In presenting their outlooks for 2026, all international asset managers have devoted significant attention to artificial intelligence, both as an investment opportunity and as a key driver of economies and global growth.

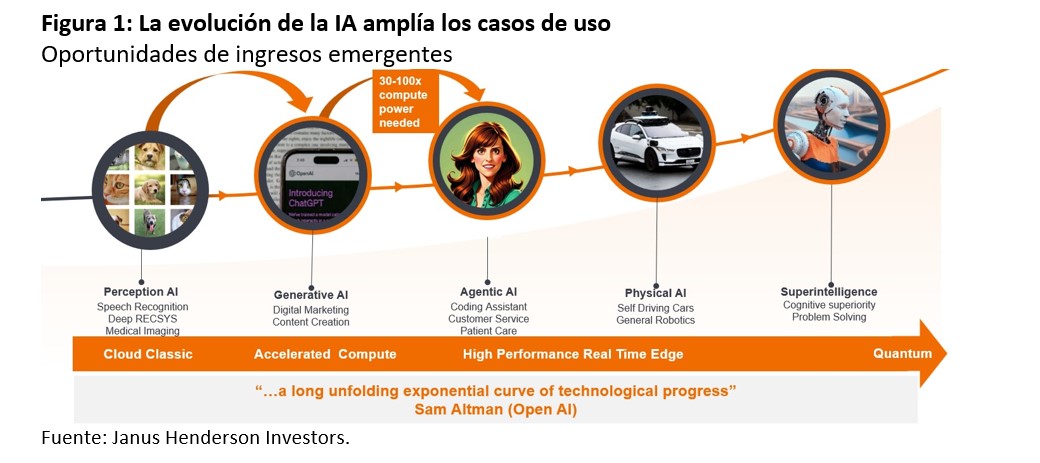

“AI is a long-term wave, not just a theme. A technological wave—AI is the fourth wave after mainframes, personal computers connected to the Internet, and the mobile cloud—is defined by the fact that it affects all aspects of the economy. It requires investment across every layer of the tech stack, from silicon—semiconductors—to platforms, devices, and models, and every company becomes, in some way, a user of AI. These waves take several years to evolve, and in the case of AI, the pace of capacity development is constrained by deglobalization, permitting, energy availability, construction limitations, and availability within the computing supply chain,” emphasize Alison Porter, Graeme Clark, and Richard Clode, portfolio managers at Janus Henderson.

According to Janus Henderson portfolio managers, there is a circular problem, as the limiting factor for demand in computing power has been the available capacity to train and develop new models. “As we move from generative AI to agentic AI, more reasoning and memory capacity is needed to provide greater context. This requires significantly more computing power to increase token generation (units of data processed by AI models). We are seeing areas such as physical AI rapidly developing, with the expansion of autonomous driving and robotics testing worldwide. In short, looking ahead to 2026 and 2027, we believe demand for computing power will continue to outpace supply,” they argue.

Are We in an AI Bubble?

In contrast to this highly positive scenario, investors remain attentive to the ongoing debate over whether we are currently in an AI bubble. According to Karen Watkin, multi-asset portfolio manager at AllianceBernstein, the defining feature of this bull market is its narrow leadership. “AI-driven technology companies have delivered extraordinary gains, creating a K-shaped market: a few large winners while many are left behind. This concentration drives index returns but introduces fragility. The U.S. economy is asymmetrically exposed: wealthier households hold most of the equity and sustain consumption, so an AI correction could impact spending and potentially lead the economy into a recession,” she explains.

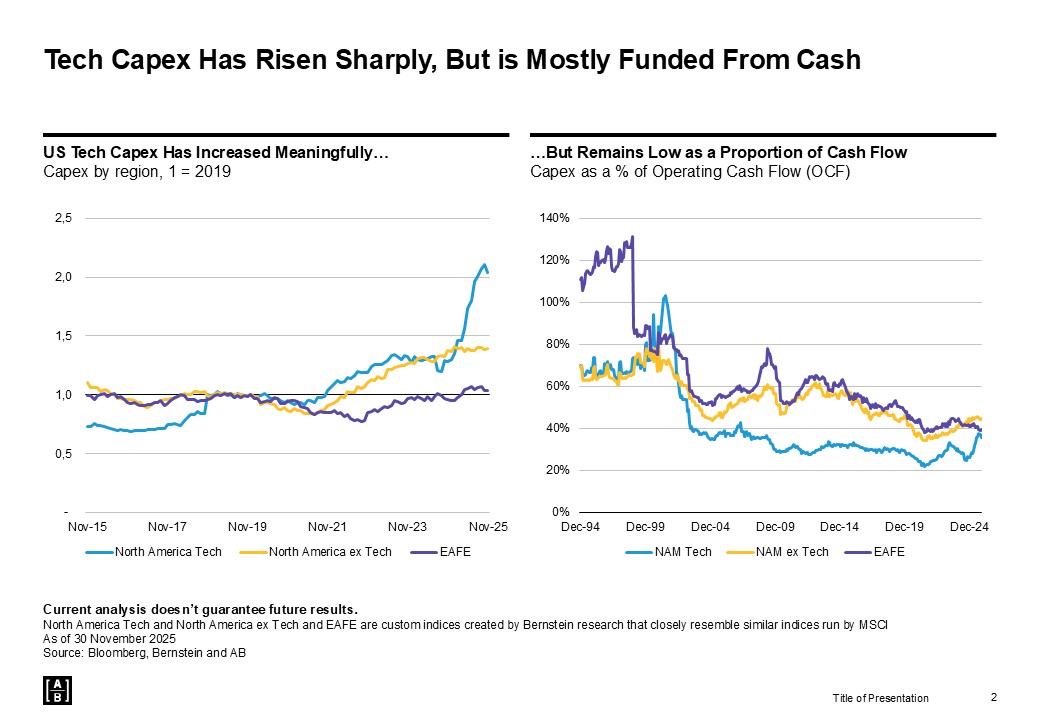

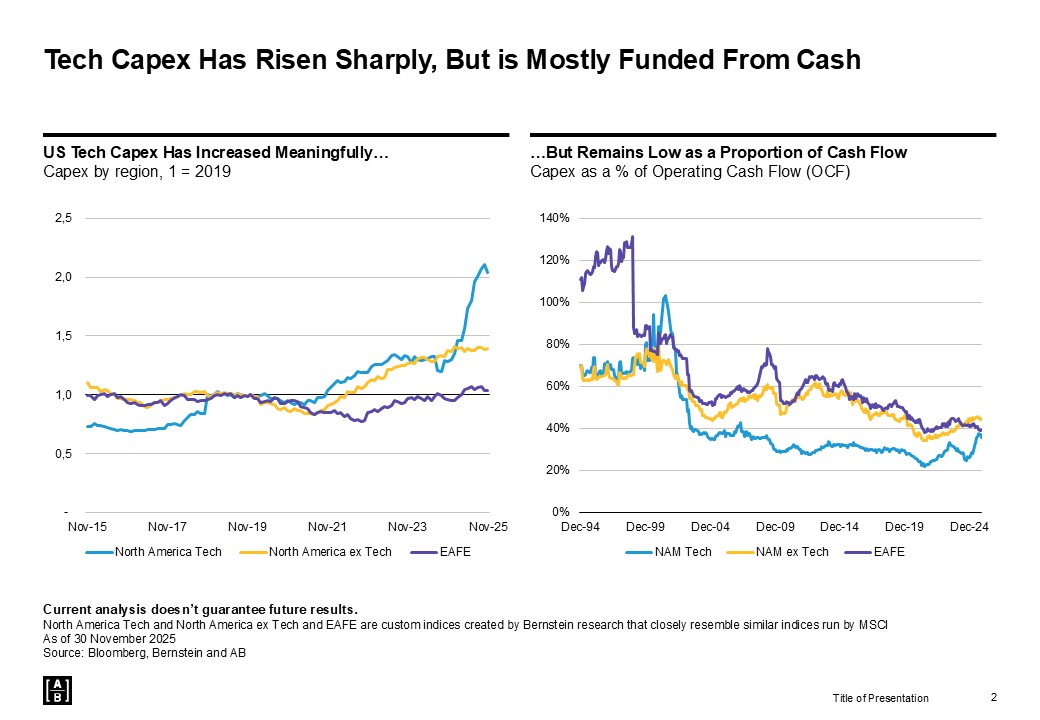

Watkin believes that, for now, fundamentals offer some reassurance: earnings growth—not just multiple expansion—has driven returns. According to her analysis, hyperscaler capex—though extraordinarily high—is largely funded by strong cash flows rather than debt, but signs of increasing leverage and debt issuance are being monitored. “We also observe more structural risks: circular funding patterns, such as repeated cross-investments and successive corporate transactions, which can introduce fragility. And while adoption trends are promising, imbalances between supply and demand, energy bottlenecks, and the risk of obsolescence could challenge the AI-driven economy,” she states.

The AllianceBernstein expert adds that elevated valuations do not guarantee poor short-term returns, but they do increase the risk of declines: “We believe that narrow leadership warrants greater diversification; asset classes such as low volatility equities can offer defensive exposure and attractive valuations, with a potential tailwind if yields fall.”

What Are the Implications of a Correction?

Until now, investment in artificial intelligence has been primarily financed through corporate cash flows and venture capital. However, as hyperscalers seek to sustain exponential growth in model size, data center construction, and chip supply, debt financing has begun to gain prominence once again.

With major U.S. equity indices becoming increasingly concentrated in AI leaders, in the view of the experts at Quality Growth (a Vontobel boutique), a significant correction could ripple through the economy not via layoffs or failed AI projects, but through the negative wealth effect caused by falling asset prices.

“This dynamic would be similar to what followed the dot-com bubble in 2000, when the decline in equity value disproportionately affected higher-income households and, consequently, overall consumer spending,” they explain.

In their view, a second transmission channel has already taken shape: capital expenditure in AI as a main driver of U.S. GDP. “By the end of 2025, technology-related capital expenditure (capex) is estimated to account for more than half of the quarterly growth in gross domestic product (GDP). This implies that the same force that has driven markets upward could become a drag if investment expectations are adjusted. In this way, AI has become both a tailwind and a potential vulnerability for the macroeconomic outlook in 2026,” conclude the team at Quality Growth.

Last Major Corporate Deal in the Asset Management Industry Before the End of 2025 Janus Henderson Group plc, Trian Fund Management, L.P. and its affiliated funds (Trian), and General Catalyst Group Management, LLC and its affiliated funds (General Catalyst) have announced that they have entered into a definitive agreement under which Janus Henderson will be acquired by Trian and General Catalyst in an all-cash transaction, with an equity valuation of approximately $7.4 billion. The investor group includes, among others, the strategic investors Qatar Investment Authority and Sun Hung Kai & Co. Limited.

Under the terms of the agreement, shareholders who do not already own or control shares through Trian will receive $49.00 per share in cash, representing an 18% premium over Janus Henderson’s unaffected closing share price on October 24, 2025, the last trading day before the initial proposal from Trian and General Catalyst was made public.

The Key Players

The asset manager recalls that Trian, an investment firm with extensive experience in investing and operating within the asset management sector, currently owns 20.6% of Janus Henderson’s outstanding shares and has been a shareholder since 2020, with board representation since 2022. For its part, General Catalyst is a global investment and transformation firm focused on applying artificial intelligence to enhance business operations. They note that this will be one of several transactions that Trian and General Catalyst teams have undertaken jointly.

Additionally, they clarify that, as a private company, Janus Henderson would continue to be led by the current management team, with Ali Dibadj as CEO, and would maintain its main presence in both London (England) and Denver (Colorado).

According to Janus Henderson, shortly after receiving the proposal from Trian and General Catalyst, the company’s Board of Directors formed a Special Committee, comprised of independent directors not affiliated with Trian or General Catalyst.

“The transaction was unanimously approved and recommended by the Special Committee after evaluating the deal with Trian and General Catalyst and completing a thorough review process. At the Special Committee’s recommendation, the Board subsequently approved the transaction by unanimous vote,” they stated.

Main Reactions

Following this announcement, John Cassaday, Chairman of the Board and Chair of the Special Committee, stated: “After a careful review of the proposed transaction and its alternatives, we have determined that this deal is in the best interest of Janus Henderson, its shareholders, clients, employees, and other stakeholders, and offers attractive certainty and cash value to our public shareholders, with a significant premium over the unaffected share price.”

Meanwhile, Ali Dibadj, CEO of Janus Henderson, said: “We are pleased with Trian and General Catalyst’s interest in partnering with us, which is a strong endorsement of our long-term strategy. Throughout our 91-year history, Janus Henderson has been both a public and private company at various times, and has never lost focus on investing—together with our clients and employees—in a more promising future. Through this partnership with Trian and General Catalyst, we are confident that we will continue investing in our product offering, client services, technology, and talent to accelerate our growth and deliver differentiated insights, disciplined investment strategies, and top-tier service to our clients. This transaction is a testament to Janus Henderson’s employees worldwide, who have executed our strategy of protecting and growing our core business, amplifying our strengths, and diversifying where it makes sense, always putting our clients first.”

Nelson Peltz, CEO and Founding Partner of Trian, added: “Our team at Trian has successfully invested in and driven growth at many iconic public and private companies over the years. As a significant shareholder of Janus Henderson and with board representation since 2022, we are proud of the company’s performance in recent years, led by Ali and his outstanding team. We see a growing opportunity to accelerate investment in people, technology, and clients. The partnership with General Catalyst enables us to bring to Janus Henderson our shared entrepreneurial spirit and complementary strengths in operational excellence and technological transformation. We look forward to working closely with Ali and the JHG team, as well as with Hemant and the General Catalyst team, to build a best-in-class business.”

From General Catalyst, its CEO Hemant Taneja added: “We see a tremendous opportunity to partner with Janus Henderson’s management team to enhance the Company’s operations and customer value proposition through the use of AI, in order to drive growth and transform the business. We are also excited to partner with Trian, with whom we share a long-term vision for success in creating additional value for Janus Henderson, a top-tier organization.”

Finally, Mohammed Saif Al-Sowaidi, CEO of QIA, stated: “QIA is pleased to be part of this agreement to take Janus Henderson private. As a long-term financial investor, we look forward to working with our partners at Trian and General Catalyst to support Janus Henderson in the next phase of its impressive growth story.”

Transaction Details

They explained that the transaction is expected to be completed by mid-2026 and is subject to customary closing conditions, including obtaining the relevant regulatory approvals, client consents, and approval from Janus Henderson shareholders.

The transaction will be financed in part through investment vehicles managed by Trian and General Catalyst, backed by funding commitments from global investors, including Qatar Investment Authority and Sun Hung Kai & Co. Limited, as well as MassMutual and others, along with the retention of Janus Henderson shares currently held by Trian and related parties.

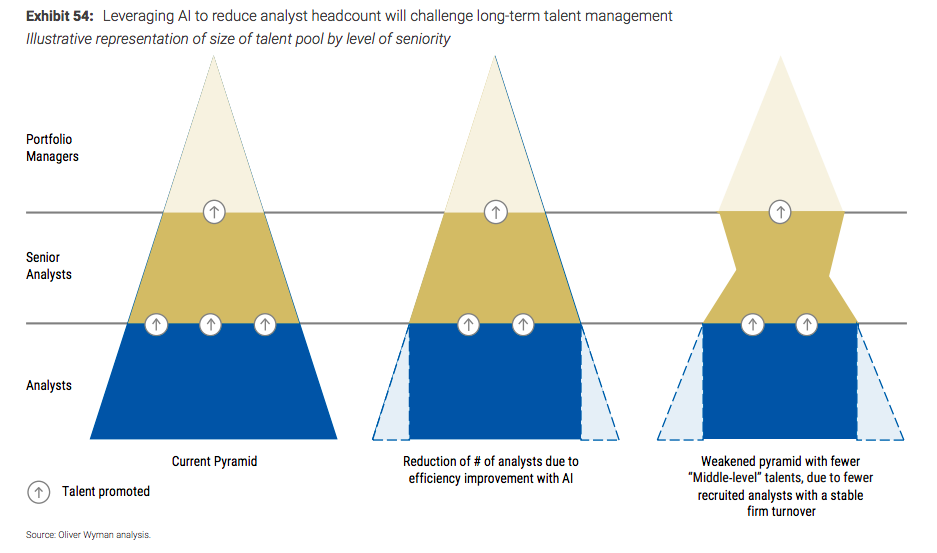

According to the latest report by Morgan Stanley and Oliver Wyman, AI tools and generative automated models have shifted from tasks typically handled by the middle and back offices—such as report preparation and operational controls—to front-office functions.

“While these advancements initially benefited employees by gradually enhancing their productivity, they are now starting to translate into efficiency gains for the company, with experiences indicating up to a 30% improvement in analytical activities,” the document states. This evolution represents an opportunity due to the efficiency it brings, but also a challenge in how to leverage that efficiency and integrate it with professionals in the sector.

The Paths of AI-Driven Efficiency

The report outlines two paths companies can take to capitalize on this efficiency. First, it suggests reinvesting efficiency gains to enhance analysis, arguing that “AI frees up analysts’ time, allowing them to increase the depth and breadth of research, which ultimately enables stronger alpha generation.” Second, it points to optimization as a way to create leaner cost structures.

“Instead of reinvesting time, some companies are reducing their analyst base and relying on AI to handle repetitive and lower-value tasks. Reinvesting efficiency has the advantage of maintaining a stable base of analysts without disrupting the traditional career path of analysts. However, it is likely to reshape their role and the associated required skills: proficiency in AI and automation tools, and the ability to generate original insights based on AI-generated results. It also challenges the learning curve for junior analysts, as they would be required to oversee AI-generated outputs without first mastering the underlying analysis themselves,” the report notes.

Furthermore, it acknowledges that reducing the number of junior analysts may provide immediate cost savings but warns that, in the medium term, it creates the challenge of the “hourglass effect”: a narrowing at the mid-senior level, which weakens the succession pipeline for senior analyst and portfolio management positions. “Just as many firms are actively seeking to ‘juniorize’ teams to control costs, this exacerbates the seniorization trend. Already, portfolio managers are becoming increasingly senior, with 50% of them having more than 25 years of experience (compared to 39% in 2020),” the report states.

“In This Context, Human Resources Functions Must Adapt Quickly and Work Hand-in-Hand With Investment and Technology Teams to Redesign Workforce Planning, Integrate AI Capabilities Into Learning Pathways, and Structure Sustainable Succession Strategies That Ensure Long-Term Organizational Resilience,” the report proposes in its conclusions.

Attracting and Retaining New Talent

The document argues that the growing influence of AI in this industry requires asset managers to seek new and scarce skill sets outside the core group of finance graduates. Furthermore, as both the asset management and wealth management industries shift toward a more client-centric model, each must increasingly cultivate a workforce that excels in relationship-building, emotional intelligence, and cultural sensitivity.

“While this broadens the scope of potential hires beyond traditional financial and mathematical backgrounds, it also forces asset managers to compete for these more transferable skills with broader industries (particularly tech companies). Therefore, firms must renew their value proposition to attract this wider audience,” the document states.

In addition to attracting and retaining talent, the conclusions assert that HR departments in investment firms need to rethink their approaches to people development in order to adapt to the hybrid “human + AI” mode of work. As explained, “teaching practical AI knowledge must be balanced with building stronger judgment skills. Leaders, in particular, may need support in change management, cross-functional collaboration (investment, data, engineering), and the ethical use of AI.”

In this regard, the report presents a clear proposal: “Rotations, hands-on AI labs, and mentorship pairings between senior portfolio managers and technologists can be used alongside traditional HR approaches to preserve deep expertise while building the leaders of the future.”

Finally, the report emphasizes that scaling AI within traditionally conservative asset and wealth management cultures will require a deliberate cultural shift. “Existing cultural profiles will shape how quickly and widely AI is adopted, so tailoring interventions to current and lived cultures will be more effective. Designing the workforces and cultures of the future will also require activating the right incentive levers and creating regular rituals, such as recognizing AI-driven improvements in performance reviews, internal showcases of AI achievements, and leaders visibly modeling new behaviors,” the report concludes.

The Aspirations of Heirs, the Challenges of New Generations, and Increased Longevity Are the Three Main Issues Billionaires Seek to Address to Sustain Their Wealth. According to the Billionaire Ambitions Report 2025, prepared by UBS, this client profile wants their children to succeed independently and places more importance on personal achievement than on reliance on inherited wealth.

In an era in which entrepreneurs often appoint professional managers or sell their businesses rather than pass them on to the next generation, independent success is particularly valued. In this context, the report reveals that 82% of billionaires with children hope to see them develop the skills and values needed to succeed on their own, rather than relying solely on inherited wealth. In addition, 67% hope their children will pursue their own passions, and 55% want them to use their wealth to make a positive impact in the world.

At the same time, a significant minority expects their heirs to continue the family business: more than four in ten (43%) state they would like to see their children continue growing the family’s operating company, brand, or assets, thereby ensuring the continuity of the family legacy.

A New Social Reality

This goal faces two challenges linked to today’s societal dynamics: the values of new generations and increased longevity. On the first factor, the report notes that billionaires see younger generations as more inclined to value holistic aspects: they say the new generations place greater importance on technological advancement and innovation, lifestyle, and impact investing than their own generation.

According to the survey, 75% consider technology and AI to be a pressing challenge that must be addressed, while 55% point to climate change. “However, opinions vary by region: billionaires in EMEA prioritize climate change and poverty and inequality; those in the Americas focus on technology and AI followed by education; and those in Asia-Pacific are primarily concerned with technology and AI,” the document clarifies.

Regarding the impact of longevity, billionaires believe that living longer may complicate the way they manage family wealth. In a shift that could have far-reaching implications, more than four in ten (44%) expect to live significantly longer than just 10 years ago, and more than a third (37%) expect to live somewhat longer.

“As a result, more than half (58%) of those who expect to live longer plan to regularly review and update their wills, trusts, and beneficiaries. Over four in ten (42%) plan to make—or have already made—longer-term investments. Family offices are also likely to take on a more prominent role in family affairs as the first generation ages,” the report concludes.

Asset Allocation of Billionaires

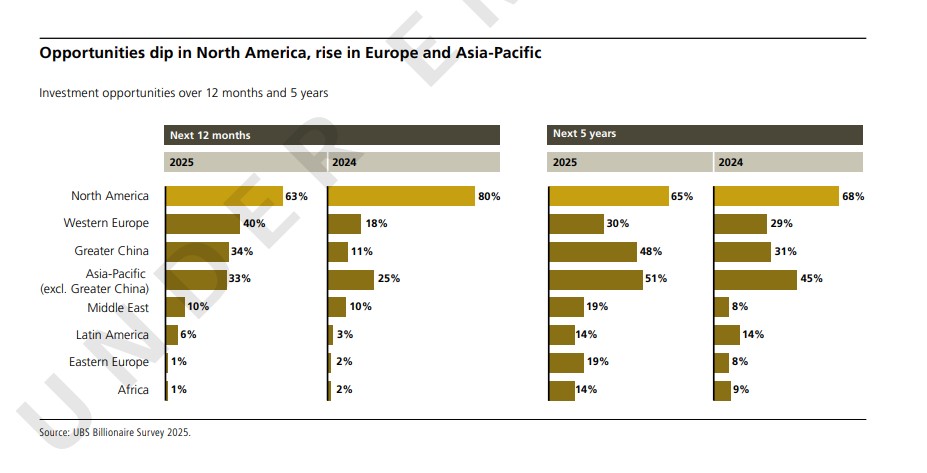

The big question is what impact these trends are having on asset allocation and how billionaires invest. The UBS report reveals that despite market volatility in 2025, North America remains the leading investment destination (63%), followed by Western Europe (40%) and Greater China (34%). 42% of billionaires plan to increase their exposure to emerging market equities, while more than four in ten (43%) are considering expanding their exposure to developed markets.

Notably, over the next 12 months, nearly two-thirds (63%) of respondents believe North America offers the greatest profit opportunity, down from four in five (80%) last year. “Looking at a five-year horizon, the proportion is slightly higher (65%), almost unchanged from the 2024 survey (68%),” UBS notes.

The report states that as the short-term appeal of North America has waned, that of other major destinations has grown: 40% believe Western Europe offers one of the greatest 12-month opportunities, ahead of Greater China (34%) and Asia-Pacific (excluding Greater China) (33%). “All of these represent significant increases compared to 2024, when fewer than one in five (18%) saw potential in Western Europe, just over one in ten (11%) in Greater China, and a quarter (25%) in Asia-Pacific (excluding Greater China),” the report explains.

Asia and Private Markets

Looking five years ahead, around half of billionaires view Asia-Pacific (excluding Greater China) (51%) and Greater China (48%) as among the most attractive investment destinations. “Perhaps reflecting their widely reported economic and political challenges, just under a third (30%) lean toward Western Europe,” UBS points out.

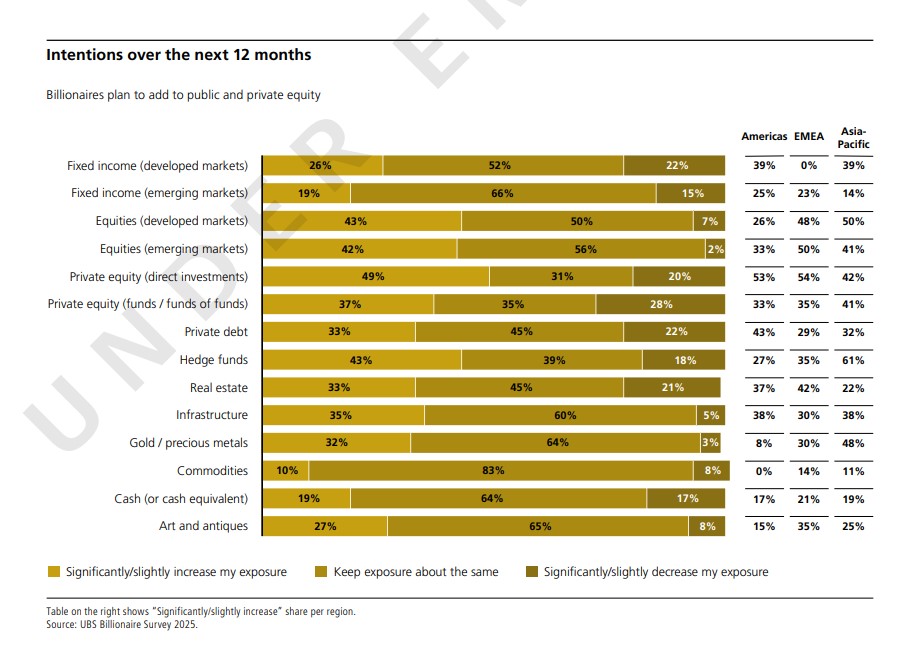

The report notes that in a context of renewed confidence in Greater China and Asia-Pacific overall, more than four in ten (42%) billionaires plan to increase their exposure to emerging market equities over the next 12 months, where returns have begun to recover after a prolonged period of underperformance compared to developed markets. In contrast, almost none (2%) of the billionaires surveyed intend to reduce their exposure. Meanwhile, in developed market equities, more than four in ten (43%) intend to increase their exposure, although nearly one in ten (7%) plan to reduce it.

Views on Private Markets

Another key finding of the report is that views on private markets are mixed: 49% plan to increase their direct exposure to private equity, while 20% plan to reduce it. 33% intend to increase exposure to private debt, while 22% aim to reduce it. As for hedge funds, more than four in ten (43%) billionaires intend to raise their exposure (compared to 18% who plan to reduce it). According to the report, “some long-short equity hedge funds may be well positioned to benefit from the current wide and persistent divergence in individual stock performance.”

Meanwhile, infrastructure and gold / precious metals are two areas billionaires are turning to in an effort to diversify their portfolios. “More than a third (35%) are increasing their exposure to infrastructure and nearly a third (32%) to gold / precious metals. Fixed income remains a relatively stable area for now. Most billionaires plan to keep their exposure to developed market fixed income (52%) and/or emerging market fixed income (66%) unchanged over the next 12 months,” the report states.

The Global Capital Markets Operate Under the Dominance of a Single, Dangerous Narrative: The Euphoria Over Artificial Intelligence in the United States. According to international asset managers, this boom has driven indexes to new highs and delivered extraordinary returns. However, they acknowledge that this same euphoria has sown the seeds of systemic risk, creating levels of market concentration not seen in decades.

The interdependence and high valuations of this select group of companies call for rigorous analysis and a strategic response. For this reason, investment firms argue that adopting a proactive global diversification strategy is essential for the coming year. In this regard, they maintain that it is not about abandoning the market, but about rebalancing the portfolio to mitigate the growing risks inherent in the concentration in U.S. technology, while at the same time capturing significant value opportunities emerging in other regions and asset classes.

The Reasons for Vertigo

A thorough analysis of the foundations of the current U.S. bull market is a strategically essential exercise. Asset managers agree that while the euphoria surrounding AI is partially justified by its transformative potential, it may conceal structural vulnerabilities that prudent investors cannot afford to ignore. In this sense, the data show that, since the launch of ChatGPT, only 41 AI-linked stocks account for 75% of the total gains in the S&P 500 index.

“We do not see an AI bubble, but rather a continuing AI boom that could generate significant productivity gains in the coming years,” acknowledges Benjardin Gärtner, Global Head of Equities at DWS. In his view, although setbacks may arise along the way—as with any technological revolution—the growth story appears to remain intact.

For Raphaël Thuin, Head of Capital Markets Strategies, and Nina Majstorovic, Product Specialist in Capital Markets Strategies at Tikehau Capital, the issue is that over the past decade, the profits of technology companies have grown faster than the market, thanks in particular to online advertising, artificial intelligence, and the cloud. They note that Nvidia’s latest results are a perfect example of this and confirm the strength of the AI cycle.

“Nonetheless, doubts remain about the sustainability of demand, visibility beyond the coming quarters, and the quality of the order backlog. The market is debating a possible marginal slowdown in innovation and still uneven return on investment (ROI). Lastly, the circularity of financing, the increased use of debt (including private debt), and the energy constraints required for mass deployment are fueling some mistrust toward the sector,” they explain.

However, despite these cautionary points, they consider AI to remain a structural megatrend. “Its adoption is tangible in terms of usage, and early signs of increased productivity are beginning to emerge. We believe the hyperscalers have solid balance sheets and the cash flow needed to finance the investment cycle. Therefore, it seems appropriate to maintain long-term exposure, while favoring a selective approach focused on sectors with demand visibility, pricing power, and the capacity to generate cash flow to cover investments. At the same time, it will be important to monitor the effective transformation of order books, financial discipline, investment trajectory, and access to and cost of energy,” argue the experts at Tikehau Capital.

Ideas for Diversification

When considering diversification, the experts at boutique firm Quality Growth (Vontobel) point out that value stocks outside the U.S. have matched the performance of the Nasdaq 100, often seen as the benchmark for high-growth tech companies. “Much of this global value resurgence is explained by the revaluation of cyclical sectors, especially banking. Investors are pricing in greater profit potential, improved capital return policies, and more favorable fiscal and monetary outlooks,” the firm explains.

Among their favorite assets are European banks, which have been notable beneficiaries of the current context. “For the first time since the global financial crisis, their price-to-book ratios have surpassed the 1x level—a symbolic and relevant shift in investor sentiment. While there are reasons for this, we observe that since 2024 European value stocks have increased their multiples, while European growth and quality companies have not. Therefore, we now identify significant opportunities in Europe among high-quality growth companies, particularly those with strong fundamentals and resilient business models,” they add.

At Janus Henderson, they argue that global equity investors should take Europe into account. “Excluding the United Kingdom, Europe is the second-largest component of the MSCI All Country World Index, behind the United States, and is often underweighted in portfolios. Although the EU’s planned initiatives may not achieve the additional 19.6% increase in total European GDP forecasted, the ambition clearly marks a break with the austerity era, with governments now actively investing in growth and security,” they state in support of the Old Continent.

In equities, from a diversification perspective, the asset manager maintains that Europe is less sector-concentrated than the U.S. and could also offer greater income-generation opportunities. “The dividend yield of the MSCI Europe Index is 3.3% compared to 1.2% for the S&P 500® Index. History shows that a higher dividend yield can translate into higher real returns. Over a five-year period, the median return of stocks with a dividend yield above 3% outperformed, on average, by a minimum of 189 basis points (bps) compared to stocks with a yield below 2%,” they argue.

Finally, Luca Paolini, Chief Strategist at Pictet AM, sees potential in European markets in domestically oriented stocks, particularly mid-caps. “Adjusted for sector composition differences, Europe trades at a 25% discount to the U.S., compared to the typical 10% before COVID and the war in Ukraine—this could be a positive surprise. European stocks may experience significant gains if just part of the promised German public spending begins to flow. High-quality companies’ stocks, after a prolonged period of low returns, are likely to resume their role of protecting portfolios during periods of market volatility, against adverse macroeconomic or geopolitical surprises,” says Paolini.

When discussing sectors, the Pictet AM expert considers pharmaceuticals especially promising, as most of the bad news on drug pricing has already been priced in, and the increase in mergers and acquisitions and the moderation of economic growth support unlocking significant value. “We also like technology, financials, and industrials, with strong earnings growth. In addition, the UK market offers protection against stagflation risks and an attractive dividend yield,” he adds.

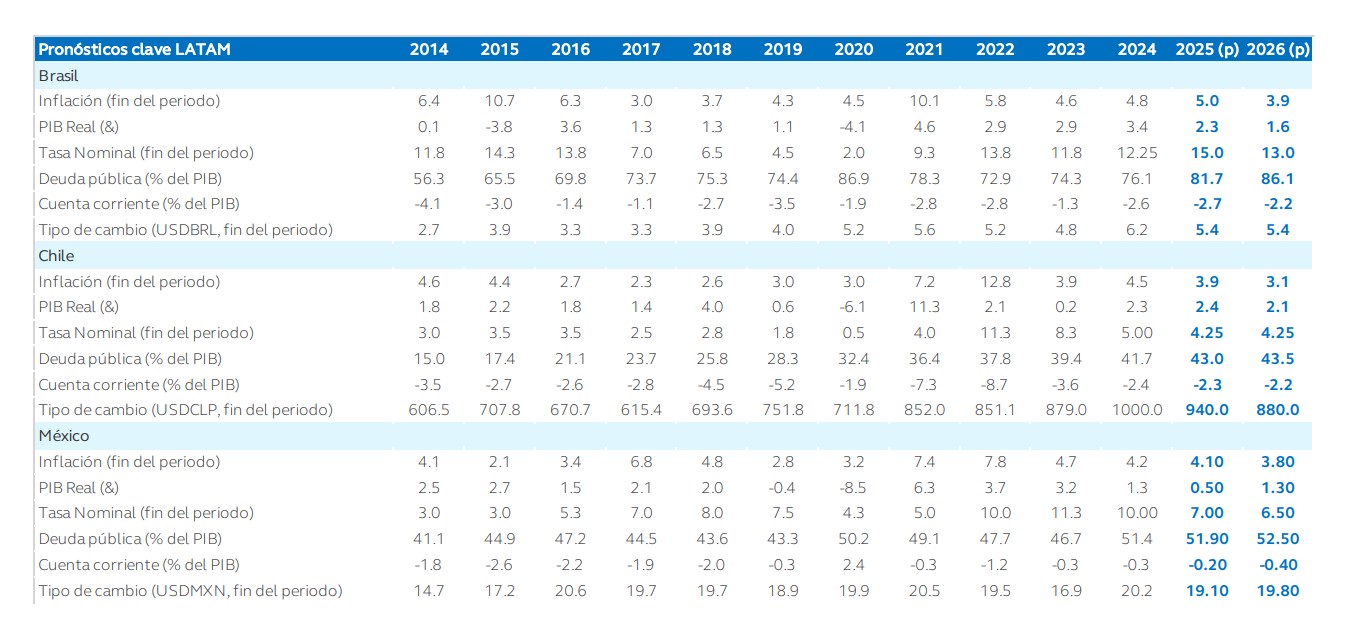

Looking back on 2025 in the Latin American region, we see that the main economies of Latin America successfully navigated a period marked by rising trade tensions and global uncertainty. According to experts’ views, the main takeaway from the year is that, except for Brazil, the impact of tariffs imposed by the Trump Administration has been much better than expected.

“Beyond the fact that the region remained largely unaffected by the direct impact of U.S. tariff pressures, favorable terms of trade and a still-tight labor market sustained consumption and explain the resilience of economic activity throughout the year. The most relevant countries are expected to grow by more than 2% in 2025 and, although Mexico would grow by only 0.5%, it avoided a recession and has seen upward revisions in recent months,” highlight the authors of the outlook report prepared by Principal Asset Management LATAM, including Marcela Rocha, chief economist, who presents the 2026 Economic Outlook.

Monetary and Fiscal Policy

One of the defining features of the region’s economy is that, while the rest of the world continued to struggle to control inflation, Latin American countries have mostly benefited from a synchronized cycle of global monetary easing and a weaker dollar, which strengthened local currencies and supported a significant disinflation trend in recent months. In fact, with the exception of Brazil, most central banks had room to cut policy interest rates.

“In 2026, the outlook changes. While Mexico’s GDP is expected to accelerate, most of the region will face slower growth. With economic activity projected below potential, Brazil stands out as the only country with significant room for further rate cuts. In the rest of the region, the persistence of core inflation limits the scope for further monetary easing, and Mexico’s trajectory will largely depend on the policy decisions of the Federal Reserve,” note analysts from Principal AM.

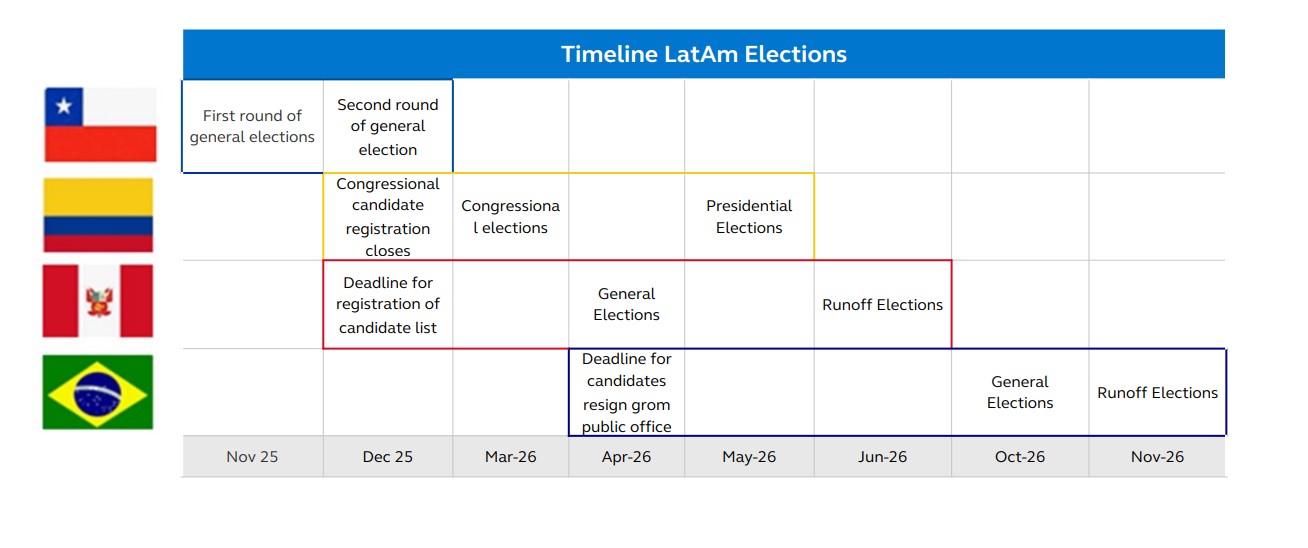

The second conclusion presented in the asset manager’s report is that long-standing concerns persist regarding the sustainability of public finances. However, they explain that “a packed electoral calendar in the coming quarters opens the door to advance the much-needed policy changes, particularly in structural reforms and fiscal management. Chile, Peru, Colombia, and Brazil will hold elections in the next 12 months, which will shape part of the outlook. In Mexico, the scenario will also depend on the outcome and timing of the USMCA negotiations.”

Brazil and Mexico: The Protagonists

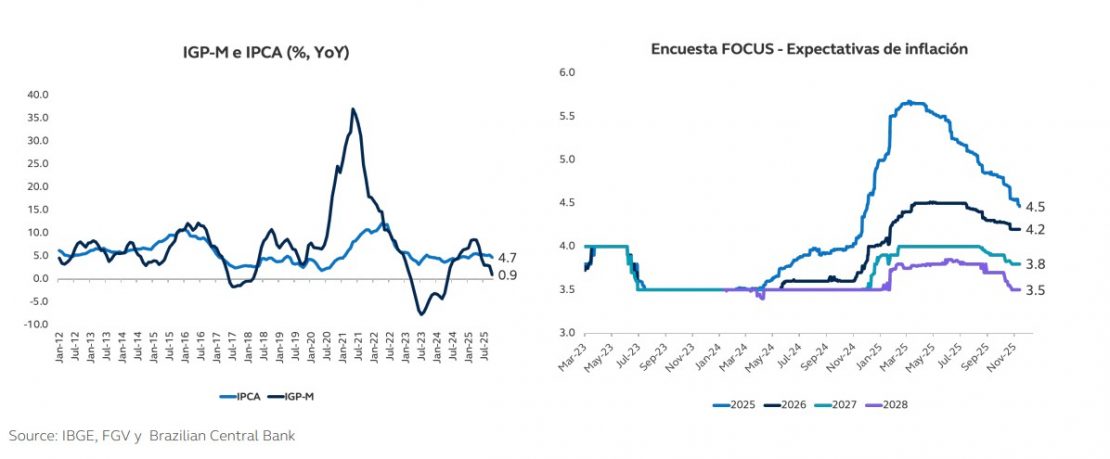

As the asset manager points out, Brazil and Mexico will play a particularly prominent role in the coming year. According to their estimates, the Central Bank of Brazil would be ready to begin a rate-cutting cycle, but the elections will shape the outlook. “In 2025, Brazil’s economic landscape was defined by high volatility and uncertainty, with the first part of the year marked by the lingering effects of the 2024 fiscal debate. Additionally, as inflation expectations also moved upward, well above the 3% target, the Central Bank was forced to halt its rate-cutting cycle and resume tightening, bringing the benchmark rate to 15%. However, more recently, the effects of higher rates have begun to appear in domestic data, with early signs of economic slowdown in credit and confidence indicators,” summarizes the asset manager.

According to their analysis, heading into 2026, “we expect the economic outlook to be determined by the balance between the pace of economic slowdown and the timing of the Central Bank’s monetary easing cycle.” They also see it as likely that the political environment will gain relevance throughout the year, with the presidential election positioned as the key event toward the end of 2026.

“In terms of growth, after several years in which GDP consistently surprised to the upside and operated above potential, we anticipate a moderate slowdown in the Brazilian economy. Given the significant monetary tightening already implemented, we expect GDP to slow from 2.3% in 2025 to 1.6% in 2026. On the inflation front, given the recent string of positive surprises in the short term, the balance of risks for 2026 appears slightly tilted to the downside,” they note.

Regarding Mexico, the asset manager warns that the review of the USMCA will be key to boosting investment and unlocking potential. In its year-end assessment, it acknowledges that the country enters 2026 having avoided the recession that, at the beginning of 2025, seemed almost inevitable. “The economy faced a combination of shocks: the slowdown at the end of 2024, increased uncertainty surrounding the new government, the need for fiscal consolidation, and a weaker external environment marked by the U.S. slowdown and the resurgence of trade tensions under President Trump. Despite this challenging scenario, the Mexican economy showed resilience,” the report summarizes.

In this context, the USMCA review takes on particular relevance. According to the asset manager, “USMCA exemptions shielded Mexican exports from the tariff shock that hit other trading partners, allowing Mexican goods—particularly non-automotive manufactured goods—to gain market share in the U.S. This boost in external demand generated a positive surprise in activity at the beginning of 2025, helping the economy avoid falling into recession even as domestic demand remained weak.”

Although the report notes that its forecast for 2026 is for a moderate rebound in economic activity, it also states that the main risk to this scenario is the upcoming USMCA review, as it introduces an additional layer of political uncertainty that could temporarily weigh on investment and markets. “Mexico has already taken visible steps to demonstrate its commitment to the North American framework, including preparing negotiation materials and selectively imposing tariffs on Asian—especially Chinese—goods. We expect a favorable trilateral outcome, though with episodes of volatility as negotiations progress. A constructive resolution with the United States remains the most important catalyst to reduce uncertainty and trigger increased investment in 2026,” the asset manager concludes.

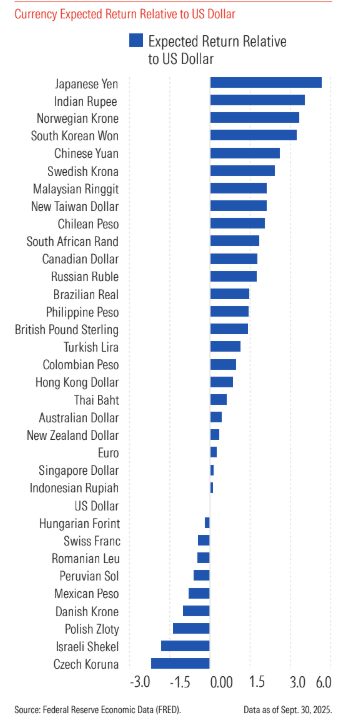

The U.S. dollar is experiencing its weakest year in over a decade. As of September 2025, the dollar index, which measures its value against other major currencies, had fallen by nearly 10%. In other words, the currency declined even further against the euro, Swiss franc, and yen, and dropped 5.6% against major emerging markets. This is according to Morningstar’s 2026 Global Outlook Report, prepared by Hong Cheng, Mike Coop, and Michael Malseed.

According to Morningstar analysts, this weakness stems from a combination of structural and cyclical factors. Among them are fiscal concerns, with sustained debt growth and the impact of the so-called “Big Beautiful Bill,” as well as reduced confidence in U.S. economic growth relative to other regions. In addition, political uncertainty—which affects perceptions of the Fed’s independence and the country’s trade decisions—has also influenced investor confidence. Changes in global capital flows and increased hedging of dollar-denominated assets have added pressure on the currency.

Despite these declines, experts stress that this does not represent a structural collapse. “The dollar remains the dominant international reserve and settlement currency and retains its appeal as a safe haven in times of stress. In fact, only nine of the 34 major developed and emerging market currencies analyzed are currently more overvalued than the dollar, indicating that it still holds relevant value for investors,” they explain.

For those investing from the U.S., Morningstar recommends taking advantage of this phase to increase exposure to international markets. “This not only allows for portfolio diversification but also offers the possibility of benefiting from the appreciation of other currencies against the dollar. For investors outside the U.S., maintaining exposure to the dollar remains relevant, especially in portfolios with a high weighting in U.S. equities. Currency hedging management can help stabilize returns, although the costs of this strategy vary: they are nearly zero in the United Kingdom, around 4% annually in Japan or Switzerland, and positive in countries with high interest rates, such as South Africa,” the document states.

Finally, the analysts agree that the weakness observed in 2025 marks a turning point in the long cycle of dollar strength, but not its structural decline. For investors, this phase represents an opportunity to strengthen global diversification and consider an increasingly relevant role for other currencies and regions in future returns. The general recommendation is to maintain a balanced approach, combining dollar exposure with international investments, to optimize the risk-return profile of portfolios.

In a conversation with Funds Society, U.S. economist Daniel J. Mitchell, a leading expert on tax and public spending issues, analyzed the pillars of the new Donald Trump cycle in the White House, fiscal tensions, the role of trade, and the outlook for 2026.

From his point of view, next year the growth of the world’s largest economy will be “modest” in terms of investment and employment due to the “suicidal protectionism” implemented by the “populist” leading the U.S. government, who acts like “Santa Claus,” thinks only in the short term, and neglects long-term growth.

The long-term damage to the economy will be greater, and fiscal risks will increase. The “spending spree will inevitably lead to future tax hikes,” and the risk of another government shutdown in 2026 is rising, he warned.

With a Ph.D. in Economics from George Mason University and a Master’s and Bachelor’s degree in Economics from the University of Georgia, Mitchell began his career in the United States Senate, where he worked as an advisor to Senator Bob Packwood (Oregon) and to the Senate Finance Committee. He also participated in the Bush/Quayle transition team in 1988.

In 1990, he joined The Heritage Foundation, where he developed an extensive career analyzing and promoting fiscal policy, advocating for income tax reform.

In 2007, he joined the Cato Institute as a senior fellow, a position he still holds, focusing on fiscal policy research, flat tax implementation, and the defense of international tax competition. He is also co-founder and president of the Center for Freedom and Prosperity, an organization dedicated to protecting and promoting global tax competition.

A More Protectionist and Interventionist Trump

Mitchell believes that the second term of the U.S. president retains traits of the first but with more pronounced emphasis, especially in trade. In his view, Trump continues to operate under an economic vision in which “the government plays Santa Claus” to gain political support, while his only deep conviction is his commitment to protectionism.

“Protectionism has worsened significantly,” he stated. The economist explained that Trump’s new tariffs imposed on the rest of the world are not based on revenue or geopolitical logic, but on a “lack of understanding” of how international trade works. The result, he warned, is greater economic inefficiency and costs for virtually all productive sectors.

According to Mitchell, the two main economic pillars of the new Trump administration are protectionism as the core of the economic program and immigration restrictions, which he also considers part of the economic package due to their direct impact on the labor market.

His view is critical: deportations or stricter immigration barriers, he argued, will reduce total GDP, although they may raise per capita GDP if they primarily affect low-skilled workers. He pointed to sectors like hospitality, construction, landscaping, and low-skill services as the most exposed to these measures.

Tax Reform: Mixed Effects and Fiscal Tensions

The economist confirmed that the 2017 tax cuts have already been extended and that some pro-growth measures were added, although also “new and absurd loopholes” in the tax code. Mitchell expects a modestly positive impact on growth, investment, and employment, but overshadowed by the economic damage from protectionism.

Is there fiscal space to support a tax cut agenda? For Mitchell, the answer is clear: “100% of the U.S. fiscal problem is excessive spending.” He insisted it is not a revenue issue, and that if not corrected, uncontrolled spending will inevitably lead to future tax increases—something he considers a significant risk to the economy.

Mitchell also emphasized that the greatest risk of the trade agenda is not just inflation or supply chain disruptions but the widespread economic inefficiency that new tariffs will cause.

Regarding inflation, he predicted that 2026 will be a year of inflationary pressures—but not due to fiscal or trade policy, but rather the Fed’s monetary policy. He warned that, like “almost all populists,” Trump favors easy money, which could undermine the independence of the central bank.

Looking Toward 2026: Three Scenarios

Mitchell outlined three possible scenarios for 2026:

Optimistic: Trump abandons his “trade war,” providing a boost to growth.

Base case: he maintains the current course, resulting in mediocre growth.

Stressed: protectionism and loose monetary policy deepen, increasing the likelihood of significant deterioration.

When asked about the coherence between pro-dollar policies and the encouragement of the crypto ecosystem, and on the other hand, restrictive immigration policies alongside a strategy of greater engagement with Latin America, Mitchell noted that consistency is not a priority for Trump. “Like all populists, he cares about what pleases voters in the short term,” he concluded.

Analysts at the McKinsey Global Institute have just published an ambitious report that looks to the future and identifies, with a horizon to 2040, the 18 main sectors of the global economy that will show high dynamism and growth.

The research estimates that these 18 sectors could generate between $29 trillion and $48 trillion in revenue, and between $2 trillion and $6 trillion in profit, by the year 2040.

Understanding the Future by Analyzing the Past

To understand the future, the consultancy analyzed what happened between 2005 and 2020 with the main sectors of the economy. Twelve segments experienced growth well above average—in particular, a compound annual growth rate in revenue of 10% and in market capitalization of 6%, while industries outside the ranking grew by just 4% and 6%, respectively.

The report develops a kind of “magic formula” for creating economic sectors with “special potential”—that is, a set of three common factors that tend to generate these dynamic arenas:

A step-change in business model or technology

Layered investment (i.e., major investments that reinforce each other and create compounding effects)

A large or growing addressable market

This Is the List of the Winning Sectors

Software and Artificial Intelligence Services AI—in all its variants: generative, predictive, automation—is creating a new digital fabric for businesses and consumers. The sector will include AI platforms, specialized services, foundation models, and productivity tools.

Next-Generation E-Commerce E-commerce will continue to expand, particularly toward integrated models (superapps, social commerce, live shopping), ultra-fast supply chains, and AI-powered personalized digital experiences. The line between physical and digital stores will keep blurring.

Digital Content Streaming Entertainment will continue shifting to digital platforms with hybrid models (subscription + advertising). Competition will intensify as premium content, advanced analytics, and global distribution enable the emergence of new players and niche segmentation.

Digital Advertising With the rise of data, AI, and new formats (short video, contextual advertising, integrated commerce), digital advertising will keep growing. The progressive elimination of cookies and tighter regulations will drive new models based on first-party data and smarter segmentation.

Video Games Gaming is expanding as a cultural, technological, and social industry, fueled by subscription models, cloud gaming, persistent worlds, in-game economies, and immersive experiences.

Cybersecurity Digital complexity and risks are rising—especially with AI, IoT, and connected critical systems. This sector will grow through managed services, infrastructure protection, digital identity, advanced threat detection, and automated response.

Cloud-Based Enterprise Software Advanced SaaS solutions, modular platforms, AI-based applications, and tools enabling full business process integration in the cloud will continue to grow, improving efficiency and scalability.

Cloud Services and Infrastructure Includes hyperscalers, data centers, computing services, storage, networking, and edge computing. Expansion is driven by generative AI, industrial automation, autonomous vehicles, and applications requiring low latency and high computing power.

Semiconductors Chip demand will soar due to AI, electric vehicles, IoT, robotics, and defense. A new phase is opening with massive investments, geopolitical competition, next-generation miniaturization, and new materials. The supply chain will expand and be globally reconfigured.

Electric Vehicles (EVs) The EV market will keep growing with improvements in batteries, lower costs, new architectures, and economies of scale. Competition will rise between traditional automakers and new entrants, especially from China.

Shared Autonomous Vehicles Robotaxis and autonomous fleets will create a new urban mobility model, with per-kilometer costs far lower than current taxis. This area requires advances in sensors, AI, regulations, and HD mapping but promises to transform transportation and city infrastructure.

Advanced Batteries Includes solid-state technologies, new materials, improvements in energy density, and cost reductions. Battery development is key for electric vehicles, stationary storage, electronic devices, and more flexible energy grids.

Next-Generation Nuclear Energy (Compact Fission) Small modular reactors (SMRs) and safer, scalable fission technologies could provide clean, continuous power. Progress depends on regulation, industrial costs, and social acceptance, but several countries and companies are accelerating investments.

Industrial Biotechnology Based on using living organisms or biological processes to produce materials, chemicals, fuels, and food. The convergence of synthetic biology, automation, and computing enables faster design cycles and lower costs.

Consumer Biotechnology Includes personalized products and services based on genetics, the microbiome, metabolomics, and biomarkers. Growth is expected in advanced supplements, preventive interventions, personalized testing, and wellness solutions based on biological data science.

Treatments for Obesity and Related Conditions New pharmacological therapies (such as GLP-1 agonists) are transforming treatment for obesity and related metabolic diseases. This sector could become one of the largest pharmaceutical markets in history due to the global scale of the issue.

Modular Construction The industrialization of construction through prefabricated modules will reduce costs and construction time.

Space Development Falling launch costs and advances in reusable rockets enable new models: small satellites, communications, Earth observation, in-orbit manufacturing, and commercial missions. The entry of private players is revitalizing a traditionally state-led sector.

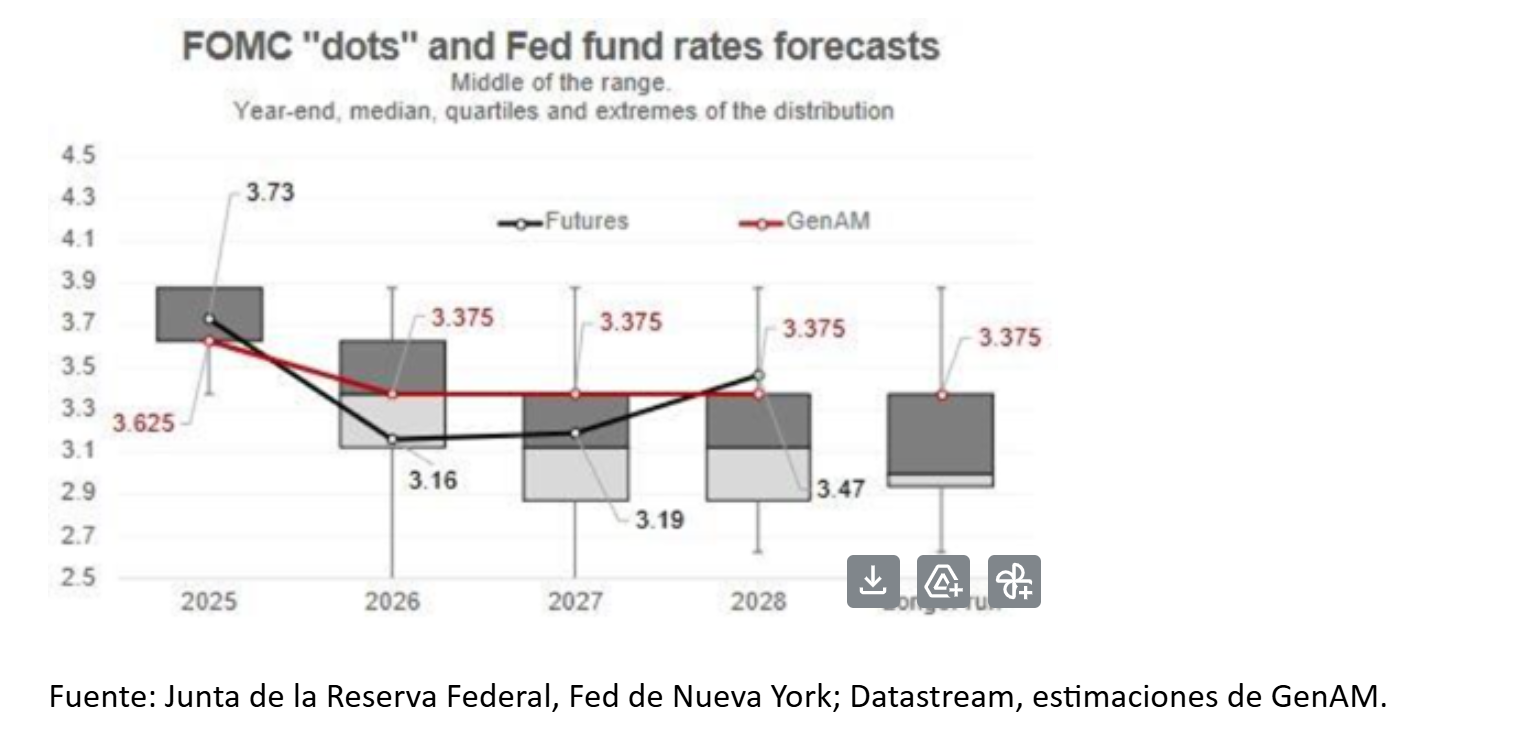

The U.S. Federal Reserve (Fed) held its final meeting of 2025 yesterday and announced a 25 basis point cut, in line with market expectations. Thus, the year ends with interest rates in the target range of 3.5% to 3.75%. In the opinion of international asset managers, the fact that the Fed continues to lean toward lower rates, even as the U.S. records stronger inflation and growth, highlights a disconnect in global monetary policy.

“Available data suggest that economic activity has expanded at a moderate pace. Employment growth has slowed this year, and the unemployment rate has slightly increased through September. The most recent indicators confirm this trend. Inflation has been rising since the beginning of the year and remains at elevated levels,” the Fed stated.

According to Gordon Shannon, portfolio manager at TwentyFour Asset Management (a boutique of Vontobel), this is an aggressive cut, as the FOMC has signaled a higher bar for monetary policy easing in 2026. “Investors are lowering their expectations for the number of rate cuts the Fed might implement. However, with the highest number of dissenters since 2019, even before the arrival of the new chair, the committee appears fractured,” Shannon notes.

From the FOMC’s Perspective

Experts from asset management firms agree that the monetary institution faces a delicate balancing act: curbing inflation while supporting the labor market so that households feel economically secure. During the meeting, Powell warned that there is no risk-free path and pointed out that a reasonable reference is that tariff-driven inflation effects—essentially a one-time shift in price levels—are likely to ease, highlighting notable progress this year in non-tariff-related inflation.

Additionally, the Fed emphasized that future measures will depend on the data, shifting to a firm meeting-by-meeting approach. As highlighted by Daniel Siluk, portfolio manager and Head of Global Short Duration and Liquidity at Janus Henderson, Powell reinforced this stance during his press conference, stating that the Committee views today’s cut as a “prudent adjustment” and not the beginning of a new cycle.

“The Summary of Economic Projections (SEP) echoed that hawkish tone. Growth forecasts for 2026 and 2027 were revised slightly upward, inflation slightly downward for 2026, and unemployment remained stable over the medium term—hardly a context conducive to aggressive easing. The median dot plot for official interest rates remained unchanged at 3.6% for 2025 and 3.4% for 2026, indicating just one cut per year. Long-term expectations remain anchored at 3.0%,” Siluk explains.

Looking Toward 2026

That covers the Fed’s reasoning—but what does this decision mean looking ahead to 2026? In the short term, Ray Sharma-Ong, Deputy Global Head of Multi-Asset Bespoke Solutions at Aberdeen Investments, believes the Fed’s decision justifies a relief rally in the markets. “Markets went into the FOMC meeting concerned about a possible discussion of a rate hike. Powell’s comment that a hike was ‘not the base case’ removed that risk for now. Additionally, markets will be relieved by the Fed’s decision to address tension in repo and funding markets through the purchase of $40 billion in bills via the OMO, which will serve as a temporary short-term liquidity measure,” explains Sharma-Ong.

Beyond this immediate relief, the Aberdeen Investments expert adds that Fed monetary policy is no longer a catalyst for markets. “The long-term neutral rate remained at 3%. Now that the federal funds rate sits between 3.5% and 3.75%, the Committee views monetary policy as within the effective neutral range. The bar for further cuts is very high, suggesting the monetary policy landscape is likely to remain static for some time,” he argues.

Looking ahead to next year, Tiffany Wilding and Allison Boxer, economists at PIMCO, maintain that the Fed enters 2026 in a wait-and-see mode, shifting from cuts to caution. With the interest rate in neutral territory, the Fed turns to data dependency and faces a delicate balancing act in 2026. “Barring an economic shock, we are unlikely to see another rate cut until the second half of next year. Our outlook is largely aligned with that of the Fed and current market pricing: we expect the Fed to keep rates steady in the 3.5% to 3.75% range for the remainder of Powell’s term as chair, which extends through May, before gradually resuming rate cuts later in the year under new Fed leadership,” the PIMCO economists argue.

Disagreements

One of the conclusions from this latest Fed meeting is that the decision taken did not have unanimous support from FOMC members, as Stephen Miran advocated for a 50 basis point cut, contrary to the majority. On the other hand, Jeffrey Schmid, Governor of the Kansas Fed, and Austan Goolsbee, Governor of the Chicago Fed, argued in favor of keeping rates unchanged.

“The Fed’s decision to cut rates came with three dissenting votes—the highest number since 2019. This highlights growing disagreement within the Fed in recent months regarding the next steps on interest rates, reinforcing a point we already made in October: the rate-setting committee now faces more complex decision-making dynamics,” notes Jean Boivin, Head of the BlackRock Investment Institute.

In this regard, for Max Stainton, Senior Global Macro Strategist at Fidelity International, the trajectory of interest rates in the market will increasingly be determined by speculation surrounding Donald Trump’s choice of the new Fed chair, rather than by the data.

“In our base case for 2026, we anticipate that the Trump Administration will appoint a dovish and non-traditional chair, whose main objective will be to further lower rates. This dynamic will likely distort the forward rate curve around the date the new chair takes office, in May 2026, with a new cutting cycle being priced in if this scenario materializes. Although the market has already begun to price in this possibility, there is still room for this to extend across both the short and long ends of the curve, with the arrival of a non-conventional dovish chair representing an underappreciated risk for the long end,” states Stainton.