A recent study by MainStreet Partners, a firm specialized in sustainable investment and part of Allfunds, warns that the European Union is facing serious difficulties in turning its ambitious green agenda into a real competitive advantage.

The report identifies overlapping regulations, administrative burden, and lack of support for key sectors such as electric vehicles as the main barriers. According to Daniele Cat Berro, the firm’s Managing Director, these obstacles are weakening Europe’s role in the ecological transition and undermining its ability to lead in global sustainability.

In the industrial sphere, the company highlights setbacks compared to the Asian market. Despite the EU’s goals to reduce emissions from new cars by 55% by 2030 and eliminate combustion engines by 2035, more than 20% of electric vehicles sold in Europe in 2023 were of Chinese origin. In addition, the battery value chain is increasingly controlled by non-European players, while local industrial projects suffer from delays and limited funding.

“The transition to electric vehicles is strategic, but without a strong industrial base, it risks triggering deindustrialization in regions dependent on the automotive sector. Stronger support for local production is necessary,” said Cat Berro.

In the financial sphere, MainStreet Partners points out that the sustainable investment regulatory framework has reached a level of complexity that hampers market confidence. The combination of SFDR, CSRD, and CSDDD has resulted in high costs and compliance challenges, especially for small and medium-sized enterprises.

As a consequence, Europe recorded net capital outflows in ESG products for the first time in the first quarter of 2025, according to Morningstar data. The European Commission responded by introducing the Omnibus Directive, which includes postponements and adjustments to reporting obligations, but MainStreet warns that the measure is insufficient without a clear and agile execution strategy.

The firm has also expressed concern over the new regulation on ESG rating providers, which in practice will favor large global operators, most of them non-European. This, they note, jeopardizes the continent’s strategic autonomy in an emerging sector.

“The commitment to climate goals must be maintained, but with an approach that prioritizes regulatory clarity, industrial capacity, and international competitiveness,” Cat Berro concluded.

Gold’s Relentless Climb: Central Banks, Geopolitical Risk, and U.S. Economic Conditions Fuel Bullish Outlook

Gold continues its upward trajectory. It was one of the best-performing assets in portfolios last year, and this year follows the same trend—with new record highs included. All signs point to this momentum continuing. Historically, the second half of the year tends to favor gold prices. Since 1971, average returns during this part of the year have outperformed those of the first half, reinforcing the bullish outlook described by analysts and underpinned by fundamental drivers.

Chris Mahoney, Investment Manager for Gold and Silver at Jupiter AM, is clear in his outlook for the precious metal: “One of the determining factors will undoubtedly be the activity of central banks.” He explains that official purchases tend to intensify in the second half of the year and cites a recent survey by the World Gold Council, which reveals that 43% of monetary authorities intend to increase their reserves in the coming months.

While he does not rule out a moderate correction—especially considering that gold hasn’t seen a drop of more than 10% in over two years—he believes the structural support remains solid.

Another factor Mahoney sees as increasingly influential on gold prices is the U.S. economic cycle. “There are growing signs that the U.S. economy is in a late-cycle phase, which could lead the Federal Reserve to ease monetary policy sooner than expected. If this expectation materializes, it would act as an additional catalyst for gold,” he says.

At the same time, geopolitical tensions remain a key driver. The recent trade truce between the U.S. and China could deteriorate, with negative effects on the global economy and additional pressure on interest rate policy. According to the Jupiter AM expert, “a resurgence of tensions would likely favor gold as a safe-haven asset.”

He also highlights the political context in the U.S.: Fed Chairman Jerome Powell‘s term ends in less than a year, and President Donald Trump—a vocal advocate of low interest rates—has expressed his intention to nominate a successor aligned with that view. Therefore, “any announcement in this regard could significantly shift expectations around rates and inflation, which are fundamental drivers of gold performance,” Mahoney concludes.

Bank of America shares a similar view. The firm recalls that gold reached an all-time high after Independence Day but later gave up those gains. To continue rising, the precious metal needed “a new trigger,” and the U.S. budget could be that bullish driver—“especially if deficits increase.”

The macroeconomic context encourages greater diversification of reserves; central banks should allocate 30% of their reserves to gold. Retail investors are also buying gold, and ongoing macro uncertainty and rising global debt levels remain supportive factors.

In short, the conditions that have driven gold’s recent strength appear likely to persist, according to Bank of America: the structural U.S. deficit; inflationary pressures from deglobalization; perceived threats to the independence of the U.S. central bank; and global geopolitical tensions and uncertainty. That is why the firm has raised its long-term price target for gold by 25% to $2,500 (real).

Ian Samson, Multi-Asset Fund Manager at Fidelity International, also maintains a positive view on gold. He believes bull markets for gold “can last for years” as it continues to provide diversification even when bonds do not, retains its privileged status as a “safe haven,” offers protection against inflation and loose economic policies, and benefits from structural trends.

Samson acknowledges that, given a macro base of economic slowdown in the U.S. or even a potential stagflationary environment in the coming months, he remains positive on gold’s prospects. He argues that the Federal Reserve is ready to cut interest rates despite inflation lingering around 3%, and that tariffs will likely keep prices elevated.

Additionally, the impact of tariff policy and a slowing labor market will also trigger a weak growth environment, in the expert’s view. This combination should support gold, which competes head-to-head with a weakening dollar as a safe haven and store of value. “We’ve never seen this scale of uncertainty and change surrounding tariff policy, and the effects are still unfolding. Furthermore, the size of the U.S. budget deficit raises concerns about monetary debasement, which further strengthens the long-term case for gold.”

Meanwhile, the structural case for investing in the precious metal remains strong, and numerous countries—including China, India, and Turkey—are structurally increasing their gold reserves in an effort to diversify away from the dollar, as gold offers diversification without the credit risk inherent in foreign currency reserves.

Moreover, gold supply remains highly constrained, meaning even a small increase in portfolio allocation could move the needle: “For example, if foreign investors were to decide to move a portion of the $57 trillion they currently hold in U.S. assets, gold would be a more than likely destination.”

For now, Samson says he is “comfortable” maintaining gold in his multi-asset portfolios through a combination of passive instruments that directly track gold prices and a selection of gold mining stocks.

The intentions of U.S. President Donald Trump to influence the Federal Reserve have recently taken another turn with the controversial removal of Fed Governor Lisa Cook, who has already taken the case to court. This pressure from Trump has not gone unnoticed by experts, who, generally speaking, believe that the consequences of this unprecedented situation are unpredictable.

For example, Clément Inbona, fund manager at La Financière de l’Échiquier, is clear that President Trump wants to have the Federal Reserve “in his grasp.” The expert explains that the objectives of this governmental interference stem from Trump’s desire to influence the institution in order to lower interest rates and potentially reduce the cost of U.S. government borrowing—“widely in deficit and heavily indebted—even at the risk of facing dire consequences.”

At this point, Inbona turns to history to detail the consequences of such actions: the Turkish example “is eloquent,” he states, recalling that the country’s president, Recep Tayyip Erdogan, brought the Turkish central bank under his control in 2019 with immediate economic effects: rampant inflation and a large-scale depreciation of the Turkish lira, which amplified the rising cost of imports. “These consequences could loom over the U.S. economy if the Fed were taken over by MAGA America.”

The La Financière de l’Échiquier manager recalls that the Fed’s independence is the result of a progressive achievement. Initiated in 1935 with the separation from the Treasury, it was consolidated in 1951 with the end of public debt monetization—a tool widely used during World War II to finance the war effort and, later, reconstruction. “However, independence does not mean completely escaping government pressure, as shown by Presidents Johnson and Nixon in the 1960s and 1970s,” he notes.

Still, Inbona believes that, in any case, “Trump’s efforts to get the Fed in his grasp matter little,” as the renewal schedule of the institution’s members “works in his favor”: in 2026 he will appoint a new chair, “which will increase his influence” over the institution.

At Edmond de Rothschild Asset Management, they share this perspective. The removal of Governor Cook is interpreted by the firm as an intensification of Trump’s efforts “to take control of the Fed,” a decision that investors understand as a greater likelihood of a more accommodative monetary stance. This environment, they argue, partly explains the drop in interest rates. In addition, the dollar fell again, especially against the euro, due to rising concerns over the Fed’s credibility, according to Edmond de Rothschild AM.

For Tiffany Wilding, economist at Pimco, Trump’s unprecedented decision regarding Cook “eclipsed” Powell’s message in Jackson Hole about a possible rate cut in September. “This event could have consequences for the perception of the Fed’s independence, although the potential impact on Fed policy (and interest rates) is far from clear,” Wilding states.

The expert argues that “this issue goes far beyond Cook” and believes that the accusations “carry political overtones, given the public pressure campaign that Trump has been conducting for a year to push for lower interest rates.” At this point, she explains that although Cook’s replacement would not directly change the voting majority of the Federal Open Market Committee (FOMC), her position is important because it could shift the voting majority of the Board of Governors on issues such as the appointment of Federal Reserve Bank presidents.

“Each regional Reserve Bank board nominates a president for a five-year term, but the final approval lies with the Fed’s Board of Governors. The Board renews the appointment of all presidents at the end of February every five years (in years ending in ‘1’ or ‘6’) in what is usually a procedural vote,” Wilding explains, noting that when the next vote is held in February 2026, “a Board majority favorable to Trump could, at least in theory, veto or reshape the leadership of the regional banks for the next five years.”

She also notes that five regional Reserve Bank presidents are voting members of the FOMC, with one-year rotating terms—except for the New York Fed president, whose position is permanent—“so politically driven changes to their list could affect policy decisions over time.”

There is no precedent for any of this, she notes, but the expert recalls that some legal scholars argue that “a majority of four members of the Fed’s Board of Governors could remove regional bank presidents outside the normal five-year reappointment cycle, though they would have to justify the reason for dismissal.” In short, this would enter “uncharted territory.”

Cook has already taken the case to court. And now, several scenarios are possible. If she does not obtain a court order against the president’s decision, the position could remain vacant while the case proceeds through the courts. But if the court confirms Cook’s dismissal for cause, Senate confirmation of those appointed to the vacant governor positions remains uncertain, despite the Republican majority.

“Key Republican senators have quietly expressed their refusal to appoint a partisan Fed chair, and we could extrapolate this to the Fed board in general,” says the Pimco expert, who believes the renewed attention on the Fed could make it harder for the Senate and the Senate Banking Committee to confirm a Fed nominee who appears too political, too partisan, or too moderate. “Any confirmation process could be difficult and lengthy, potentially leading to a prolonged period of vacancies on the Fed’s Board of Governors,” she concludes.

There is also uncertainty, according to Wilding, about what individual Board governors would do—even if appointed by Trump and confirmed by the Senate—when faced with the reappointment of regional bank presidents. According to Bloomberg, based on a Freedom of Information Act request, current Fed governors Christopher Waller and Michelle Bowman abstained from voting on the 2022 appointment of Austan Goolsbee as president of the Chicago Fed (which was still approved by a majority). However, abstention “has far fewer consequences than overturning decades of precedent and voting to remove a sitting bank president.”

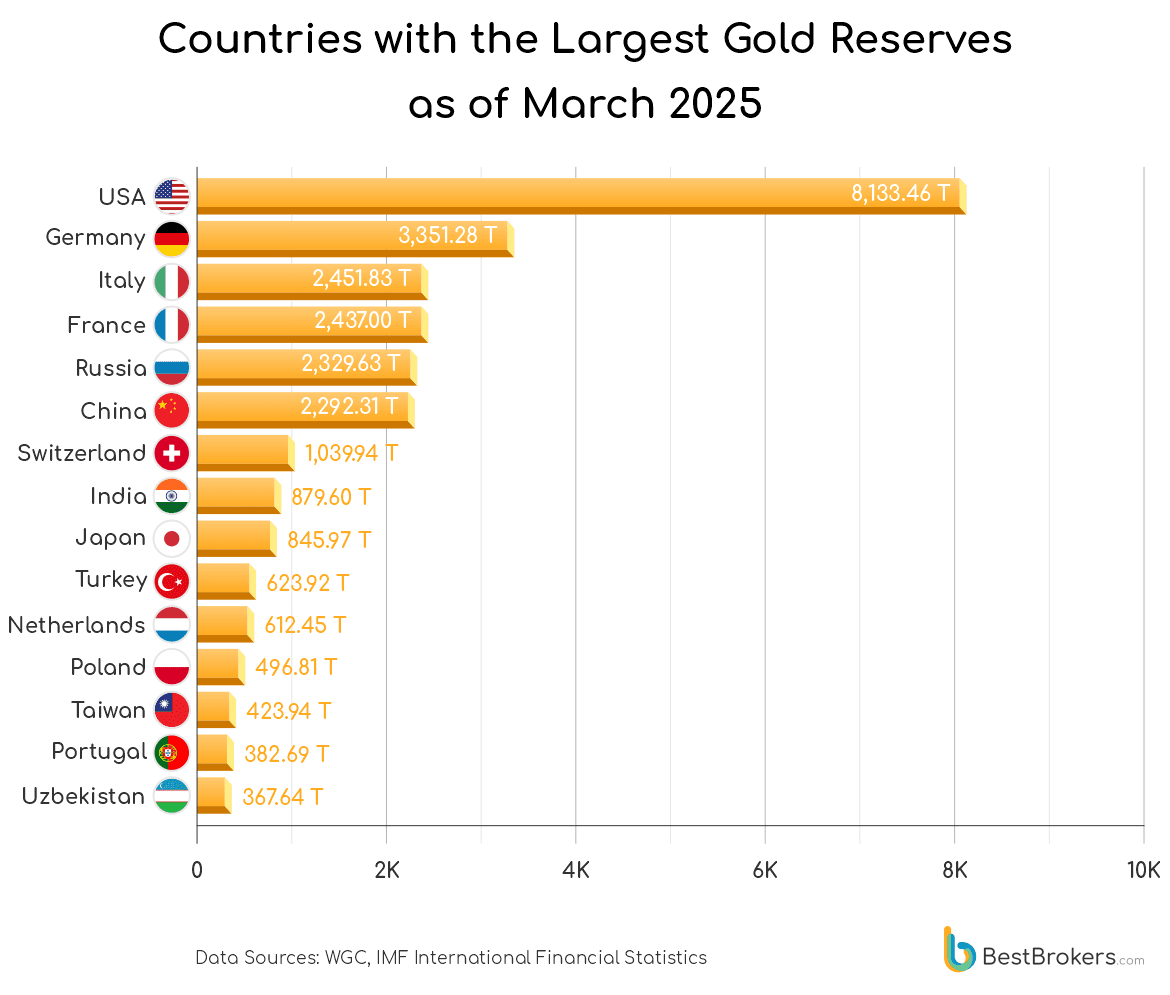

The price of gold began to rebound last year, in a context where both central banks and investors sought safe-haven assets amid rising geopolitical tensions and economic uncertainty. While many took advantage of the situation to buy, others opted to sell, capitalizing on high prices. The BestBrokers report, based on data from the World Gold Council for the first quarter of 2025, reveals that Poland maintained its leadership as the world’s top buyer by acquiring 48.6 tonnes of gold between January and March 2025.

According to the report, this figure represents nearly half of its total purchases in 2024, which amounted to 89.5 tonnes. The Polish central bank, Narodowy Bank Polski (NBP), has significantly accelerated its accumulation of reserves, most likely motivated by its geographic proximity to the conflict between Russia and Ukraine. At the end of the first quarter, Poland held a total of 496.8 tonnes of gold, valued at $53.1 billion based on the May 9 price, which stood at $3,324.55 per ounce.

The document also highlights Azerbaijan, which in March added 18.7 tonnes of gold to the State Oil Fund (SOFAZ), after having made no purchases in the previous two months. As a result, its reserves reached 165.3 tonnes, representing 25.8% of its assets. China, for its part, bought 12.8 tonnes during the first quarter of the year, a lower figure than the 15.3 tonnes acquired in the last quarter of 2024. Although it could surpass the 44.2 tonnes accumulated last year if it maintains this pace, its purchases still fall far short of the record 224.9 tonnes reached in 2023.

Kazakhstan, which led gold sales in 2024, changed its strategy in 2025 and resumed accumulation with 6.4 tonnes purchased in the first quarter. In contrast, Uzbekistan led the sales with a net divestment of 14.9 tonnes, after buying 8.1 tonnes in January and selling 11.8 in February and 11.2 in March. It was followed by the Kyrgyz Republic and Russia, with sales of 3.8 and 3.1 tonnes, respectively.

Meanwhile, the United States remains the country with the largest national gold reserve, with 8,133.46 tonnes in the form of bars and coins. However, Switzerland stands out for having the highest per capita gold holdings: 115.19 grams per person, equivalent to 3.70 troy ounces or 37 small 0.1-ounce coins.

If Poland maintains its current pace, it could double its 2024 purchases, further strengthening its position as the world’s leading gold buyer. In contrast, Turkey has fallen to sixth place in the 2025 ranking after adding only 4.1 tonnes in the first quarter, representing a decrease of 15.5 tonnes compared to the previous quarter. India shows a similar trend, with just 3.4 tonnes purchased between January and March, a drop of 19.1 tonnes from the end of 2024, placing it in seventh position.

In addition to Poland, Azerbaijan, China, and Kazakhstan, other countries that increased their reserves in the first quarter of 2025 were the Czech Republic (5.1 tonnes), Turkey (4.1), India (3.4), Qatar (2.9), Egypt (1.4), and Serbia (0.9).

As for sellers, the landscape has shifted significantly compared to 2024. Countries such as the Philippines, Kazakhstan, and Singapore, which led sales last year, are no longer on the current list. In their place, Uzbekistan tops the sales, followed by the Kyrgyz Republic, Russia, Mongolia, and Germany, the latter two with more moderate divestments of approximately 200 kilograms each.

The French Prime Minister, François Bayrou, has called for a vote of confidence on his fiscal plans, which include €44 billion in budget cuts. The vote is scheduled for September 8, and Bayrou has stated that he will resign if it does not pass. Since this announcement, the main French opposition parties have been quick to declare that they will not support the prime minister’s proposals.

Markets have also reacted to Bayrou’s plans. Notably, the spread between German and French 10-year bonds surged to nearly 80 basis points. Although still below the highs recorded at the end of 2024, it is worth noting that the spread is now higher than that of Spain or Greece. In other words, France pays more than those countries on newly issued debt.

The consequences will extend to other areas. For example, John Taylor, Head of European Fixed Income at AllianceBernstein, expects credit rating agencies to update their ratings on France in the coming months, starting with Fitch on September 12. “There is a high probability that at least one agency will downgrade France’s rating to a single A in the coming months,” the expert predicts, noting that September usually sees an increase in sovereign supply, “which has historically had a negative seasonal impact on European spreads.”

Some agencies have already shared their views on the matter. One such case is Scope Ratings, which states clearly: “political obstacles hinder fiscal consolidation.” The firm points out that political gridlock “undermines” the projected reduction of the budget deficit to 5.4% in 2025 and 4.6% in 2026, from 5.8% of GDP in 2024. Instead, their base case is that France’s budget deficit will only decline to 5.6% of GDP in 2025 and 5.3% in 2026.

The agency also notes that net interest payments are expected to rise to approximately 4% of government revenue in 2025 from 3.6% in 2024, in line with Belgium (AA-/Negative, 3.8%) but still below Spain (A/Stable, 5.2%) and the United Kingdom (AA/Stable, 6.6%). Similarly, yields on 10-year French government bonds have risen moderately but steadily to 3.5%, converging with those of Spain and Italy (BBB+/Stable).

While this is not their base case, Scope Ratings believes that a favorable outcome in the vote of confidence would be a significant step forward and would support short-term budgetary commitments. However, they warn that political uncertainty ahead of the municipal elections in March 2026 and the presidential elections in April–May 2027 “remains a key credit challenge.”

Therefore, they conclude that France’s medium-term fiscal outlook “remains constrained by a fragmented political landscape, growing polarization, and an electoral calendar that hampers political consensus on economic and fiscal reforms.”

Credit ratings, along with quantitative tightening and the additional bond supply the market must absorb, “could contribute to increased volatility in the coming weeks,” according to Taylor.

The AllianceBernstein expert acknowledges that the firm had already anticipated this political development as “inevitable,” given the difficult budget negotiations France must conduct with a fragmented parliament. As a result, they have maintained an underweight position in French sovereign debt in their global and European accounts, “as the market seemed to have underestimated this risk.” However, he believes the risk will remain isolated to French sovereign and agency debt, thus reiterating his overweight position on the euro.

Meanwhile, Mitch Reznick, Head of Fixed Income for London at Federated Hermes Limited, says the market is reacting to concerns that one of the widest budget deficits in Europe may not be reversed; the prospect of a wave of strikes and protests; and general economic disruption. “Under these conditions, it’s very difficult to imagine that French risk assets can outperform in the short term,” he argues, while explaining that the rise in French bond yields “could open some interesting medium- to long-term investment opportunities for strong credit profiles.”

The political situation in France has forced Schroders strategists to rethink their strategy. This is revealed by Thomas Gabbey, Global Fixed Income Manager at the firm. “We expect political tension to return in the second half of 2025, as we anticipate that the 2026 budget negotiations will spark inter-party disagreements and lead to new elections.” With this in mind, Gabbey began underweighting French sovereign bonds in portfolios starting in June and increased that underweighting in early August, “as we did not believe the market was sufficiently pricing in the political or fiscal risk of French bonds.”

One of the key themes Gabbey admits to having worked with this year has been signs of European recovery, driven mainly by the manufacturing sector and supported by a sharp shift in German fiscal policy toward increased infrastructure spending. “Renewed political uncertainty in France could derail this European growth rebound, and it’s something we’ll continue to monitor for any sign of impact on business confidence,” the expert explains.

Julius Baer points out that, as has occurred in the past, France’s debt affordability remains relatively high, “given that the country has benefited from a very long period of very low financing costs and a long average debt maturity.” A situation which, in the firm’s view, “should limit the potential for a massive sell-off of French government bonds.” Nevertheless, Julius Baer experts do not foresee a quick resolution to the current political dilemma and therefore believe that “the additional spread on French public debt is not going to disappear so easily either.”

Meanwhile, at Bank of America, they see opportunities in this situation: given the political risk premium, they consider it attractive to hold CAC volatility and protective puts on certain French stocks, “based on a proxy hedging analysis, in case concerns over a government collapse intensify.” In fact, they see room not only for CAC volatility to continue rising relative to the German DAX, but also for the spread itself to widen further “if history is any guide.”

Geopolitical Factors Like Military Conflicts, Sanctions, and Long-Term Shifts Such as Trade Barriers Are Increasingly Influencing Investment Decisions, according to findings from the report “Friendvesting: The New Architecture of Investment in a Fractured World”, developed by Economist Impact and sponsored by Xtrackers from DWS.

The document reveals that equity and fixed income, in particular, react quickly to political events, forcing fund managers and investors to rethink old assumptions about risk and return. In this context, the report’s authors propose friendvesting—investing alongside geopolitical allies with shared economic and strategic interests—as a core strategy for institutional investors in 2025.

What Is the “Friendvesting Era”?

“Institutional investors no longer treat geopolitical conflict as background noise. The war in Ukraine and the Middle East, tensions in the Taiwan Strait, and tariff threats from Washington have turned geopolitics into a central variable in portfolio construction. The firm’s survey of 300 global investors shows a shift: from viewing geopolitics as episodic to treating it as structural—redefining the destination of capital flows, their allocation, and management. The emerging pattern is friendvesting: aligning capital with jurisdictions where geopolitics is less intrusive and avoiding—or at least protecting against—any rising risks,” the report states.

Friendvesting begins with geography: two-thirds of investors state that it is the main factor influencing the geopolitics of their portfolios. For real assets (ports, pipelines, or real estate), location is crucial. But in most cases, investors are less concerned about where an asset is recorded than about its exposure to geopolitical risks that move across geographic borders. In equities, the question isn’t whether a company is listed in Boston or Beijing, but whether it depends on suppliers, clients, or operations in volatile jurisdictions. The new geography of capital is defined less by proximity than by dependency.

Asset Classes and the Shape of Risk

If geography defines the boundaries of friendvesting, asset allocation gives it shape. Different assets carry geopolitical risk in different ways. Some transmit it openly; others conceal it until problems emerge. Bonds depend on legal enforceability; stocks reveal operational entanglements; and real assets are vulnerable due to their physical immobility. For investors, the task is to understand how each asset absorbs and transmits geopolitical tension. This is made more difficult by the unreliability of traditional risk metrics when international conflicts arise.

According to the report, geopolitical risks are unevenly distributed across sectors. Some industries lie closer to dividing lines and are vulnerable to sanctions and regulatory barriers. The study prioritizes technology, energy, and defense. However, the specific boundaries of exposure vary by country. Investors ask what each sector represents—how it is perceived, politicized, and potentially weaponized.

The Bureaucratization of the Unpredictable

Quantifying geopolitical risk remains difficult, which is why nearly half of investors cite forecasting uncertainty as their main challenge. Sanctions and tariffs are hard to model, and wars break out without warning. Institutional responses vary: some firms create cross-functional risk committees; others outsource to consulting firms staffed by former diplomats. Hybrid investment models—combining passive exposures with dynamic hedging—are gaining ground, offering both stability and responsiveness.

Throughout August, markets have observed various meetings between the United States, Russia, and the EU aimed at ending the war in Ukraine. This peace negotiation process on the Ukrainian front is expected to carry both economic and financial consequences.

Kim Catechis, Chief Strategist at the Franklin Templeton Institute, explains that for Europe, these negotiations are possibly “the last chance to avoid a war for the survival of the European model,” while for the United States, “it seems that policy direction is solely in the president’s hands and, as such, is not clearly defined for the external observer.”

On this point, Catechis has the impression that, for U.S. President Donald Trump, “reaching a peace agreement is more important than the structure of that agreement, which implies that the sustainability of any peace may not be a priority.” He even considers that “it could be that the President of the United States loses interest and decides to withdraw.”

Still, he notes a few clear considerations. First, that a clear resolution is unlikely in the short term—within six months—and that “an unstable truce” is more probable, along with “little clarity about the outcome of this process.”

On the economic front, Catechis states that the European defense sector is in the early stages of a multi-decade investment boom that will not be affected by any peace agreement in Ukraine. He also believes that Europe’s focus on electrification will continue “regardless of the circumstances, purely for security reasons.” Even in a potential peace scenario where Ukraine does not become another Belarus, it is likely that Europeans will launch a “mini Marshall Plan to rebuild the country,” which would mean “a significant opportunity for local and European companies.”

As for the United States, Catechis does not see clearly how companies will be affected throughout this process. The expert recalls already known figures: $600 billion over three years from the EU, $100 billion from Ukraine—plus revenues from critical mineral extraction. “It’s likely that the majority of these sums will go toward purchasing Patriot missile batteries, but there is a production capacity issue: Raytheon plans to increase production to 12 per year,” the expert notes.

Nicolás Laroche, Global Head of Advisory and Asset Allocation at Union Bancaire Privée (UBP), is clear that a possible peace agreement in Ukraine could have significant implications for various asset classes and sectors, “though this will depend on the details.”

The expert focuses on the future of sanctions on Russian energy. He believes that any easing of sanctions “would further accelerate and expand” the global oil and gas oversupply scenario, which would put downward pressure on energy prices and “benefit European economies such as Germany.”

Among the side effects of a new energy landscape would be a continuation of the disinflationary trend in Europe, which would improve consumer confidence and corporate margins, and trigger “a sector rotation from defensive sectors to more cyclical ones.” Additionally, Laroche believes that since a peace deal would also be an additional catalyst for further dollar weakness, “domestic and cyclical companies in Europe would likely find a catalyst for a revaluation, given their undemanding valuations.”

In summary, “Europe may be tactically attractive,” but Laroche acknowledges that long-term structural growth and political challenges persist, which makes U.S. equities more appealing to him for generating sustained returns.

Lastly, a peace agreement could tilt the European yield curve upward, according to the UBP expert, due to expectations of higher fiscal spending, “a positive environment for the European financial sector.”

Nicolas Bickel, Head of Investment at Edmond de Rothschild Private Banking, also sees opportunities in Europe in the event of a ceasefire in Ukraine. “While caution must prevail, if peace is achieved, it would act as a catalyst for stock markets, particularly for European equities,” the expert states, adding that a definitive ceasefire would result in lower energy prices, which would support European manufacturing activity and industrial company stocks.

However, Bickel does not rule out that the prospects of de-escalation in Ukraine could affect the European defense sector, “as a reduction in deliveries of ammunition and combat vehicles to Ukrainian forces is expected.” Additionally, a more favorable geopolitical context could also put downward pressure on gold prices.

Nonetheless, he believes the correction in both assets would be short-lived, as they benefit from long-term supportive factors: European defense is backed by the €500 billion ReArmEU program, while gold is supported by increased demand from emerging market central banks, which are reducing their exposure to the U.S. dollar in favor of the precious metal.

“At Edmond de Rothschild, we believe that the ongoing negotiations could act as an additional catalyst for European equities, alongside existing factors such as lower ECB interest rates, Germany’s infrastructure plan, and the stabilization of confidence in Europe,” says Bickel, who nonetheless prefers to be cautious. He advises against “drawing hasty conclusions, especially regarding the reconstruction of Ukraine.”

Thomas Hempell, Head of Macro and Market Research at Generali AM (part of Generali Investments), takes a more cautious stance. He acknowledges that hopes for a ceasefire or peace agreement between Russia and Ukraine could provide moderate support for the euro/dollar exchange rate, “as falling oil and gas prices would reduce Europe’s energy import bill.”

However, he points out that energy costs have already moderated and supply has not been disrupted, so he sees it as “unlikely that the negotiations will have a significant impact on the currency market, as they will be overshadowed by the Federal Reserve’s monetary policy.”

On the other hand, he believes that the prospects of reconstruction efforts, to be carried out in the event of a peace agreement, could to some extent benefit the eurozone economy, thereby strengthening European risk assets. However, he observes that the path to a peace deal “remains fraught with significant obstacles,” and given that Russian President Vladimir Putin still holds the advantage on the battlefield, “he has many incentives to keep buying time.”

The euro features prominently in the outlook of François Rimeu, Senior Strategist at Crédit Mutuel Asset Management, in the event of a peace agreement in Ukraine. The expert expects the euro to appreciate. He recalls that at the time of the invasion of Ukraine in February 2022, the euro was trading around $1.15, before falling below parity in October of that year. “A reversal, probably not of the same magnitude, seems to be the most likely scenario,” forecasts the expert, who also considers that the prospect of peace may have already partly contributed to the single currency’s rebound over the past six months.

Many defined contribution pension plans are not convinced that their participants are on the right path to securing sufficient income during retirement and believe that reversing this situation will take several decades, according to a new report by the Thinking Ahead Institute, a global organization dedicated to investment analysis and innovation at WTW.

The Global DC Peer Study 2025, conducted by the Thinking Ahead Institute, brought together 20 of the leading defined contribution pension plans from the APAC, Americas, and EMEA regions. Collectively, these funds manage more than $2.2 trillion in assets, including both public pension funds and private retirement systems.

According to its findings, 60% of the experts surveyed indicated that the main concern for defined contribution pension plans over the next decade is ensuring adequate income during retirement.

These concerns are particularly evident in regions where minimum contribution levels are low or where auto-enrolment systems lead participants to believe they are saving enough without making additional contributions. Some respondents emphasized the need to focus on the adequacy of retirement savings—beyond just coverage or participation—as a key issue for future government reforms.

Although many plans already offer gradual retirement transition paths, many members in the retirement phase continue to make late decisions with a tactical rather than strategic approach. Some of them are exploring collective defined contribution schemes or hybrid models that combine flexibility with sustainable income, though such cases remain rare.

The study also revealed that alternative investments now represent, on average, 20% of pension plan allocations, equaling for the first time the allocation to bonds. Equities, meanwhile, make up the remaining 60%. This shift, though quiet, reflects a significant evolution in the investment strategies of defined contribution plans, especially in mature markets such as Australia. Despite the challenges that private markets pose in terms of governance and communication, this move reflects the growing conviction that long-term returns must be maximized, given the limited effectiveness of traditionally bond-heavy portfolios.

A recurring issue among the plans analyzed is the concern that current lifecycle designs are underperforming, especially due to overly conservative asset allocation in the early stages of accumulation. Some plans are considering dynamic risk budgets that adjust over time or the use of leveraged equities for younger cohorts to improve long-term outcomes.

Others are reevaluating decumulation strategies altogether, seeking to better align them with members’ evolving capacity to take on risk. Additionally, the concept of liability-driven defined contribution, similar to defined benefit schemes, has been proposed as a potential future design alternative.

“In many parts of the world, defined contribution systems are now the dominant pension model. However, they remain relatively young and have not reached full maturity, which presents challenges such as income adequacy in retirement, participation rates, and contribution levels,” says Tim Hodgson, co-founder of the Thinking Ahead Institute.

In his view, as the defined contribution system matures, there is a growing focus on the decumulation phase and on lifelong, integrated solutions. “Some countries are further along in this process than others. Most defined contribution plan participants have several decades to secure an adequate pension. However, there are only two fundamental ways to improve retirement adequacy: increasing contributions and generating higher long-term investment returns,” he adds.

According to his analysis of the report, there is a growing consensus that current lifecycle designs in defined contribution plans may be missing out on return opportunities, particularly due to insufficient risk-taking in the early accumulation phase. “However, in the most essential aspect of retirement saving, further progress is needed. Maximizing returns is crucial, but it has limits.

In many markets, most savers need to increase their contributions during the accumulation phase. While financial education may help, it will ultimately be up to governments to determine whether contributions to defined contribution plans are truly sufficient to ensure a dignified retirement for all future pensioners,” Hodgson notes.

In conclusion, Oriol Ramírez–Monsonis, Head of Investments at WTW, emphasized that “Spain is at a crucial moment to consolidate its defined contribution pension plans, considering that only about 25% of workers participate in complementary private systems—approximately 15% in individual plans and 10% in collective plans. We have the opportunity to incorporate best practices observed globally to design a system that ensures long-term sustainable pensions, focusing on strengthening savings capacity and optimizing risk management.”

U.S. President Donald Trump announced the dismissal of Federal Reserve Governor Lisa Cook over alleged irregularities in obtaining mortgage loans. This unprecedented decision could test the limits of presidential power over the independent monetary policy body if challenged in court, according to Reuters.

Trump stated in a letter addressed to Cook—the first African American woman to serve on the Fed’s governing board—that he had “sufficient grounds to remove her from office” due to Cook’s declaration in 2021, in documents related to separate mortgage loans on properties in Michigan and Georgia, that both properties were primary residences in which she intended to live.

The U.S. president accused Cook in the letter of having engaged in “deceptive and criminal conduct in a financial matter” and said he no longer trusted her “integrity.”

“At a minimum, the conduct in question demonstrates the kind of negligence in financial transactions that calls into question her competence and reliability as a financial regulator,” he said, asserting his authority to dismiss Cook under Article 2 of the U.S. Constitution and the Federal Reserve Act of 1913.

Cook’s Response

Cook responded in a statement emailed to journalists via attorney Abbe Lowell’s law firm, saying that Trump “has no legal grounds or authority” to remove her from the post to which she was appointed by former president Joe Biden in 2022. “I will continue performing my duties to support the U.S. economy,” the statement from Cook read.

Lowell, for his part, stated that Trump’s “demands lack any proper process, basis, or legal authority. We will take all necessary steps to prevent this attempted legal action.”

Questions about Cook’s mortgages were first raised last week by the director of the U.S. Federal Housing Finance Agency, William Pulte, who referred the matter to Attorney General Pamela Bondi for investigation.

Although Fed governors’ terms are structured to outlast any given president’s term—and Cook’s runs until 2038—the Federal Reserve Act allows for the removal of a sitting governor “for cause.”

This provision has never been tested by presidents who, particularly since the 1970s, have largely taken a hands-off approach to the Fed in order to preserve confidence in U.S. monetary policy.

Legal scholars and historians say the web of issues that could arise in a court challenge would include questions related to executive power, the Fed’s unique and quasi-private nature and history, and whether Cook’s actions constituted grounds for removal.

Trump’s Pressure

Trump has repeatedly criticized Powell for not lowering interest rates, although he has stopped short of threatening to fire him from a post that, in any case, ends in just under nine months.

Last week, his attention turned to Cook, whose removal would allow Trump to select his fourth nominee to the Fed’s seven-member board, including Governor Christopher Waller, Vice Chair for Supervision appointed during his first term, and the pending nomination of Council of Economic Advisers chair Stephen Miran to a currently vacant seat.

Cook took out the mortgages in question in 2021, when she was an academic. A 2024 official financial disclosure form lists three mortgages in Cook’s name, two of them for personal residences. Loans for primary residences may carry lower interest rates than mortgages for investment properties, which banks consider riskier.

Reaction

U.S. President Donald Trump announced the dismissal of Federal Reserve Governor Lisa Cook over alleged irregularities in obtaining mortgage loans. This unprecedented decision could test the limits of presidential power over the independent monetary policy body if challenged in court, according to Reuters.

Trump stated in a letter addressed to Cook—the first African American woman to serve on the Fed’s governing board—that he had “sufficient grounds to remove her from office” due to Cook’s declaration in 2021, in documents related to separate mortgage loans on properties in Michigan and Georgia, that both properties were primary residences in which she intended to live.

The U.S. president accused Cook in the letter of having engaged in “deceptive and criminal conduct in a financial matter” and said he no longer trusted her “integrity.”

“At a minimum, the conduct in question demonstrates the kind of negligence in financial transactions that calls into question her competence and reliability as a financial regulator,” he said, asserting his authority to dismiss Cook under Article 2 of the U.S. Constitution and the Federal Reserve Act of 1913.

Cook’s Response

Cook responded in a statement emailed to journalists via attorney Abbe Lowell’s law firm, saying that Trump “has no legal grounds or authority” to remove her from the post to which she was appointed by former president Joe Biden in 2022. “I will continue performing my duties to support the U.S. economy,” the statement from Cook read.

Lowell, for his part, stated that Trump’s “demands lack any proper process, basis, or legal authority. We will take all necessary steps to prevent this attempted legal action.”

Questions about Cook’s mortgages were first raised last week by the director of the U.S. Federal Housing Finance Agency, William Pulte, who referred the matter to Attorney General Pamela Bondi for investigation.

Although Fed governors’ terms are structured to outlast any given president’s term—and Cook’s runs until 2038—the Federal Reserve Act allows for the removal of a sitting governor “for cause.”

This provision has never been tested by presidents who, particularly since the 1970s, have largely taken a hands-off approach to the Fed in order to preserve confidence in U.S. monetary policy.

Legal scholars and historians say the web of issues that could arise in a court challenge would include questions related to executive power, the Fed’s unique and quasi-private nature and history, and whether Cook’s actions constituted grounds for removal.

Trump’s Pressure

Trump has repeatedly criticized Powell for not lowering interest rates, although he has stopped short of threatening to fire him from a post that, in any case, ends in just under nine months.

Last week, his attention turned to Cook, whose removal would allow Trump to select his fourth nominee to the Fed’s seven-member board, including Governor Christopher Waller, Vice Chair for Supervision appointed during his first term, and the pending nomination of Council of Economic Advisers chair Stephen Miran to a currently vacant seat.

Cook took out the mortgages in question in 2021, when she was an academic. A 2024 official financial disclosure form lists three mortgages in Cook’s name, two of them for personal residences. Loans for primary residences may carry lower interest rates than mortgages for investment properties, which banks consider riskier.

Reactions

It remains unclear how events will unfold from here, as Trump has stated the dismissal is effective immediately and the Federal Reserve’s next meeting is scheduled for September 16–17.

President Trump’s decision caused a movement in the U.S. fixed income yield curve, as yields on two-year bonds—sensitive to short-term monetary policy expectations—fell sharply, while yields on ten-year bonds—sensitive to inflation risks—rose significantly.

The market reaction reflects expectations that the Fed could lower interest rates, but at the cost of its commitment to control inflation.

Some firms have already weighed in on Trump’s decision to fire Cook. For example, economist and Fortuna SFP founder José Manuel Marín Cebrián commented that Trump is establishing “true state capitalism” in the U.S., “with a focus against the central bank.” He stated that “Powell’s days are numbered,” adding that Trump has refrained from dismissing him before his term ends but is “actively preparing his replacement” and even “plans to announce the next Fed chair before Powell’s term ends in May to gain time.”

It remains unclear how events will unfold from here, as Trump has stated the dismissal is effective immediately and the Federal Reserve’s next meeting is scheduled for September 16–17.

The most anticipated event of the week, the central bank symposium held this weekend in Jackson Hole (Wyoming), did not disappoint. In the most highly awaited speech, Jerome Powell, Chair of the Federal Reserve, signaled a potential interest rate cut, which would be the first under the Trump administration.

Commenting on Powell’s remarks, Richard Clarida, Global Economic Advisor at PIMCO, noted that the presentation of the revised monetary policy framework “did not disappoint markets, nor did it surprise Fed watchers,” as the U.S. central bank “appears to be on track to lower short-term interest rates, albeit with a cautious approach.” He considers the changes to the policy framework “sensible and well communicated,” while also highlighting “the Fed’s unwavering commitment to its mandate.”

For his part, Nabil Milali, Multi-Asset and Overlay Manager at Edmond de Rothschild AM, emphasized that before the conference, Powell faced the dual risk of disappointing investors hoping for a shift toward more accommodative policy and undermining the central bank’s credibility by appearing to yield to political pressure from U.S. President Donald Trump. However, the expert believes Powell struck “the difficult balance of opening the door to a rate cut at the September meeting, without at the same time fueling doubts about the Fed’s independence,” through two actions: generally well-measured communication and clear reasoning for future moves.

Milali pointed out that Powell stated that despite recent statistics suggesting an acceleration of inflation in both goods and services, he still considers tariff-related inflationary pressures to be only temporary. Additionally, he noted that the labor market is in a “particular situation,” marked by a decline in business demand as well as a drop in the supply of workers, meaning the unemployment rate “is not yet at alarming levels.”

Even so, the expert highlighted that although Powell’s remarks sparked strong risk appetite across asset classes—as evidenced by the narrowing of high-yield spreads and gains in U.S. equity prices—“the Fed’s decision remains heavily dependent on upcoming inflation data and, above all, employment figures, the latter being more than ever the true arbiter of U.S. monetary policy.”

Meanwhile, Bret Kenwell, U.S. investment analyst at eToro, acknowledged that prior to the symposium, markets were pricing in roughly a 75% probability of a U.S. interest rate cut in September. “Those odds should rise significantly following Chair Powell’s comments in Jackson Hole,” he said, explaining that investors got the response they were hoping for when Powell stated that current conditions “could justify an adjustment to our [restrictive] stance.”

However, Kenwell is also aware that the Fed is in a “difficult position,” with rising inflation and signs of deterioration in the labor market. “As economists have observed in the most recent data, the labor market can change quickly—a risk the Fed is highly aware of,” he noted.

Kenwell explained that if the Fed cuts rates too much or too soon, “it risks stoking the fire of inflation.” Conversely, if it moves too late or too mildly, “it risks deeper deterioration in the labor market and, consequently, the economy.” He concluded that “this delicate balance is precisely why the Fed finds itself in a difficult position.” That said, he has no doubt that once inflationary pressure affects employment, “the Fed is likely to step in to prevent further weakness in the labor market,” and that “it is unlikely the committee will stand by idly if we see further labor market weakness.”

The issue of Federal Reserve independence loomed in the background. In fact, Luke Bartholomew, Deputy Chief Economist at Aberdeen, believes that “the elephant in the room in Jackson Hole was the Trump administration’s attacks on the Federal Reserve.” At this point, he recalled that Powell emphasized the importance of monetary policy independence, but the expert is convinced that “Trump’s influence over central bank decisions is likely to increase from here.”

According to Bartholomew, “all signs point to the Senate attempting to appoint Stephen Miran to the Fed before September, where he would likely vote in favor of even more aggressive stimulus than the currently expected 25 basis points.” He also considers it possible that if the administration succeeds in removing Lisa Cook from her post, “another seat would open up.” Consequently, the Aberdeen economist stated, “Powell’s authority could begin to erode in the coming months, with markets paying increasing attention to the preferences of his potential successor. This could make it harder to anchor inflation expectations in a context of rising prices and add pressure on long-term Treasury yields.”

The Taylor Rule Under Debate

Beyond Powell, the most relevant contribution to the conference came from a presentation by Emi Nakamura, professor at the University of California, Berkeley, according to Karsten Junius, Chief Economist at J. Safra Sarasin Sustainable AM. In her speech, Nakamura explained why the Taylor Rule has performed poorly since 2008 and why it should not be strictly applied going forward—the Taylor Rule suggests that interest rates should rise more than proportionally to inflation.

Nakamura explained why and under what circumstances that is not necessary, allowing central banks to disregard certain potentially temporary shocks. A key factor, as the expert recalled, is how well-anchored inflation expectations are, “which in turn depends on the credibility of the central bank.” In her remarks, she warned that “the high degree of credibility is due in part to the Fed’s strong track record, but also to institutions such as central bank independence. These are valuable assets that can be destroyed much faster than they were built.”