Bank of America has published its first global fund manager survey of the year, reflecting a somewhat positive sentiment, particularly regarding the U.S. dollar and equities. However, the survey also reveals nuances that convey a cautious outlook, especially toward Europe, as well as concerns about inflation and monetary policy.

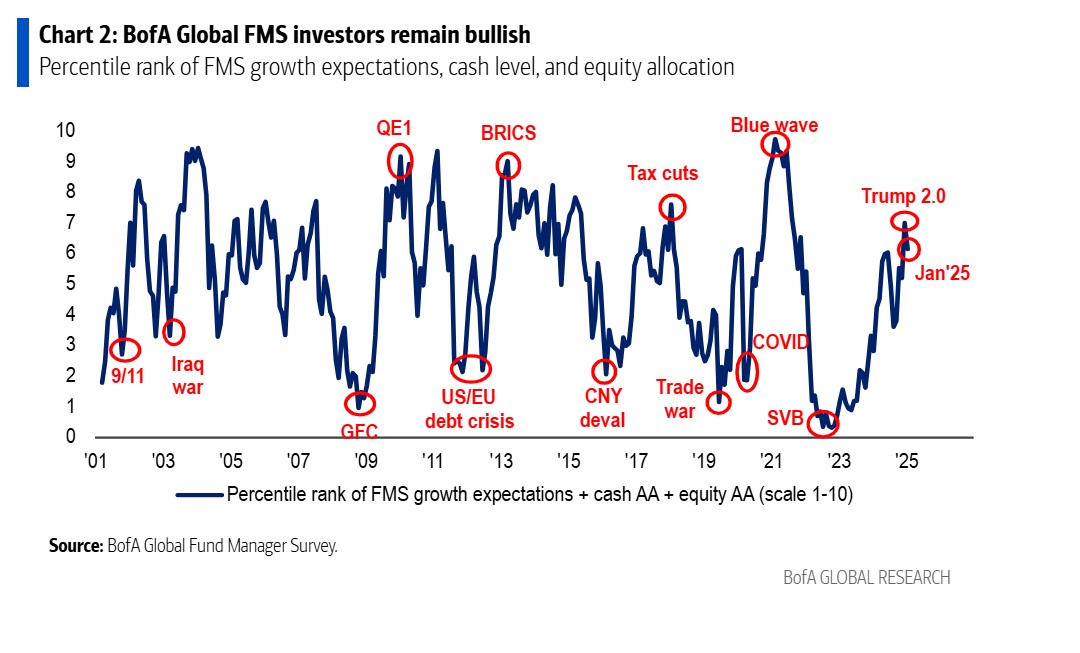

“Our broader sentiment measure from the FMS survey, based on cash levels, equity allocation, and global growth expectations, dropped from 7.0 to 6.1 in January, indicating that some of the ‘excess’ seen in the December 2024 FMS has dissipated. Cash levels in the FMS remained unchanged in January at 3.9%, the lowest level since June 2021. This marks the second consecutive month with a ‘sell’ signal based on the FMS cash rule since 2011. In the 12 previous instances when this ‘sell’ signal was triggered, global equity returns were -2.4% in the following month and -0.7% in the three months after the signal was activated,” the institution notes in its survey.

The most optimistic takeaway from managers is that institutional allocation to equities remains high: 41% of FMS survey investors hold an overweight position in global equities, though this has declined from the 3-year high of 49% recorded in December.

The Nuances

However, retail enthusiasm has waned in early 2025. Furthermore, in this January survey, global growth expectations fell to a net -8% from 7% in December, and optimism declined for both the United States and China.

“Global growth expectations remain moderate, but the percentage of macroeconomic investors anticipating a boom is the highest since April 2022. Inflation expectations are at their highest level since March 2022, and the probability of a ‘no landing’ scenario has increased (38%) at the expense of ‘soft landing’ (50%) and ‘hard landing’ (5%) scenarios,” BofA indicates.

When it comes to risks, the survey reveals that 41% of respondents cite inflation, which could lead the Federal Reserve to raise rates, as the biggest “tail risk,” followed by a trade war with recessionary effects.

A notable statistic is that 79% of investors expect the Federal Reserve to cut rates in 2025, while only 2% anticipate an increase. In fact, the FMS survey shows that investors, entering the first week of Trump 2.0, are most positioned for announcements related to selective tariffs (49%), immigration cuts (20%), and universal tariffs.

“When asked which development would be considered the most bullish for risk assets in 2025, respondents pointed to an acceleration in China’s growth (38%), followed by rate cuts by the Federal Reserve (17%) and AI-driven productivity gains (16%),” the report adds.

Asset Allocation

According to BofA’s interpretation of the January survey results, investors remain optimistic about the U.S. dollar and equities. Conversely, they are pessimistic about nearly everything else. This is evident in the largest underweight in bonds since October 2022 and the low cash levels of 3.9%. “However, if January’s concerns about Trump’s tariffs and messy bonds prove unfounded, asset allocation will remain tilted toward risk, allowing lagging assets to recover,” the institution states.

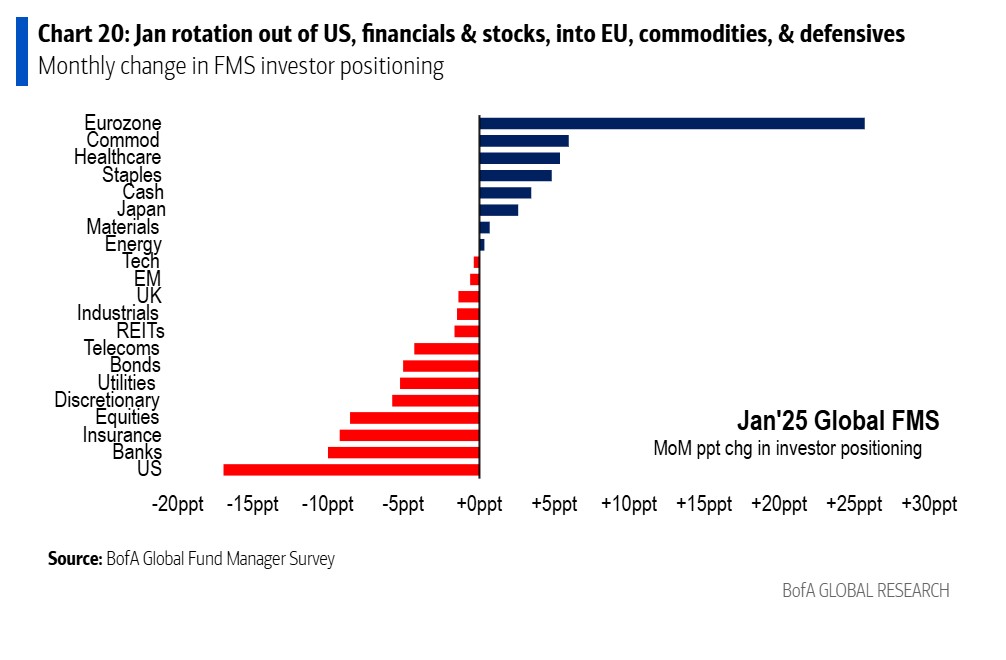

Looking at the asset allocation of fund managers, 41% are overweight equities, compared to an underweight of 6% in commodities, 11% in cash, and 20% in bonds. Notably, January saw a significant rotation into European equities—from a 22% underweight to a net 1% overweight—and out of U.S. equities, from 36% to just 19%. Additionally, global FMS investors rotated back into large caps over small caps and growth over value.

Specifically, investors increased their allocation to the eurozone, commodities, and defensive sectors (healthcare and consumer staples) while reducing their allocation to the U.S., financials (insurance and banks), and equities. According to the survey, investors are most overweight equities, banks, and the U.S., while they are most underweight bonds, the U.K., and energy.

The world is experiencing a new environment marked by a cycle of interest rate cuts by the major central banks in developed markets, as well as in emerging regions. According to experts, over the past quarter, most monetary institutions have adopted a more cautious stance.

The best example of this is the Fed, which has once again shifted its focus to inflation, as economic activity has remained strong while disinflation has stalled. “The Fed maintains its data-dependent approach and is beginning to shift its attention to the labor market. We believe labor market conditions could shape the path of its future policy decisions. Similarly, the Bank of England and the European Central Bank also cut interest rates by 25 basis points in the third quarter of 2024, emphasizing data dependency without precommitting to any specific interest rate trajectory,” explain experts from Capital Group.

According to Invesco in its outlook for this year, rates remain generally restrictive in major economies but are easing. “On the one hand, the Fed is likely to remain neutral by the end of 2025, but improved growth prospects may delay rate cuts. On the other hand, European central banks are easing their policies, with relatively weaker growth than the U.S.,” they note.

Divergences in Monetary Policy

This reality brings us to a key conclusion: yes, we are in a cycle of rate cuts, but there will be noticeable divergences in the monetary policies of the major central banks. In fact, Capital Group believes that this divergence will play a significant role in the coming months.

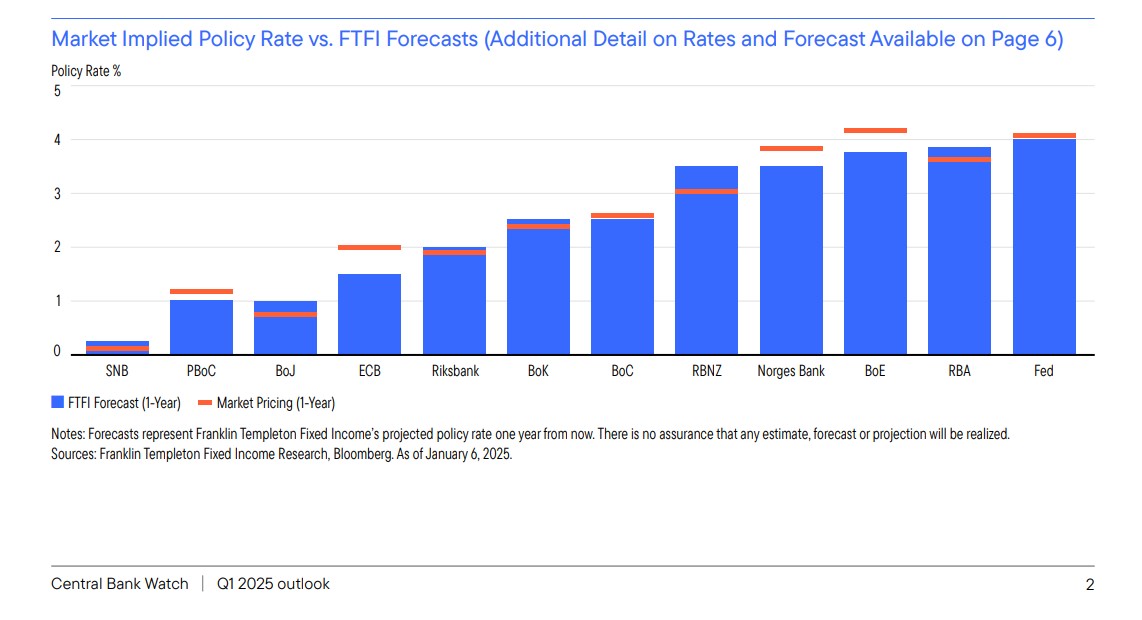

This is reflected in the Central Bank Watch report, prepared by Franklin Templeton, which reviews the activity of G10 central banks, plus two additional countries (China and South Korea), along with their forecasts.

According to the report, the Fed’s shift in strategy has refocused its attention on inflation, as economic activity has remained robust while disinflation has stalled. “The policies of the newly elected president are also likely to influence the Fed’s interest rate projections, which currently only anticipate two cuts in 2025. Across the Atlantic, the European Central Bank and the Bank of England are observing insufficient growth but remain cautious about the future interest rate path, as domestic and geopolitical uncertainties remain high,” the report states.

“Monetary policy divergence is likely to remain a prominent theme in the coming months. The Bank of Japan remains the exception among developed markets, as it has embarked on a rate hike cycle to end an era of negative interest rates. We maintain a relatively cautious stance regarding Japanese rates, as the central bank may make further policy adjustments in response to potential currency pressures. In Europe, the trajectory of monetary easing could depend on the weight policymakers place on downside growth risks compared to the pace and progression of wage pressures and services inflation,” Capital Group experts emphasize.

Another conclusion from the Franklin Templeton report is that “most central banks have become more cautious than they were a quarter ago.” According to their analysis, while the Bank of Canada cut its benchmark rate by 50 basis points in December, this may be its last significant move. “The Riksbank also seems to be taking a more neutral stance, and we believe the Reserve Bank of New Zealand will need to implement fewer cuts than the market currently anticipates. Meanwhile, the Swiss National Bank and the People’s Bank of China remain the most dovish,” the report highlights, noting the behavior of other key monetary institutions.

Lastly, the document underscores that some central banks face a set of dilemmas. “We believe the Norges Bank will lower rates, likely in the first quarter, followed by the Reserve Bank of Australia in the second quarter. Both were among the last to join the easing trend. Meanwhile, the Bank of Japan is expected to continue raising rates gradually in 2025. However, we believe the rigidity of inflation gives the central bank ample room to adopt a more aggressive stance,” the report concludes.

Jupiter Asset Management has announced that the investment team and assets of Origin Asset Management, a global investment boutique based in London, were transferred to Jupiter on January 21, 2025. This integration follows the acquisition announcement made on October 3, 2024.

According to the firm, this addition strengthens its presence in the strategic institutional client channel and enhances its capabilities in emerging market equities, while also expanding its expertise in other multiregional equity strategies. The team, led by Tarlock Randhawa, includes Chris Carter, Nerys Weir, Ben Marsh, and Ruairi Devery-Kavanagh. As noted by Jupiter AM, the team’s solid track record is based on an investment process that combines a quantitative asset selection approach with proprietary algorithms and rigorous qualitative analysis.

Following the announcement, Kiran Nandra, Head of Equities at Jupiter, stated: “Origin is the latest example of Jupiter’s ability to attract highly successful investment talent with strong commercial vision. We aim to expand our investment capabilities to serve a wide range of clients. Last year’s arrival of Adrian Gosden and Chris Morrison, followed by Alex Savvides and his team, significantly strengthened our UK equities expertise. Likewise, we eagerly anticipate the addition this year of the prestigious European equities team comprising Niall Gallagher, Chris Sellers, and Chris Legg.”

For his part, Tarlock Randhawa, who leads the team, added: “We are excited to join Jupiter, where the active and differentiated management philosophy, combined with a strong client focus, is clearly evident. The transition for our clients will be seamless, and we believe they will benefit from Jupiter’s commitment to excellence in client experience.”

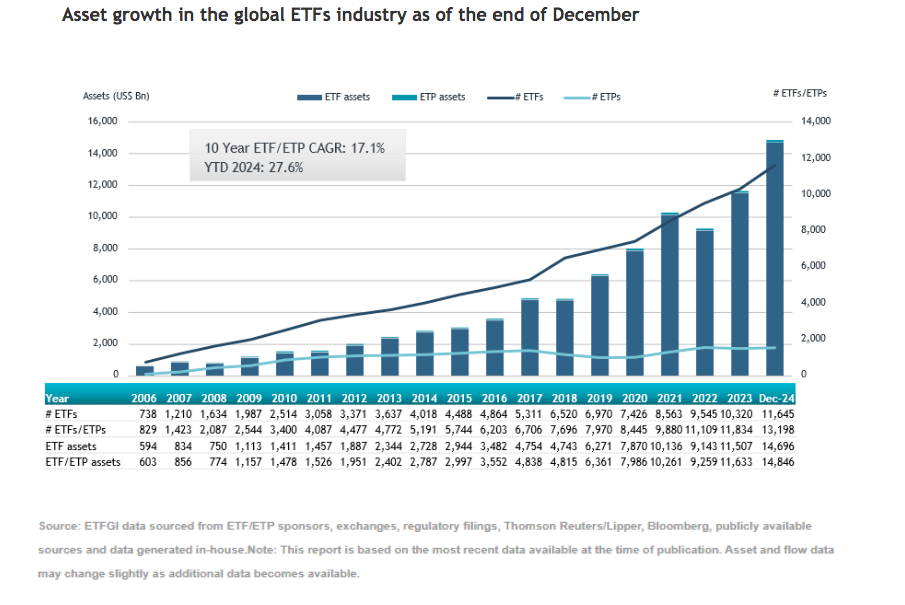

In December, the global ETF industry captured $207.73 billion, raising net inflows for all of 2024 to $1.88 trillion, according to the report by ETFGI. This marks a new record for the sector, surpassing the previous high of $1.29 trillion recorded in 2021 and, of course, exceeding the 2023 total of $974.50 billion.

Additionally, global ETF assets stood at $14.85 trillion in 2024, the second-highest level ever recorded, only below the record of $15.12 trillion in November of the same year. “Assets under management increased by 27.6% in 2024, rising from $11.63 trillion at the end of 2023 to $14.85 trillion at the close of 2024,” notes the latest report by ETFGI.

Regarding the behavior of flows, the ETFGI report shows that out of the $207.73 billion in net inflows, equity ETFs captured $151.58 billion, raising 2024 net inflows to $1.11 trillion, far exceeding the $532.28 billion in 2023. As for fixed income ETFs, these vehicles attracted $16.14 billion in December, bringing 2024 net inflows to $314.32 billion, higher than the $272.90 billion in 2023.

Looking at other asset classes, commodity ETFs reported net outflows of $1.11 billion in December, bringing 2024 net inflows to $3.91 billion, better than the net outflows of $16.88 billion in 2023. Meanwhile, active ETFs attracted net inflows of $41.78 billion in December, bringing 2024 net inflows to $374.30 billion, much higher than the $184.07 billion in net inflows in 2023.

According to Deborah Fuhr, managing partner, founder, and owner of ETFGI, “The S&P 500 index declined 2.38% in December but rose 25.02% in 2024. Developed markets, excluding the U.S. index, declined 2.78% in December but increased 3.81% in 2024. Denmark (down 12.34%) and Australia (down 7.90%) recorded the largest declines among developed markets in December. The emerging markets index increased 0.19% during December and rose 11.96% in 2024. The United Arab Emirates (up 6.42%) and Greece (up 4.21%) recorded the largest increases among emerging markets in December.”

Evolution of Offerings

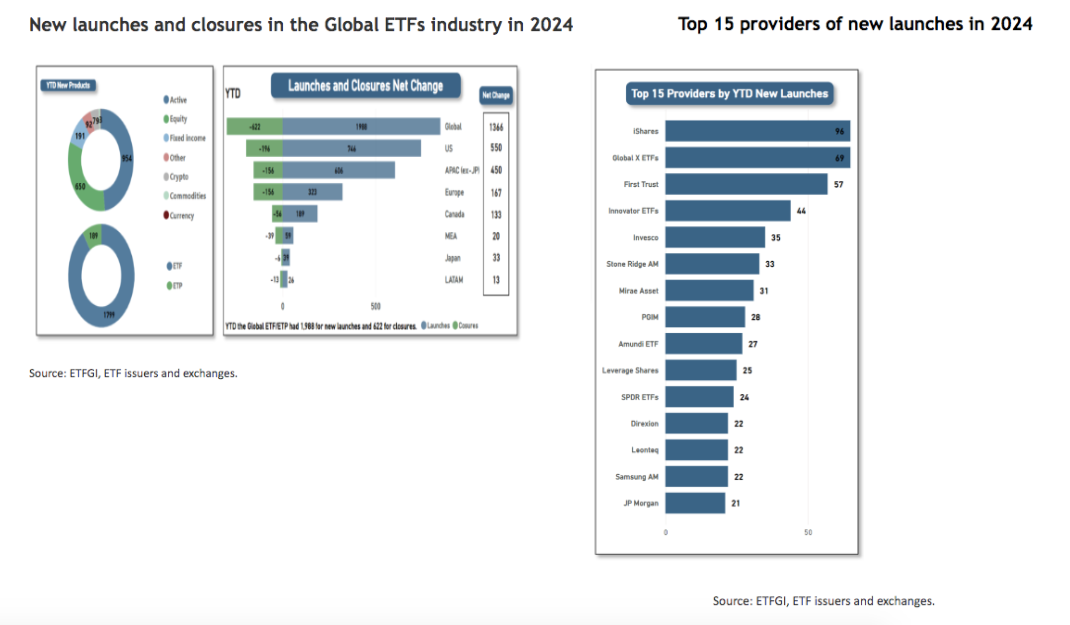

The ETFGI report also highlights that the global ETF industry reached a new milestone with 1,988 new products launched in 2024. It explains that this represents a net increase of 1,366 products after accounting for 622 closures, surpassing the previous record of 1,841 new ETFs launched in 2021.

Specifically, the distribution of new launches in 2024 was as follows: 746 in the United States, 606 in Asia-Pacific (excluding Japan), and 323 in Europe. Additionally, a total of 398 providers contributed to these new launches, which are distributed across 43 exchanges worldwide. Notably, iShares launched the largest number of new products, with 96, followed by Global X ETFs with 69 and First Trust with 57.

“There were 622 closures from 177 providers across 29 exchanges. The United States reported the highest number of closures with 196, followed by Asia-Pacific (excluding Japan) with 156, and Europe also with 156. Among the new launches, there were 954 active products, 650 indexed equity products, and 191 indexed fixed-income products,” noted ETFGI.

Between 2020 and 2024, the global ETF industry experienced significant growth in the number of launches, increasing from 1,131 to 1,988. In 2024, the United States and Asia-Pacific (excluding Japan) recorded the highest number of launches, reaching 746 and 606, respectively, while Latin America had the fewest launches, with only 26. The United States and Canada achieved record numbers of new launches in 2024, with 746 and 189, respectively. Additionally, Asia-Pacific (excluding Japan) achieved its launch record in 2021, with 645; Europe set its record of 434 in 2021; Latin America recorded 41 in 2021; Japan reached 44 in 2023; and the Middle East and Africa achieved 86 in 2020.

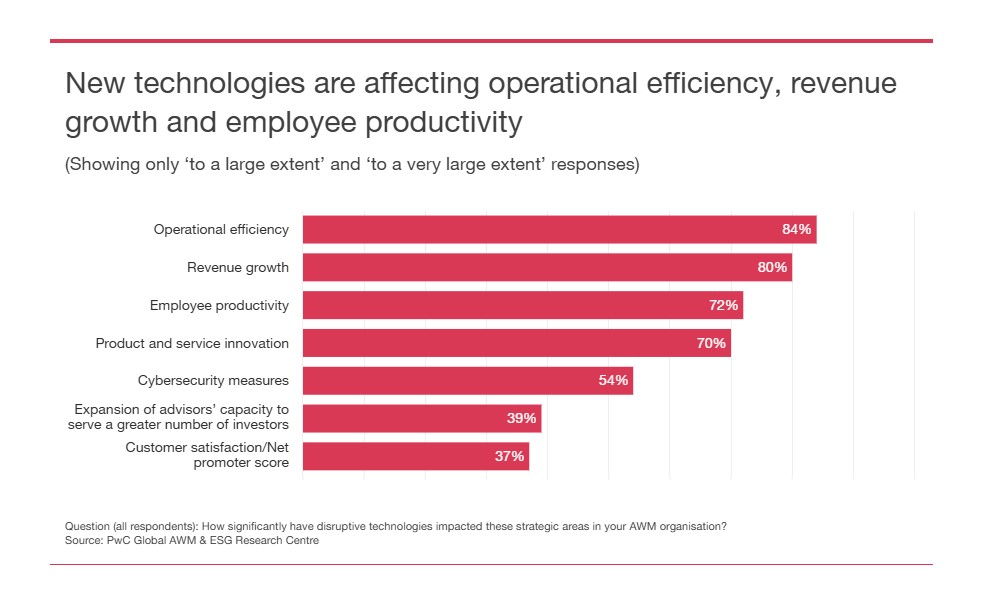

80% of asset management and wealth management firms state that AI will drive revenue growth, while the “technology-as-a-service” model could boost revenues by 12% by 2028, according to the Asset and Wealth Management 2024 report by PwC. A significant finding is that 73% of organizations believe AI will be the most transformative technology in the next two to three years.

The report reveals that 81% of asset managers are considering strategic alliances, consolidations, or mergers and acquisitions (M&A) to enhance their technological capabilities, innovate, expand into new markets, and democratize access to investment products, in a context marked by a significant wealth transfer. According to Albertha Charles, Global Asset & Wealth Management Leader at PwC UK, disruptive technologies, such as artificial intelligence (AI), are transforming the asset and wealth management industry by driving revenue growth, productivity, and efficiency.

“Market players are turning to strategic consolidation and partnerships to build technology-driven ecosystems, eliminate data management silos, and transform their service offerings amid a major wealth transfer, where affluent individuals and younger audiences will play a more significant role in shaping demand for services. To emerge as leaders in this new digital market, asset and wealth management organizations must invest in their technological transformation while ensuring they reskill and upskill their workforces with the necessary digital capabilities to remain competitive and innovative,” explains Charles.

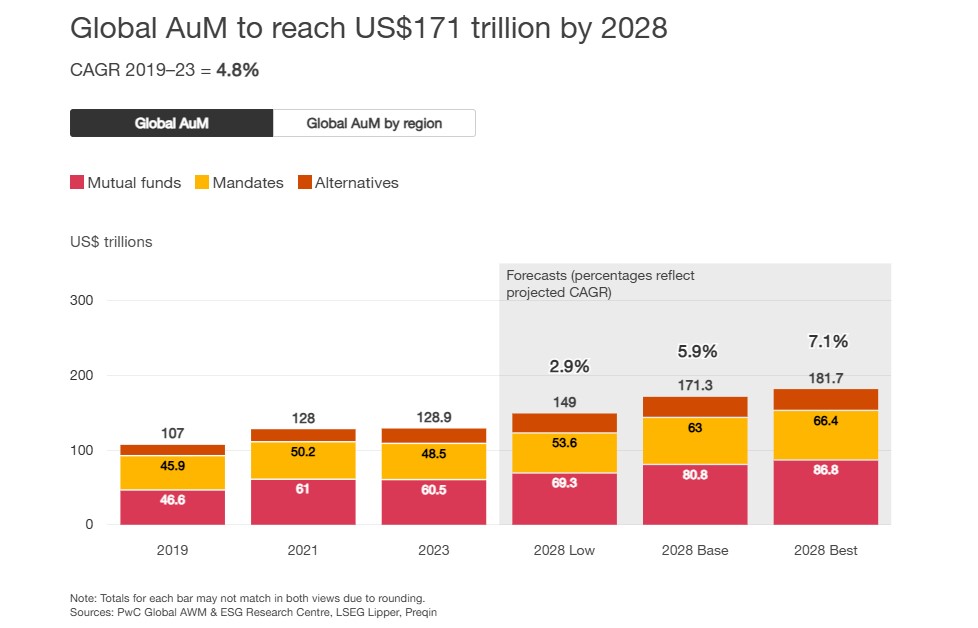

This focus will be critical in addressing an industry whose assets under management are expected to reach $171 trillion by 2028. According to PwC projections, the sector will see a compound annual growth rate (CAGR) of 5.9%, compared to last year’s 5%. Notably, alternative assets stand out, expected to grow even faster with a CAGR of 6.7%, reaching $27.6 trillion during the same period.

“Despite the potential of alternative assets, only 18% of investment firms currently offer emerging asset classes, such as digital assets, though eight out of ten firms that do report an increase in capital inflows,” the report notes in its conclusions.

Key Trends

Taking into account this growth forecast and the role technology will play, PwC’s report identifies several trends. The first is that tokenization stands out as a key opportunity, with tokenized products projected to grow from $40 billion to over $317 billion by 2028, representing a CAGR of 51%.

Tokenization, or fractional ownership, can democratize finance by expanding market offerings and reducing costs. According to PwC, asset managers plan to offer tokenization primarily in private equity (53%), equities (46%), and hedge funds (44%).

Another identified trend is the consolidation and development of technology ecosystems while talent remains the top priority. In this context, 30% of asset managers report facing a lack of relevant skills and talent, while 73% see mergers and acquisitions as a key driver for accessing specialized talent in the coming years.

“The conclusions of this report highlight the urgent need for asset managers and firms to rethink their investment strategies. Their long-term viability will depend on a radical, fundamental, and ongoing reinvestment in how they create and deliver value. Strategic alliances and consolidation will play a vital role in creating technology ecosystems that facilitate greater exchange of ideas and knowledge. Smaller players will be able to modernize their systems quickly and cost-effectively, while larger players will gain access to critical talent and information for growth, particularly as new and emerging technologies like AI transform the investment management landscape,” says Albertha Charles, Global Asset & Wealth Management Leader at PwC UK.

To prepare the report, 264 asset managers and 257 institutional investors from 28 countries and territories were surveyed.

The latest data on the U.S. labor market, published last Friday, marked a turning point for assessing how the year has begun. It also serves as an opportunity to adjust some of the 2025 forecasts released by international asset managers.

The main takeaway from experts is that this latest data rules out an interest rate cut in January—the Fed meeting will take place on January 28–29. Meanwhile, markets have even begun shifting expectations for new cuts to the second half of the year. “Despite strong demand, wages did not respond to the increased labor market activity, as they rose by 0.3% compared to the previous month, the same as in November, and the year-on-year measure even fell to 3.9% from 4.0%. This aligns with central bankers’ assessment that, for now, there are no additional inflationary pressures coming from labor markets, and it is unlikely they will intensify their recent hawkish tone,” explains Christian Scherrmann, Chief U.S. Economist at DWS.

“With no clear signs of weakening, we suspect that the Fed will be happy to pause its easing cycle at its upcoming January meeting, as broadly indicated in December. We remain of the view that the Fed will make only one cut this year, and while we still foresee it happening in March, we acknowledge that the Fed will be data-dependent. However, we expect the Fed to resume rate cuts in 2026 as a result of the net negative impact on growth that we believe will stem from the new administration’s unorthodox economic programs,” argues David Page, Head of Macro Research at AXA IM.

It is clear that a more aggressive Fed impacts the outlook of international asset managers, but it is not the only thing that has changed as the year has begun. According to Fidelity International, there has been a widespread improvement in earnings revisions across most regions. However, in their view, two aspects remain unchanged compared to this year: “We expect U.S. exceptionalism to continue for now, driven by upcoming tax cuts and deregulation policies, which is why we maintain our preference for U.S. equities. At the same time, we still see a high political risk. Trade war risks have increased, while the likelihood of a peace agreement between Russia and Ukraine has grown,” they state.

For Jared Franz, an economist at Capital Group, the U.S. economy is experiencing the same phenomenon depicted in the movie The Curious Case of Benjamin Button (2008). “The U.S. economy is evolving similarly. Instead of advancing through the typical four-stage economic cycle that has characterized the post-World War II era, the economy seems to be moving from the final stage of the cycle to the mid-cycle, thereby avoiding a recession. Looking ahead, I believe the United States is heading toward a multi-year period of expansion and could avoid a recession until 2028,” he says.

Historically, and according to Capital Group’s analysis of economic cycles and returns since 1973, the mid-cycle phase has provided a favorable context for U.S. equities, with an average annual return of 14%.

Implications for Investors

According to Jack Janasiewicz, Chief Strategist and Portfolio Manager at Natixis Investment Managers Solutions, his outlook for the year can be summarized as U.S. stocks rising and bonds falling in 2025. “As we enter the new year, the labor market seems to be in recovery mode, as inflation continues to decline, contributing to higher real wages. This translates into greater purchasing power for U.S. consumers. Since consumption drives most of the growth in the U.S., this is a very healthy scenario. Looking ahead to 2025, our outlook remains positive, with expectations of even slower inflation and an expanding labor market. Investment strategies are likely to favor U.S. equities with a balanced investment approach and the use of Treasury bonds to mitigate risk. We foresee that new investments in artificial intelligence will continue to drive productivity and economic growth. The stock market is expected to maintain its upward trend, while the bond market will earn its coupon,” highlights Janasiewicz.

Fixed Income: Focus on Treasuries

One of the most notable movements in these early weeks of January is that the yield on U.S. Treasuries is approaching 5%. According to Danny Zaid, manager at TwentyFour Asset Management (a Vontobel boutique), last Friday’s U.S. unemployment data provides a strong argument for the Fed to remain patient regarding the possibility of further rate cuts. “This has caused a significant increase in U.S. Treasury yields in recent weeks, as the market is lowering expectations for additional cuts. Moreover, rates have also been pushed higher due to market uncertainty about the extent of the new Trump administration’s policy implementation, particularly concerning tariffs and immigration, which could have an inflationary impact,” notes Zaid.

Analysts at Portocolom add that another notable development was that, for the first time in over a year, the 30-year bond exceeded a 5% yield. “European debt experienced virtually identical behavior, with both the Bund and the 10-year bond gaining 15 basis points, closing at 2.57% and 3.26%, respectively,” they point out.

Among the outlooks from the manager at TwentyFour AM, he considers it likely that 10-year U.S. Treasuries will reach 5%. “However, if we take a medium-term view, yield levels are likely to become attractive at these levels. But we believe that for there to be a significant rally in U.S. Treasuries, at least in the short term, we would need to see data pointing to economic weakness or further deterioration in the labor market, and currently, neither condition is present. The rate movements, while significant, are largely justified given the current economic context,” he argues.

The increase in sovereign bond yields has also been observed in the United Kingdom. Specifically, last week saw the largest rise in bond yields, with 10-year Gilts reaching an intraday high of 4.9%, a level not seen since 2008. “Although specific U.K. factors, such as the budget, contributed to the rise, most of the increase was due to the rise in U.S. Treasury yields during the same period. Both weaker growth and higher interest rates put pressure on public finances. Unlike most other major developed countries, the U.K. borrows money at a much higher interest rate than its underlying economic growth rate, worsening its debt dynamics. If current trends of rising yields and slowing growth persist, the likelihood of spending cuts or tax hikes will increase for the government to meet its new fiscal rules,” explains Peder Beck-Friis, an economist at PIMCO.

Equities

As for equities, the year began with the stock market facing a correction that, according to experts, is far from alarming and seems like a logical adjustment after a strong 2024 in terms of earnings. “This data has dispelled fears of an imminent recession but has also ruled out the possibility of rate cuts by the Federal Reserve in the short term, a factor that has pressured major indices like the S&P 500 and Nasdaq, which have fallen around 1.5%. This correction seems to reflect a normal adjustment in valuations rather than a deterioration in economic fundamentals. Credit spreads become a key indicator for interpreting this environment, as long as they remain stable, the market is simply adjusting after a period of rapid gains. Only if we see a widening of these spreads could it signal the first sign of growing concerns about economic growth,” says Javier Molina, Senior Market Analyst at eToro.

In this context, Molina acknowledges that the upcoming earnings season, starting this week, is generating high expectations. “An 8% year-over-year growth in S&P 500 earnings is anticipated, one of the highest levels since 2021. Sectors such as technology and communication services are leading the forecasts, with expected growth of 18% and 19%, respectively. In contrast, the energy sector faces a sharp contraction in earnings, reflecting the challenges of this environment,” he says.

According to the investment team at Portocolom, their assessment of the first weeks is very clear: “The first week of the year in equity markets was characterized by the opposite movement between Europe and the U.S. While U.S. indices fell 2% (the S&P 500 closed at 5,827.04 points and the Nasdaq 100 at 20,847.58 points), in Europe we saw gains exceeding 2% for the Euro Stoxx 50 and 0.60% for the Ibex 35, which ended the week at 4,977.26 and 11,720.90 points, respectively. The performance of a key benchmark, the VIX, was also noteworthy, as the volatility index rose by more than 8% during the week, adding tension to the markets, particularly in the U.S.”

For the Chief Strategist and Portfolio Manager at Natixis Investment Managers Solutions, earnings growth and multiple expansion were the biggest drivers of U.S. equity market returns during 2024. Looking ahead to 2025, Janasiewicz points out: “While some may argue that valuations are at exaggerated levels, we believe these valuations may be justified by the fact that U.S. corporate margins are at historic highs, and investors are willing to pay more for higher-quality companies with stronger margins. Moreover, risk appetite does not appear to be very high, as many investors seem content to remain in money market funds earning 5%, hesitant to jump into equities, which would push prices even higher.”

In the past, ETFs were synonymous with equity tracking instruments. Ten years after WisdomTree’s launch in Europe, the adoption of this asset type (or wrapper) has opened a new frontier in investing for clients of all profiles. Over the decade since we entered the European market, the ETF landscape has radically changed in terms of available products, assets under management (AUM), and ETF users.

Many European clients who, years ago, were buying an ETF for the first time are now firm believers in this asset type. In fact, many have replaced their mutual fund holdings with ETFs due to the transparency, liquidity, and exposure they can access through this cost-effective wrapper.

ETFs have also moved past their reputation as passive vehicles. We never pigeonholed them that way because we always believed investors needed more innovative solutions than market capitalization-weighted indices. This led us to pioneer the launch of ETFs that invest in systematic strategies based on fundamentals.

Their ability to encompass all types of investment strategies is just one of the reasons why ETFs have done more to level the playing field for investors than any other innovation in asset management. One of their effects in recent years has been their adoption by retail clients, which has accelerated across the region. While there is still room to catch up with the U.S. market, this trend represents an exciting growth opportunity for ETF issuers in Europe.

And it’s not just individual investors benefiting from ETFs. Private banks, high-net-worth individuals, and financial advisory firms can also access institutional-quality products in a direct, cost-effective, transparent, and liquid manner, truly transforming their client offerings in ways previously unattainable.

ETF users today are more curious and open-minded than they were 10 years ago, when these products were mainly used for large-cap equity allocations. At that time, few believed that non-market-cap-weighted exposures could be viable investment options in an ETF. The world now understands that these products are highly efficient, which is another reason why, according to our latest survey of professional investors, nearly all of them invest in ETFs. This point is reinforced by the fact that nearly half expect to increase their allocations in the next 12 months.

The Potential of ETFs

There is no doubt that ETFs have become essential for asset allocators. While most ETF assets are invested in products tracking traditional benchmark indices, investors are increasingly seeking access to a wider range of asset classes through these strategies. More than one-third (35%) of professional investors use ETFs to access alternative asset classes, including commodities and cryptocurrencies. This marks a significant shift from earlier skepticism about the viability of non-equity exposures in an ETF.

To understand the impact of these products, one must consider the global adoption of cryptocurrency ETPs. This innovation has bridged the gap between traditional finance and this emerging asset class, as evidenced by the $20 billion that has flowed into bitcoin ETPs this year. Turning bitcoin into an exchange-traded product democratized access to the world’s largest cryptocurrency. It has succeeded because bitcoin adds something different to portfolios, and there are fewer barriers to entry—most European investors can now buy a cryptocurrency ETP.

The Next Chapter: Smart Innovation in ETFs

Innovation focuses on enhancing portfolio value, and the demand for it is undeniable. According to our survey, 98% of European professional investors are seeking greater product innovation. Additionally, 25% identify the development of innovative products as the key trend that will drive ETF growth in Europe over the next decade. This perspective strengthens our belief that ETFs are the ideal platform for delivering innovation to investors—a commitment we have honored from the outset.

The past decade has shown us that ETFs have a promising future. This will translate into greater adoption, more options for investors, and continuous innovation from issuers, who must adapt to evolving client needs. Failure to innovate can be costly. The future of ETFs is immensely promising, and I am confident that smart ETF innovation will shape a bright future for both the industry and investors.

After Trump’s victory late last year, commodities began to weaken. Even gold, which had an exceptional year, started losing value as the dollar strengthened. These turbulences in the last quarter of 2024 have filled investment firms’ outlooks for commodities with both light and shadow, and, above all, with highly diverse interpretations.

For example, Bank of America expects commodity prices, including oil, to decline. According to Francisco Blanch, Head of Commodities and Derivatives Research, the demand growth for commodities will weaken: “Macroeconomic fundamentals suggest that in 2025, markets will be oversupplied with oil and grains but more balanced in the case of metals. After facing headwinds early in the year, gold should reach a high of $3,000 per ounce.”

In its outlook, the institution explains that the risks of a global trade war, combined with a strong U.S. dollar and higher terminal rates, create a bearish scenario for commodity returns. “Fundamentals point to lower prices for oil, grains, and metals in the first half of 2025, but the outlook could improve with stimulus in China or trade agreements. Negative macroeconomic shocks (tariffs, higher rates) or positive ones (trade, fiscal, or peace agreements) could increase correlations between asset classes in 2025,” Bank of America emphasizes.

Ofi Invest, for its part, believes that the roughly 10% correction in industrial and precious metal prices following Trump’s victory was a one-off event caused by a strong dollar. Despite this “setback,” it considers that nothing has changed the medium-term structural drivers for metals: the energy transition and high levels of debt. The asset manager believes that these two trends will once again support rising metal prices, given the structural imbalances in both supply and demand.

“The short-term rebound in the dollar is not the most relevant factor for gold. Debt issues and the emerging distrust in the dollar are structural and persistent problems that have a greater impact on gold prices. Additionally, the price of metals will benefit from shifts in consumption due to the energy and digital transition. In short, the structural drivers of metals, led by the energy and digital transitions, should soon support rising metal prices, given the current supply and demand imbalances,” explains Ofi Invest.

On the other hand, Macquarie holds that, given its economists’ global GDP growth forecast of 3% for 2025, with sequential acceleration in the first half, commodity prices should find some support against the current headwind of a strong U.S. dollar. That said, they note that the prospect of a stronger tailwind, with a notable acceleration in global industrial production, has diminished. “In fact, the negative implications for goods demand from a trade war threaten the recovery potential for manufacturing relative to services. The possibility that commodity demand will receive a boost from manufacturing restocking in developed markets is also limited by the negative confidence impact of a trade war and by our reduced expectations for Federal Reserve rate cuts,” they explain.

Headwinds

According to Macquarie’s outlook, in their baseline scenario, the incremental implementation of both U.S. tariffs and Chinese policy easing will likely result in comparatively slow price action. “Without something to drive real demand growth or a narrative to reinvigorate financial flows, fundamentally oversupplied markets will likely see most prices trend downward over the next 18 months, interspersed with headline-driven volatility and the possibility of regional mismatches,” they explain.

Additionally, they warn of a wide range of associated risks, heavily dependent on whether any trade agreements are reached. In their outlook document, they indicate that the most volatile alternative scenario would undoubtedly be one in which the incoming Trump administration adopts a maximalist approach to tariff implementation. This could lead to increased financial risk and real demand destruction for industrial commodities, only to be followed by a much more robust and likely commodity-intensive stimulus package from the Chinese government.

Growth Trends

“Apart from cyclical uncertainties, the pace of the energy transition remains the key factor we expect to determine global final demand growth trends. Given the absence of commodity demand growth from the ‘old economy’ in developed markets over the last two decades, we remain skeptical about its potential as a future growth driver. Furthermore, the argument that the energy transition is already being perceived as a demand differentiator is underscored by the assessment that global electric vehicle (EV) production should account for approximately 40% of net copper demand growth in 2024. At the same time, strong EV sales in China should mean that fleet penetration rates are now sufficient for refined oil demand for road transportation in the country to have peaked,” adds Macquarie.

Their conclusion is that not only will the pace of these developments vary over time, but the degree to which financial markets price them in will likely exacerbate these changes. “In light of this, as well as the reflexivity of commodity markets, periods of excessive price strength will likely offset the potential for future fundamental tightening by incentivizing primary and secondary supply growth, as well as demand destruction. Conversely, any period of excessive price weakness—such as from a trade war—will add to the potential for medium-term shortages,” concludes Macquarie’s outlook document.

As we enter 2025, it is crucial to reflect on the events of the past year and prepare for the challenges and opportunities ahead. At the end of 2024, the investment leaders of Neuberger Berman gathered to analyze the evolving investment environment and identify the themes they consider essential for the next twelve months. As a result of this exercise, the investment firm highlights five key themes.

A Year of Above-Trend Growth

Although policies may change, industrial strategies aimed at influencing domestic production patterns will continue, whether through government spending and investment, fiscal policy, trade policy, deregulation, or other means, according to Neuberger Berman. “If inflation can remain contained—and we believe it is possible—central banks could stay on the sidelines and allow economies to operate at a slightly faster pace. This scenario suggests above-trend U.S. GDP growth, which could pull other global economies along. The implications for debt and deficits, as well as the efficient allocation of capital, could surprise investors by proving to be manageable concerns in 2025,” the experts highlight.

Extending the Soft Landing with Real Income Growth

The negative impact of high inflation on lower-income consumers and small businesses has been a key factor in this year’s political uncertainty. According to the firm, countries and governments that achieve moderate inflation and greater participation in real wage and income growth will define success, reflected in data such as higher consumer confidence, improved political approval ratings, and GDP growth rates. “While it remains to be seen whether certain policy combinations can achieve this, we see evidence that the new U.S. administration at least recognizes this goal, and active industrial policies are proof of a growing recognition in other regions,” the experts emphasize.Setting the Stage for Broader Equity Market Performance

Deregulation, business-friendly policies, moderate inflation, and lower rates could allow for broader earnings growth and price performance, according to Neuberger Berman. “At the same time, the growth rates of large technology companies are likely to slow and normalize as capital expenditures increase. Value stocks, small-cap stocks, and sectors such as financials and industrials could start to regain ground against large tech companies. Non-U.S. markets could perform more strongly due to higher global growth and lower commodity prices. Relative valuations, along with fundamentals, should support this trend,” the experts note.

Bond Markets to Focus on Fiscal Policy Over Monetary Policy

“For more than two years, bond markets have been dominated by inflation data and central bank responses. We believe that in 2025, a reacceleration of inflation can be avoided, and central banks will settle into the more predictable routine of debating the level of the neutral rate,” Neuberger Berman states.

Bond investors are likely to shift their focus toward growth prospects for most of 2025, and possibly toward deficits and the issue of the term premium by the end of the year and into 2026, according to the firm’s experts. The result will be a moderate steepening of yield curves and a migration of bond market volatility from the short end of the curve to the intermediate and long ends.

A Boom in Mergers and Acquisitions

“Several factors are converging to unleash a pent-up wave of corporate deals: above-trend growth, optimistic valuations in public equity markets, a more stable outlook on inflation and central bank policies, the return of banks to the leveraged loan market, declining interest rates, and tighter credit spreads. Perhaps most importantly, a shift in the regulatory approach in the U.S. is anticipated,” the firm highlights.

That said, secondary private equity markets and co-investments will continue to thrive, as liquidity is still required to manage a large backlog of mature investments. However, raising new primary funds will remain a challenge. Event-driven hedge fund strategies will benefit from a large set of new opportunities, the experts conclude.

Vanguard Will Expand Its Fixed-Income Offering with the Launch of the Vanguard Short Duration Bond ETF (VSDB), an Actively Managed Fixed-Income ETF to Be Managed by Vanguard’s Fixed-Income Group.

“The Vanguard Short Duration Bond ETF adds to our growing lineup of actively managed fixed-income ETFs and offers investors the opportunity to outperform the market in their short-term fixed-income allocations,” said Dan Reyes, Head of Vanguard’s Portfolio Review Department.

The firm plans to launch this ETF in early April of this year, and it will offer diversified exposure, primarily to short-term U.S. investment-grade bonds, including some exposure to structured products such as asset-backed securities.

The ETF is designed “to provide clients with current income and lower price volatility, consistent with short-duration bonds,” according to the statement.

Additionally, it will have the flexibility to invest in below-investment-grade debt and emerging markets to seek additional yield.

“This multi-sector approach aligns with investors’ preferences within their short-term fixed-income allocations and allows Vanguard’s fixed-income group to leverage the best ideas within a broad investable universe. The VSDB will have an estimated expense ratio of 0.15%,” the manager’s statement adds.

The ETF will be actively managed, enabling portfolio managers to seek the best opportunities within their investment universe while always maintaining a highly risk-aware approach, the information concludes.