U.S. stocks were lower in February, primarily driven by underperformance in the Nasdaq and Russell 2000. The month was characterized by a shift from growth to value, as rising concerns over the sustainability of the AI secular growth narrative nudged several of the “Magnificent 7” stocks into correction territory.

Political dynamics remained a dominant theme as President Trump, now a full month into his second term, continued to push his deregulation and pro-growth policies. Yet, market sentiment was tempered by persistent concerns over the impact of his tariff policies on both domestic and international companies. The month began with President Trump announcing 25% tariffs on Canada & Mexico and 10% on China*. While those tariffs were ultimately delayed as negotiations were ongoing, the uncertainty of trade war developments has set the stage for potential volatility ahead.

Economists worry that expectations of higher growth under President Trump’s administration could keep inflation elevated for longer, potentially complicating the Federal Reserve’s policy path. In Fed Chair Powell’s semiannual monetary policy report to Congress, he noted that recent indicators suggest economic activity has continued to expand at a solid pace, with GDP rising 2.5% in 2024. He added that as the economy evolves, the Fed will adjust its policy stance to best promote maximum employment and stable prices.

Small-cap value stocks underperformed their large-cap value counterparts during the month, as concerns over “higher for longer” interest rates have continued to be a near-term headwind. However, as rates trend lower, we believe small- and mid-sized companies are well-positioned to benefit through 2025/2026 from stronger domestic growth and pro-business policies.

New deal activity remains healthy at $862 billion globally, an increase of 15% compared to 2024 levels. M&A advisers remain upbeat about corporate appetite to make acquisitions due to a return to a more traditional regulatory framework. Some acquirers are choosing to wait for greater certainty and/or clarity on tariffs and the Trump Administrations priorities.

Opinion by Michael Gabelli, managing director of Gabelli & Partners

* This article was written prior to U.S. President Donald Trump’s recent announcements on tariffs.

Last week, Google announced that it would acquire Wiz for $32 billion, marking its largest acquisition ever. Wiz, which offers cloud security solutions, was founded in 2020 and by the end of 2022 was already valued at $6 billion. By 2023 the company had achieved $100 million in recurrent revenue “ARR”, and by YE-2024 the company was reported to reach a stunning $500 million in ARR, demonstrating a unique capacity to grow sales at an impressive pace. Wiz received venture backing from its onset. Its first institutional round was for $20 million. Those early investors, which included the famous Sequoia Capital may reap close to a 100X gross over their original investment.

Venture is the one category within the private assets world that it is not actively raising capital from the wealth industry, yet certainly exploring options on how to. It’s also the riskiest and probably least understood space of private investing, although nowadays there’s a never-ending sleuth of podcasts and articles to learn about it.

Accessing and selecting VC funds is also complicated. The one easy path for retail investors is to participate in venture-backed companies when these become public through an IPO. Once publicly traded, VC funds will typically maintain their position until they find the right moment to exit, potentially generating better outcomes for investors, keeping their board seats and therefore their influence. Not all VC-backed companies go public though, many exits occur through strategic acquisitions as in the case of Wiz.

VC-backed companies raise money through capital rounds, starting with seed and all the way to growth capital. At the seed stage, a particular technology or service may still be a project in paper and the funds would be used by the founders to kickstart the company. Once the growth stage is reached, the company typically has proven sales and customers. Capital would be employed for expansion projects through marketing, hiring top performing sales professionals or developers, amongst other initiatives. From seed to growth to a potential IPO, an average VC-backed company would have raised capital about 6 to 8 times throughout a cycle of 10 years or more, although the amount of capital and number of rounds required varies.

The VC industry has historically been recognized for being able to generate exponential results over relatively small investments. A good example is Amazon: it took only two rounds of outside investor funding (the second by a venture fund) for a total of $9 million to help it achieve self-sustainability and its future valuation.

However, cases like Amazon and Wiz are true outliers, even within the VC universe: they resulted in outsized returns for institutional backers. Double or even triple digit multiples are quite rare yet are targeted by all VC funds as they represent a fundamental element of the industry: the power-law.

You will hear that VC is a power-law industry meaning in practical terms that for any number of investments, it is only a very limited number of those that explain the returns of a venture fund. Imagine for instance a seed fund that made a series of investments and 10% of capital returned 100X. No matter what happens to the rest of the portfolio, that fund would have achieved at least a 10X gross (10% times 100).

As mentioned above, very high returns (in the order of 50X or above) are extremely rare (less than 1% of all seed investments made) whereas capital loss due to projects failing can exceed 50% in any given seed fund. Devoid of power-law results, seed funds would likely provide poor returns for investors.

Alas, not all VC investing relies solely on a model where a very small fraction of invested capital drives all returns. Growth-venture is a more accessible space as funds that focus on this category tend to be much larger than early stage ones and typically invest in companies that have a proven track record, reducing the probability of capital loss. Entry points and prices though can be substantially higher than at the seed stage and therefore return expectations for specific investments tend to be lower. Wiz for instance was valued at about $70M when it got its institutional seed checks back in 2020 but it raised a growth round at the end of 2021 at the aforesaid $6B valuation. Compared to its destined exit value of $32B, that is more than a 5X growth multiple in value achieved in only 3-4 years, which is still impressive.

The message: growth venture can still produce very attractive returns, relying on a model in which investment periods are expected to be somewhat shorter and capital losses lower relative to seed investing. The table below compares some characteristics between these two categories.

Typical characteristics of seed and growth funds (using data for Vintages 2012 to 2022)

Source: produced with Grok Artificial Intelligence application. Carta Q2 2024 (fund sizes), PitchBook Q3 2024 (fund sizes up to $2B investments, rounds for 2012– 2022), Cambridge Associates (2024) (stage definitions for 2012– 2022).

Can I invest in venture?

This article covers a limited scope of the VC industry and some of its characteristics. Note that VC fund styles can vary and be more flexible in terms of investing strategy. Multistage funds, for instance, can invest in seed, core venture (which we did not touch upon in this article) and growth. Some of the most recognized VC funds actually fall under the multi-stage category.

VC funds are generally limited to qualified purchasers through traditional drawdown funds. Achieving top quartile returns in venture requires investing with the most recognized managers of the industry. To begin with, access to startup funding varies across VC funds: it is not a plain level field. It is widely recognized that founders tend to favor the most reputable funds and their partners, who often are invited first to invest in top-tier projects.However, accessing these partnerships is a time-consuming exercise. Typically, it is the purview of institutional investors and teams who focus on manager selection and nurturing relations with GP’s. In some cases, being invited to a capacity-constrained venture fund can take years of insistence.

Given this condition, an adequate allocation strategy for qualified retail investors is to commit to a fund of funds “FoFs” with demonstrated access to some of the top names. Interestingly, FoF’s nowadays may even accept capital commitments as low as $100K, providing proper diversification. Some of these may even incorporate co-investments in their approach to have direct exposure to companies like Wiz.

UBS Asset Management (UBS AM) has announced the launch of two new UCITS ETFs that offer exposure to the Nasdaq-100 Notional and Nasdaq-100 Sustainable ESG Select Notional indices. According to Clemens Reuter, Head ETF & Index Fund Client Coverage, UBS Asset Management, “these are the first two Nasdaq-100 ETFs we are launching, giving clients the option to choose between the iconic index and the sustainable version of the same benchmark.”

Regarding the funds, they state that the UBS ETF (IE) Nasdaq-100 UCITS ETF passively replicates the Nasdaq-100 Notional Index, which is composed of the 100 largest U.S. and international non-financial companies listed on the Nasdaq Stock Market, based on market capitalization. The index includes companies from various sectors such as computer hardware and software, telecommunications, retail/wholesale, and biotechnology. The manager clarifies that the fund is aligned with Art. 6 under SFDR and is physically replicated.

Meanwhile, the UBS ETF (IE) Nasdaq-100 ESG Enhanced UCITS ETF passively replicates the Nasdaq-100 Sustainable ESG Select Notional Index, which is derived from the Nasdaq-100 Notional Index. Companies are evaluated and weighted based on their business activities, controversies, and ESG risk ratings. Companies identified by Morningstar Sustainalytics as having an ESG risk rating score of 40 or higher, or as involved in specific business activities, are not eligible for inclusion in the index. The ESG risk rating score indicates the company’s total unmanaged risk and is classified into five risk levels: negligible (0–10); low (10–20); medium (20–30); high (30–40); and severe (40+).

In addition, the ESG risk score of the index must be 10% lower than that of the parent index at each semi-annual review. A lower index-weighted ESG risk score means lower ESG risk. The fund is physically replicated and aligned with Art. 8 under SFDR.

According to the manager, the UBS ETF (IE) Nasdaq-100 UCITS ETF will be listed on SIX Swiss Exchange, XETRA, and London Stock Exchange, while the UBS ETF (IE) Nasdaq-100 ESG Enhanced UCITS ETF will be listed on SIX Swiss Exchange and XETRA.

For wealth managers, growth has been strong over the past five years, with a global increase of 20% in assets under management (AuM). According to the Wealth Industry Survey by Natixis IM, the pursuit of growth is even greater this year, as firms project an average increase of 13.7% in wealth just in 2025. However, given geopolitical changes, economic uncertainty, and accelerated technological advances, investment leaders know that meeting these expectations will not be an easy task.

Geopolitics and Inflation: Key Concerns

The results show that while 73% are optimistic about market prospects in 2025, macroeconomic volatility remains a major concern. 38% of respondents cite new geopolitical conflicts as their main economic concern, closely followed by inflation, with 37% of respondents fearing that it may resurge under Trump’s policies. Additionally, 66% anticipate only moderate interest rate cuts in their regions.

Despite these concerns, 68% of analysts state that they will not adjust their return expectations for 2025, as wealth managers are implementing strategies for their businesses, the market, and most importantly, their clients’ portfolios, with the aim of delivering results.

In addition to new geopolitical conflicts and inflation, respondents also identified other concerns for 2025. 34% point to the escalation of current wars, and another 34% highlight U.S.-China relations. Lastly, 27% underscore the tech bubble as another factor to consider.

With this in mind, wealth managers are carefully considering how geopolitical turbulence and persistent inflation will impact the macroeconomic environment. Half of the respondents forecast a soft landing for their region’s economy, with the strongest sentiment in Asia (68%) and the U.S. (58%). However, this drops to 46% in Europe and just 37% in the U.K. Additionally, 61% are concerned about stagflation prospects in Europe.

Regarding the specific impacts of the U.S. elections on the economic outlook, two-thirds globally are concerned about the possibility of a trade war. However, wealth managers also see opportunities on the horizon, as 64% believe that the regulatory changes proposed by the Trump administration will drive the development of innovative investment products.

In addition, two-thirds believe that the proposed tax cuts will drive a sustained market rally. Taking all of this into account, 57% globally say that, in light of the U.S. election outcome, clients are more willing to take on risk, with the potential to disrupt the cash accumulation pattern investors have maintained since central banks began raising rates.

The Investment Potential of AI

After witnessing the rapid development of generative AI models, 79% of surveyed wealth managers say that AI has the potential to accelerate profit growth over the next 10 years. With this in mind, firms are looking to leverage the benefits of the new technology in three key areas: tapping into the investment potential of AI, implementing AI to improve their internal investment process, and using AI to optimize business operations and customer service.

69% of respondents say that AI will improve the investment process by helping them uncover hidden opportunities, and another 62% say that AI is becoming an essential tool for assessing market risks. In fact, the potential is so significant that 58% say that companies that do not integrate AI will become obsolete.

With this in mind, 58% say their company has already implemented AI tools in their investment process. The highest concentration of early adopters is found among wealth management firms in Germany (72%), France (69%), and Switzerland (64%).

Beyond investment opportunities and portfolio management applications, wealth managers also anticipate that AI will impact the service side of the business. Overall, 77% say that AI will help them meet their growth goals by integrating a wider range of services. However, the technology can be a double-edged sword, as 52% also fear that AI is helping turn automated advice into a real competitive threat.

“Wealth managers face a wide range of challenges in 2025, from educating their clients on the benefits of holding private investments to finding the best ways to integrate AI into their investment and business processes. However, despite potential obstacles, wealth managers are confident that they can harness disruptive forces to unlock new opportunities and meet the AUM growth goals they need to achieve in 2025,” says Cecile Mariani, Head of Global Financial Institutions at Natixis IM.

Appetite for Private Assets Continues to Grow

Technology may have the potential to transform the industry, but firms face more immediate challenges in meeting clients’ investment preferences and return expectations.

Wealth managers are exploring a wider range of vehicles and asset classes to meet their clients’ needs. Globally, portfolios now consist of 88% public assets and 12% private assets, a ratio that is likely to shift as focus on private assets increases. Additionally, 48% state that meeting the demand for unlisted assets will be a critical factor in their growth plans.

However, private asset allocation is not without its challenges. 26% of respondents consider access to these assets—or lack thereof—a threat to their business. Despite this, new product structures are helping to ease this pressure, with 66% noting that private asset vehicles accessible to retail investors improve diversification.

The next challenge will be financial education, as 42% believe that a lack of understanding about liquidity is a barrier to incorporating private assets into client portfolios. Nevertheless, the lack of liquidity can also work in favor of some investors, given that 75% of wealth managers globally say that the long-term nature of retirement savings makes investment in private assets a sound strategy.

Overall, 92% plan to increase (50%) or maintain (42%) their private credit offerings, and similarly, 91% plan to increase (50%) or maintain (41%) their private equity investments on their platforms. Few among the respondents see this changing, as 63% say that there is still a significant difference in returns between private and public markets. Additionally, 69% say that despite high valuations, they believe private assets offer good long-term value.

The 2025 Wealth Management Industry Survey by Natixis Investment Managers gathers the views of 520 investment professionals responsible for managing investment platforms and client assets across 20 countries.

Paulina Esposito, Head of Sales Uruguay – Argentina at LarrainVial

Paulina Esposito, the newly appointed Head of Sales Uruguay – Argentina at LarrainVial, is a distinguished professional with over 25 years of experience in the sector. She shares her insights with FlexFunds and Funds Society through The Key Trends Watch initiative, reflecting on the challenges and opportunities that have shaped her career.

As Head of Sales, she aims to position the company as a key player in the region by leveraging its multi-manager model to offer investment strategies based on rigorous analysis and strategic vision. To achieve this, she considers it essential to build trust and communicate the company’s value effectively.

In her approach, Esposito underscores the importance of selecting timeless investment strategies that can endure market fluctuations over time. These strategies are based on consistent processes and strong management teams, enabling investors to navigate volatility confidently. Additionally, she emphasizes the need to educate clients, helping them understand what they are investing in and why a particular investment is suitable for their portfolio.

What are the most important trends currently shaping the asset management industry?

Two key areas stand out: technology and alternative assets. Technological innovation is transforming the industry, driven by a new generation with different training and mindsets. Meanwhile, alternative assets such as private credit and direct lending are gaining relevance, offering stability and diversification in emerging markets like Latin America.

How do you think the industry will evolve—toward separately managed accounts (SMAs) or collective investment vehicles?

The industry will likely adopt a hybrid model combining separately managed accounts (SMAs) and collective investment vehicles. The diversity of clients and capital requires flexible solutions. While high-net-worth investors often seek personalized management due to their specific interests and ability to seize unique opportunities, collective investment vehicles are ideal for more diversified, lower-volume portfolios. In this context, both approaches can coexist and complement each other based on client profiles and needs.

What is the biggest challenge in capital raising and client acquisition today?

One of the most significant challenges is understanding each client’s evolving needs deeply. The key lies in active listening. Today’s investors assess more complex factors than before and seek more than just returns—they want trust, consistency, and a personal connection with their advisors.

This approach requires discipline, consistency, and effective communication that prioritizes client expectations over personal preferences. Becoming a trusted advisor means listening actively and adapting communication to ensure clients feel understood.

What factors do clients prioritize when making investment decisions today?

Decision-making dynamics are shifting. While clients still seek returns, they are increasingly focused on managing volatility and understanding how products behave in turbulent markets. Additionally, investors are paying closer attention to managers’ track records and ability to navigate challenging scenarios.

Liquidity has also become a critical factor, particularly for alternative products. Although alternative investments can provide stability and diversification, their illiquid nature must be explained and understood by clients. Designing a well-balanced portfolio is essential—one that combines liquid assets such as bonds, equities, and funds with global diversification to mitigate the risks associated with sector-specific fluctuations.

How is technology transforming the asset management sector?

Technology is forcing all financial sector players to stay constantly updated. This presents a significant challenge for advisors, as younger generations naturally possess strong technological skills.

Integrating these tools is not just necessary for advisors—it is an opportunity to add value in an environment where technology has made investment platforms and options more accessible. Younger clients are already leveraging these advancements to build savings more efficiently. The challenge, therefore, is to understand these new dynamics while maintaining the relevance of human advisors, particularly in direct client interactions and the personalization of investment strategies.

The impact of artificial intelligence on investment management

According to Esposito, artificial intelligence is beginning to play a crucial role in investment analysis. Many investors already use AI-driven platforms that provide specific recommendations for portfolio adjustments. This pushes advisors to be more proactive and adapt quickly to emerging client needs.

In the past, clients tended to hold certain investments for extended periods. However, AI-generated alerts are now driving a trend of continuous portfolio adjustments. “This shift underscores the importance of communication and client proximity. Without these interactions, advisors risk losing their role in portfolio management.”

In her view, the most critical skills investment advisors need to develop are “active listening and effective communication.” Beyond mastering the technical aspects of financial products, an advisor must understand clients’ needs, goals, and concerns. “The ability to tailor strategies to each client and communicate ideas clearly and simply is crucial in an environment where not all clients have the same level of financial sophistication,” Esposito emphasizes.

Trends and challenges in the coming years

The financial sector is undergoing a generational shift over the next 5-10 years. The younger generations, raised in the digital era, will have different expectations and become more familiar with technological tools. This means the biggest challenge for advisors will be finding ways to add value beyond what technology can offer.

Looking ahead, Esposito highlights key themes and strategies essential for a diversified portfolio. Private credit, infrastructure trends, and global equity positions will be crucial. Additionally, opportunities in emerging markets—particularly in Latin America—should be considered. Countries like Argentina present attractive possibilities but have inherent risks, requiring active management.

Finally, reflection and portfolio rebalancing become indispensable in a constantly evolving market. More than ever, Esposito emphasizes, “the ability to listen, communicate, and anticipate will distinguish those who lead the change from those who fall behind.”

The interview was conducted by Emilio Veiga Gil, Executive Vice President of FlexFunds, as part of the Key Trends Watch initiative by FlexFunds and Funds Society.

As he does every year, Larry Fink, CEO of BlackRock, has published his annual letter to investors, in which he analyzes the long-term forces shaping the global economy and how BlackRock is helping its clients navigate these dynamics and seize emerging opportunities.

What stands out is that in the opening lines of his letter, he acknowledges that investors are nervous. “I hear it from nearly every client, nearly every leader, nearly every person I speak with: they’re more worried about the economy than at any time in recent memory. And I get it. But we’ve been through moments like this before. And somehow, over the long term, we find a way through,” he writes.

To explain how the asset manager is approaching today’s environment and its view of the world, the letter opens by highlighting a key principle of BlackRock’s business: that capital markets can help more people experience the growth and prosperity that capitalism can deliver.

“Of all the systems we’ve created, one of the most powerful — and especially suited for moments like this — began over 400 years ago. It’s the system we invented specifically to overcome contradictions like scarcity amid abundance and anxiety amid prosperity. We call this system the capital markets.”

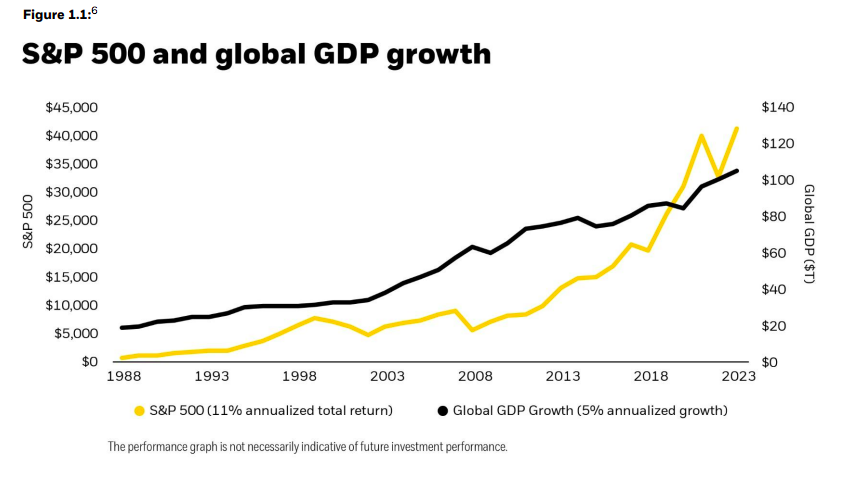

The CEO highlights that investors have benefited from the greatest period of wealth creation in human history, noting that in the last 40 years, global GDP has grown more than in the previous 2,000 years combined. He argues that this extraordinary growth — driven in part by historically low interest rates — has generated exceptional long-term returns. However, he acknowledges that not everyone has shared in this wealth.

Fink concedes that capitalism has clearly not worked equally for everyone, and that markets are not perfect. To change this, he believes the answer is not to abandon the markets, but to expand them: “to complete the democratization of the market that began 400 years ago and enable more people to have meaningful participation in the growth happening around them.” How can investment continue to be democratized? In his view, there are two general ways: helping current investors access parts of the market that were previously out of reach, and enabling more people to become investors from the outset.

“More investment. More investors. That’s the answer. Since BlackRock is a fiduciary and the world’s largest asset manager, some readers might say I’m talking my book. That’s understandable. But it’s also the path we consciously chose, long before it was fashionable. From the beginning, we believed that when people can invest better, they can live better — and that’s exactly why we created BlackRock,” he states.

Unlocking Private Markets

In Fink’s view, the assets that will define the future — such as data centers, ports, power grids, and the world’s fastest-growing private companies — are not available to most investors. “They are in private markets, locked behind high walls, with doors that only open to the largest or wealthiest market participants. The reason for this exclusivity has always been risk. Illiquidity. Complexity. That’s why access is limited to certain investors. But nothing in finance is immutable. Private markets don’t have to be so risky, opaque, or out of reach — not if the investment industry is willing to innovate. And that’s exactly what we’ve been working on at BlackRock over the past year.”

In this vein, over the last fourteen months, BlackRock has acquired Global Infrastructure Partners (GIP) and Preqin, and announced the acquisition of HPS Investment Partners. According to the CEO, these moves enable broader access to private markets for more clients and provide investors with greater choice. “BlackRock is transforming the future of our industry to better serve today’s clients,” he adds.

The Big Retirement Question

For BlackRock, these strategic moves are driven by the mismatch between investment demand and capital available from traditional sources. Capital markets can help fill that gap. In this regard, the CEO explains how democratizing investment can help more people secure their financial future and that of their families.

In the letter, he outlines ideas such as helping people start investing earlier and giving retirees the peace of mind and security needed to spend in retirement. “A good retirement system acts as a safety net that protects people when they face hardship. But a great system also offers a path to build savings, accumulating wealth year after year,” he notes. More than half of the assets managed by BlackRock are for retirement funds. “It’s our core business, and that makes sense: for most people, retirement accounts are their first — and often only — experience with investing. So if we truly want to democratize investing, retirement is where the conversation has to start,” he adds.

Focusing on the U.S., he considers the situation there to be critical: “Public pension systems are facing massive shortfalls. Nationally, data shows they are only 80% funded — and that number is likely too optimistic. Meanwhile, one-third of the country has no retirement savings at all. As money becomes scarce, people are living longer. Today, if you’re married and both partners reach age 65, there’s a 50% chance that at least one of you will live to 90.”

In response, he highlights that last year, BlackRock launched LifePath Paycheck® to address this fear. “It offers people the option to convert 401(k) retirement savings into a steady, reliable monthly income. In just 12 months, LifePath Paycheck® has already attracted six plan sponsors representing 200,000 individual retirement savers,” he explains.

A Look at Europe

On major market trends, Fink also shared his views. Regarding Europe, he believes the continent is waking up and wonders if it’s time to turn bullish on the region. “The policymakers I speak with — and I speak with many — now recognize that regulatory barriers won’t disappear on their own. They must be addressed. And the potential is enormous. According to the IMF, reducing internal trade barriers within the EU to the level that exists among U.S. states could boost productivity by nearly 7%, adding a staggering $1.3 trillion to the economy — the equivalent of creating another Ireland and another Sweden,” he states.

He adds that the biggest economic challenge facing the continent is the aging workforce: “In 22 of the 27 EU member states, the working-age population is already shrinking. And since economic growth largely depends on the size of a country’s labor force, Europe faces the risk of a prolonged economic slowdown.” The letter highlights that BlackRock manages $2.7 trillion for European clients, including around 500 pension plans supporting millions of people.

It also notes that ETFs contribute to developing an investment culture in Europe, making it easier for more individuals to reach their financial goals by using capital markets: “When first-time investors start entering capital markets, they often do so through ETFs — and particularly iShares. We are working with established players, as well as several newcomers to Europe, such as Monzo, N26, Revolut, Scalable Capital, and Trade Republic, to lower investment barriers and build financial literacy in local markets.”

Tokenization: The Great Revolution of Democratization

While expanding access to capital markets requires innovation and effort, Fink believes it’s not an insurmountable challenge. As an example of such innovation, he points to tokenization as a clear step toward democratization. In his view, if SWIFT is like postal mail, then tokenization is email: assets move directly and instantly, bypassing intermediaries.

“What exactly is tokenization? It’s the process of turning real-world assets (stocks, bonds, real estate) into digital tokens that can be traded online. Each token certifies your ownership of a specific asset, much like a digital deed. Unlike traditional paper certificates, these tokens live securely on a blockchain, enabling instant buying, selling, and transferring — without cumbersome paperwork or waiting periods. Every stock, every bond, every fund, every asset can be tokenized. If they are, it will revolutionize investing. Markets would no longer need to close. Transactions that now take days could settle in seconds. And billions of dollars currently trapped by settlement delays could be immediately reinvested into the economy, generating more growth,” he explains.

In his view, perhaps most importantly, tokenization makes investing far more democratic. “It can democratize access, shareholder voting, and returns. One day, I hope tokenized funds become as familiar to investors as ETFs — provided we solve one critical issue: identity verification,” Fink concludes.

On Thursday, March 27, the SEC voted to end its defense of rules requiring the disclosure of climate-related risks and greenhouse gas emissions.

Acting SEC Chair Mark T. Uyeda stated: “The purpose of the Commission’s action and today’s notice to the court is to cease its involvement in defending the costly and unnecessarily intrusive climate change disclosure rules.”

The rules, adopted by the Commission on March 6, 2024, established a special, detailed, and extensive disclosure regime regarding climate risks for reporting and emitting companies.

The rules have been challenged by states and individuals. The litigation was consolidated in the Eighth Circuit (Iowa v. SEC, No. 24-1522 (8th Cir.)), and the Commission had previously stayed the effectiveness of the rules pending the outcome of the case. Briefing in the case was completed before the change in administration.

Following the Commission’s vote, SEC staff sent a letter to the court stating that it was withdrawing its defense of the rules and that Commission attorneys are no longer authorized to present arguments in support of the Commission’s brief. The letter indicates that the Commission defers to the court on the timing of oral arguments.

Vanguard has announced the appointment of Pablo Bernal as Country Head for Spain, underscoring the firm’s commitment to the Spanish market.

Bernal joined Vanguard in Mexico in 2017 and most recently served as Head of Intermediary Sales for Latin America. In his new role, he will be based in London, from where he will initially serve the Spanish market, reporting to Simone Rosti, Head of Italy and Southern Europe.

Earlier this year, Vanguard appointed Álvaro Hermoso Ferreiro as Sales Executive and Head of Client Support in Spain. He will now report to the new Country Head.

“We are very pleased to welcome Pablo to our team in Europe and to strengthen Vanguard’s presence in Spain. We have been working with clients in this country for many years and have built strong on-the-ground relationships that we now aim to expand and deepen. Spain represents a significant opportunity to serve both wholesale and advisory clients, as well as those serving self-directed investors. We believe Vanguard’s investment principles, backed by 50 years of proven experience, will resonate well with Spanish investors and give them the best chance for investment success,” said Robyn Laidlaw, Head of European Distribution at Vanguard.

The firm highlights that Spain is one of the largest investment management markets in Europe. However, it acknowledges that one of the main challenges in the Spanish market is the relatively low penetration of indexing and ETFs. As one of the world’s largest managers of both passive and active investments, Vanguard believes it is well positioned to help investors understand the benefits of low-cost index funds and ETFs.

Following the announcement, Pablo Bernal, now Country Head for Spain, commented: “I’m excited to bring Vanguard closer to Spanish investors. As we celebrate the firm’s 50th anniversary this year, it’s the perfect time to share our mission of standing up for all investors. We believe our broadly diversified index funds and ETFs, designed for long-term investing, along with our value-added services for intermediaries, will align well with a wide range of local clients. We also plan to expand our local operations and team by the end of this year.”

The last 25 years have been marked by a growing focus on diversity and gender inclusion worldwide, with specific strategies aimed at eliminating biases across all areas of society. This trend has also reached the investment sector and its investment criteria.

According to UBS in its Gender-Lens Investment report, the origins of gender-focused investing are deeply rooted in the collective effort to empower women. “However, it would be a mistake not to recognize the significant economic benefits that can result from it. Closing the gender gap in labor force participation and management positions could alone contribute up to 7 trillion dollars to global GDP. This number rises to between 22 and 28 trillion dollars if gender equality is achieved,” the report states.

These potential economic benefits are capturing the attention of governments and economists, who are implementing new strategies to strengthen the role of women in society. However, UBS also believes that investors can benefit from this momentum by identifying opportunities within the three gender-focused investment perspectives.

Investment Ideas With a Gender Perspective

The first perspective proposed by UBS is based on the idea that investments for women encompass a wide range of products and services that meet their needs. “We believe the most viable investment opportunity lies in emerging digital technologies,” the report states. In their view, many gender-focused efforts, such as those related to education or financial inclusion, have concentrated on serving women in emerging and frontier markets, often through philanthropic mechanisms such as blended finance and grant funding.

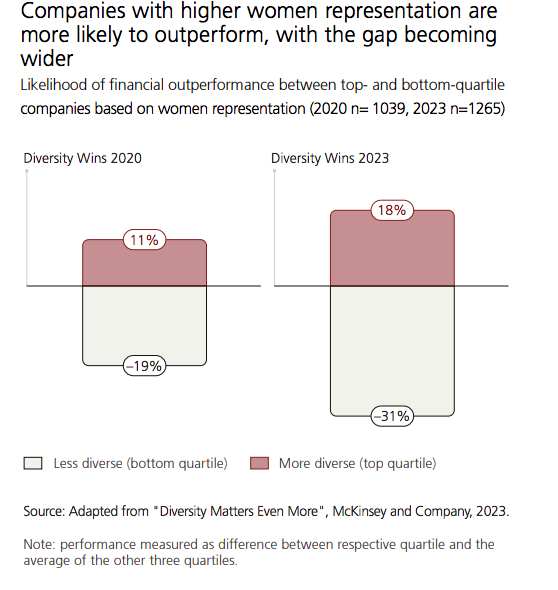

The second idea UBS advocates in its report is that investments in women represent, in their opinion, the most scalable and diversified investment opportunity, as they provide access to various industries, regions, and types of companies. In this regard, they explain that this includes more established approaches, such as “investing in companies with significant female representation in management positions, based on the investment thesis that diverse companies tend to achieve better financial performance.”

Lastly, the UBS report argues that “investments made by women offer the opportunity to incorporate capital with a more defined purpose into portfolios, with credible sustainable and impact investment solutions, as well as less liquid investments in private companies and assets that are likely to gain greater relevance.”

From Approach to Fund Construction: Three Examples

As a result of this approach, asset managers have created specific funds that incorporate the ideas proposed and analyzed in the UBS report. For example, in 2019, Nordea AM launched the Global Diversity Engagement Strategy fund, aiming to capitalize on the growing awareness of diversity and inclusion. According to Julie Bech, the fund manager, the strategy focuses on investing in companies that lead in gender equality and diversity while also engaging with those at the beginning of their diversity journey to help accelerate their progress.

“The strategy consists of a global equity portfolio with an additional level of social engagement. Stock selection is based on the multi-asset team’s quantitative model at NAM, which filters the most attractive investments using factors such as quality, value, momentum, and historical relative profitability. The strategy evaluates companies using a ‘diversity overlay,’ which assigns them a score based on four criteria: leadership diversity, talent pipeline, inclusion efforts, and diversity change,” Bech adds.

Along the same lines, the Mirova Women Leaders Equity Fund, launched in 2019 by Mirova, a subsidiary of Natixis Investment Managers, stands out. This vehicle invests in companies that contribute to the UN’s Sustainable Development Goals, with a special focus on gender diversity and female empowerment.

Also within the equity market, investors have access to the RobecoSAM Global Gender Equality Equities fund. According to the asset manager, it is an actively managed vehicle that invests globally in companies that promote gender diversity and equality. “Stock selection is based on fundamental analysis, and the strategy integrates sustainability criteria as part of the selection process through a specific gender-focused sustainability assessment. The portfolio is built from an eligible investment universe that includes companies with higher gender scores, based on an internal gender assessment methodology. This methodology covers various criteria, such as board diversity, pay equity, talent management, and employee well-being,” they explain.

The world’s major economies are making their move in response to the Trump administration’s tariff game. Meanwhile, markets are feeling the impact of commercial and geopolitical uncertainty, and investors are beginning to consider a scenario of economic recession in the U.S. alongside rising inflation. This heightened volatility translated into another turbulent session on Wall Street, with declines in the S&P and Nasdaq, as well as European stock markets falling for the fourth consecutive session (EuroStoxx 50 -1.4%; Ibex -1.5%).

“The fear of a U.S. economic recession and its spillover to the rest of the world, partly driven by Trump’s unstable trade policy in these early months of his term, is leading to profit-taking after an excellent start to the year for European stock markets,” explain analysts at Banca March.

According to Gilles Moëc, chief economist at AXA IM, “there is a revolutionary atmosphere in Europe.” He believes that “the reaction of EU institutions and national governments to the U.S. challenge has been quicker and stronger than expected.” He warns of two key issues: first, “whether national governments have the willingness and capacity, given already unstable fiscal positions and watchful markets”; second, “the magnitude of the multiplier effects that this additional spending will have on GDP, both in Europe and in Germany,” a country about which he notes, “the revolution could be relatively painless.”

Where Are We in This Tariff Game?

To summarize quickly, Trump has implemented 25% tariffs on all steel and aluminum imports, with Canada, Brazil, and Mexico being the most affected. Additionally, the U.S. president has threatened to double tariffs on Canadian steel and aluminum to 50%, in response to a 25% increase in the electricity price Ontario exports to the United States.

On the receiving end of these new tariffs, the latest response has come from the European Union. Ursula von der Leyen, president of the European Commission, has just announced countermeasures worth €26 billion, which will affect U.S. products such as textiles, appliances, and agricultural goods starting April 1. The European Commission “regrets the U.S. decision to impose such tariffs, which are unjustified and harmful to transatlantic trade, damaging businesses and consumers and often resulting in higher prices.” Brussels estimates that these tariffs on steel, aluminum, and derivative European products will have an impact of around $28 billion.

How Much and How the Landscape Has Changed

In response to this situation, international asset managers are adjusting their scenarios. According to Lizzy Galbraith, political economist at Aberdeen Investments, the rapid adoption of executive measures by President Trump, particularly in trade, has led them to update their outlooks from several important perspectives.

“We now see the U.S. weighted average tariff rate continuing to rise to 9.1%. We assume a reciprocal tariff will be implemented, though with several exemptions. We anticipate higher general tariffs on China and more sector-specific tariffs, including those applied to the EU, Canada, and Mexico. Additionally, the risk that trade policy becomes even more disruptive has increased,” she notes.

Galbraith acknowledges that their “Unleashed Trump” scenario assumes reciprocal tariffs are systematically applied and include non-tariff trade barriers, while the United States-Mexico-Canada Agreement (USMCA) collapses entirely. “This results in the average U.S. tariff reaching 22%, surpassing the highs of the 1930s,” she explains.

The Aberdeen Investments political economist believes that the economic fundamentals remain strong. However, she acknowledges that “our updated baseline political expectations, along with the risk bias in our forecasts, will present headwinds for U.S. economic growth and inflation.”

Finally, according to Enguerrand Artaz, strategist at La Financière de l’Echiquier (LFDE), part of the LBP AM group, “the market scenarios that prevailed at the beginning of the year have been erased.” Artaz explains that the U.S. exceptionalism that had been shining for the past two years—and that consensus expected to continue—is now faltering. “Weighed down by the collapse of the trade balance, driven in turn by a sharp increase in imports in anticipation of tariff hikes, U.S. growth is expected to slow significantly, at least in the first quarter. On the other hand, Europe, a region in which very few investors had any hope at the start of the year, has returned to center stage.”

Implications for Investments

Given this backdrop, Amundi‘s latest Investment Talks report states that “the Trump trades are over, and the market rotation away from major U.S. tech stocks continues.” They explain that despite the recent sell-off, they believe the expected correction in excessively valued areas of the U.S. equity market could continue, leading to further rotation in favor of Europe and China.

“In fixed income, it is crucial to maintain an active duration approach. Since the beginning of the year, we first became more bullish on European duration, and more recently, we have started moving toward neutrality. We have also shifted to a neutral stance on U.S. duration and expect the U.S. 2-10 year yield curve to steepen. Regarding credit, we remain cautious on U.S. high-yield bonds and prefer investment-grade European credit. As our original euro/dollar target of 1.10 approaches, we expect volatility to remain high and believe there is still room for further dollar correction. Overall, we believe it is essential to maintain a balanced and diversified allocation that includes gold and hedges to counter the increasing downside risk in equities,” Amundi analysts state.

Meanwhile, BlackRock Investment Institute highlights that political uncertainty and rising bond yields pose risks to growth and equities in the short term. “We see further upward pressure on European and U.S. yields due to persistent inflation and rising debt levels, although lower U.S. yields suggest markets expect the typical Federal Reserve response to a slowdown. However, we believe that megatrends like artificial intelligence (AI) could offset these drags on equities, which is why we remain positive over a six- to twelve-month horizon,” they indicate in their weekly report.