Allfunds has announced the appointment of Carlos Berastain as its new Global Head of Investor Relations, replacing Silvia Ríos, who is stepping down to pursue new opportunities.

Berastain, who brings over 25 years of experience in the industry, joins Allfunds from Santander, where he has served as Head of Investor Relations since 2017.

According to the company, Ríos will remain at Allfunds for a few months to ensure a smooth and orderly transition. During this period, she will work closely with Carlos Berastain, who will officially take on his new role at Allfunds on March 17, 2025.

“We are grateful for Silvia’s outstanding work, dedication, and contributions over the years, and we wish her success in her next career steps. We look forward to welcoming Carlos as he leads our investor relations initiatives and strengthens communication with our shareholders and the broader financial community,” said Álvaro Perera, CFO of Allfunds.

Allfunds highlighted Silvia Ríos’ pivotal role in the company, particularly in its IPO and strategic positioning within the financial community over the past four years. She was recently recognized as one of the top Investor Relations Directors at the Investor Relations Society Awards 2024.

Once again, Monaco will become the meeting hub for asset and wealth management leaders during IMpower FundForum, taking place from June 23 to 25, 2025. As the only specialized event dedicated to investment managers across active, passive, and private markets—with a focus on private wealth management—it is a must-attend for senior executives in the industry.

Join 1,400+ senior leaders, including 500+ asset managers, 400+ fund selectors, and asset owners, for three dynamic days of networking and collaboration. Year after year, the event is the preferred choice for CEOs, CIOs, COOs, and partners from leading asset managers and GPs worldwide. With a 35-year track record, it delivers unparalleled industry insights.

With the highest concentration of fund buyers and LPs from private banking and wealth management, this is the only event where you can connect with over 500 influential professionals. According to the event organizers, “One-third of attendees are fund selectors and asset owners.” Stay ahead in the asset and wealth management community at IMpower FundForum, the ultimate event for meaningful connections and valuable industry insights.

Fund selectors attend for free, while asset and wealth managers benefit from discounted rates. Register now and save 10% with code: FKN3972FUNDSOC.

In today’s investment landscape, alternative assets have become a compelling portfolio and risk diversification strategy. Real estate has proven to be an attractive option within this category due to its ability to generate recurring income and preserve value over time. However, liquidity has historically been one of its limitations. This is where asset securitization plays a crucial role, allowing real estate to be converted into tradable securities accessible to a broader base of investors.

Real estate securitization generally involves creating a special purpose vehicle (SPV), a legal entity that isolates and manages properties. This SPV issues securities backed by the property’s income flows, such as bonds or notes, which institutional investors can acquire in capital markets. For asset managers, this mechanism improves portfolio liquidity, optimizes capital allocation, and enables structuring attractive financial products for different investor profiles.

Real estate securitization can take many forms; among the main ones are:

Residential Mortgage-Backed Securities (RMBS): These are securities backed by pools of residential mortgages. Banks or financial institutions typically originate mortgages and then sold to an SPV. The SPV bundles the mortgages and issues securities backed by the underlying loans.

Commercial Mortgage-Backed Securities (CMBS): These securities are backed by pools of commercial real estate mortgages. Commercial property owners, such as office buildings, shopping centers, or industrial properties, take out the loans. The SPV pools these loans and issues securities backed by the underlying mortgages.

Real Estate Investment Trusts (REITs): These investment vehicles own and operate income-generating real estate assets. REITs allow investors to gain exposure to real estate without directly owning the underlying properties. REITs must distribute at least 90% of their taxable income to shareholders as dividends, making them attractive for investors seeking regular income.

Securitized real estate assets offer multiple advantages for asset managers and their clients, including:

Diversification: Exposure to a broad spectrum of real estate assets across various regions and sectors.

Professional Management: Assets are managed by experienced real estate and finance specialists.

Optimized Returns: Securitized real estate can offer an attractive return profile compared to traditional investments.

However, securitized real estate assets also carry certain risks, including:

Market Risk: The value of securitized instruments may fluctuate based on real estate market conditions.

Credit Risk: The underlying assets may fail to meet payment obligations, affecting the instrument’s profitability.

Liquidity Risk: Changes in market conditions may impact the ease of buying or selling these securities at fair prices.

Success story: CIX Capital

CIX Capital is a firm specializing in real estate investments in Brazil and the U.S., focusing on structuring and managing tailored strategies for institutional investors, asset managers, and family offices. With over R$7.3 billion in transactions, CIX sought an efficient investment vehicle to access international private banking swiftly and cost-effectively.

In this context, FlexFunds‘ solutions enabled CIX Capital to structure a customized issuer for exchange-traded products (ETPs), transforming real estate assets into tradable securities with access to international markets. Thanks to this solution, CIX has securitized over $200 million, optimizing costs and timelines compared to traditional structures in jurisdictions such as the Cayman Islands, the British Virgin Islands, and Luxembourg.

Carlos Balthazar Summ, CEO of CIX Capital, highlights: “FlexFunds’ investment vehicles are ideal for real estate. In a record time, we set up and launched our Bond (ETP), quickly accessing private banking channels via Euroclear, broadening our international capital raising ability, and successfully acquiring 358 multifamily units in Florida, USA. The simplicity in the onboarding of investors and its accompanying savings in the back-oce make FlexFunds’ your ideal partner to create internationally accredited investment structures. It is also a state-of-the-art solution that was well perceived by the private and asset management industries in Brazil and abroad.”

Key benefits achieved by CIX Capital with FlexFunds:

Simplify the investor onboarding and underwriting process

Reduced the administrative costs of fund management.

Facilitate the raising of capital from international investors.

Enable access to international private banking channels.

Real estate securitization provides asset managers an efficient tool to optimize portfolios, enhance liquidity, and attract institutional investors. However, conducting a thorough risk analysis and structuring vehicles tailored to each investment strategy is crucial.

FlexFunds serves as a strategic partner in the repackaging of real estate assets, offering accessibility and management optimization through securitization and as a bridge to multiple private banking platforms. If you are interested in securitizing your real estate investment fund, contact the experts from FlexFunds at info@flexfunds.com.

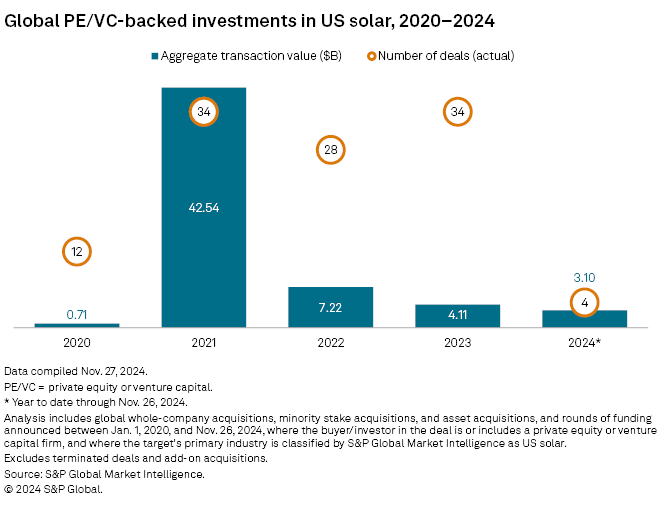

Private equity and venture capital activity in the U.S. solar industry is on track to reach its lowest level in the past four years. This contrasts with significant global private equity inflows into the sector during 2024, according to a new global report by S&P.

According to the report, private equity investments in residential and utility-scale solar energy in the U.S. from January 1 to November 26 totaled $3.1 billion, approximately 24.6% lower than the total reached in 2023 and representing only 7.3% of the $42.54 billion accumulated in 2021. So far, only four private equity deals in U.S. solar energy have been announced in 2024.

Globally, the value of transactions in residential and utility-scale solar energy reached $25.04 billion, an increase of approximately 52% from the $16.46 billion recorded for the entire year of 2023, according to data from S&P Global Market Intelligence.

This rise in global investment comes amid China’s dominance in solar panel production, which has led to oversupply levels. According to a report by Wood Mackenzie, the Asian country will continue to hold more than 80% of global solar manufacturing capacity through 2026.

Europe, including the United Kingdom, attracted the majority of private equity investments in residential and utility-scale solar energy, with 23 deals exceeding $20 billion. The value of private equity transactions involving UK-based renewable energy companies has already surpassed private investments in the U.S. renewable energy sector this year.

Additionally, the U.S. and Canada ranked second in transaction value, with $3.25 billion across seven solar energy deals. The Asia-Pacific region, including China, followed closely with 20 deals worth over $795 million.

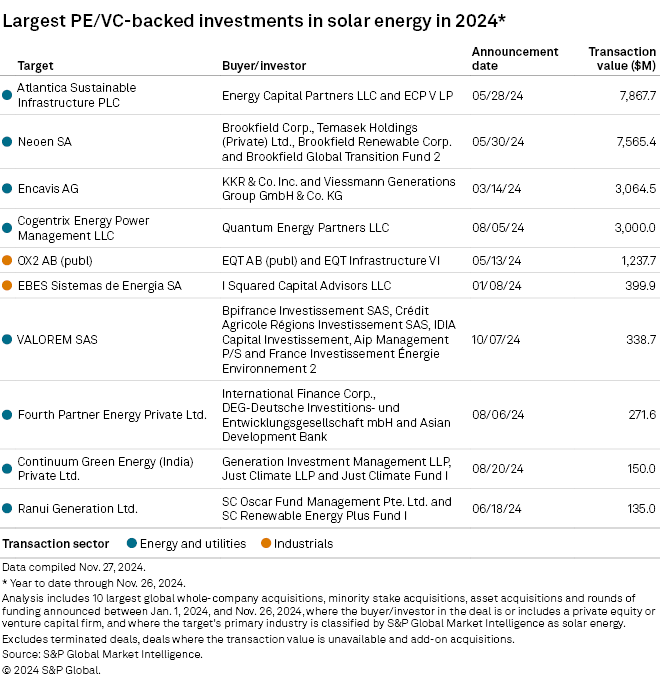

European Mega-Deals Drive Private Equity Financing Growth

Several multibillion-dollar transactions have contributed to the total value of solar sector deals so far this year. The largest private equity-backed solar energy deal announced in 2024 is Energy Capital Partners LLC’s planned $7.87 billion acquisition of Atlantica Sustainable Infrastructure PLC, a UK-based company. Its ECP V LP fund is set to purchase Atlantica from Algonquin Power & Utilities Corp., which decided to sell after conducting a strategic review of its renewable energy business.

The second-largest deal is Brookfield Asset Management Ltd. and Temasek Holdings (Pvt.) Ltd.’s proposal to acquire 53.32% of Neoen SA, a Paris-based company, for $7.57 billion. The buyers are expected to eventually acquire full ownership of the company and take it private.

Private investments in the industry can help pave the way for the development of new solar technologies. The shorter development timeline, lower capital costs, and compatibility with battery energy storage systems have kept solar energy more attractive than other alternative energy sources, such as wind or nuclear, according to Benedikt Unger, director at consulting firm Arthur D. Little.

“By financing next-generation solar technologies, such as bifacial modules and perovskite cells, private equity investments can accelerate innovation,” Unger wrote in an email to Market Intelligence.

The technical explanation is that bifacial modules capture light on both sides of the solar panel, while perovskite cells are high-performance, lower-cost materials compared to those currently used in solar technology. Unger also sees opportunities for private equity in emerging local solar technology supply chains and the growing solar panel recycling industry.

“Photovoltaic recycling is an emerging industry, but its development is crucial, especially in more mature markets like Europe or the United States. Localized supply chains will be needed in many regions, including Africa and Southeast Asia,” Unger concludes.

Across Europe, women are less likely than men to participate in financial markets, leading to what experts call the gender investment gap. The numbers are striking: on average, women own 30% to 40% less in investments and private pensions than men, putting them at a long-term financial disadvantage (OECD, 2023).

While structural factors such as the gender pay gap—which stands at 12.7% in the EU (European Commission, 2024)—and career interruptions due to caregiving responsibilities contribute to this disparity, another key factor is confidence and perception. Many women feel that investing “is not for them,” often due to financial jargon, a natural aversion to risk, and a lack of female role models in finance.

However, the reality is clear: without investing, women risk greater financial insecurity and accumulate less wealth over time. Beyond personal finances, the gender investment gap is an economic issue, costing Europe an estimated €370 billion* annually in lost potential.

Why Aren’t Women Investing Enough?

Despite increasing financial independence, women across Europe are less likely to invest in stocks, funds, and pensions than men. A 2024 ING survey found that only 18% of women invest regularly, compared to 31% of men. In Germany, the disparity is even more pronounced, with only 30% of women actively investing their savings, a significantly lower rate than their male counterparts (DWS, 2024).

In the UK alone, the gender investment gap is estimated at €687 billion (Portfolio Adviser, 2024), with a similar trend across the EU. Women are more likely to hold their savings in cash, missing out on the long-term growth potential of financial markets.

One of the main reasons? Fear of risk. The European Banking Authority (EBA) reports that women are far more likely to keep their money in cash savings accounts, even as inflation erodes their value, rather than investing in diversified portfolios that offer higher growth potential (EBA, 2023).

Another factor is the representation of finance in media and culture. A 2025 study from King’s Business School in London analyzed 12 finance-related movies and 4 television series and found that 71% of male protagonists held senior executive roles, while none of the female characters did (Baeckstrom et al., 2025). More often, women were portrayed as wives or assistants rather than investors or decision-makers.

From Monopoly to the Markets

The fight for women’s financial empowerment is not new. Consider Lizzie Magie, the often-overlooked inventor whose game later became Monopoly. In 1904, she designed The Landlord’s Game to highlight wealth inequality and promote economic education. Yet, years later, Charles Darrow adapted and commercialized her idea, taking full credit and reaping financial rewards (Women’s History Museum, 2024). Her story reflects a broader issue—women’s contributions in finance are often undervalued.

The Cost of Not Investing

Women’s reluctance to invest is not just a financial literacy issue—it is a direct threat to their long-term financial security. On average, women live five years longer than men (Eurostat, 2024), meaning they need larger retirement savings. However, they are more likely to invest in “safe” but low-yield products, such as low-interest savings accounts or government bonds, rather than diversified stock portfolios that generate long-term growth.

The risk of staying on the sidelines is clear: if a woman holds €50,000 in cash for 30 years, inflation could cut its purchasing power in half. Meanwhile, a diversified stock portfolio with an average annual return of 7% could grow to €380,000 over the same period.

Breaking the Cycle: How to Close the Gender Investment Gap

To ensure that women are better represented in financial markets, we need structural changes, cultural shifts, and targeted initiatives to make investing more accessible and inclusive. The financial education plays a crucial role, with programs that simplify investment strategies and address women’s specific concerns.

The representation in media is key: currently, only 18% of financial experts quoted in the press are women, reinforcing the outdated perception that investing is a male-dominated field (Baeckstrom et al., 2025). Normalizing women as financial experts and investors can help dismantle stereotypes and encourage participation.

Additionally, more financial institutions recognize the need for tailored investment products. An example is Female Invest in Denmark, which offers investment courses and community-based support (Female Invest, 2024).

The workplace pension policies must evolve to reflect the reality that women take more career breaks than men. Sweden, for example, has introduced state-matching pension contributions to help women save more for retirement (Pensions Europe, 2024).

By addressing these systemic barriers, we can create an environment where women have both the opportunity and the confidence to invest, ensuring their financial security and independence for future generations.

If history has taught us anything, it’s that when women take control of their finances, they change the game—just as Lizzie Magie did with Monopoly.

This time, let’s make sure they receive both the credit and the financial rewards. By breaking down barriers, increasing confidence, and making investing more accessible, we can help more women build a strong and lasting financial future.

On International Women’s Day, we envision a future where every woman feels empowered to invest, grow her wealth, and take control of her financial destiny. Because when women invest in themselves, they invest in a stronger and more prosperous society for all.

Opinion Piece by Britta Borneff, Chief Marketing Officer (CMO) of the Association of the Luxembourg Fund Industry (ALFI).

Note: The European Investment Bank (EIB) estimates that the gender investment gap results in an annual economic loss of approximately €370 billion, equivalent to 2.8% of the EU’s GDP (2016). This figure highlights the severe economic consequences of gender inequalities in the financial sector.

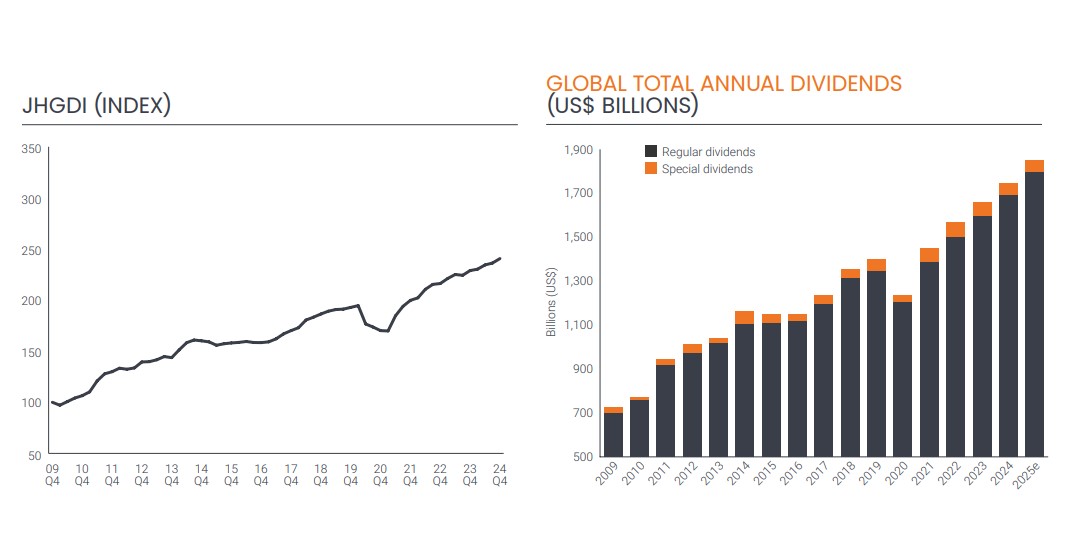

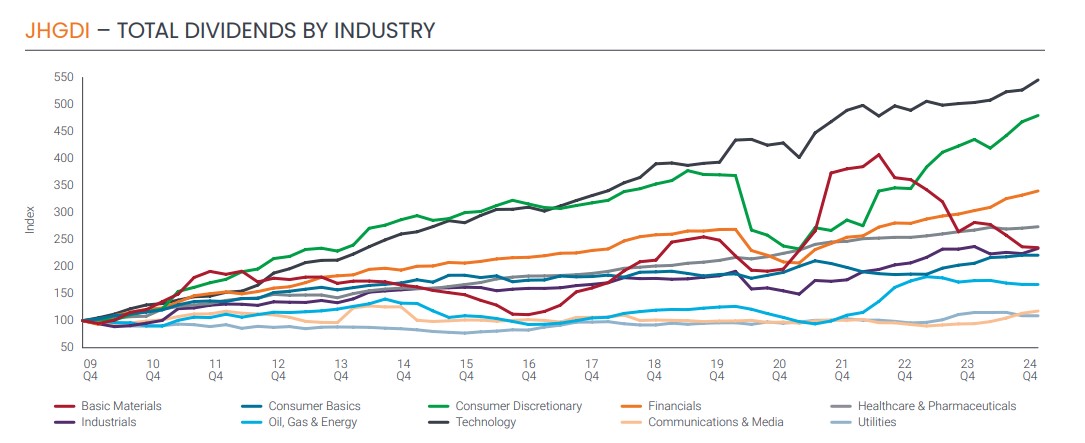

Global dividend payouts reached a record $1.75 trillion in 2024, representing underlying growth of 6.6%, according to the latest Janus Henderson Global Dividend Index. The asset manager explains that, at a general rate, growth was 5.2%, driven by lower special dividends and the strength of the dollar.

The year’s results slightly exceeded Janus Henderson’s forecast of $1.73 trillion, mainly due to a better-than-expected fourth quarter in the U.S. and Japan. In Q4, dividend payouts increased by 7.3% on an underlying basis.

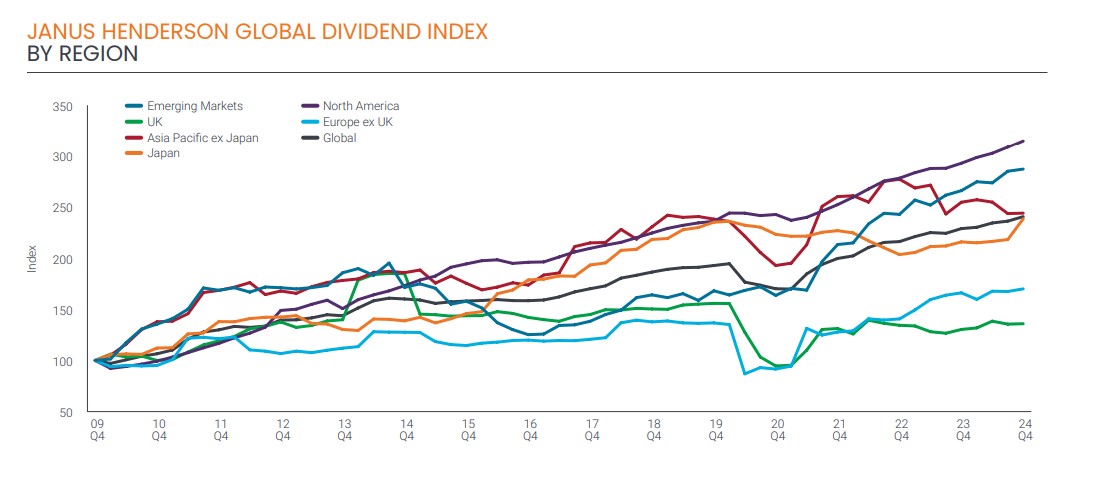

According to their assessment, overall growth was strong across Europe, the U.S., and Japan throughout the year. Some key emerging markets, such as India, and Asian markets like Singapore and South Korea, also recorded decent growth. In 17 of the 49 countries included in the index, dividend payouts hit record levels, including some of the largest distributing nations like the U.S., Canada, France, Japan, and China.

When analyzing the source of this growth, the Janus Henderson report highlights that several major companies distributing dividends for the first time had a disproportionate impact.

“The largest payouts came from Meta and Alphabet in the U.S. and Alibaba in China. Together, these three companies distributed $15.1 billion, representing 1.3% of total dividends or one-fifth of global dividend growth in 2024,” the report states.

Another key finding is that 88% of companies either increased or maintained their payouts globally, while the median dividend growth—or typical growth rate—stood at 6.7%.

By sector, nearly half of the dividend increase in 2024 came from the financial sector, primarily banks, which saw underlying dividend growth of 12.5%.

According to Janus Henderson, dividend growth in the media sector was also strong, doubling on an underlying basis, largely due to payouts from Meta and Alphabet. However, the increase was broad-based, with double-digit growth in telecommunications, construction, insurance, durable consumer goods, and leisure.

In contrast, mining and transportation were the worst-performing sectors, paying a combined $26 billion less than in 2023.

The report also highlights that, for the second consecutive year, Microsoft was by far the world’s largest dividend payer. Meanwhile, Exxon, which expanded its portfolio with the acquisition of Pioneer Resources, climbed to second place—a position it hadn’t held since 2016.

For the year ahead, Janus Henderson expects dividends to grow by 5% on a general basis, pushing total payouts to a record $1.83 trillion. Underlying growth is projected to be closer to 5.1% for the full year, as the strong U.S. dollar against multiple currencies is expected to slow overall growth.

Janus Henderson’s Assessment of the Index Data

Commenting on these figures, Jane Shoemake, portfolio manager at the Global Equity Income team of Janus Henderson, highlights that several of the world’s most valuable companies—particularly those rooted in the U.S. tech sector—are now starting to distribute dividends. This contradicts previous assumptions that these firms would avoid returning capital to shareholders through dividends.

“In doing so, they are following the path of other successful companies before them. As they mature, they start generating cash surpluses that can be returned to investors. These companies are currently providing a significant boost to global dividend growth,” says Shoemake.

2025: An Uncertain Year for the Global Economy

Overall, Shoemake sees 2025 as a potentially uncertain year for the global economy.

“The world economy is expected to continue growing at a reasonable pace, but the risk of tariffs and potential trade wars, along with high public debt levels in many major economies, could lead to greater market volatility in 2025. In fact, fixed-income yields in some markets have risen to levels not seen in years,” she explains.

She also points out that higher interest rates impact investment, slow long-term earnings growth, and increase financing costs, all of which affect corporate profitability.

“That said, the market still expects corporate earnings to increase this year, with consensus forecasts projecting growth above 10%. While this may seem overly optimistic given the current economic and geopolitical challenges, the good news for income-focused investors is that dividends tend to be more resilient than profits throughout the economic cycle.

Companies decide how much to distribute to shareholders, meaning dividend income streams are far less volatile than corporate earnings. For this reason, we expect dividends to reach a new record this year,” concludes Shoemake.

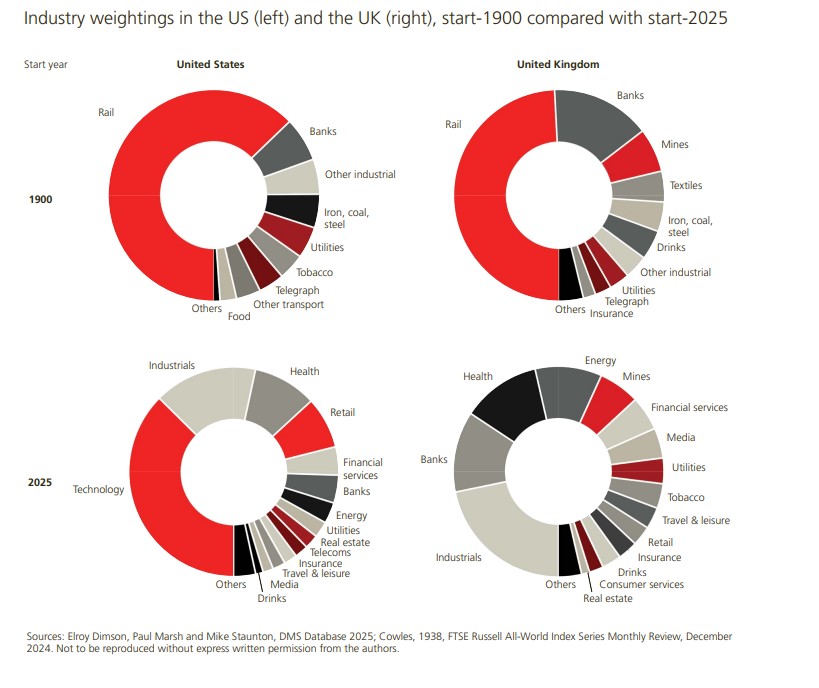

Financial markets and the industrial landscape have changed enormously since 1900, and these changes can be observed in the evolution of the composition of publicly traded companies in global markets. As depicted by UBS Global Investment in its report Global Investment Returns Yearbook, at the beginning of the 20th century, markets were dominated by railroads, which accounted for 63% of the stock market value in the U.S. and nearly 50% in the U.K.

In fact, nearly 80% of the total value of U.S. publicly traded companies in 1900 came from sectors that are now small or have even disappeared. This percentage stands at 65% in the case of the U.K. Additionally, a large proportion of companies currently listed on the stock market come from sectors that were either small or nonexistent in 1900, now representing 63% of market value in the U.S. and 44% in the U.K. “Some of the largest industries in 2025, such as energy (excluding coal), technology, and healthcare (including pharmaceuticals and biotechnology), were practically absent in 1900. Likewise, the telecommunications and media sectors, at least as we know them today, are also relatively new industries,” the report notes in its conclusions.

Among the key findings of this report, which analyzes historical data from the past 125 years, one standout conclusion is that long-term equity returns have been remarkable. According to the document, equities have outperformed bonds, Treasury bills, and inflation in all countries. An initial investment of 1 dollar in U.S. stocks in 1900 had grown to 107,409 dollars in nominal terms by the end of 2024.

Concentration, Synchronization, and Inflation: Three Clear Warnings

Throughout this historical evolution, the report’s authors have identified concentration as a growing concern. “Although the global equity market was relatively balanced in 1900, the United States now accounts for 64% of global market capitalization, largely due to the superior performance of major technology stocks. The concentration of the U.S. market is at its highest level in the past 92 years,” they warn.

In contrast, diversification has clearly helped manage this concentration and, more importantly, volatility. According to the report’s conclusions, while globalization has increased the degree of market synchronization, the potential benefits of international diversification in reducing risks remain significant. For investors in developed markets, emerging markets continue to offer better diversification prospects than other developed markets.

Finally, the conclusions emphasize that inflation is a key factor to consider in long-term returns. In this regard, the authors’ analysis shows that asset returns have been lower during periods of rising interest rates and higher during cycles of monetary easing. “Similarly, real returns have also been lower during periods of high inflation and higher during periods of low inflation. Gold and commodities stand out among the few effective hedges against inflation. Since 1972, gold price fluctuations have shown a positive correlation of 0.34 with inflation,” the report states.

Key Insights from the Report’s Authors

Following the release of this report, Dan Dowd, Head of Global Research at UBS Investment Bank, commented: “I am pleased to once again collaborate with professors Dimson, Marsh, and Staunton, as well as our colleagues from Global Wealth Management, in presenting the 2025 edition of the Global Investment Returns Yearbook. The 2025 edition marks an important milestone. With 125 years of data, it provides our clients across the firm with a valuable framework for addressing contemporary challenges through the lens of financial history.”

Meanwhile, Mark Haefele, Chief Investment Officer of UBS Global Wealth Management, highlights that the Global Investment Returns Yearbook can help us understand the long-term impacts of following principles such as diversification, asset allocation, and the relationship between return and risk. “Once again, it teaches us that having a long-term perspective is crucial and that we should not underestimate the value of a disciplined investment approach,” Haefele states.

Finally, Professor Paul Marsh of the London Business School notes that “equity returns in the 21st century have been lower than in the 20th century, while fixed income returns have been higher. However, equities continue to outperform inflation, fixed income, and cash. The global stock market has delivered an annualized real return of 3.5% and a 4.3% premium over cash. The ‘law’ of risk and return remains valid in the 21st century.”

In an environment where accurate and accessible information is key to decision-making, FlexFunds continues to strengthen its service offerings for asset managers through platforms recognized at the institutional level. Now, Morningstar joins a group of top-tier providers, further enhancing the visibility and reach of investment vehicles (ETPs) under FlexFunds’ securitization program, the firm announced in a statement.

Starting in March 2025, qualitative and quantitative data on ETPs will be available on Morningstar Direct, an essential tool for institutional investors, as well as on Morningstar’s public website. This integration increases the exposure of investment vehicles, strengthens transparency, and provides access to advanced analytics on one of the most trusted platforms in the industry.

The combination of pricing providers offered by the FlexFunds program, including Morningstar, Bloomberg, LSEG Refinitiv, and SIX Financial, provides a comprehensive market view and helps asset managers build a public track record, enabling informed and strategic decision-making.

DWS has expanded its Xtrackers product range, enabling investment in a broadly diversified selection of bonds with similar maturities, by adjusting the investment objectives and names of two existing fixed-income ETFs. The new Xtrackers II Rolling Target Maturity Sept 2027 EUR High Yield UCITS ETF invests for the first time in high-yield corporate bonds with a specific maturity.

According to the asset manager, since the bonds remain in the ETF portfolio until maturity, price fluctuations are reduced for investors who stay invested until September 2027. To achieve this, the ETF now tracks the iBoxx EUR Liquid High Yield 2027 3-Year Rolling Index. This index includes around 80 liquid high-yield corporate bonds denominated in euros, with credit ratings below Investment Grade, according to major rating agencies. As a result, investors bear a higher credit and default risk compared to investing in Investment Grade bonds. In return, according to the firm, “there is an opportunity to achieve a significantly higher aggregate yield at maturity, estimated at around 5.3% as of February 17, 2025, for the ETF’s portfolio.”

They also state that all bonds in the index have an initial maturity date between October 1, 2026, and September 30, 2027. Additionally, to provide greater flexibility, the ETF’s target maturity will be “extended” in the future. This means that the ETF will not be liquidated at the end of its term in September 2027, and the fund’s assets will be paid out to shareholders. Instead, the assets will be reinvested in bonds with a maturity of approximately three years.

“By expanding our current range of target maturity ETFs with an innovative product in the high-yield bond segment, we aim to offer investors the opportunity to generate attractive mid-term returns in the current environment of declining interest rates,” says Simon Klein, Global Head of Sales for Xtrackers at DWS.

The asset manager also highlights that they offer the Xtrackers II Target Maturity Sept 2029 Italy and Spain Government Bond UCITS ETF. In this case, the underlying index has also been modified for this ETF. “It now provides access to Italian and Spanish government bonds maturing between October 2028 and September 2029. Like all Xtrackers target maturity ETFs, these new products combine the advantages of fixed-income securities—predictable redemption at maturity—with the benefits of ETFs, such as broad diversification, liquidity, and ease of trading,” they state.

The 21st century is nearing its first quarter, and Global X has already drawn key lessons from this period: the U.S. economy and markets tend to be resilient.

The firm highlights several examples—the dot-com bubble, the global financial crisis, and COVID-19—all of which occurred since the turn of the century, yet the S&P 500 has quadrupled in value. “We keep this lesson in mind as we enter 2025 with a mix of optimism and uncertainty,” says Global X, noting that investor confidence and consumer expectations are improving, even as questions persist about economic policy and GDP growth is expected to slow.

Just like last year, Global X believes economic growth may once again surprise to the upside, supporting further market gains. However, the key drivers of growth this time will likely be different. “Some market participants argue that broad equity valuations look stretched, but in our view, fund flows suggest that investors remain willing to embrace risk assets,” they state. They add that broader market participation, improving profit margins, and continued earnings growth “could further lift equity valuations.” Conversely, they see fixed income as potentially “stuck in limbo due to interest rate volatility, which may force investors to be more creative and seek differentiated strategies.”

The strength of the services sector and corporate investment from large tech firms helped drive stronger-than-expected economic growth in 2024. However, Global X warns that economic uncertainty is likely to remain high, given the trade-offs and net effects of lower taxes, higher tariffs, reduced immigration, increased stimulus, and lighter regulation. That said, a manufacturing sector recovery, combined with renewed investment in small and mid-cap companies, could extend the mid-cycle expansion, leading to broader market participation and higher valuation multiples.

As a result, Global X will focus in 2025 on growth themes tied to U.S. competitiveness that still appear reasonably priced.

Building Portfolio Resilience in 2025

Equities and risk assets may be poised for another strong year, according to Global X. However, “the unique set of economic and political circumstances will likely warrant a more targeted approach in 2025.” A portfolio strategy aligned with key themes related to U.S. competitiveness “can provide reasonable upside and a degree of insulation from potential volatility.” The firm’s top investment themes include:

1. Infrastructure Development

A core part of the U.S. competitiveness narrative is the ongoing infrastructure renaissance. Construction, equipment, and materials companies have benefited from infrastructure-related policies and are positioned to gain from approximately $700 billion in additional spending over the coming years. Despite strong performance in recent years, these companies still trade at valuation multiples below the S&P 500. Moreover, traditionally rigid industries are adopting new technologies and practices, which could help expand profit margins.

2. Defense and Global Security

A series of interconnected global conflicts is creating new challenges for the U.S. and its allies. These evolving threats are expected to be persistent and unconventional, driving demand for new tactics, techniques, and technologies. Global defense spending, which reached $2.24 trillion in 2022, is projected to grow 5% in 2025, while defense company revenues are expected to rise nearly 10%, with profit margins improving from 5.2% to 7.6%. Compared to traditional defense platforms—such as battleships and fighter jets—lower-cost solutions like AI-driven defense systems and drones are expected to boost profitability, alongside greater automation in production processes.

3. Energy Independence and Nuclear Power

Even before AI-driven growth, energy demand was expected to rise sharply—and those forecasts have only increased. Fossil fuels will remain an essential part of the energy mix, but cost-effective and environmentally friendly alternatives will be critical to meeting surging demand. The tech sector has turned its attention to nuclear power, with many major companies announcing plans to utilize existing facilities or build small modular reactors (SMRs). Beyond the U.S., Japan, Germany, and Australia are expected to expand nuclear capacity, driving strong demand for uranium.

Selective Income Strategies for 2025

Income-focused investors may need to adopt a more selective approach in 2025, according to Global X, “given political uncertainty and potential interest rate volatility.” Many fixed-income instruments may underperform in a volatile rate environment, particularly long-duration assets. To minimize interest rate risk, Global X suggests equity-based strategies that could provide income with less sensitivity to rate fluctuations:

1. Covered Options Strategies

Equity-based covered options strategies can generate stable income while limiting direct exposure to interest rate movements. While the underlying asset may still fluctuate with the overall market (and indirectly with rate volatility), these strategies are not directly impacted by interest rate risk like traditional fixed income. Additionally, when rate volatility increases equity market volatility, option premiums tend to rise, maximizing income potential.

2. Energy Infrastructure Investments

Master Limited Partnerships (MLPs)—which own energy infrastructure assets such as pipelines—can generate steady incomewithout direct exposure to interest rate movements. These assets typically pay consistent dividends and have long-term supply contracts that stabilize cash flows. While their values can fluctuate with oil prices, their correlation to commodities is generally modest, as they do not extract or own the raw materials—they simply transport them. Additionally, real assets like commodities and energy infrastructure are often viewed as inflation hedges.

3. Preferred Stocks

Preferred stocks sit above common equity but below fixed income in the capital structure. They trade at par value and pay fixed or floating dividends. While investors are not guaranteed payments, preferred shareholders receive dividends before common stockholders. Since they are issued at par with a predetermined payout structure, they can be sensitive to interest rates. However, because they carry more risk than bonds, they tend to offer higher yields.

Most preferred shares are issued by banks, which generate steady cash flows from net interest income. With potential financial sector deregulation and increased small-business lending, preferred stocks could become an attractive income option in 2025.