Binance, a global cryptocurrency exchange firm, and Franklin Templeton have announced a collaboration to “build digital asset initiatives and solutions tailored to a wide range of investors.” According to the announcement, they will explore ways to combine Franklin Templeton’s expertise in compliant asset tokenization with Binance’s global trading infrastructure and investor reach.

Specifically, their goal is to offer innovative solutions to meet the evolving needs of investors, providing greater efficiency, transparency, and accessibility to capital markets, along with competitive yield generation and settlement efficiency.

“As these tools and technologies evolve from the margins into the financial mainstream, partnerships like this will be essential to accelerate adoption. We see blockchain not as a threat to legacy systems but as an opportunity to reimagine them. By working with Binance, we can leverage tokenization to bring institutional-grade solutions like our Benji Technology Platform to a broader set of investors and help bridge the worlds of traditional and decentralized finance,” said Sandy Kaul, EVP, Head of Innovation at Franklin Templeton.

According to the experience of Roger Bayston, EVP and Head of Digital Assets at Franklin Templeton, investors are asking about digital assets to stay ahead, but they need them to be accessible and reliable. “By working with Binance, we can deliver groundbreaking products that meet the requirements of global capital markets and co-create the portfolios of the future. Our goal is to bring tokenization from concept to practice so that clients can achieve efficiencies in settlement, collateral management, and portfolio construction at scale,” he stated.

Meanwhile, Catherine Chen, Head of VIP and Institutional at Binance, explained: “Our strategic collaboration with Franklin Templeton to develop new products and initiatives reinforces our commitment to bridging crypto and traditional capital markets and unlocking greater possibilities.”

International asset managers believe that the European Central Bank (ECB) has entered a new pause phase. In its meeting this week, the monetary institution kept rates unchanged and, despite offering few clues, indicated that it would take more time to assess economic developments in an international context it acknowledges as complex.

“President Lagarde reiterated that future monetary policy decisions will depend on data, while emphasizing that current rates are within the range the ECB considers neutral. Growth forecasts for 2025 were revised upward to 1.2%. Regarding the political situation in France, President Lagarde stated that it is not a matter for the ECB to comment on, while conveying the message that fiscal responsibility is extremely important,” summarized Felipe Villarroel, partner and portfolio manager at TwentyFour AM (a Vontobel boutique).

For Forest, it is significant that the interest rate gap with the Federal Reserve is expected to narrow in the coming months. “With signs of a weaker U.S. labor market, the Fed could cut rates twice this year. However, price pressures related to tariffs could resurface, leaving Jerome Powell caught between political pressure from President Trump and a shrinking margin for maneuver,” explains the CIO of Candriam.

Despite political instability, this September meeting gives the impression that the ECB has fulfilled its role. “At a time when free trade is faltering, political tensions are resurfacing, and the independence of the Federal Reserve is being questioned, the eurozone can count on a credible central bank. It has managed to navigate smoothly through the turbulent environment of recent months,” notes Raphaël Thuin, head of capital markets strategies at Tikehau Capital.

Has Its Job Finished?

For Luke Bartholomew, deputy chief economist at Aberdeen Investments, the most relevant question is whether the ECB has truly concluded its easing cycle or is merely pausing before implementing further cuts in the future. In his view, the economic forecasts seem broadly consistent with the idea that this easing cycle has come to an end.

“We continue to believe that the next move is more likely to be a rate hike rather than a cut, although this may still take time to materialize. Of course, a sharp rise in France’s financing costs could still destabilize the eurozone economy and force new stimulus measures. However, an explicit ECB intervention in the French debt market still seems distant,” says Bartholomew.

In the opinion of Nicolas Forest, CIO of Candriam, with interest rates already at neutral levels, the European Central Bank has largely achieved its immediate objective of containing inflation. Although he acknowledges that, in the current scenario, the ECB is keeping all options open, its next decisions will depend on whether incoming data continue to show moderate improvements or whether U.S. tariffs and the deterioration of the Chinese economy weigh more heavily on Europe.

Irene Lauro, eurozone economist at Schroders, also sees the ECB’s decision as confirmation of her view that the easing cycle has ended. “With declining trade uncertainty, the eurozone recovery will accelerate. The risks for the eurozone have shifted from trade uncertainty to political instability, with France now in the fiscal spotlight. But the resilience of the economy and the strengthening of domestic demand mean that the ECB can afford to maintain its monetary policy unchanged,” she argues.

When it comes to cuts, Sandra Rhouma, vice president and European economist on the fixed income team at AllianceBernstein, believes there may be one more cut before the end of the year, although the monetary institution will need “compelling evidence.” Rhouma argues that the ECB is in “a good position,” as President Lagarde often repeats, which also means they could and should apply further cuts when necessary.

“I believe the data at the December meeting will be convincing enough, but we must acknowledge that the ECB’s current reaction function increases the risk that no further cuts will occur this year. Particularly given that they continue to ignore signs of falling below their medium-term target, as reflected in their own forecasts,” she adds.

In this regard, Guy Stear, head of developed markets strategy at Amundi Investment Institute, adds that by lowering the inflation forecast for 2027 to below 2%, the ECB could be paving the way for a rate cut before the end of the year. “ECB President Christine Lagarde is optimistic about growth, but we are concerned that all efforts to reduce deficits outside Germany may end up hurting consumer demand,” explains Stear.

Implications for Investors

Markets interpreted Lagarde’s comments as hawkish, further reducing expectations for an additional rate cut in the future. Following these statements, a modest bear flattening of the Bund curve occurred. “Given positioning tensions, we cannot rule out further modest flattenings in the 5–30 year segment in the short term, although we suspect that, once a rate cut is completely ruled out, the curve will begin to steepen again. The balance of risks suggests that curves will remain steep or steepen further in the medium term,” notes Annalisa Piazza, fixed income research analyst at MFS Investment Management.

According to Forest, this environment points to a period of higher volatility but also of opportunities: European growth, together with supportive fiscal measures, could sustain certain segments of equities and credit, while the prospect of rate cuts in the U.S. would increase demand for high-quality bonds.

According to David Zahn, head of European fixed income at Franklin Templeton, following the ECB’s September meeting, the decision to keep rates at 2% reflects stable inflation amid signs of slowing growth. “We consider monetary policy to remain broadly neutral, which favors short-duration bonds and high-quality defensive equities. The financial sector could come under pressure if rate expectations remain subdued, while geopolitical and energy risks require close monitoring,” says Zahn.

Some firms believe that fixed income is quietly recalibrating. According to Thomas Ross, head of high yield at Janus Henderson, investor confidence should be supported not only by the ECB’s benign view on downside risks to the economy, but also by the possibility of a new cut to add further protection and consolidate a low-volatility environment. “In our view, yield-capture strategies—such as securitized credit, corporate credit, and multi-sector income strategies—should attract greater interest from investors,” says Ross.

A new report by TMF Group reveals that family offices are intensifying their efforts to diversify, professionalize, and align their investments with the values of the next generation, in response to geopolitical instability and regulatory changes that are transforming the global wealth management landscape.

The report, titled “Redefining Resilience: How Family Offices Are Adapting to Global Uncertainty and Next-Generation Priorities,” presents insights from leading private wealth and family office professionals and shows how political shifts in key jurisdictions have driven increased efforts in wealth relocation, restructuring, and corporate governance.

The study identifies several trends currently shaping family office strategies. Geopolitical volatility is encouraging diversification, with families entering new markets and industries—often beyond their traditional areas of expertise—to mitigate jurisdictional risks and capture growth in regions with strategic trade access or emerging economic hubs. Increasingly, decisions are based on scenario planning, using risk models that evaluate each jurisdiction’s resilience under various political and economic outcomes.

Jurisdiction selection is also evolving. While tax remains an important factor, institutional stability, legal system transparency, the depth of local capital markets, and the security of cross-border arrangements now carry more weight. Families are seeking predictable, agile regulatory frameworks that combine investor protection with operational efficiency.

The next generation of family leaders, meanwhile, remains focused on ethical investing. Interest is growing in socially responsible, environmentally sustainable, and well-governed assets. These priorities are an integral part of long-term strategy, with investments in sectors such as renewable energy, climate technology, and sustainable agriculture, accompanied by philanthropic projects aimed at generating measurable outcomes.

At the same time, the professionalization of family offices is advancing. The shift from informal advisory structures to fully integrated, multi-jurisdictional operations is accelerating, with the hiring of senior executives with international experience, the adoption of corporate-level governance frameworks, and the development of internal compliance capabilities to manage diverse regulatory standards across multiple territories.

“The private wealth management sector is undergoing a fundamental transformation. Families are not only seeking to protect their assets in a volatile world, but they are also actively redefining what resilience means, with a greater focus on diversification, operational excellence, and ethics. The most successful family offices will be those able to combine strategic agility with strong governance,” said Tim Houghton, global head of private wealth and family offices at TMF Group.

A Regional Perspective

The report also offers a regional overview. In the Middle East, investment strategies—particularly in Saudi Arabia and the United Arab Emirates—are becoming more sophisticated thanks to the professionalization of family offices, which are hiring senior executives to manage portfolios more effectively. This process requires attracting top talent with competitive incentives and benefits to retain them.

In Asia-Pacific, Hong Kong and Singapore remain leading hubs due to their connectivity with global capital flows. However, increasing requirements for due diligence and anti-money laundering compliance are lengthening onboarding processes and raising operational costs. Maintaining a strategic presence in these markets requires balancing access to regional wealth networks with growing regulatory compliance demands.

In North America, market conditions are prompting some family offices to reevaluate the geographic distribution of their portfolios and operational structures. Interest in alternative jurisdictions reflects a desire to diversify exposure and enhance flexibility in asset deployment.

Finally, in the United Kingdom and the Channel Islands, post-election reforms—including changes to non-dom rules and inheritance tax—are driving both inflows and outflows of wealth. Jersey, in particular, continues to strengthen its appeal through a solid legal framework and alignment with international transparency standards.

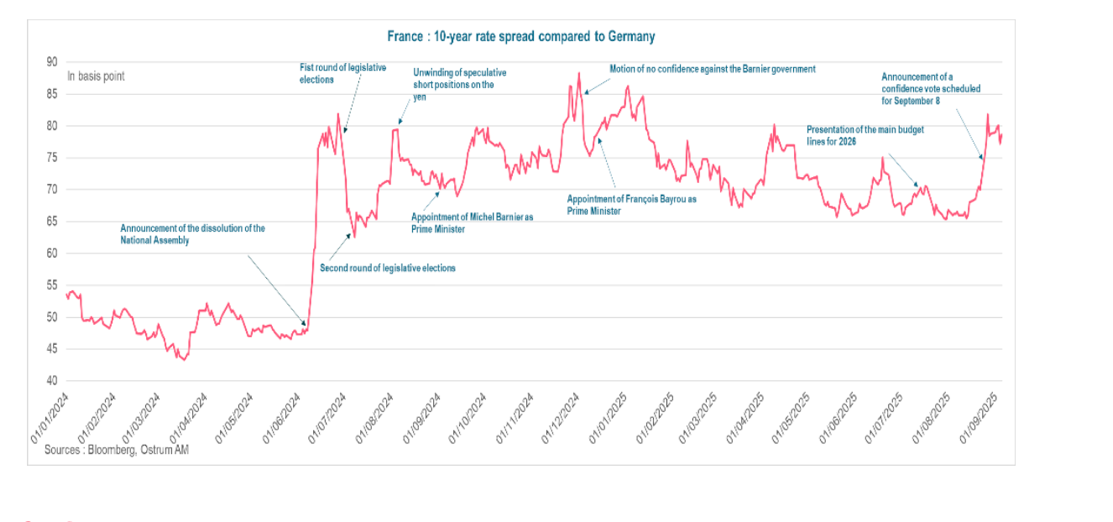

France: Political Instability Raises Concerns, but Market Impact Remains Contained

French Prime Minister François Bayrou gambled everything on a single move—a vote of confidence—and lost. According to experts, France is entering a new political crisis, beginning with the challenge of addressing a €44 billion fiscal adjustment. Although this scenario had already been anticipated by some investors, the coming days will be crucial to assess the country’s ability to stabilize its political outlook and reassure markets regarding its fiscal trajectory.

“The preferred alternative for President Macron is now the swift appointment of a new prime minister, who will attempt to reach an agreement in the tense budget negotiations. Early elections remain a possibility if this fails. In any case, current developments reflect a challenge with limited room for an easy solution: fragile governments in a fragmented political landscape. Thus, uncertainty remains high, although we do not expect bond markets to derail from here,” comments Dario Messi, Head of Fixed Income Research at Julius Baer.

Experts agree that the chaos in French politics does add more volatility. Peter Goves, Head of Developed Market Sovereign Research at MFS Investment Management, sees it likely that spreads will remain wide, with episodes of short covering; however, political instability is undoubtedly here to stay. “Macron will likely rush to appoint a new prime minister as a first reaction, before considering calling new parliamentary elections. The situation is highly fluid, and how events unfold will likely dictate the market tone in the coming days. So far, the market reaction has been relatively contained, but we take into account the strikes scheduled for Wednesday and the imminent risk of a potential downgrade. Meanwhile, France still needs to pass a budget,” says Goves.

Contained Impact

According to Raphaël Thuin, Head of Capital Markets Strategies at Tikehau Capital, for now, the economic impact is uneven. “The CAC 40 companies, mostly multinationals, exporters, and with low levels of debt, appear relatively protected from political turbulence and rising interest rates. Their limited exposure to public procurement reduces their sensitivity to budget swings. Furthermore, the excess of private savings in France continues to finance part of the deficits, which mitigates external vulnerabilities,” he points out.

However, he acknowledges that two areas of concern are emerging: “In the short term, corporate taxation could become a critical issue, as several parties are considering specific reforms. In the long term, political instability and chronic deficits could gradually erode investor confidence, private investment, and the country’s attractiveness. This evolution could ultimately weigh on consumption and economic growth.”

Michael Browne, Global Investment Strategist at the Franklin Templeton Institute, notes that France has the backing of the EU, the ECB, and the euro—and it’s not going anywhere. “Its financial system is solid. It’s true that it’s the only country in Europe where spreads have widened against Germany, but only to 80 basis points. There will be no currency or funding crisis. So, whoever takes office won’t matter. Nothing is expected of them—just to weather the situation until 2027 and hope that economic improvement in Europe, driven by German Chancellor Mertz, generates enough growth to offset the risk of going two years without a new budget. The bond market remains calm, while equities have suffered more from weakness in luxury goods sales than from political turmoil. An operational government is, clearly, a luxury France will not be allowed; and when it finally gets one in 2027, markets will be ready with their verdict,” argues Browne.

France’s Risk Premium

In a context of persistent deficits and rising interest rates, Thuin considers that the issue of France’s risk premium remains key. “Although it varies by asset class, it currently seems to offer limited compensation when taking political and fiscal tensions into account. The main transmission channel of risk continues to be interest rates, in an international environment marked by a general increase in financing costs,” he explains.

According to the Julius Baer expert, political risk is already reflected in asset prices. “Before the confidence vote, the spread between 10-year government bonds of Germany and France once again approached 80 basis points, having already remained elevated for some time compared to other eurozone countries. Although primary deficits are considered unsustainable, we believe France’s current capacity to handle its debt remains relatively high, given that the country benefited for a long period from exceptionally low financing costs. In other words, early elections (or, in the worst-case scenario, Macron’s resignation) could lead to a further widening of spreads, but we expect the impact to be limited in magnitude and do not anticipate bond markets to derail from here,” he notes.

“The risk of a new dissolution of the National Assembly seems the highest to us, which would lead to a widening of the spread between French and German 10-year yields. In that case, tensions on peripheral country spreads should be more limited, not justifying ECB intervention. In the extreme scenario of President Emmanuel Macron’s resignation, the French spread would exceed 100 basis points, justifying ECB intervention to limit contagion,” says Aline Goupil-Raguénès, Developed Markets Strategist at Ostrum AM (Natixis IM), when discussing possible scenarios.

France’s Political Deadlock Deepens Fiscal Concerns, but ECB Intervention Remains Unlikely—for Now

This dynamic is part of a global trend, where inflation and growing doubts about the sustainability of public deficits are putting upward pressure on interest rates. Asset management experts acknowledge that France is not an isolated case, but its political instability could worsen its position compared to more stable partners.

“The ECB could intervene only in the case of significant tensions on interest rates that pose a risk to financial stability or to the transmission of monetary policy—which is currently not the case. It could also intervene in the event of the president’s resignation to contain spread tensions among peripheral countries triggered by contagion effects. It could activate the TPI. Announced in July 2022 and never used, its goal is ‘to counter disorderly market dynamics that pose a serious threat to the transmission of monetary policy within the eurozone,’” adds the strategist from Ostrum AM.

Possible Scenarios

Looking ahead, France faces three possible options: the appointment of a new prime minister, the dissolution of the National Assembly and the calling of new elections, or the resignation of its president, Emmanuel Macron. According to Goupil-Raguénès, the most likely scenario is the dissolution of the National Assembly, given the inability to find a new prime minister capable of broadening the government’s support in Parliament.

“New legislative elections would have to be held within 20 to 40 days of the dissolution. The outcome would likely result once again in a deeply divided National Assembly, with a probable increase in seats won by the far right, according to recent polls, though without a majority. The risk of social unrest—already present with protests planned for September 10 and 18—would be heightened. Uncertainty would rise along with the risk of an insufficient fiscal adjustment, which could keep the deficit elevated and lead to an increase in the public debt-to-GDP ratio. The risk of confrontation with Brussels would grow,” she adds.

According to the multi-asset team at Edmond de Rothschild AM, regardless of the outcome of the current political crisis, the likelihood of a meaningful reform of public finances will remain low—“to the point that financial markets themselves appear resigned and may settle for a scenario in which the budget deficit simply doesn’t deteriorate further.”

However, they note that while the situation is not catastrophic, it is worrisome, as France stands apart from the rest of the eurozone with the highest budget deficit and public debt on an upward trajectory (113% in 2024 and 117% forecast for 2025). “This deterioration in fiscal balances is mainly due to the decline in tax revenues, resulting from tax cuts granted to households (-1.6 percentage points since 2017) and companies (-0.8 points), which has not been offset by a reduction in public spending (which returned to 2017 levels after the pandemic peak). Although many parties agree on the need to cut public spending—which currently represents 57% of GDP (compared to an average of 50% in the eurozone)—it remains difficult to form a majority to adopt measures that would bring the primary deficit below the debt-stabilizing level,” they explain. They add that the status quo is likely to remain unless pressure from the European Commission—and especially from financial markets—increases, in which case tougher decisions will have to be made, likely after new legislative or presidential elections.

Finally, Alex Everett, Senior Investment Director at Aberdeen Investments, notes that while the political situation unfolds, the urgent financial need is to pass a prudent budget that reduces the deficit, no matter how unlikely that seems. “At this point, even a small reduction would be better than nothing. Confidence in the French economy is already low, and the longer this situation drags on, the bigger the problem becomes. It’s clear that France’s political gridlock won’t be resolved this year, and perhaps not even until the presidential elections in 2027. This will likely keep French government bond spreads—known as OATs (Obligations assimilables du Trésor)—elevated, at least around current levels, over the coming months. We continue to favor short positions in OATs versus their peers,” concludes Everett.

To the sea, to the rock, to the glacier: that is what the cuisine of the end of the world tastes like. The company Cruceros Australis recently celebrated its 35th anniversary by bringing to Madrid the flavors of its cuisine, based on seafood found only in the southernmost waters of the planet through which it sails: the Strait of Magellan, the Beagle Channel, and Cape Horn.

The company offered a tasting in Madrid to showcase that its voyages also represent a full gastronomic experience. “To our journey through the most untouched and unknown part of Patagonia and Tierra del Fuego, we add a flavor experience thanks to the carefully crafted onboard cuisine and the pairing with fine wines,” said Frederic Guillemard, Australis’ manager for Europe and Asia.

As with the tasting, the cuisine offered on their cruises is prepared using locally sourced ingredients from the Chilean and Argentine Patagonian region.

“This also marks the celebration of our company’s 35 years navigating this protected route, which is accessible only via our two ships, the Ventus Australis and the Stella Australis, as it cannot be reached by land or air,” he added.

Present at the event, from Chile, was renowned Peruvian chef Emilio Peschiera, who has been advising Australis for over a decade.

The menu presented—just like on the cruise—is based on “the region’s most representative products, such as king crab, glacier scallops (large scallops), Magellanic grouper, and the region’s iconic lamb, in a carefully curated selection of the dishes served during the voyage.”

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.

Pairing is also a key part of this gastronomic experience. The offering includes “fine Chilean wines that enhance these flavors, such as a crystalline Sauvignon Blanc to accompany the scallops, followed by Pinot Noir paired with king crab chupe, and a red wine made from Carménère (the legendary 19th-century European varietal that survived in Chile, now the world’s largest producer) to accompany the Magellanic lamb.”

The menu consisted of two starters: octopus carpaccio with black olive sauce and crispy sweet potato threads, and a tiradito of glacier scallops with citrus sauce, mango, and chalaquita, paired with a Casa Silva Sauvignon Blanc, Cool Coast, Paredones, Chile.

Among the main courses were Magellanic king crab chupe, and a Magellanic sea duo featuring grilled conger eel over crispy a lo macho rice and oven-roasted deep-sea Magellanic grouper with olive oil and golden garlic over a potato biscuit, paired with Viña Villard Pinot Noir, Gran Reserva, Le Pinot Noir.

Next, a Magellanic lamb medallion was served over carrot purée with yogurt, paired with a Von Siebenthal Carménère, Gran Reserva.

A standout feature of these dishes is that they are prepared using regional recipes, such as the king crab pie or the lamb, which is stewed and gelled before being served as a medallion.

As for the desserts, the tasting featured a unique and typical flavor: rhubarb, a sweet-and-sour plant native to Patagonia. Specifically, a rhubarb crumble with vanilla ice cream was served.

A Commitment to Ecotourism

The fact that the entire offering is produced using regional ingredients aligns with Australis’ commitment to ecotourism—“which in this case is accompanied by bold and unique flavors,” added the Australis manager—making the journey not only an experience through the beauty of the landscapes visited, “but also one in which the tasting of our food and wines is a fundamental part of the voyage.”

The journeys last five days and four nights, departing from either Punta Arenas (Chile) or Ushuaia (Argentina).

Each day includes zodiac landings to explore native forests found only in these remote regions—accessible through treks of varying difficulty—or to observe penguins, flora and fauna, and glaciers, as well as to navigate the Patagonian channels all the way to Cape Horn, crossing the Strait of Magellan. A true voyage to the end of the world… accompanied by its cuisine.

Goldman Sachs and T. Rowe Price announced a strategic collaboration aimed at offering a range of diversified solutions in public and private markets, designed for the needs of retirement and wealth investors.

Goldman Sachs intends to invest, through a series of purchases in the open market, up to $1 billion in common shares of T. Rowe Price, with the intention of owning up to 3.5%, which would make it the firm’s fifth largest shareholder, according to a joint statement issued by both companies.

“This investment and collaboration represent our conviction in a shared legacy of success in delivering results to investors,” said David Solomon, chairman and CEO of Goldman Sachs.

“With Goldman Sachs’ decades of leadership in innovating across public and private markets, and T. Rowe Price’s expertise in active investing, clients can confidently invest in new opportunities for retirement savings and wealth creation,” he added.

Rob Sharps, CEO of T. Rowe Price, stated: “As retirement leaders, we have a proven track record of leveraging our expertise to drive solutions that help our clients prepare, save, and live confidently in retirement.”

“We are excited to collaborate with Goldman Sachs, leveraging our broad capabilities in public and private markets to offer clients the opportunity to unlock the potential of private capital as part of their retirement and wealth management strategies,” he added.

The collaboration will leverage the strengths of both firms, including their investment expertise, solution-oriented approach, and deep understanding of the needs of intermediaries and their clients. The core focus will be on providing a range of wealth and retirement offerings that incorporate access to private markets for individuals, financial advisors, plan sponsors, and plan participants, the companies stated in the release.

Major financial firms like Goldman Sachs, BlackRock, and Morgan Stanley are betting heavily on alternative assets—an area dominated by private equity firms—to capitalize on their growth potential and attract new clients.

“Goldman didn’t buy a friend, it bought a fast track to 401(k) distribution, since two-thirds of T. Rowe’s assets come from retirement accounts,” Michael Ashley Schulman, chief investment officer at Running Point Capital Advisors, told Reuters.

“We believe that Goldman brings a broad range of capabilities in private markets and wealth management to this relationship, which will enable the two companies to design a very wide range of solutions that can meet client demand as it evolves,” wrote analysts at Evercore ISI in a note.

Key Points

Target-date strategies:

The firms will offer new joint and co-branded target-date strategies that will leverage T. Rowe Price’s expertise in the Retirement Blend series, while expanding plan participants’ access to private markets by incorporating investment capabilities from Goldman Sachs, T. Rowe Price, and OHA. Goldman Sachs will act as the external provider of private market strategies for the target-date series. These solutions are expected to launch in mid-2026.

Model portfolios:

Joint and co-branded model portfolios will be introduced, leveraging the strengths of both organizations. These will include separately managed accounts (SMAs), direct indexing, ETFs, mutual funds, and private market vehicles, tailored to the needs of advisors serving mass affluent and high-net-worth (HNW) clients.

Multi-asset offerings:

T. Rowe Price and Goldman Sachs will also collaborate on multi-asset offerings. They are currently considering two strategies: one that will provide access to asset classes such as private equity, private credit, and private infrastructure in a diversified portfolio through a single vehicle, and another that will integrate investment in both public and private U.S. equities into a single offering.

Personalized advisory solutions and advisor-managed accounts:

The firms are collaborating on the development of an innovative, scalable advisory platform for advisors and other RIAs to offer managed retirement accounts both within and outside of plans. This includes the integration of retirement planning and advisory services from both firms into T. Rowe Price’s recordkeeping and individual investor platforms.

China Mid-Year Economic Review and Outlook: Moderate Optimism in Equities and the Nation’s Transformation

After passing the halfway point of the year, it is time to assess China’s economic situation. The country’s GDP grew by 5.3% in the first half of the year compared to the same period in 2024, aligning with the government’s target. The deficit stood at 4% of GDP—its highest in thirty years—seemingly confirming the government’s intention to support the economic cycle through decisive industrial policies.

Beijing also announced a record trade surplus of around $586 billion, with exports growing 5.8% year-on-year in June, exceeding analysts’ estimates. Despite tariffs currently standing at 55%, China’s trade surplus with the United States rose to $114.77 billion by June, up from $98.94 billion a year earlier, once again surpassing market expectations. “This is a clear indicator of the resilience of Chinese companies: decoupling is a long-term process, and in many technology sectors, global dependence on China remains structural,” says Carlo Gioja, Portfolio Manager and Head of Business Development in Asia at Plenisfer Investments—part of Generali Investments—in his mid-year review of the Chinese economy.

However, to truly understand the country’s trajectory and the scope of its ongoing transformation, Gioja sees it as “crucial” to look beyond the numbers, as “this is where a new Chinese paradigm emerges.” More than ever, he argues, understanding China’s transformation requires “observing its contradictions simultaneously”: the real estate crisis and the growth of high technology; apparent consumer weakness and the rise of innovative business models; geopolitical tensions and the disruptive strength of key industrial sectors; and finally, local government fiscal crises alongside innovation-driven growth ambitions.

In this context, the expert sees selective opportunities in the country’s equity markets. He notes that the Chinese government has strengthened its commitment to support the domestic stock market by requiring major institutional investors to increase their allocation to onshore listed equities—those on the Shanghai and Shenzhen exchanges, denominated in RMB and traditionally reserved for local investors and a small group of institutions—by 10% annually over three years. Insurance companies are also required to allocate 30% of new premiums for this purpose.

“The government and the Party in China continue to adopt certain elements of a planned economy, but at the same time, they support market competition and believe in innovation as a lever for increasing productivity,” Gioja states. He believes the success of this approach largely depends on Beijing’s ability to manage the balance between central control and local initiative.

Even with U.S. tariffs, many sectors in which China holds a cost and scale advantage—batteries, electronic components, machinery, footwear, solar panels—remain competitive despite higher barriers to entry.

Despite this, “international capital remains predominantly speculative: even after the ‘DeepSeek effect’ earlier this year, long-term investors have yet to return in force.” The Plenisfer expert notes that a market dominated by speculative participants tends to be more volatile and less efficient in pricing the potential of top companies. Therefore, he believes current valuations in some cases offer good opportunities for future gains.

“China may seem like a multifaceted enigma, difficult to grasp at a glance. However, it is precisely in the complexity of its manufacturing, technological, and cultural ecosystems that selective opportunities lie for the patient and well-informed investor,” he concludes.

Nicholas Yeo, Head of China Equities at Aberdeen Investments, is somewhat more optimistic. He continues to see an improving environment for his fundamental approach in China’s equity markets, which gives him confidence for the remainder of the year.

Yeo also notes that the onshore equity market “is playing an increasingly important role in Chinese society” and that reforms and policy support for the markets are ongoing. “The market is an important mechanism to channel capital into innovation-related sectors,” he says, adding that he continues to see a growing number of opportunities in the A-share space.

In this landscape, he maintains a positive bias following the policy shift at the end of last year: external pressure could lead to a stronger focus on domestic stimulus, which is key to economic recovery. “Recent policies such as the fight against ‘involution’ suggest that authorities are taking steps to protect the economy,” he states.

“There is abundant liquidity in the system, with bank deposits equivalent to the market capitalization of China’s A-share market. With low interest rates, retail investors will seek higher-yielding assets, and the stock market is the primary destination for this money given the current state of the real estate sector,” Yeo asserts.

Thus, he believes the Chinese A-share market is “on the verge of sustained performance,” supported by a potentially weakening U.S. dollar and attractive valuations—not only compared to the U.S. market but also to other emerging markets. “Despite reaching new highs, the valuation of the Chinese A-share market remains below its five-year average,” he adds.

Meanwhile, Vivek Bhutoria, Emerging Markets Equity Portfolio Manager at Federated Hermes Limited, advocates for putting U.S.–China trade tensions into context: exports to the United States account for less than 3% of China’s GDP, and consumer goods and electronics make up the majority of those exports. “Nevertheless, punitive tariffs are likely to negatively impact Chinese exports. However, they will also increase costs for U.S. importers—and potentially for consumers,” he argues.

If tariffs persist, leading emerging market countries and regions—particularly China, India, and Southeast Asia—are expected to continue growing at an annual rate of 4% to 6%, compared to a global GDP growth of 50 to 100 basis points, supported by structural reforms and fiscal stimulus. “China retains the fiscal capacity to stimulate growth and absorb excess capacity resulting from reduced exports if U.S. tariffs are punitive,” Bhutoria explains.

The expert acknowledges that his view on China has always been long-term, noting, “The lack of investor interest in China in recent years has presented us with attractive entry points to invest in high-quality companies trading at significant discounts to their intrinsic value.” At this point, he believes the market has “overpriced” the risks associated with Chinese equities and that even if President Donald Trump imposes punitive tariffs, “China has the capacity to grow into prosperity,” which is why he remains positive on the country.

A recent study by MainStreet Partners, a firm specialized in sustainable investment and part of Allfunds, warns that the European Union is facing serious difficulties in turning its ambitious green agenda into a real competitive advantage.

The report identifies overlapping regulations, administrative burden, and lack of support for key sectors such as electric vehicles as the main barriers. According to Daniele Cat Berro, the firm’s Managing Director, these obstacles are weakening Europe’s role in the ecological transition and undermining its ability to lead in global sustainability.

In the industrial sphere, the company highlights setbacks compared to the Asian market. Despite the EU’s goals to reduce emissions from new cars by 55% by 2030 and eliminate combustion engines by 2035, more than 20% of electric vehicles sold in Europe in 2023 were of Chinese origin. In addition, the battery value chain is increasingly controlled by non-European players, while local industrial projects suffer from delays and limited funding.

“The transition to electric vehicles is strategic, but without a strong industrial base, it risks triggering deindustrialization in regions dependent on the automotive sector. Stronger support for local production is necessary,” said Cat Berro.

In the financial sphere, MainStreet Partners points out that the sustainable investment regulatory framework has reached a level of complexity that hampers market confidence. The combination of SFDR, CSRD, and CSDDD has resulted in high costs and compliance challenges, especially for small and medium-sized enterprises.

As a consequence, Europe recorded net capital outflows in ESG products for the first time in the first quarter of 2025, according to Morningstar data. The European Commission responded by introducing the Omnibus Directive, which includes postponements and adjustments to reporting obligations, but MainStreet warns that the measure is insufficient without a clear and agile execution strategy.

The firm has also expressed concern over the new regulation on ESG rating providers, which in practice will favor large global operators, most of them non-European. This, they note, jeopardizes the continent’s strategic autonomy in an emerging sector.

“The commitment to climate goals must be maintained, but with an approach that prioritizes regulatory clarity, industrial capacity, and international competitiveness,” Cat Berro concluded.

Gold’s Relentless Climb: Central Banks, Geopolitical Risk, and U.S. Economic Conditions Fuel Bullish Outlook

Gold continues its upward trajectory. It was one of the best-performing assets in portfolios last year, and this year follows the same trend—with new record highs included. All signs point to this momentum continuing. Historically, the second half of the year tends to favor gold prices. Since 1971, average returns during this part of the year have outperformed those of the first half, reinforcing the bullish outlook described by analysts and underpinned by fundamental drivers.

Chris Mahoney, Investment Manager for Gold and Silver at Jupiter AM, is clear in his outlook for the precious metal: “One of the determining factors will undoubtedly be the activity of central banks.” He explains that official purchases tend to intensify in the second half of the year and cites a recent survey by the World Gold Council, which reveals that 43% of monetary authorities intend to increase their reserves in the coming months.

While he does not rule out a moderate correction—especially considering that gold hasn’t seen a drop of more than 10% in over two years—he believes the structural support remains solid.

Another factor Mahoney sees as increasingly influential on gold prices is the U.S. economic cycle. “There are growing signs that the U.S. economy is in a late-cycle phase, which could lead the Federal Reserve to ease monetary policy sooner than expected. If this expectation materializes, it would act as an additional catalyst for gold,” he says.

At the same time, geopolitical tensions remain a key driver. The recent trade truce between the U.S. and China could deteriorate, with negative effects on the global economy and additional pressure on interest rate policy. According to the Jupiter AM expert, “a resurgence of tensions would likely favor gold as a safe-haven asset.”

He also highlights the political context in the U.S.: Fed Chairman Jerome Powell‘s term ends in less than a year, and President Donald Trump—a vocal advocate of low interest rates—has expressed his intention to nominate a successor aligned with that view. Therefore, “any announcement in this regard could significantly shift expectations around rates and inflation, which are fundamental drivers of gold performance,” Mahoney concludes.

Bank of America shares a similar view. The firm recalls that gold reached an all-time high after Independence Day but later gave up those gains. To continue rising, the precious metal needed “a new trigger,” and the U.S. budget could be that bullish driver—“especially if deficits increase.”

The macroeconomic context encourages greater diversification of reserves; central banks should allocate 30% of their reserves to gold. Retail investors are also buying gold, and ongoing macro uncertainty and rising global debt levels remain supportive factors.

In short, the conditions that have driven gold’s recent strength appear likely to persist, according to Bank of America: the structural U.S. deficit; inflationary pressures from deglobalization; perceived threats to the independence of the U.S. central bank; and global geopolitical tensions and uncertainty. That is why the firm has raised its long-term price target for gold by 25% to $2,500 (real).

Ian Samson, Multi-Asset Fund Manager at Fidelity International, also maintains a positive view on gold. He believes bull markets for gold “can last for years” as it continues to provide diversification even when bonds do not, retains its privileged status as a “safe haven,” offers protection against inflation and loose economic policies, and benefits from structural trends.

Samson acknowledges that, given a macro base of economic slowdown in the U.S. or even a potential stagflationary environment in the coming months, he remains positive on gold’s prospects. He argues that the Federal Reserve is ready to cut interest rates despite inflation lingering around 3%, and that tariffs will likely keep prices elevated.

Additionally, the impact of tariff policy and a slowing labor market will also trigger a weak growth environment, in the expert’s view. This combination should support gold, which competes head-to-head with a weakening dollar as a safe haven and store of value. “We’ve never seen this scale of uncertainty and change surrounding tariff policy, and the effects are still unfolding. Furthermore, the size of the U.S. budget deficit raises concerns about monetary debasement, which further strengthens the long-term case for gold.”

Meanwhile, the structural case for investing in the precious metal remains strong, and numerous countries—including China, India, and Turkey—are structurally increasing their gold reserves in an effort to diversify away from the dollar, as gold offers diversification without the credit risk inherent in foreign currency reserves.

Moreover, gold supply remains highly constrained, meaning even a small increase in portfolio allocation could move the needle: “For example, if foreign investors were to decide to move a portion of the $57 trillion they currently hold in U.S. assets, gold would be a more than likely destination.”

For now, Samson says he is “comfortable” maintaining gold in his multi-asset portfolios through a combination of passive instruments that directly track gold prices and a selection of gold mining stocks.

The intentions of U.S. President Donald Trump to influence the Federal Reserve have recently taken another turn with the controversial removal of Fed Governor Lisa Cook, who has already taken the case to court. This pressure from Trump has not gone unnoticed by experts, who, generally speaking, believe that the consequences of this unprecedented situation are unpredictable.

For example, Clément Inbona, fund manager at La Financière de l’Échiquier, is clear that President Trump wants to have the Federal Reserve “in his grasp.” The expert explains that the objectives of this governmental interference stem from Trump’s desire to influence the institution in order to lower interest rates and potentially reduce the cost of U.S. government borrowing—“widely in deficit and heavily indebted—even at the risk of facing dire consequences.”

At this point, Inbona turns to history to detail the consequences of such actions: the Turkish example “is eloquent,” he states, recalling that the country’s president, Recep Tayyip Erdogan, brought the Turkish central bank under his control in 2019 with immediate economic effects: rampant inflation and a large-scale depreciation of the Turkish lira, which amplified the rising cost of imports. “These consequences could loom over the U.S. economy if the Fed were taken over by MAGA America.”

The La Financière de l’Échiquier manager recalls that the Fed’s independence is the result of a progressive achievement. Initiated in 1935 with the separation from the Treasury, it was consolidated in 1951 with the end of public debt monetization—a tool widely used during World War II to finance the war effort and, later, reconstruction. “However, independence does not mean completely escaping government pressure, as shown by Presidents Johnson and Nixon in the 1960s and 1970s,” he notes.

Still, Inbona believes that, in any case, “Trump’s efforts to get the Fed in his grasp matter little,” as the renewal schedule of the institution’s members “works in his favor”: in 2026 he will appoint a new chair, “which will increase his influence” over the institution.

At Edmond de Rothschild Asset Management, they share this perspective. The removal of Governor Cook is interpreted by the firm as an intensification of Trump’s efforts “to take control of the Fed,” a decision that investors understand as a greater likelihood of a more accommodative monetary stance. This environment, they argue, partly explains the drop in interest rates. In addition, the dollar fell again, especially against the euro, due to rising concerns over the Fed’s credibility, according to Edmond de Rothschild AM.

For Tiffany Wilding, economist at Pimco, Trump’s unprecedented decision regarding Cook “eclipsed” Powell’s message in Jackson Hole about a possible rate cut in September. “This event could have consequences for the perception of the Fed’s independence, although the potential impact on Fed policy (and interest rates) is far from clear,” Wilding states.

The expert argues that “this issue goes far beyond Cook” and believes that the accusations “carry political overtones, given the public pressure campaign that Trump has been conducting for a year to push for lower interest rates.” At this point, she explains that although Cook’s replacement would not directly change the voting majority of the Federal Open Market Committee (FOMC), her position is important because it could shift the voting majority of the Board of Governors on issues such as the appointment of Federal Reserve Bank presidents.

“Each regional Reserve Bank board nominates a president for a five-year term, but the final approval lies with the Fed’s Board of Governors. The Board renews the appointment of all presidents at the end of February every five years (in years ending in ‘1’ or ‘6’) in what is usually a procedural vote,” Wilding explains, noting that when the next vote is held in February 2026, “a Board majority favorable to Trump could, at least in theory, veto or reshape the leadership of the regional banks for the next five years.”

She also notes that five regional Reserve Bank presidents are voting members of the FOMC, with one-year rotating terms—except for the New York Fed president, whose position is permanent—“so politically driven changes to their list could affect policy decisions over time.”

There is no precedent for any of this, she notes, but the expert recalls that some legal scholars argue that “a majority of four members of the Fed’s Board of Governors could remove regional bank presidents outside the normal five-year reappointment cycle, though they would have to justify the reason for dismissal.” In short, this would enter “uncharted territory.”

Cook has already taken the case to court. And now, several scenarios are possible. If she does not obtain a court order against the president’s decision, the position could remain vacant while the case proceeds through the courts. But if the court confirms Cook’s dismissal for cause, Senate confirmation of those appointed to the vacant governor positions remains uncertain, despite the Republican majority.

“Key Republican senators have quietly expressed their refusal to appoint a partisan Fed chair, and we could extrapolate this to the Fed board in general,” says the Pimco expert, who believes the renewed attention on the Fed could make it harder for the Senate and the Senate Banking Committee to confirm a Fed nominee who appears too political, too partisan, or too moderate. “Any confirmation process could be difficult and lengthy, potentially leading to a prolonged period of vacancies on the Fed’s Board of Governors,” she concludes.

There is also uncertainty, according to Wilding, about what individual Board governors would do—even if appointed by Trump and confirmed by the Senate—when faced with the reappointment of regional bank presidents. According to Bloomberg, based on a Freedom of Information Act request, current Fed governors Christopher Waller and Michelle Bowman abstained from voting on the 2022 appointment of Austan Goolsbee as president of the Chicago Fed (which was still approved by a majority). However, abstention “has far fewer consequences than overturning decades of precedent and voting to remove a sitting bank president.”

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.

The expert highlighted that the places of origin of ingredients such as austral hake or deep-sea grouper—“which is caught at 2,000 meters, or the famous smoked salmon (sourced from some of the most pristine waters in the world), smoked with native woods like lenga”—give them a unique and unfamiliar flavor, suited to the most discerning palates.