Once Again, UBS AM Gets Into the Minds of Top Central Bank Leaders With a New Edition of Its UBS Annual Reserve Manager Survey

After gathering the views of 40 monetary institutions, the main conclusion of the report is that geopolitics has displaced monetary policy as one of the most relevant issues of the moment.

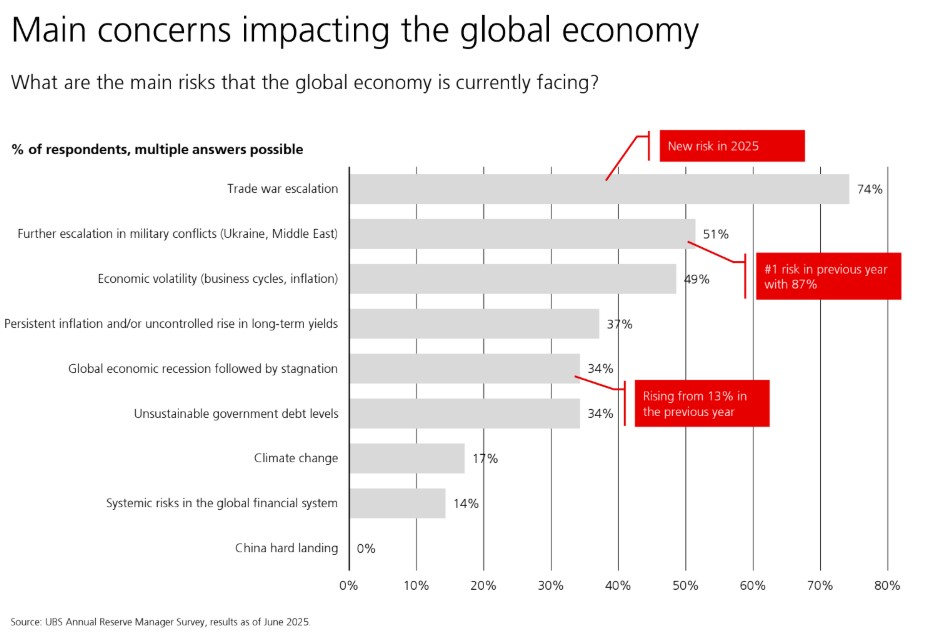

“This year, the shift from monetary policy to geopolitics was palpable. There was much less talk about inflation or interest rate paths, and much more about scenario planning for global disruptions. The widespread concern over a possible resumption of the trade war under a second Trump administration stood out most. Nearly three-quarters of reserve managers identified this as the main global risk, ahead of inflation or rate volatility. That says a lot about current sentiment,” says Max Castelli, Head of Strategy and Advice for Global Sovereign Markets at UBS Asset Management.

According to Castelli, this year’s conversations felt less like forecasting and more like “contingency planning.” “Reserve managers know the playbook has changed: they’re not just reacting to volatility—they’re repositioning for a world where fragmentation is the norm, not the exception,” he notes.

He also acknowledges that what struck him most was the “quiet urgency” with which they are acting. “Reserve managers aren’t panicking, but they are preparing. From FX hedging strategies to liquidity buffers, there’s a clear sense that the coming years won’t look like the last ten. In a context of high uncertainty, there is a marked rise in pessimism among central banks; for instance, they now consider stagflation to be just as likely as the soft landing that was generally expected in last year’s survey,” he states.

Key Findings

In this context, it is notable that 86% of respondents expect that the MAGA agenda (tariffs, deregulation, lower taxes, cheap energy, and DOGE-style cost cutting) will not succeed in boosting the U.S. economy in the long term. Instead, reserve managers believe that several key factors that made the U.S. the preferred destination for international asset allocators may be at risk:

65% believe that the independence of the Federal Reserve is at risk.

47% think there could be a deterioration in the rule of law significant enough to influence reserve managers’ asset allocation decisions.

29% see a risk to the openness of U.S. capital markets.

When Sharing Their View on Economic and Financial Outlooks, Respondents Showed a Notable Increase in Pessimism

40% expect the U.S. headline CPI to be in the 3%–4% range within a year, and more than 80% believe the Fed’s interest rates will also fall within that range during the same period.

When it comes to risks, the most frequently mentioned word is geopolitics, which has now taken center stage in central banks’ concerns, displacing economic issues. Evidence of this shift is seen in the fact that 74% of reserve managers identify an escalation of the trade war as the main risk, followed by a rise in military conflicts (51%).

Implications for Asset Allocation

So how does this translate into asset allocation? According to the survey, reserve managers remain well diversified in public markets, but the trend toward greater diversification appears to have peaked. In this regard, gold continues to show strong demand and is expected to offer the best risk-adjusted returns over the next five years.

Emerging market debt, corporate bonds, and particularly green bonds were also frequently mentioned as assets that central banks plan to incorporate over the next year. At the same time, the trend toward increasing equity exposure is slowing.

Another key data point is that 80% of respondents expect the U.S. dollar to remain the global reserve currency, although there are clear signs of diversification toward other currencies, with the euro being the primary beneficiary.

“The dollar is not favored, but reserve managers are uncertain. There are no true alternatives. Most central banks surveyed expect the U.S. dollar to remain weak, although they remain skeptical about whether this signals the start of a prolonged trend. Dollar weakness is not unprecedented, given the extended period of strength,” notes Castelli.

Sentiment toward the renminbi (RMB) also appears to be improving slightly. In this regard, Castelli adds: “While demand for U.S. assets is more vulnerable, the U.S. dollar is still widely expected to remain the dominant reserve currency (79% of respondents). The euro is seen as the most likely to benefit from macroeconomic and geopolitical shifts over the next five years (74%), followed by the renminbi (59%) and, perhaps surprisingly, digital currencies ranked third (44%).”

Lastly, the survey highlights the trend of digital assets—including cryptocurrencies and stablecoins—which were mentioned as one of the asset classes expected to benefit most from the current geopolitical environment, just after the euro and the renminbi.

Sector Estimates Point to Private Markets Growing From the Current $13 Trillion to Over $20 Trillion by 2030. But Before Then, Investors Must Face a Uncertain Second Half of 2025.

On this shorter-term outlook, leading investment firms have expressed their views in their mid-year outlooks, which agree that alternative assets will continue to make sense in investor portfolios.

For example, in the view of Goldman Sachs AM, private markets, hedge funds, and strategies for hedging against extreme risks can offer alternative paths to resilience, while also providing exposure to themes of persistent and accelerated growth. “In private markets, we continue to expect strong investor demand for private credit, driven by its historically attractive risk-adjusted returns and diversification benefits,” they note.

They also add that for investors needing liquidity or looking to rebalance their portfolios, ongoing innovations in secondary markets are offering new options. “We also believe the current environment will continue to favor alpha generation by hedge funds, while reinforcing the diversification value that these investments have historically provided,” they state.

From M&G’s perspective, they believe the recent recovery in private markets is unlikely to be derailed by recent events, since “the structural growth drivers remain intact and will continue,” they note. They add: “The outlook for private credit is more positive than before, with spreads and demand likely to improve. Private equity could be affected by higher financing costs and a more complex operating environment for investments. The unlisted nature of private markets is likely shielding investors from the worst of short-term market volatility, while preserving the long-term appeal of this asset class,” they emphasize.

Peter Branner, CIO of Aberdeen Investments, and Paul Diggle, Chief Economist of Aberdeen Investments, consider private markets to be a structural opportunity given their “ideal” position amid a falling interest rate environment, an economy that is slowing but not contracting, and a historical undersupply of quality assets in areas such as real estate, infrastructure, and private credit.

Investment Ideas

When it comes to specific ideas, Goldman Sachs AM points out that flexible financing solutions, such as hybrid capital, can help companies with strong fundamentals optimize their capital structures. “In an unpredictable macroeconomic environment, we see opportunities to invest in themes of persistent and accelerated growth. Increased spending on defense and infrastructure in developed markets reinforces the strength of economic security, despite recent short-term volatility in equity markets. Artificial intelligence, the clean energy transition, and the return of industrial production are driving strong energy and electricity demand. We believe more private credit aimed at climate transition will be necessary to expand energy solutions across different countries and use cases,” the firm explains.

According to the asset managers, private credit has been one of the most attractive alternative assets during the first six months of the year and is expected to remain so in the next six. “In private markets, rising financing costs could pose a challenge for riskier, unconventional companies and/or those with long-term cash flows exposed to uncertainty. However, despite the challenges, opportunities may arise for debt-focused specialist investors, along with greater incentive for companies to seek funding from parties more willing to assess their specific conditions,” notes M&G.

For the firm, this is not the only investment idea for the second half of the year—they also believe that real estate may remain relatively unaffected by uncertainty. “While it’s possible, it seems unlikely that a weaker economic or corporate environment would significantly harm the currently strong demand for occupancy. In fact, the limited supply and consistent evidence of rising rental levels suggest that the current real estate recovery is well-founded,” they explain.

In that sense, the two experts from Aberdeen Investments add: “The global direct real estate market appears attractive, with improving occupancy and credit markets, but with limited supply. Portfolio diversification is important in an unpredictable world. With increasingly frequent signs of positive correlation between equities and fixed income—both rising and falling in unison—standard equity and bond portfolios will not provide sufficient diversification.”

On the other hand, M&G warns that not all areas of the private markets universe would be immune to a drop in market confidence, and for private equity, the situation could become more complicated: “If the world resigns itself to higher tariff levels than today, this could have an inflationary effect, making it harder for central banks to cut interest rates as much or as quickly as expected. This would increase financing costs for private equity. The operating environment for companies would also be affected, possibly lengthening holding periods and making exits more difficult.”

Large banks, insurers, and other financial services firms are leading in investment and adoption of generative AI technology compared to companies in other industries. We’re talking about sums that in 2024 reached nearly €22.1 million, and the involvement of 270 full-time employees on average, among those with revenues of at least $5 billion—compared to $17.6 million among their counterparts in other sectors. The 10 largest financial companies analyzed would invest an average of more than $100 million in 2024. This is one of the main conclusions drawn from a recent survey conducted by Bain & Company among 109 U.S. financial services firms.

According to Santiago Casanova, partner in Financial Services at Bain & Company Spain, “Although the sample was conducted in the United States, the macro results are not far from what is happening in the financial sector in other countries, including Spain—especially in terms of productivity gains from the application of generative AI. In any case, smart technology choices alone will not drive the full transformation of the sector. True adoption requires a deep cultural shift. At Bain, we help our clients in the financial sector strategically assess and apply use cases to improve efficiency and customer loyalty, among other factors, and to move forward on the path toward that necessary change.”

Regarding the impact of generative AI on the productivity of the financial services firms analyzed, Bain & Company found that it results in a global average increase of 20%, considering all areas in which it has been used (software development, IT, customer service, marketing, legal department, operations, etc.), as shown in the following table:

Despite the clear positive impact of generative AI implementation, financial services firms remain reluctant to accelerate their pace of adoption due to several issues, such as regulatory uncertainty and concerns over data quality and security. These concerns are more prevalent among financial services firms than in less regulated sectors and cast doubt on the return of the investments made.

“To succeed with AI tools at scale, financial services firms will need to engage in dialogue with regulators and develop deeper expertise at the intersection of regulation, data security, and privacy. This will require more deliberate governance around compliance, task allocation, and individual roles,” explained Casanova.

Firms in the financial sector will also need to attract and develop the right talent. In this regard, nearly 70% of respondents stated that there are talent gaps across all functions related to AI implementation, especially in technical, risk, and compliance areas.

Centralizing and Building: Two Clear Trends

Bain & Company also found that almost half of the financial services firms analyzed fully or partially centralize their AI-related decision-making processes. For companies using a hybrid model, it is common to centralize strategy and governance while decentralizing execution.

Furthermore, when choosing between buying or building their own generative AI solutions, most financial services firms surveyed said they had developed their own solutions across all applications—at a slightly higher rate than in other sectors. Many applications are developed in-house either because commercial versions are not yet ready or because firms want greater control over their solutions. In any case, third-party offerings are becoming increasingly sophisticated and relevant to this highly regulated sector, so the number of companies opting to buy rather than build is expected to grow.

“In general, our analysis suggests that financial services firms have already reaped benefits from generative AI and expect to gain even more. Therefore, they are making significant investments in talent and other resources. In any case, although progress is rapid, we are still in the very early stages of a technology that promises to further improve operations and customer experience,” concluded Santiago Casanova.

Allfunds adds the first funds to its Middle East entity. The strategies, developed in collaboration with Schroders, are designed to enable the seamless distribution of the asset manager’s UCITS funds across jurisdictions, while maintaining regulatory alignment.

“Allfunds is honored to have Schroders as the first partner of its ManCo in the Middle East, reinforcing the longstanding and fruitful relationship between both institutions. This milestone represents our commitment to the region, as well as providing comprehensive fund distribution solutions in the world’s major markets, and demonstrates our ability to navigate complex regulatory environments while delivering value to our clients,” said Yunus Selant, head of MENA at Allfunds.

For his part, Joe Tennant, senior executive director at Schroders, added: “We are very proud to partner with Allfunds to offer three active management solutions in multi-asset, credit, and equities to retail investors in the United Arab Emirates. With over 15 years of presence in the region, this step represents a further commitment to our clients, as we aim to continue contributing to the growth of financial services in the area, placing our clients at the center of everything we do.”

As explained, Allfunds (Middle East) Limited, based in the Dubai International Financial Centre, offers a tailored framework for accessing Middle Eastern markets. Its local presence and regulatory expertise enable fund managers like Schroders to efficiently and compliantly serve onshore retail clients in the UAE. Through this entity, with management companies now operating in both Luxembourg and Dubai, Allfunds provides asset managers with a scalable and compliant platform for global fund distribution, combining local expertise with a unified infrastructure.

WisdomTree has reached a definitive agreement to acquire Ceres Partners, a U.S.-based alternative asset manager specializing in farmland investments. They explain that this transaction marks its entry into private asset markets, starting with the real estate sector and, specifically, farmland. In addition, Ceres benefits from opportunities in adjacent strategic areas with demand for solar energy, artificial intelligence data infrastructure, and water, which are expected to drive faster growth.

According to WisdomTree, this acquisition provides immediate scale and a long-term advantage, bringing approximately 1.85 billion dollars in assets under management across about 545 U.S. farmland properties located in 12 states, mainly in the Midwest. “Ceres has a solid performance track record, with an average annual net total return of 10.3% since its inception in 2007, outperforming farmland benchmarks,” they state.

The manager believes that, as farmland is recognized as one of the largest and most underutilized real asset classes in the United States, there is significant growth potential. In their view, this asset class has historically delivered resilient, inflation-protected returns, and is uncorrelated with traditional equity and fixed income markets. As demand accelerates for private investments that generate income and offer inflation protection, they believe this transaction positions them well to provide differentiated access at an institutional scale. Farmland prices and asset values have increased in the United States in all but nine years since World War II, and Ceres represents a value-added platform in a category with the fundamentals for greater adoption by advisors and institutions.

“Farmland is one of the largest and most underutilized real asset classes in the United States, offering both scale and scarcity. This acquisition expands our leadership in innovative, income-generating investment solutions while strategically accelerating our entry into private asset markets with a scalable, high-quality platform. This reflects our commitment to offering differentiated exposures that deliver long-term value for both clients and shareholders. This strategic acquisition now positions WisdomTree to capitalize on the most significant structural growth opportunities in wealth and asset management today: ETPs, private markets, managed models, and tokenization,” added Jonathan Steinberg, founder and CEO of WisdomTree.

For his part, Perry Vieth, founder and CEO of Ceres Partners, stated: “We are proud of Ceres’ lasting partnerships and legacy with farmers. Joining forces with WisdomTree marks an exciting new chapter for Ceres. For nearly two decades, we have built a differentiated farmland investment platform, grounded in performance, operational expertise, and a deep understanding of U.S. agricultural markets. This partnership brings product innovation, scale, and distribution that will allow us to reach more investors seeking resilient, inflation-protected, income-generating real assets. Together, we are uniquely positioned to capitalize on the next wave of growth in farmland, including solar energy, artificial intelligence data infrastructure, and water, with a shared commitment to innovation and long-term value creation.”

Transaction objectives and details

As part of this transaction, WisdomTree’s goals for 2030 include raising over 750 million dollars in farmland assets by the end of 2030 with fee structures of approximately 1% base / 20% performance, doubling base fee revenue by the end of 2030, increasing performance fee revenue by 1.5 to 2 times—assuming historical performance levels are maintained—and accelerating WisdomTree’s global margin expansion trajectory.

According to the manager, the transaction involves an initial cash consideration of 275 million dollars payable at closing, subject to customary adjustments. “Consideration for future earnings of up to 225 million dollars payable in 2030, subject to a compound annual revenue growth rate of 12–22% measured over five years. Subject to customary approvals, financing, and closing conditions, the transaction is expected to close in the fourth quarter of 2025,” they note.

Finally, they add that this transaction establishes Ceres as a cornerstone of WisdomTree’s long-term strategy to build the next-generation asset management platform, combining structural growth sectors, an innovative offering, and a future-ready product range. “Alongside its current strengths in ETPs, managed models, and tokenization, WisdomTree will offer its clients institutional access to a highly differentiated set of exposures in public and private markets,” they conclude.

Technology is a consolidated theme in investors’ portfolios. In the first half of 2025, the so-called Magnificent 7 experienced a sharp correction at the beginning of the year, followed by an AI-driven rebound that mainly benefited Meta, Microsoft, and Nvidia. In the opinion of Madeleine Ronner, a DWS manager specializing in technology, the investors’ response has been clear: although we have not seen a widespread increase in sensitivity to valuations, investors have become more selective. We discussed how to approach technology investment in our latest interview.

Do you think the perception investors have when investing in technology has changed?

The focus is more on cost discipline, AI-driven efficiency improvement, and tangible growth, especially in areas such as infrastructure, automation, and computing. The market is also more critical of how large-scale AI investments will be monetized, particularly given the high investment-to-sales ratios across the sector. That said, speculative behavior remains present, especially in certain parts of the U.S. technology market, as reflected by the growing number of stocks trading at more than 10 times their market value. From our point of view, this reinforces the importance of focusing on critically important technologies with long-term structural relevance, and not only on short-term growth arguments.

Have investors adjusted their portfolios’ exposure to the technology sector?

There has been a slight shift. ETF flows show a rotation away from the U.S. and, therefore, from large U.S. technology companies, and toward European and diversified exposures. Investors are increasingly opting for broader sector allocation strategies that reduce reliance on a few dominant technology stocks, especially as geopolitical risks rise. However, gross exposure to large technology companies remains high.

Have you adjusted your expectations for this sector’s performance?

Our expectations are becoming increasingly differentiated. While the sector as a whole may no longer deliver the broad outperformance of previous years, certain specific segments—such as cutting-edge AI, custom semiconductors, and mission-critical software—still enjoy strong secular tailwinds. We are cautious in areas with inflated multiples and low visibility but continue to see long-term value in enablers of automation, digital resilience, and computing efficiency.

In today’s context of uncertainty, tariffs, and high valuations, what do you consider the best way to approach technology investment now—ETFs, active management, or thematic investing?

In this environment, active management and selective thematic investing present clear advantages. The macroeconomic and geopolitical context—especially tariffs, supply chain adjustments, and tighter regulation—creates dispersion in the market. An active approach can help avoid overpriced or geopolitically exposed names, while thematic strategies (for example, nearshoring, AI infrastructure, sovereignty) can target specific pockets of opportunity.

Over the past 24 months, investors seem to have focused on AI. Do you consider this an area saturated with investors and funds, or do you believe there is still room to launch new funds and channel investment into it?

AI investment is saturated, but not exhausted. While competition is intense and valuations are high, the underlying innovation cycle is still in its early stages. There is room for differentiated strategies, especially those targeting industrial AI, edge computing, and AI infrastructure. The AI hype is real, but the set of opportunities remains broad. While overall exposure to AI may seem saturated, there is still plenty of room for differentiated strategies focusing on vertical AI applications, AI infrastructure, energy efficiency, or AI governance and security. We believe new funds can succeed if they offer genuine specialization or exposure to undercapitalized segments of the AI stack.

What are the technologies of the future that investors should start considering?

In my opinion, several technology areas stand out as critical for evaluating future investments, especially in the context of national resilience and economic competitiveness. AI remains a dominant force, not only as an independent theme but as an enabling element across all sectors. It is worth highlighting that automation is beginning to extend into traditionally under-served sectors, such as pharmaceuticals and food and beverages, supported by AI-driven efficiencies.

Semiconductor manufacturing and equipment is another area of strategic importance. We are particularly focused on the long-term development of U.S. manufacturing capacity, which aims to reduce dependence on Taiwan and strengthen domestic supply chains. In our case, defense and dual-use technologies are a cornerstone of our strategy, as is cybersecurity, especially as nations prioritize digital sovereignty and the protection of critical infrastructure. The sector continues to evolve rapidly, with growing importance in both the public and private spheres.

We also see attractive opportunities in energy infrastructure and grid modernization, which are essential for energy security and the transition to more sustainable systems. In this area, battery technology is especially promising, with recent advances suggesting transformative potential in energy storage and distribution.

In the current context of uncertainty and tariff wars, which parts of the technology sector are most exposed?

Consumer electronics and automobiles, due to supply chain dependence and specific tariffs, as well as semiconductors, especially those reliant on Asian manufacturing or with significant sales to Asian markets.

What could this mean for investors, and how can they protect themselves against this risk?

To build a resilient and forward-looking portfolio, it is essential to diversify both geographically and across relevant subsectors. Priority should be given to companies that demonstrate strong local production capacity and robust, adaptable supply chains. Moreover, the use of active investment strategies can help avoid overexposure to specific securities or concentrated risks. We have a bottom-up fundamental approach, and in my selection I am currently placing great emphasis on pricing power, as well as strong management teams capable of navigating this volatile and changing environment and addressing supply chain challenges.

One of the latest studies by Vanguard examines the risk of overconcentration in high-cap U.S. stocks and whether, as a result, ETF investors are adjusting the global allocation of their portfolios.

The report reveals that while the market shows a marked tilt toward selected Magnificent Seven companies, Vanguard indicates that advisors may have already adjusted their clients’ portfolios accordingly.

The firm conducted a survey of 1,747 clients, which shows that advisors are already tilting their portfolios toward small- and mid-cap stocks, moving away from large- and mega-cap growth stocks that have experienced a strong rally.

The median among respondents has been overweighting mid and small caps by approximately 10 percentage points above benchmark allocations, which are around 25%.

While advisors appear to be reducing their exposure to large-cap stocks, another critical factor they may be overlooking is the bias toward domestic markets.

Research by Vanguard shows that the median client portfolio has a 75% weighting in U.S. stocks, well above the 63% allocated to American stocks in global benchmark indexes.

That represents an overweight of 12 percentage points, and more than three-quarters of client portfolios show some level of home bias.

Market capitalization indexes risk a greater allocation to a handful of names, which can make exposure seem excessive. Such indexes are arguably the best strategy for holding a representative slice of the broader macroeconomy, but moving away from the highest-returning U.S. companies addresses only one part of a portfolio’s overconcentration source.

Adding more international equities can make portfolios more diversified—a benefit that, according to the study, could prove profitable “if the current valuation gap between U.S. and international stocks normalizes over the long term.”

Donald Trump continues to fulfill his campaign promises. On Thursday, the U.S. president signed an executive order to allow the inclusion of private equity, real estate, cryptocurrencies, and other alternative assets in 401(k) retirement accounts in order “to enable investors to access alternative assets for better returns and diversification,” according to the official statement released by the White House.

The order paves the way for private equity managers and other funds to access the trillions of dollars (American trillions) in Americans’ retirement savings.

“It could open a new and broad source of funding for managers of so-called alternative assets, outside of stocks, bonds, and cash, although critics claim it could also pose an excessive risk to retirement investments,” reported the Reuters agency.

According to Bloomberg, the order is “a big win for industries seeking to tap into some of the approximately $12.5 trillion (American trillions) held in those retirement accounts.”

“The order instructs the Securities and Exchange Commission (SEC) to facilitate access to alternative assets for participant-directed defined contribution retirement plans by reviewing applicable regulations and guidelines,” a White House official stated in the morning under condition of anonymity, according to the cited sources.

The document instructs the Secretary of Labor to reexamine the Department of Labor’s guidelines on fiduciary duties related to investments in alternative assets within 401(k) plans and other defined contribution plans regulated by ERISA. It also instructs the Secretary of Labor to clarify the Department’s stance on alternative assets and the proper fiduciary process associated with offering asset allocation funds that include investments in alternative assets.

Initial Reactions

The new investment options have less stringent disclosure requirements and are generally harder to sell quickly for cash compared to publicly traded stocks and bonds, which most retirement funds rely on. In addition, investing in them usually involves higher fees, Reuters noted.

Many private equity firms are eager for the new source of cash that retail investors could provide after three years in which high interest rates shook their traditional model of buying companies and selling them for profit.

“The entire market cap of the crypto market as a whole is nearly 4 trillion,” Iñaki Apezteguia, a Bitcoin specialist and co-founder of Crossing Capital, told Funds Society. “So the amount of money handled in crypto could triple with this availability of pension funds; it’s a huge advancement,” he added.

The expert clarified that this does not mean all the money would go into crypto. “But globally respected analysts, among them Ray Dalio,” he stated, “say that about 15% of a portfolio’s capacity should be allocated to investing in Bitcoin and cryptocurrencies. So we’re talking about a possible injection of massive institutional capital and allowing many people nearing retirement to access diversification of the money tied to their retirement. Bitcoin further legitimizes its place as a global store of value.”

“The approval of the Genius, Clarify, and anti-CBDC laws, the White House’s crypto report, the appointment of key figures in regulatory agencies who are sympathetic to the financial world and have a pro-crypto outlook, and even his own approach of accumulating cryptocurrencies through his companies, both Bitcoin and Ethereum — Trump’s new order is in line with all of this,” said Apezteguia, referencing his campaign announcements.

In fact, the final lines of the official statement announcing the executive order include references to Trump’s promise to make the United States the “world capital of cryptocurrencies,” emphasizing the need to embrace digital assets to boost economic growth and technological leadership.

Not an Immediate Effect

For plan sponsors, the order does not immediately change existing regulations. Jaret Seiberg, a financial services policy analyst at TD Cowen Washington Research Group, said in a note published by CNN that “agencies will still have to develop new rules. That could take until 2026.”

For their part, employers will have to conduct their own due diligence before offering new investment options. Lisa Gómez, former Assistant Secretary of Labor for Employee Benefits Security, told CNN: “It’s going to be more complicated.”

Private market assets have traditionally been excluded from 401(k) plans due to high fees, lack of transparency, and longer lock-up periods, CNBC noted.

After liberation day, we saw a sharp market correction and a wave of new ETFs with more balanced weighting and improved exposure to certain U.S. stocks and this is because, in the opinion of Sefian Kasem, Global Head of ETF & Indexing Investments Specialists at HSBC AM, the appeal of ETFs lies precisely in their dynamic nature—ideal for these times of uncertainty. We spoke with him about the role of these vehicles in portfolios and about the ETF phenomenon in our latest interview.

How is all this market instability and uncertainty affecting the creation of new ETF products and strategies?

They can be used to quickly increase or decrease risk by investors or to gain access to specific markets or strategies. There is now much more innovation. Active ETFs, for example, offer investors access to asset classes for those seeking the beta of a specific market with an additional alpha component and low tracking error. As markets become increasingly volatile and fragmented, we are more frequently seeing tactical adjustments within portfolios. The great flexibility they provide is precisely what is driving much of the current innovation in the sector, by incorporating new strategies that allow investors to access different sources of risk and return. In the realm of traditional ETFs, concern about concentration in certain stocks within U.S. benchmark indices has also driven innovation around capping methodologies (such as equal weighting) to mitigate concentration risk in the indices.

In this regard, where are ETFs and index strategies heading? How is innovation achieved in this part of the business?

The major shift has been the transition toward increasingly offering exposure to asset classes and access to specific investment strategies. Within the ETF space, you now have the opportunity to invest in strategies that use active stock selection from a bottom-up perspective, whether in a discretionary sense or in a quantitative and systematic sense, where a rule-based methodology is used for stock selection—as is the case with our active ETF range. We’ve spoken in terms of investment strategies, but we also need to consider the evolution of product features, as it is increasingly common for traditional index funds to provide access to strategies through the launch of ETF share classes that operate under the same umbrella. ETF issuers are showing dynamism in this regard, and we are increasingly seeing these hybrid structures in the market, which allow investors to access specific markets or strategies in the usual way through index funds, while also offering access to investors who wish to invest in ETFs, perhaps with a shorter time horizon. They can do this because there is a class that is an ETF, and it is available alongside the traditional non-listed share classes. In short, we are seeing ETF product providers increasingly offer market access to a broader range of asset classes and strategies through more innovative methods.

In the ETF market, we’re seeing strong growth in active ETFs in Europe, but in the U.S., this market is already more developed. What can the European industry learn from how the active ETF segment has grown in the U.S.?

I believe the key lesson from the U.S. experience is the innovation and infrastructure that have been developed there. Historically, they have been pioneers in the creation and growth of the ETF market, including the variety of asset classes offered and the strategies embedded within the structures. The U.S. has gone through a trial phase that proves active investment strategies can be successfully integrated within an ETF. This shows there is enormous potential for growth in Europe, but that doesn’t necessarily mean the same types of strategies will appeal to European investors in the same way they do to Americans. The needs of European investors are different, due to the nature of the investor base. Europe will naturally develop its own range of products demanded by clients, depending on their needs at any given time and tailored to the different jurisdictions.

Considering that active ETFs in the U.S. enjoy a number of advantages not present in Europe, what growth prospects do you see for the active ETF market in Europe? What opportunities could this offer asset managers and, in particular, your firm?

From the U.S. perspective, there are some advantages in that sense, such as a regulatory framework that is a bit more open to innovation, but I believe that mindset is changing in Europe. There is increasing innovation happening in Europe, so there is plenty of room for ETF issuers to develop products that are relevant to their target market. We fully understand that certain concepts are especially relevant to the European public, such as capital-protected solutions, sustainable investing, etc. The creation of products that meet the needs of European investors is something that will likely accelerate from now on, so there may be some divergence from the U.S. as more local innovation takes place. In many respects, I believe much of the innovation is transferable, so we will see many concepts that have taken root in the U.S.—for example, options-based ETFs, such as buffer ETFs, and other types of structured solutions—gradually become more prevalent in Europe.

In which other markets do you see growth potential for the ETF business, both traditional and active?

There is enormous potential for ETFs to become tools used for asset allocation across a wide variety of jurisdictions, in both developed and emerging markets, given how easily they can be used to build and manage portfolios. And this is not only for short-term investors looking for quick access to liquid markets, but also for long-term investors building strategic asset allocations with a 10- to 15-year investment horizon. ETFs can offer them access to different sources of risk premia in both public and private markets, as well as sectoral, factor-based, and thematic strategies. ETFs are becoming a much more important part of portfolios not only in the U.S. and Europe, but also in other jurisdictions—emerging markets, the Far East, the Middle East, Latin America, etc. They are highly relevant tools being used by virtually all types of investors.

HSBC Asset Management has strengthened its presence in the ETF business in recent years. What role do these vehicles play within the firm’s overall strategy?

They play a very important role, as our passive and quantitative equity business is under the same investment leadership (CIO), which greatly helps from an innovation standpoint. In that sense, there is a lot of collaboration and knowledge transfer between the two. The active ETF strategies we’ve launched in the market are considered a natural complement to the range of traditional ETF investment strategies we offer to investors. We will continue to innovate and explore how to use the ETF structure to provide investors with access to selected asset class exposures and strategies—and we have a few more surprises in store for them this year.

The new tariffs from the Trump Administration have come into effect, with a general minimum of 10%, amid renewed social media messages, threats, and moves that add noise to the current context of uncertainty. Markets are absorbing these fluctuations with relative calm, and European stock markets opened the day in positive territory—for example, futures on the STOXX Europe 50 index are pointing to an increase of approximately 0.3%, while in Asian markets, the main indices closed the session with gains.

What does the new “tariff map” look like? According to the summary from Banca March, three main groups can be identified. “On one hand, there are countries in a sort of truce with the U.S., such as Mexico and China, awaiting the outcome of negotiations. Secondly, we have countries like Japan, the United Kingdom, Vietnam, the EU, among others, that have already reached preliminary agreements with the American giant, although in many cases, key details of those pacts are unknown, and in cases like Japan or the EU, negotiations are ongoing. Lastly, there is the rest of the countries which, starting today, will face a tariff ranging from 10%—if they have a trade deficit with the U.S.—up to levels of 50%, in cases like Brazil and India,” they explain.

In this new tariff environment, central banks have become more cautious. “Both the Fed and the ECB have kept official interest rates unchanged. The apparent stability of labor markets and the potential inflationary pressures caused by U.S. tariffs are leading central banks to act with caution. In July, the U.S. administration concluded several tariff agreements with key trading partners (Japan, Eurozone). Although not all details have been negotiated, tariffs around 15% are lower than feared, which has supported risk assets. In the process, equities have once again outperformed fixed income,” highlights Alex Rohner, Fixed Income Strategist at J. Safra Sarasin Sustainable AM.

Chips and Semiconductors

In the past 48 hours, several announcements have come from Trump, adding more percentages and tension to the tariffs that are now in force. In particular, he has announced that he will impose a 100% tariff on chip and semiconductor imports to force their production within the country. “We are going to apply a very high tariff on chips and semiconductors. But the good news for companies like Apple is that if they manufacture in the United States or are fully committed to manufacturing in the United States, no charges will apply to them,” the president stated during an event in the Oval Office.

The Republican, who this week indicated his intention to announce tariffs on these high-tech components, said that “a 100% tariff will be applied to all chips and semiconductors entering the United States.”

According to the analysis by Amadeo Alentorn, Head of Investments in the Systematic Equity area at Jupiter AM, “U.S. technology continues to rely heavily on international supply chains,” as “most advanced semiconductor manufacturing is concentrated in East Asia, especially in Taiwan and South Korea.” Alentorn explains that major U.S. companies like Apple and Nvidia rely heavily on Taiwan for chip manufacturing, even though they design them domestically.

For some experts, this is a clear message to China. U.S. and Chinese delegations concluded a third round of negotiations in Stockholm at the end of July without reaching a definitive agreement, but with a joint intention to extend the tariff truce set to expire on August 12. “Tensions between the U.S. and China are escalating into a full-scale trade war, with technology at its core. President Trump demands that all chips used in critical industries be Made in America. In response to Washington’s tightening of export controls and domestic origin requirements, China is intensifying audits, fines, and new data localization rules. It is suspending licensing and slowing down customs clearance for goods related to semiconductors. Supply chain bottlenecks are multiplying,” adds the expert from Jupiter AM.

Meanwhile, according to experts, the Asian giant is designing a new trade map to diversify its exports within Asia. Its main targets are Southeast Asian countries with friendlier ties to the U.S., such as Vietnam, Thailand, and Indonesia, where results are already visible.

In fact, according to analysis by Crédito y Caución, Chinese exports to the U.S. plummeted in April, when the American tariffs came into effect, with a drop of $9.3 billion in goods exports compared to the previous year. At the same time, Chinese exports to Asia increased by $14.8 billion. This is a trade strategy that aims not only to minimize the impact of tariffs. As Bert Burger, economist at Atradius, explains, “Chinese manufacturers are also setting up production facilities in Southeast Asia to take advantage of local benefits.” These advantages include lower wages and tax incentives.

Pharmaceutical Sector

“We will initially impose a small tariff on pharmaceutical products, but within a year—a year and a half at most—it will rise to 150%, and then to 250%, because we want pharmaceutical products to be made in our country,” stated Trump just 48 hours ago. According to experts, companies in this sector face dual pressure: on one hand, tariffs; on the other, the restructuring of the healthcare system in their largest and most profitable market, the United States. “Pharmaceuticals are included in the trade agreement between the EU and the U.S., which has mitigated some concerns in the sector. However, they were excluded from the recent 39% tariff imposed by the U.S. on Swiss imports. A specific update on pharmaceutical product tariffs is still pending,” say Alexandra Ralli and Simon Lutier, Equity Analysts for the Healthcare Sector at Lombard Odier.

According to Lombard Odier experts, it is important to put this into context: the U.S. healthcare system is undergoing a phase of political reform, with expected changes in production, regulation, and pricing. Furthermore, President Trump has urged major pharmaceutical companies to lower prices, adding pressure to an already strained sector. “Global pharmaceutical giants are trading at a discount compared to their historical averages, reflecting investor caution amid regulatory and political uncertainty.

While the healthcare sector is not among our top picks, we see potential in certain pharmaceutical or biotech companies with strong product pipelines. Swiss pharmaceutical companies could rebound if the tariff framework becomes clearer. In the view of Marie de Mestier, Head of Large-Cap Equity Fund Management at Crédit Mutuel AM, this sector—traditionally considered a safe haven in times of instability—is now in a volatile situation and clearly exposed to political risk. “Donald Trump’s policies will have cross-border repercussions. Possible changes in pricing, regulation, and supply chains, along with increased competition, will force European companies to adapt in order to remain competitive despite U.S. policies. In fact, European pharmaceutical companies generate nearly 50% of their sales in the United States, but not all the drugs they sell are manufactured there. With rising protectionism, the challenge will be to produce more locally, which is why many European pharmaceutical firms have already announced massive investments in the United States,” they emphasize.

India: Energy and Geopolitics

The other major announcement from Trump was the imposition of additional 25% tariffs on India in retaliation for its purchase of Russian oil, bringing the total tariff on Indian imports to 50%. According to analysts, India, the third-largest oil importer in the world, has taken a neutral and pragmatic stance on the war in Ukraine, shifting from importing less than 2% of its oil from Russia to more than one-third, making Moscow its main supplier.

“One of the additional factors negatively impacting the market was President Donald Trump’s decision to impose a 25% tariff on products from India. The measure responds to accusations that the Asian country continues to buy Russian oil, sparking new trade tensions amid an already fragile international relationship,” point out the Financial Markets Analysts for LATAM at XS.com.

In their opinion, despite downward pressures, physical market data offered a bullish signal. “The market is closely watching details on the implementation of U.S. sanctions. Traders are looking to understand which sectors will be affected and whether the measures will have a real effect on global oil supply. At the same time, there is growing concern over a potential production increase by the OPEC+ alliance—which includes Russia—which could offset any supply loss caused by the sanctions,” they add.