In fact, fixed-income yields in some markets have risen to levels not seen in years,” she explains.

She also points out that higher interest rates impact investment, slow long-term earnings growth, and increase financing costs, all of which affect corporate profitability.

“That said, the market still expects corporate earnings to increase this year, with consensus forecasts projecting growth above 10%. While this may seem overly optimistic given the current economic and geopolitical challenges, the good news for income-focused investors is that dividends tend to be more resilient than profits throughout the economic cycle.

Companies decide how much to distribute to shareholders, meaning dividend income streams are far less volatile than corporate earnings. For this reason, we expect dividends to reach a new record this year,” concludes Shoemake.

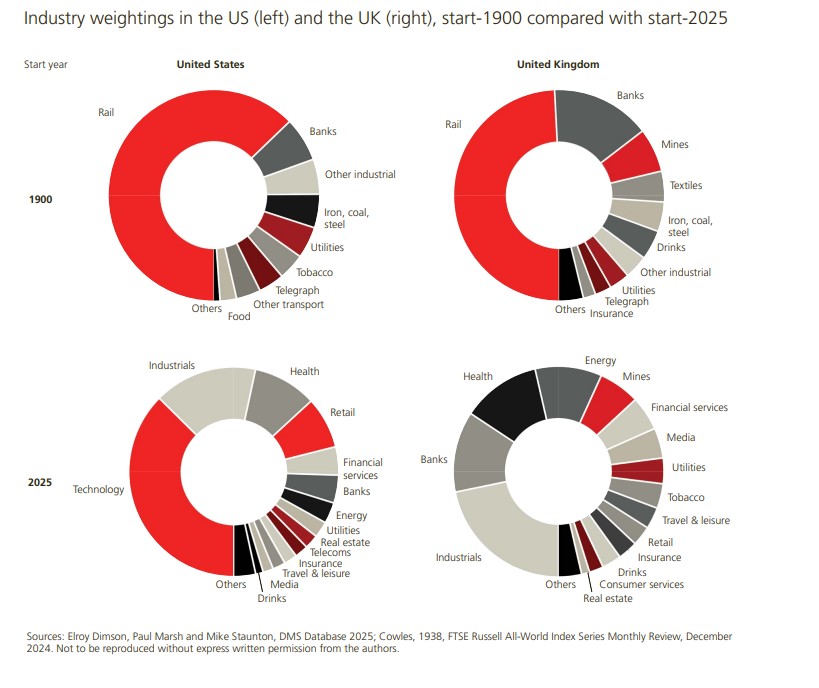

Financial markets and the industrial landscape have changed enormously since 1900, and these changes can be observed in the evolution of the composition of publicly traded companies in global markets. As depicted by UBS Global Investment in its report Global Investment Returns Yearbook, at the beginning of the 20th century, markets were dominated by railroads, which accounted for 63% of the stock market value in the U.S. and nearly 50% in the U.K.

In fact, nearly 80% of the total value of U.S. publicly traded companies in 1900 came from sectors that are now small or have even disappeared. This percentage stands at 65% in the case of the U.K. Additionally, a large proportion of companies currently listed on the stock market come from sectors that were either small or nonexistent in 1900, now representing 63% of market value in the U.S. and 44% in the U.K. “Some of the largest industries in 2025, such as energy (excluding coal), technology, and healthcare (including pharmaceuticals and biotechnology), were practically absent in 1900. Likewise, the telecommunications and media sectors, at least as we know them today, are also relatively new industries,” the report notes in its conclusions.

Among the key findings of this report, which analyzes historical data from the past 125 years, one standout conclusion is that long-term equity returns have been remarkable. According to the document, equities have outperformed bonds, Treasury bills, and inflation in all countries. An initial investment of 1 dollar in U.S. stocks in 1900 had grown to 107,409 dollars in nominal terms by the end of 2024.

Concentration, Synchronization, and Inflation: Three Clear Warnings

Throughout this historical evolution, the report’s authors have identified concentration as a growing concern. “Although the global equity market was relatively balanced in 1900, the United States now accounts for 64% of global market capitalization, largely due to the superior performance of major technology stocks. The concentration of the U.S. market is at its highest level in the past 92 years,” they warn.

In contrast, diversification has clearly helped manage this concentration and, more importantly, volatility. According to the report’s conclusions, while globalization has increased the degree of market synchronization, the potential benefits of international diversification in reducing risks remain significant. For investors in developed markets, emerging markets continue to offer better diversification prospects than other developed markets.

Finally, the conclusions emphasize that inflation is a key factor to consider in long-term returns. In this regard, the authors’ analysis shows that asset returns have been lower during periods of rising interest rates and higher during cycles of monetary easing. “Similarly, real returns have also been lower during periods of high inflation and higher during periods of low inflation. Gold and commodities stand out among the few effective hedges against inflation. Since 1972, gold price fluctuations have shown a positive correlation of 0.34 with inflation,” the report states.

Key Insights from the Report’s Authors

Following the release of this report, Dan Dowd, Head of Global Research at UBS Investment Bank, commented: “I am pleased to once again collaborate with professors Dimson, Marsh, and Staunton, as well as our colleagues from Global Wealth Management, in presenting the 2025 edition of the Global Investment Returns Yearbook. The 2025 edition marks an important milestone. With 125 years of data, it provides our clients across the firm with a valuable framework for addressing contemporary challenges through the lens of financial history.”

Meanwhile, Mark Haefele, Chief Investment Officer of UBS Global Wealth Management, highlights that the Global Investment Returns Yearbook can help us understand the long-term impacts of following principles such as diversification, asset allocation, and the relationship between return and risk. “Once again, it teaches us that having a long-term perspective is crucial and that we should not underestimate the value of a disciplined investment approach,” Haefele states.

Finally, Professor Paul Marsh of the London Business School notes that “equity returns in the 21st century have been lower than in the 20th century, while fixed income returns have been higher. However, equities continue to outperform inflation, fixed income, and cash. The global stock market has delivered an annualized real return of 3.5% and a 4.3% premium over cash. The ‘law’ of risk and return remains valid in the 21st century.”

In an environment where accurate and accessible information is key to decision-making, FlexFunds continues to strengthen its service offerings for asset managers through platforms recognized at the institutional level. Now, Morningstar joins a group of top-tier providers, further enhancing the visibility and reach of investment vehicles (ETPs) under FlexFunds’ securitization program, the firm announced in a statement.

Starting in March 2025, qualitative and quantitative data on ETPs will be available on Morningstar Direct, an essential tool for institutional investors, as well as on Morningstar’s public website. This integration increases the exposure of investment vehicles, strengthens transparency, and provides access to advanced analytics on one of the most trusted platforms in the industry.

The combination of pricing providers offered by the FlexFunds program, including Morningstar, Bloomberg, LSEG Refinitiv, and SIX Financial, provides a comprehensive market view and helps asset managers build a public track record, enabling informed and strategic decision-making.

DWS has expanded its Xtrackers product range, enabling investment in a broadly diversified selection of bonds with similar maturities, by adjusting the investment objectives and names of two existing fixed-income ETFs. The new Xtrackers II Rolling Target Maturity Sept 2027 EUR High Yield UCITS ETF invests for the first time in high-yield corporate bonds with a specific maturity.

According to the asset manager, since the bonds remain in the ETF portfolio until maturity, price fluctuations are reduced for investors who stay invested until September 2027. To achieve this, the ETF now tracks the iBoxx EUR Liquid High Yield 2027 3-Year Rolling Index. This index includes around 80 liquid high-yield corporate bonds denominated in euros, with credit ratings below Investment Grade, according to major rating agencies. As a result, investors bear a higher credit and default risk compared to investing in Investment Grade bonds. In return, according to the firm, “there is an opportunity to achieve a significantly higher aggregate yield at maturity, estimated at around 5.3% as of February 17, 2025, for the ETF’s portfolio.”

They also state that all bonds in the index have an initial maturity date between October 1, 2026, and September 30, 2027. Additionally, to provide greater flexibility, the ETF’s target maturity will be “extended” in the future. This means that the ETF will not be liquidated at the end of its term in September 2027, and the fund’s assets will be paid out to shareholders. Instead, the assets will be reinvested in bonds with a maturity of approximately three years.

“By expanding our current range of target maturity ETFs with an innovative product in the high-yield bond segment, we aim to offer investors the opportunity to generate attractive mid-term returns in the current environment of declining interest rates,” says Simon Klein, Global Head of Sales for Xtrackers at DWS.

The asset manager also highlights that they offer the Xtrackers II Target Maturity Sept 2029 Italy and Spain Government Bond UCITS ETF. In this case, the underlying index has also been modified for this ETF. “It now provides access to Italian and Spanish government bonds maturing between October 2028 and September 2029. Like all Xtrackers target maturity ETFs, these new products combine the advantages of fixed-income securities—predictable redemption at maturity—with the benefits of ETFs, such as broad diversification, liquidity, and ease of trading,” they state.

The 21st century is nearing its first quarter, and Global X has already drawn key lessons from this period: the U.S. economy and markets tend to be resilient.

The firm highlights several examples—the dot-com bubble, the global financial crisis, and COVID-19—all of which occurred since the turn of the century, yet the S&P 500 has quadrupled in value. “We keep this lesson in mind as we enter 2025 with a mix of optimism and uncertainty,” says Global X, noting that investor confidence and consumer expectations are improving, even as questions persist about economic policy and GDP growth is expected to slow.

Just like last year, Global X believes economic growth may once again surprise to the upside, supporting further market gains. However, the key drivers of growth this time will likely be different. “Some market participants argue that broad equity valuations look stretched, but in our view, fund flows suggest that investors remain willing to embrace risk assets,” they state. They add that broader market participation, improving profit margins, and continued earnings growth “could further lift equity valuations.” Conversely, they see fixed income as potentially “stuck in limbo due to interest rate volatility, which may force investors to be more creative and seek differentiated strategies.”

The strength of the services sector and corporate investment from large tech firms helped drive stronger-than-expected economic growth in 2024. However, Global X warns that economic uncertainty is likely to remain high, given the trade-offs and net effects of lower taxes, higher tariffs, reduced immigration, increased stimulus, and lighter regulation. That said, a manufacturing sector recovery, combined with renewed investment in small and mid-cap companies, could extend the mid-cycle expansion, leading to broader market participation and higher valuation multiples.

As a result, Global X will focus in 2025 on growth themes tied to U.S. competitiveness that still appear reasonably priced.

Building Portfolio Resilience in 2025

Equities and risk assets may be poised for another strong year, according to Global X. However, “the unique set of economic and political circumstances will likely warrant a more targeted approach in 2025.” A portfolio strategy aligned with key themes related to U.S. competitiveness “can provide reasonable upside and a degree of insulation from potential volatility.” The firm’s top investment themes include:

1. Infrastructure Development

A core part of the U.S. competitiveness narrative is the ongoing infrastructure renaissance. Construction, equipment, and materials companies have benefited from infrastructure-related policies and are positioned to gain from approximately $700 billion in additional spending over the coming years. Despite strong performance in recent years, these companies still trade at valuation multiples below the S&P 500. Moreover, traditionally rigid industries are adopting new technologies and practices, which could help expand profit margins.

2. Defense and Global Security

A series of interconnected global conflicts is creating new challenges for the U.S. and its allies. These evolving threats are expected to be persistent and unconventional, driving demand for new tactics, techniques, and technologies. Global defense spending, which reached $2.24 trillion in 2022, is projected to grow 5% in 2025, while defense company revenues are expected to rise nearly 10%, with profit margins improving from 5.2% to 7.6%. Compared to traditional defense platforms—such as battleships and fighter jets—lower-cost solutions like AI-driven defense systems and drones are expected to boost profitability, alongside greater automation in production processes.

3. Energy Independence and Nuclear Power

Even before AI-driven growth, energy demand was expected to rise sharply—and those forecasts have only increased. Fossil fuels will remain an essential part of the energy mix, but cost-effective and environmentally friendly alternatives will be critical to meeting surging demand. The tech sector has turned its attention to nuclear power, with many major companies announcing plans to utilize existing facilities or build small modular reactors (SMRs). Beyond the U.S., Japan, Germany, and Australia are expected to expand nuclear capacity, driving strong demand for uranium.

Selective Income Strategies for 2025

Income-focused investors may need to adopt a more selective approach in 2025, according to Global X, “given political uncertainty and potential interest rate volatility.” Many fixed-income instruments may underperform in a volatile rate environment, particularly long-duration assets. To minimize interest rate risk, Global X suggests equity-based strategies that could provide income with less sensitivity to rate fluctuations:

1. Covered Options Strategies

Equity-based covered options strategies can generate stable income while limiting direct exposure to interest rate movements. While the underlying asset may still fluctuate with the overall market (and indirectly with rate volatility), these strategies are not directly impacted by interest rate risk like traditional fixed income. Additionally, when rate volatility increases equity market volatility, option premiums tend to rise, maximizing income potential.

2. Energy Infrastructure Investments

Master Limited Partnerships (MLPs)—which own energy infrastructure assets such as pipelines—can generate steady incomewithout direct exposure to interest rate movements. These assets typically pay consistent dividends and have long-term supply contracts that stabilize cash flows. While their values can fluctuate with oil prices, their correlation to commodities is generally modest, as they do not extract or own the raw materials—they simply transport them. Additionally, real assets like commodities and energy infrastructure are often viewed as inflation hedges.

3. Preferred Stocks

Preferred stocks sit above common equity but below fixed income in the capital structure. They trade at par value and pay fixed or floating dividends. While investors are not guaranteed payments, preferred shareholders receive dividends before common stockholders. Since they are issued at par with a predetermined payout structure, they can be sensitive to interest rates. However, because they carry more risk than bonds, they tend to offer higher yields.

Most preferred shares are issued by banks, which generate steady cash flows from net interest income. With potential financial sector deregulation and increased small-business lending, preferred stocks could become an attractive income option in 2025.

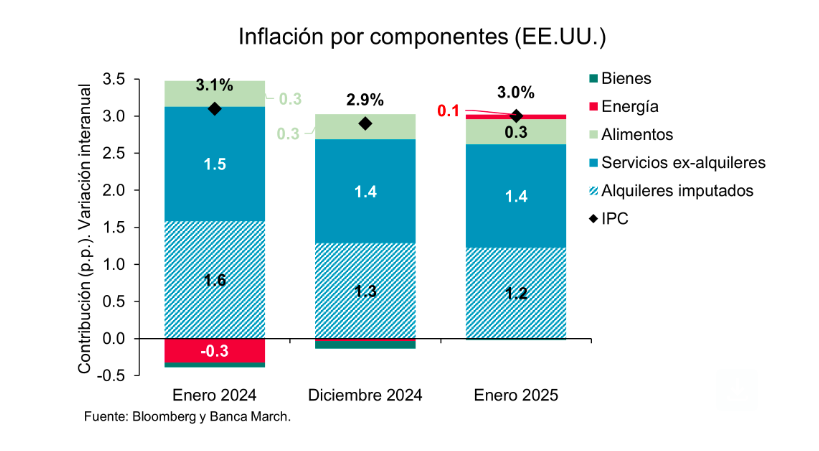

The latest report on the U.S. Consumer Price Index (CPI) showed that core inflation rose 0.4% month-over-month, surpassing consensus expectations. This pushed annual inflation to 3% in January 2025, up from 2.9% in December 2024. Additionally, the report detailed price spikes in categories that typically increase at the start of the year, including auto insurance, internet/TV subscriptions, and prescription drugs.

According to analysts at Banca March, the data presented a mixed picture: “The increase was mainly due to energy prices contributing to inflation (+0.06%) for the first time since last July, as well as a weaker downward drag from goods prices, which fell -0.13% year-over-year in January, marking their smallest decline since December 2023.”

They note that this shift in goods prices was driven largely by two components—used cars and prescription drugs—which together contributed +0.3% to January’s inflation, whereas in December, they had subtracted three-tenths from the CPI.

On a more positive note, service prices continued their gradual moderation trend, though not enough to prevent the inflation uptick. Service inflation rose at a 4.3% annual rate—one-tenth lower than in December—marking the slowest increase in service prices since January 2022. “Notably, the largest component, imputed rents, moderated to +4.4% year-over-year, down from +6% a year ago, supporting the gradual ‘normalization’ of inflation. However, upward pressure came from transportation services such as insurance and vehicle maintenance,” explain Banca March experts.

What Does This Mean?

According to Tiffany Wilding, U.S. economist at PIMCO, these figures do not change the broader narrative that the U.S. economy remained strong at the turn of the year while inflation progress stalled. “If anything, this reinforces the Federal Reserve’s (Fed) stance of keeping rates steady for some time. We believe inflation is likely to remain uncomfortably high through 2025 (with core CPI at 3%), despite growing risks of a more pronounced slowdown in the labor market and real GDP growth, stemming from Trump’s recent immigration policy announcements and broader political uncertainty,” explains Wilding.

She adds that Trump’s policies put the Fed in a difficult position: “Sticky inflation raises questions about whether the Fed will ultimately deliver the two 25-basis-point rate cuts implied in its December Summary of Economic Projections (SEP). At the same time, a more significant slowdown in real GDP growth and labor markets—both of which have been buoyed by strong immigration trends—could increase downside risks to the economy,” she says.

Uncertainty for Central Banks

Experts agree that this situation puts the spotlight on the Fed and other monetary institutions. “Central banks are no longer a source of stability, as they are caught between the need to control inflation and the desire to avoid an economic slowdown that may be necessary to bring inflation sustainably back in line with targets. This dilemma could worsen if the U.S. tariff threat materializes, as governments may have no choice but to loosen fiscal policies. Monetary policy decisions could take investors by surprise, as central banks may take very different paths,” note Marco Giordano, Chief Investment Officer at Wellington Management, and Martin Harvey, fixed income portfolio manager at Wellington Management.

Trump and Inflation

Benjamin Melman, Global CIO at Edmond de Rothschild AM, warns that global inflation no longer seems to be retreating, especially in the U.S. services sector, while rising oil, gas, commodity, and agricultural prices have added further inflationary pressures in recent months. In this context, he argues that Trump’s administration has introduced an additional layer of uncertainty regarding future inflation trends with its tariff and deportation policies.

“While it may be tempting to downplay these concerns by suggesting that tariffs are merely a negotiation tool to extract concessions from affected countries, and that large-scale deportations are technically difficult to implement, it would be a mistake to draw conclusions just one week into Trump’s second term,” Melman points out.

However, he clarifies that even if Trump does not fully implement these inflationary measures, or does so on a limited scale, the unleashing of so-called ‘animal spirits’ in the U.S.—driven by expectations of deregulation and tax cuts—cannot be ruled out. “This is likely to stimulate the economy and inflation through more traditional channels, particularly given that the output gap is already positive,” he concludes.

The Trump administration is once again boosting the crypto market with a new initiative. Over the weekend, the U.S. president announced the creation of a “Strategic Cryptocurrency Reserve,” which will include digital assets such as Bitcoin, Ethereum, Ripple, Solana, and Cardano. These new steps align with Donald Trump’s goal of making the U.S. the “crypto capital of the world.”

As a result of this announcement, the price of some cryptocurrencies surged: Bitcoin reached $93,000, while Ripple and Cardano saw significant gains, and Ethereum rose by 11%.

Without a doubt, the initiative announced by Trump has revitalized the entire industry, as crypto market sentiment had hit rock bottom. “The Crypto Fear and Greed Index had dropped from 55 (neutral) to 21 (extreme fear) in less than a week. Last Friday’s Bybit hack shook investor confidence, compounded by growing uncertainty over tariffs on Mexico and Canada, which will indeed take effect, adding to market anxiety,” acknowledged Simon Peters, an analyst at eToro, just three days ago.

This negative sentiment was also evident in Bitcoin’s price, which was holding at the $92,000 support level. The cryptocurrency has fallen 20% from its all-time high of $109,300. According to experts, a 35% correction could bring it down to around $70,000.

The SEC Clearly Shifts Its Stance on Cryptocurrencies

Crypto industry experts highlight that these initiatives reflect a shift in Trump‘s stance on cryptocurrencies, from initial skepticism in 2019 to active support today, with the declared goal of making the U.S. the “crypto capital of the world.” A clear example of this shift is that Trump is set to host the first Cryptocurrency Summit at the White House next Friday—the first such event organized by a U.S. president.

Another example of this change in approach involves Coinbase. Last week, the SEC announced that it had agreed to dismiss its enforcement case against the company. “If incoming SEC Chairman Paul Atkins approves the decision, the dismissal will mark the end of the ‘regulation by enforcement’ approach led by former SEC Chairman Gary Gensler,” explains Frank Dowing, Director of Analysis for Next Generation Internet at ARK.

According to Dowing, during Gensler’s tenure—from April 2021 to January 2025—the SEC filed numerous cases against Coinbase and its competitors, alleging that digital asset exchanges and staking businesses violated U.S. securities laws. “Despite good-faith efforts to comply with ambiguous securities regulations applied to digital assets, cases against these companies continued. Now, a crypto-friendly administration has taken the lead. Several bills on stablecoins and digital asset market structure are expected to move quickly through the Republican-controlled Congress, providing regulatory clarity for companies in the sector. In our view, the shift toward common-sense legislation and regulation will accelerate the adoption of public blockchains, benefiting investment strategies with significant exposure to digital assets,” Dowing notes.

Crypto ETFs: An Unstoppable Success

A clear sign of the favorable environment for crypto assets is the surge in passive investment vehicles. According to State Street projections, growing demand for crypto ETFs will soon surpass assets in precious metal ETFs in North America, making them the third-largest asset class in the ETF industry—behind only stocks and bonds.

Bitcoin and Ethereum ETFs were launched in the U.S. just last year, yet they have already accumulated $136 billion in assets, despite the recent market correction. State Street also forecasts that the SEC will approve more crypto-specific ETFs this year, with Litecoin, XRP, and Solana being the most likely to receive spot ETF approval, given that multiple U.S. ETF providers have already filed applications for these products.

This week has made it clear that we are in a new multipolar world, marked by a geopolitical and multilateral relations realignment. In this scenario, populism and politics generate increasing noise, which the market, for its part, strives to ignore. According to investment firms, this context calls for investors to rethink their roadmaps. What are they proposing?

For Michael Strobaek, Global CIO, and Nannette Hechler-Fayd’herbe, Head of Investment Strategy, Sustainability, and Research, and EMEA CIO at Lombard Odier, “a geopolitical realignment could significantly reshape the global economy and financial markets, leading to more balanced risk-adjusted returns across all asset classes and highlighting the benefits of broad diversification for asset allocators.”

According to these experts, investors are navigating a new post-Cold War multipolar era, where risk-adjusted returns are converging across major asset classes. “The global liberal democratic order seems to be taking a back seat to short-term national and economic interests, led by the new U.S. administration. Asset allocators must manage risk diligently and diversify broadly, leveraging alternative assets whenever possible,” stress experts at Lombard Odier.

For Gianluca Ungari, Head of Hybrid Portfolio Management at Quantitative Investments (Vontobel), and Sven Schubert, Head of Macro Research at Quantitative Investments (Vontobel), markets are moving quickly in response to this new environment. “Despite the initial impact of the tariff announcement on Canada, Mexico, and China—followed by a 25% increase on steel and aluminum imports starting March 12—the markets have absorbed the news relatively well. The direction of market movements in early February reflects the economic effects of the U.S. tariff hikes,” they note.

February now ends with the idea of reciprocal tariffs and ongoing negotiations between the U.S. and Russia to end the war in Ukraine. Because of this, Ungari and Schubert believe investors must stay vigilant. “While we maintain a constructive market outlook and a long position in equities, hedging strategies could be crucial for performance this year. So far, our tail hedges, such as the Japanese yen and gold, have performed well. Meanwhile, European equities have outperformed in recent weeks, driven by expectations of fiscal stimulus after the German elections and Trump’s decision to delay tariffs on Canada and Mexico,” they explain.

Enguerrand Artaz, strategist and fund manager at La Financière de l’Échiquier (LFDE), acknowledges that uncertainty has surged to levels even higher than during the trade tensions of 2019. In his view, equities should rotate towards more defensive sectors that are less exposed to global trade, such as utilities and real estate. “This scenario is not necessarily negative for European small caps, which are, on average, less exposed to international trade and more sensitive to falling interest rates,” he notes.

Additionally, Artaz believes that in a diversified allocation, it would be advisable to increase the proportion of fixed-income assets. “This is a logical move, as a tariff hike is both deflationary and recessionary for affected countries. An escalation could prompt the ECB to cut rates even further. While interest rates have shown resilience so far, if uncertainty persists, it could affect investor sentiment.” Artaz concludes that “for markets, an unpleasant but defined scenario—such as a fixed and final tariff increase—is often better than ambiguity fueled by political volatility.”

Market Behavior

According to Axel Botte, Head of Market Strategy at Ostrum AM (Natixis IM), financial markets appear isolated from the erratic communications coming from Donald Trump. “The flattening of the yield curve has led to a generalized tightening of spreads. Despite the Fed’s stance of maintaining the status quo and the restrictive policy of the Bank of Japan, monetary easing remains the predominant global trend. However, the sharp rise in gold prices sends a lone note of concern,” says Botte.

This global instability is also reflected in oil prices. In fact, the price of West Texas Intermediate (WTI) crude oil reached $72.80 per barrel on February 19, 2025, closing at $72.05 per barrel. “The increase in WTI crude prices is due to a combination of geopolitical, climatic, and supply-demand factors. Uncertainty surrounding production in Russia and the United States, along with the possibility of OPEC maintaining supply restrictions, has created a favorable environment for price escalation,” explains Antonio Di Giacomo, Senior Market Analyst at XS.com.

Additionally, in his view, investors have responded to these events with increased financial speculation in oil. “Market volatility has led to a higher volume of futures contract trading, contributing to price fluctuations. In this sense, traders are closely watching for any signs of changes in production policies from major exporting countries,” says Di Giacomo.

Another asset reflecting this context is gold. “Its price will remain high throughout 2025 amid increased central bank purchases, growing concerns over the harmful effects of U.S. tariffs, and demand for newly introduced gold ETFs. However, it could weaken if the interest rate differential between the U.S. and the rest of the world remains wide, which could keep the dollar strong, exerting downward pressure on gold. That said, this is not our base-case scenario,” adds Peter Smith, Senior International Equity Strategist at Federated Hermes.

0100 Europe will return to Amsterdam from April 2 to 4, 2024, bringing together 700 LPs, GPs, and SPs from the global private equity and venture capital industry. Organized by Zero One Hundred Conferences, this premier event offers an exclusive platform for top investors and industry leaders to connect and analyze emerging trends, investment strategies, and key market shifts shaping the future of private markets.

As the industry faces challenges related to liquidity and exits, fundraising uncertainty, valuation corrections, regulatory changes, and macroeconomic volatility, two investment strategies stand out as critical focus points for 2025: growth investing and the rise of the secondary market, as highlighted by key speakers at the upcoming conference.

The Rise of the Secondary Market

The secondary market has grown 16 times over the past 15 years, becoming a key liquidity tool. Joaquín Alexandre Ruiz, Head of Secondaries at the European Investment Fund (EIF), explains: “We have gone from a $10 billion market in 2009 to over $160 billion last year, with projections reaching $200 billion in 2025. This growth is largely driven by low capital distribution and the liquidity needs of LPs.”

With GP-led transactions now representing half of the market, continuation funds, portfolio sales, and partial sales have become essential liquidity solutions. Ruiz highlights the impact of the secondary market on industry dynamics: “Securing liquidity in today’s market requires creativity. Many GPs are using the secondary market not only to develop strategic assets but also to return capital to LPs.”

Growth Investing in Europe: Bridging the Capital Gap

The growth capital ecosystem in Europe is at a critical juncture, as large exits remain scarce and investor caution slows momentum. Shu Nyatta, Founder and Managing Partner of Bicycle Capital, compares this challenge to Latin America, where his firm invests: “The growth capital gap is real in both Latin America and Europe, but for different reasons. Latin America has never had a steady flow of growth capital, while Europe faces a sense of unmet expectations due to the lack of large exits.”

Despite having world-class early-stage venture funds, Europe’s growth equity markets must evolve. Nyatta emphasizes that the next wave of growth capital must focus on capital efficiency and resilience to ensure long-term success: “The next wave of growth capital must prioritize unit economics, resilient business models, and capital efficiency to drive sustainable success.”

A Gathering of Industry Leaders

0100 Europe will provide an in-depth analysis of how fund managers, investors, and institutions are addressing current challenges. Pavol Fuchs, CEO of Zero One Hundred Conferences, highlights the event’s role in shaping the industry’s future:

“As private markets evolve, adaptability is key. Finding the best opportunities—whether in the secondary market, growth investments, or co-investments—depends on strong, long-term relationships built at events like this. The 0100 Europe conference provides an exclusive environment where investors and fund managers can exchange strategies, explore new opportunities, and connect with the most influential players in the industry.”

State Street Corporation and Mizuho Financial Group have announced an agreement under which State Street will acquire Mizuho‘s global custody business and related activities outside Japan. According to the companies, these businesses support the overseas investments of Mizuho‘s Japanese clients.

Currently, Mizuho operates its global custody business and related services outside Japan through its local subsidiaries: Mizuho Trust & Banking (Luxembourg)—owned by Mizuho Trust & Banking—and Mizuho Bank (USA), a wholly owned subsidiary of Mizuho Bank, Ltd. Both entities manage approximately $580 billion in assets under custody and $24 billion in assets under management.

According to the companies, following this transaction, Mizuho will leverage its expertise and network as one of Japan’s leading financial institutions to continue providing its Japanese clients with reliable custody services for their domestic assets while collaborating with State Street on global custody and related services.

The transaction is expected to be completed in the fourth quarter of 2025, as it remains subject to regulatory approvals and other closing conditions.

Key Statements on the Transaction

“Japan, Luxembourg, and the United States are key markets for State Street. This transaction demonstrates our strong commitment to accelerating our growth in these markets. Mizuho’s decision to entrust State Street with serving its valued clients reaffirms its confidence in our high-quality service, industry-leading capabilities, and commitment to product innovation and technology investment. With 35 years of experience in Japan and Luxembourg, along with our long-standing presence in the United States, State Street is well-positioned to support the global growth and business transformation of Mizuho‘s clients,” said Stefan Gmür, Head of Asia-Pacific and Head of Strategic Business Growth at State Street.

Meanwhile, Tsutomu Yamamoto, Senior Executive Officer and Head of the Global Transaction Banking Unit at Mizuho, added: “In today’s increasingly complex investment landscape, clients require global custody providers with significant scale and deep expertise. After careful evaluation, we have decided to transfer our global custody business to State Street, a recognized leader with an established presence in Japan. This strategic move will ensure that our clients benefit from State Street‘s global platform and extensive expertise.”

According to Hiroshi Kobayashi, Head of Japan at State Street, this transaction aims to meet clients’ needs not only in global custody but also in data management, risk and performance analysis, currency management, and securities financing.

“We look forward to ensuring a seamless transition for Mizuho’s clients. As the acquired business integrates into our global operating model, we are confident that our increased scale will allow us to further expand our technological and service capabilities, enhancing the experience for both existing and new clients in Japan,” Kobayashi stated.

State Street’s Business in Japan and Luxembourg

State Street established its business in Japan more than 35 years ago. With an experienced team of over 500 employees across its offices in Tokyo and Fukuoka, State Street provides Japanese institutional investors with a full range of services, including trusts, global custody, middle- and back-office outsourcing, data management, trading solutions, and financing. State Street also operates a center of operational excellence in Fukuoka, which has been supporting clients in Japan and the broader Asia-Pacific region for over a decade.

Additionally, State Street has been present in Luxembourg for 35 years, offering services such as fund administration, custody, and transfer agency. Headquartered in Boston, Massachusetts, State Street operates globally across more than 100 markets.