Ali Zaidi, until now head of client business for the Middle East and North Africa at Goldman Sachs Asset Management, has joined DoubleLine Capital as head of international client business. Within his responsibilities, he will lead the firm’s international client team in business development and client service outside the United States.

According to the asset manager, his work and that of his team will be “to help clients align their return and risk management objectives with active investment strategies tailored to a world undergoing both secular and cyclical changes.” Based in DoubleLine’s Dubai office, Zaidi reports to DoubleLine president Ron Redell.

“Under the leadership of CEO Jeffrey Gundlach, and on the strength of our long-tenured investment team and our client-centered service, DoubleLine has established itself as a leading active asset manager. I am delighted to welcome Ali on board. His extensive experience will elevate our firm by bringing our asset management expertise to global clients,” said Ron Redell, president of DoubleLine.

For his part, Zaidi stated: “As an independent, employee-owned firm, DoubleLine has an alignment of interests and values that resonates with clients. I am excited to join and offer our global clients the intellectual leadership and fixed income expertise of our firm.”

Before joining DoubleLine, Zaidi worked from December 2010 until mid-September 2025 at Goldman Sachs Asset Management as managing director, head of MENA client business and new markets, Dubai. In that role, he led a team of client coverage professionals based in London, Riyadh, Dubai, Abu Dhabi, and Doha.

In previous roles, he worked in credit and structured products structuring and sales (including Sharia-compliant products); equity and equity derivatives financial control; and financial services auditing. Over the course of his career, he has been based in London, Kuala Lumpur, and Dubai.

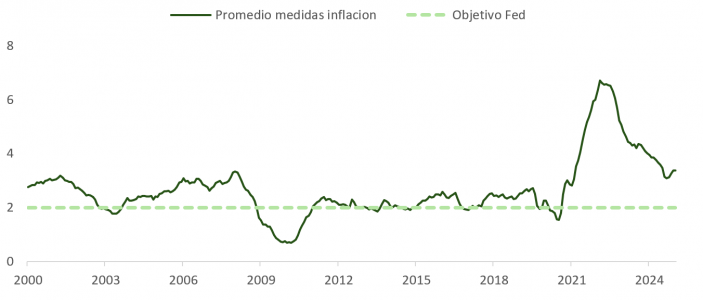

After a nine-month pause, the Federal Reserve cut rates again at its latest meeting—a widely expected decision, though not without implications. Jerome Powell made it clear that the balance between inflation and employment—the core of the Fed’s mandate—has shifted, with growing concern over the deterioration of the labor market.

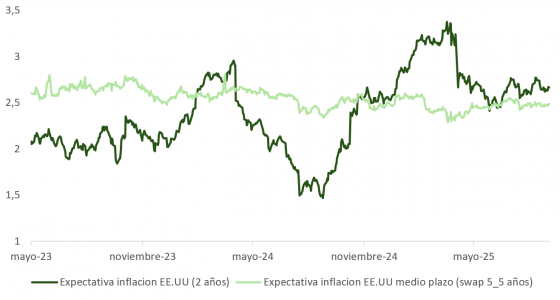

In line with his message at Jackson Hole, Powell emphasized that inflationary risks have moderated. The uncertainty generated by the Trump administration’s tariff policy remains, but the data points to contained inflation in both the short and long term. Metrics such as the “trimmed” CPI (Cleveland Fed) or the “sticky” CPI (Atlanta Fed) have risen since April, although two-year swaps indicate that the peak is already behind us.

The 5y5y swaps, meanwhile, remain stable and very close to the Fed’s long-term target, reinforcing the thesis that the monetary authority is comfortable with the projected level of inflation.

Labor Market: Tensions Beneath the Surface

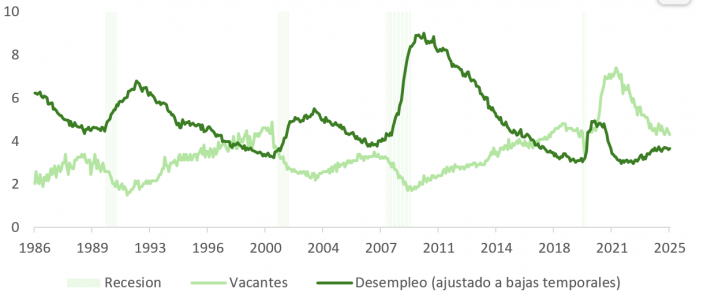

The labor market is now at the center of attention. The sharp decline in immigration has reduced the supply of workers. And although demand has also moderated, the participation rate continues to decline, which keeps unemployment within the Fed’s comfort range… for now.

Revised forecasts for 2026 and 2027 anticipate lower unemployment, but the context remains fragile. The BLS revision placed job creation between March 2024 and March 2025 at 900,000 fewer workers than originally reported. The average number of new jobs created has fallen to just 29,000 per month over the past three months—well below the 70,000 to 100,000 needed to maintain equilibrium. This keeps the Fed on alert, with a high probability of further 25-basis-point cuts in October (87%) and December (92%), according to the futures market and the dot plot. Even so, only half of the FOMC members support this double cut.

Powell was clear: “Labor demand has weakened, and the recent pace of job creation appears to be below the equilibrium rate needed to keep the unemployment rate constant.”

Monetary Policy: The Path Toward Neutrality

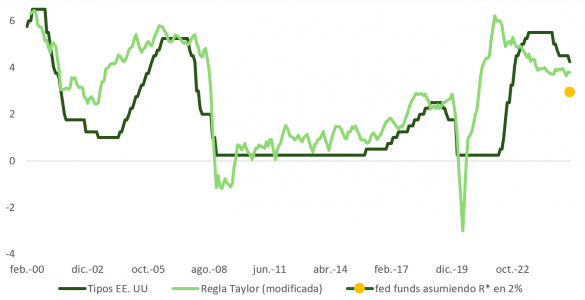

Powell emphasized that there is no predefined plan: each decision will be made meeting by meeting. However, the new balance—less inflationary pressure and greater weakness in employment—suggests that rates should move toward neutral levels.

The Taylor Rule confirms that Fed Funds are still in restrictive territory. The projections implied in the futures and swaps curves appear reasonable, although the margin of error remains high due to macro uncertainty. Powell was unequivocal: “There is no risk-free path.”

Political Tensions and Mixed Signals

During the press conference, questions arose about the apparent disconnect between the economic projections—higher inflation and lower unemployment—and the moderate pace of monetary adjustment. Some interpret this as a sign of political pressure, particularly from President Trump.

The contrast between those favoring a moderate adjustment (Waller and Bowman, with 0.25%) and the more aggressive camp (Miran, proposing 0.5%) could be seen as a statement of independence in the face of external pressure. The Fed appears determined to distance itself from any partisan narrative.

Market Implications: Duration, Dollar, and Positioning

With the curve pricing in up to five additional cuts between now and December 2026, the risk now falls on those holding short dollar positions and long duration.

The OBBA fiscal plan, which balances stimulus with spending cuts, is favorable to growth in 2026. Monetary policy is easing while companies continue to report growth in earnings per share—an unusual combination at this stage of the cycle.

The normalization of the labor market following post-pandemic distortions reinforces the thesis that there will not be a demand-induced recession. The Atlanta Fed’s GDP model for the current quarter, in fact, anticipates an acceleration in growth.

Dollar Valuation and Flows Toward U.S. Assets

The dollar remains overvalued according to purchasing power parity, but its recent drop against the euro has been abrupt. Positioning and sentiment indicators suggest room for a consolidation of the euro’s gains.

Business confidence data in Europe, such as the ZEW or Sentix, deteriorated in September. This increases the likelihood of positive macroeconomic surprises in the United States, which could attract flows toward dollar-denominated assets.

From a technical standpoint, the positive divergence between price and the RSI (Relative Strength Index) reinforces this view of short-term support for the dollar.

The week draws to a close with attention focused on how markets have reacted to the latest monetary policy decisions: the Federal Reserve (Fed) confirmed a 0.25% cut, while the Bank of England (BoE) and the Bank of Japan (BoJ) kept rates unchanged. As a result, the U.S. dollar edged higher on Thursday after a volatile trading session, the British pound weakened, and the dollar/yen rate dropped more than 0.52% immediately after the decision.

According to the view of international asset managers, Western central banks are currently at a point in the cycle close to the neutral interest rate. “That is, the equilibrium point at which interest rates neither restrict nor stimulate economic activity and may be influenced by various factors, such as productivity growth or demographics,” explains James Bilson, global fixed income strategist at Schroders. Despite the great expertise of monetary institutions, it is very difficult to determine exactly what the neutral rate is. In Bilson’s view, if a central bank believes it has reached neutrality, it is likely to react to new data differently than one that believes it is still in restrictive territory.

The Fed: A Balancing Act

In that pursuit of balance, data continues to serve as a compass for monetary institutions and, of course, for the Fed. According to Jean Boivin, head of BlackRock Investment Institute, the outlook for Fed rate cuts depends on the labor market remaining sufficiently weak, making future policy highly data-dependent. In fact, Powell referred to this as a “risk management” cut, emphasizing the move as a form of insurance against growing signs of labor market weakness.

For Boivin, it is important to take a broader view. “Powell acknowledged that there is no risk-free path for policy and the ongoing tension in his dual mandate to support growth and contain inflation. We see the real tensions elsewhere: keeping inflation in check and managing debt servicing costs. Again, a weak labor market gave the Fed cover to resume rate cuts. That tension between inflation and debt servicing costs could easily reemerge if Fed rate cuts help boost business confidence – and hiring. For now, markets see that tension easing – and the premium investors demand for holding long-term bonds has sharply declined in recent weeks,” he notes.

BoE: Containing Inflation

In the United Kingdom, the Bank of England (BoE) met market and expert expectations by holding interest rates steady, once again at 4%. According to Mahmood Pradhan, director of Global Macroeconomics at the Amundi Investment Institute, although the decision was clear, the monetary institution still faces tough choices on what to do next. “August figures showed that inflation is high and persistent, but growth is patchy, and the Fed appears to be back on a prolonged rate-cutting path. We believe the BoE will need to cut 25 basis points in December, and reducing its balance sheet by £70 billion over the next 12 months is in line with expectations, but the £20 billion reduction in gilt sales should support the bond market,” explains Pradhan.

According to Mark Dowding, BlueBay CIO at RBC BlueBay Asset Management, the BoE governor may want to cut rates if possible, but this will depend on price moderation or a faster cooling in employment data. His outlook is clear: “We continue to believe that stagflation risks are present in the UK, and therefore it will be difficult for the BoE to act. Meanwhile, political risks keep us cautious on the pound. Certainly, if Starmer were to step down suddenly at some point, we think this could lead to significant pressure on UK assets and the currency, due to fears of a more hard-left alternative.”

BoJ: A Hawkish Tone

In Japan’s case, the BoJ kept rates unchanged—a decision also widely expected by the market. However, experts noted the surprisingly hawkish tone, and a rate hike is now being priced in for the October meeting. According to Dowding, it seems plausible that the BoJ wants to wait for greater clarity around Japan’s political leadership following Ishiba’s departure. “If the LDP leadership race results in a ‘business-as-usual’ candidate like Koizumi, this could pave the way for a potential rate hike as early as October – a scenario that could also see the yen strengthen further,” says the RBC BlueBay AM expert.

For Christophe Braun, Director of Equity Investments at Capital Group, the BoJ’s decision underscores its cautious stance amid slowing inflation and global uncertainty, prioritizing stability over premature tightening. “By preserving policy flexibility, the BoJ signals its readiness to respond to external volatility while continuing to assess the strength of Japan’s economic recovery. Unlike the U.S. and Europe, where central banks are leaning toward rate cuts, Japan’s macroeconomic conditions require a more deliberate approach. The BoJ’s strategy supports the early stages of a deflationary cycle, rather than reversing course. We expect the yen to strengthen gradually as interest rate differentials narrow, which will increase Japan’s purchasing power and support domestic demand,” explains Braun.

The U.S. SEC approved new rules that simplify the listing of exchange-traded products (ETPs) based on commodities, including those backed by cryptoassets.

The measure will allow three national securities exchanges to list and trade these instruments under generic standards, eliminating the need for individual agency approval in each case. From now on, if an ETP meets the established requirements, the exchange will only need to publish information on its website within five business days after the start of trading. “This simplified listing process will benefit investors, issuers, other market participants, and the Commission by reducing the time and resources needed to bring new ETPs to market,” the regulator stated in a press release.

According to the SEC, the goal is to facilitate market innovation without compromising investor protection.

In the past, the agency had been criticized for delays and regulatory hurdles, especially regarding ETPs linked to cryptoassets. Until now, exchanges were required to demonstrate that they had surveillance-sharing agreements with regulated markets of significant size, which limited the development of such products.

New Eligibility Criteria

With the approved rules, the underlying commodities of an ETP may be considered eligible if they meet any of the following requirements:

Listed on a market that is a member of the Intermarket Surveillance Group.

Underlie a futures contract with at least six months of trading on a market regulated by the CFTC.

Represented in an ETF that allocates at least 40% of its net asset value to that commodity and is already listed on a national exchange.

In this way, ETPs based on cryptoassets will have a clearer and more direct path to market.

The SEC emphasized that exchanges will still need to file special applications when a product does not meet the generic standards. However, it left the door open for the criteria to be expanded in the future, for example, through objective quantitative standards that would provide more predictability and speed in the approval of new instruments.

The report, produced by One Goldman Sachs Family Office, gathered the opinions of a total of 245 decision-makers in family offices around the world on how they are approaching the current complex investment landscape.

“Family offices have shown extraordinary consistency in their investment approach, despite concerns over geopolitical tensions and protectionist trade policies. The 2025 results underscore how long-term orientation and flexibility enable family groups to manage volatility and seize opportunities,” says Meena Flynn, Co-Head of Global Private Wealth Management and Co-Head of One Goldman Sachs, in the report’s conclusions.

Key Findings

The document shows that portfolios remained in line with those of 2023, with slight shifts in allocations to listed equities (rising from 28% to 31%) and a slight decline in alternative assets (from 44% to 42%). Moderate increases in investments in private credit, fixed income, real estate, and private infrastructure partially offset the slight decrease in private equity. When it comes to risks, geopolitics remains the main concern. In fact, 61% of respondents cited geopolitical conflicts as the greatest investment risk, followed by political instability (39%) and economic recession (38%).

As in 2023, geopolitical conflicts remain the most cited investment risk, with 61% of respondents including it among their top three concerns (75% in APAC) and 66% expecting geopolitical risks to increase over the next year. Political instability (39%) and economic recession (38%) follow closely, with global tariffs not far behind (35%). According to the report, most now consider higher tariffs to be the new normal, with 77% expecting increased economic protectionism and 70% anticipating tariff levels to remain stable or rise over the next 12 months. Even so, respondents generally believe that the fundamental drivers of global growth and traditional investment themes remain intact.

Among the conclusions, it stands out that family offices are willing to allocate capital. In this regard, more than one-third of respondents plan to reduce their cash balances (currently at 12%) and invest in risk assets. Notably, most family offices plan to increase their exposure to private equity (39%), followed by equities (38%) and private credit (26%).

Innovation and Thematic Trends

Finally, a key trend is that family offices are becoming more open to investing in technology, especially in AI. “58% expect their portfolios to overweight the sector in the next 12 months. Widespread investments in artificial intelligence (AI): 86% have exposure to AI, largely through listed equities, although many cite concerns about valuation,” the report notes in its conclusions.

In addition to AI, a growing interest in cryptocurrencies has been observed: 33% invest in cryptocurrencies compared to 26% in 2023. A relevant nuance is that the APAC region shows the greatest interest in future investments.

Asset Allocation

Family offices maintain a strong weighting in risk assets, with public equities at 31% and alternatives at 42% (with private equity standing out at 21%). There are slight increases in real estate, infrastructure, and private credit, the latter booming due to its attractive yield. Exposure to hedge funds remains stable, though with greater interest in EMEA and APAC. Looking ahead, they plan to maintain overall stability with selective adjustments: more allocations to private equity (39%), public equities (38%), and private credit (26%), along with a reduction in cash (34%).

On the other hand, innovation is emerging as a central driver. Most are already investing in artificial intelligence, and many are integrating it into their investment processes, with expectations that the technology will gain more weight in portfolios. Interest is also growing in digital assets, especially in Asia-Pacific, as well as in secondary markets due to their increased transparency. Another emerging area is sports, where a growing number of family offices are seeking opportunities related to both teams and media/content.

“Artificial Intelligence Is Constantly Evolving, and That Makes It Both a Challenge and an Opportunity” — This statement was made by Elena Alfaro, head of global AI adoption at BBVA, during her presentation titled State of the Art of AI and Use Cases at BBVA, delivered at the first Funds Society Leaders Summit recently held in Madrid.

What Alfaro means is that “AI is constantly evolving, with impact across various sectors; anyone who feels it’s moving incredibly fast is not mistaken—this is a full-blown revolution.” Just one data point proves the case: ChatGPT has been the fastest-adopted technology to date, reaching 100 million users just two months after its launch. Moreover, the expert stated, “ChatGPT is the most successful product in history.”

In fact, Alfaro noted, today, OpenAI (the company that owns ChatGPT) is generating 700 million active users per week, of which around 20 million are paying users. The BBVA representative added that if the user bases of the main competitors in this field are added, there are likely more than 1 billion generative AI users worldwide. Furthermore, considering that AI is part of a technology ecosystem born in the U.S., it has taken only three years to reach 90% of users outside the U.S. (compared to the 23 years it took the internet).

Double-Digit Investment

The BBVA representative also pointed out that the drop in costs has been dramatic since its launch three years ago. This, combined with user interest, has led to spectacular growth in every sense. Reflecting this trend, job openings in the U.S. IT sector related to AI have surged by 448%, while non-AI IT jobs have contracted by 9%.

That said, hyperscalers have doubled down on their AI development investments. Alfaro recalled that the so-called Big Six increased their capex by 63% from 2023 to 2024—a figure that was already high, reaching $212 billion.

Alfaro did not shy away from acknowledging that it’s unclear whether all the major players in this race are generating profits. She cited NVIDIA as the obvious beneficiary—thanks to GPU sales—and Accenture for the success of its AI-related services business line. Additionally, she stated that OpenAI is expected to report revenues of $12 billion by the end of 2025. Even so, the expert explained that major tech firms will continue doubling down on their investments because “they are making a long-term bet on this technology.”

Five Relevant Trends in the Financial Industry

Given that something that happened in April already feels “almost like the Pleistocene” in this fast-moving space, Alfaro outlined five trends that are already impacting the financial industry and that users should understand and familiarize themselves with.

Expansion of Reasoning Capabilities in Language Models Alfaro explained that we are now dealing with AIs that respond versus AIs that reason—and the final result can differ greatly depending on the task assigned. Reasoning AIs can break down problems through chains of thought, follow logical steps, take time to reason, and flag doubts when needed (she cited GPT-5, Gemini 2.5Pro, and Claude 3.7–4 as examples). On the other hand, non-reasoning bots offer faster responses without verifying or cross-checking information (GPT-4, Gemini 1, Grok 2, Deepseek Base). “This reasoning capability needs to keep advancing because otherwise, automating complex tasks will remain limited,” reflected the BBVA representative.

Multimodality This refers to the shift from generative AI being text-only to now encompassing images, video, voice, music, or combinations thereof—capable of generating diverse outputs.

Evolution from Assistants to Agents We are moving from bots that respond to human prompts to AIs that can be given goals and execute them autonomously. Alfaro forecasts that, eventually, each person could have their own “AI Chief of Staff” — capable of coordinating a group of AIs to carry out complex tasks.

Integration of Data and Tools Currently, ChatGPT typically isn’t connected to internal corporate data sources (like Salesforce, Google Drive, Outlook, etc.), but “there is significant progress in enabling connectivity to integrate company data sources or apps.” She stressed the importance of this integration for task automation and added, “Security and compliance teams will play a fundamental role in this integration.”

Growth of No-Code Tools “From now on, we’ll be able to do more complex things,” said Alfaro, citing Google Flows, a new tool that helps chain together processes, as an example of what’s coming next.

AI Use Cases at BBVA

Finally, the head of global AI adoption at BBVA shared that the bank is developing a portfolio of various projects across areas such as risk, operations, and software development.

One example is the mobile banking app Futura, which adapts to each user based on their activity and finances—for example, by identifying their most frequent operations and offering shortcuts. It also includes Blue, a chatbot similar to ChatGPT that answers user questions ranging from product inquiries to detailed personal finance queries.

BBVA is also engaged in a highly ambitious project grounded in the philosophy of AI adoption among employees: “This is a people project, not just a technology deployment project. Technology is very important, but it’s people who must adopt it,” she emphasized.

Launched in May last year, the initiative began by making AI capabilities available to a growing number of employees to help boost productivity, encourage creativity, and enable them to build their own assistants. The results, according to Alfaro, have been “extraordinary”: the program has achieved nearly 90% user retention and led to the creation of over 5,000 functional applications by people with no coding experience. Around 1,000 high-value use cases have already been identified and are being implemented, leveraging solutions from OpenAI and Google.

Conclusion: Better In Than Out

In conclusion, Alfaro emphasized that in the face of this revolution, “it’s better to be in than out; staying out doesn’t make much sense.”

She closed her talk on an optimistic note, asserting that humans won’t be left out of the equation. Instead, their role will evolve from task executors to orchestrators—though with important nuances: “We should always analyze tasks from the perspective of what makes sense for AI to do and what makes sense for a human to do.” She cited a study indicating that skills such as organization, prioritization, and training still require strong human involvement. In her view, the most likely outcome is a division of labor, leading to the evolution of current roles and the creation of new ones. “In that evolution, continuous training for all employees is key,” she concluded.

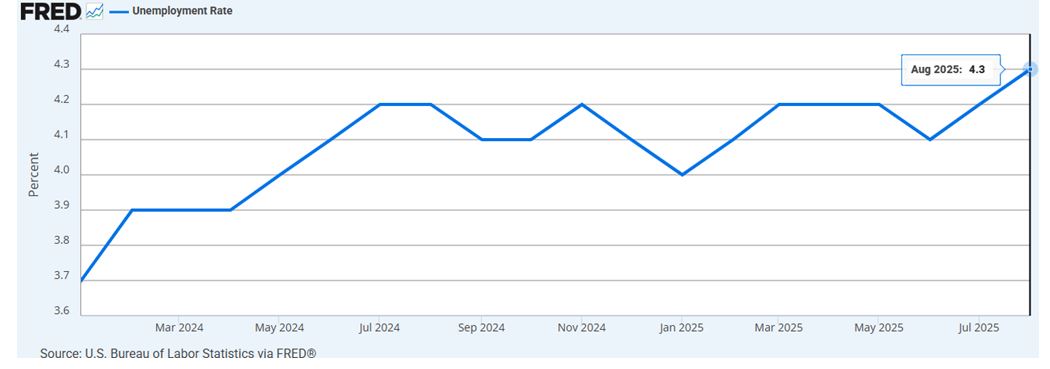

The U.S. labor market is showing clear signs of weakness. In August 2025, the economy generated only 22,000 nonfarm jobs, far below the expected 75,000, pushing the unemployment rate up to 4.3%, the highest level since 2021. This comes on top of the largest historical job revision in decades, with 911,000 positions erased from the statistics between 2024 and 2025.

This cooling of the labor market reinforces expectations that the Federal Reserve (Fed) will accelerate its interest rate cut cycle, with the possibility of further adjustments in the coming months.

For asset managers, this environment combines risks and opportunities, according to FlexFunds. On the one hand, traditional assets—equities and fixed income—may face limited returns and greater volatility. On the other hand, asset securitization is emerging as a key tool to diversify portfolios, improve liquidity, and enhance the distribution of investment strategies across international private banking platforms.

When unemployment rises and the Fed is forced to cut rates to contain recession risks, equity and bond returns tend to carry more systemic risks. In this context, accessing less correlated asset classes becomes a strategic priority.

Securitization allows liquid, illiquid, listed, and alternative assets to be repackaged into investment vehicles and distributed across multiple international private banking platforms. This gives managers access to cash flows different from traditional ones, reducing dependence on immediate macroeconomic performance.

A recurring challenge in times of heightened uncertainty is the need for liquidity without sacrificing diversification. Through structures such as Special Purpose Vehicles (SPVs), developed by FlexFunds, managers can transform illiquid assets into easily transferable and Euroclearable instruments, optimizing both operational and tax efficiency.

This benefit is significant: in an environment where investors demand agile and transparent solutions, securitization provides investment strategies with scalability, strengthens distribution, and facilitates capital raising in international markets.

Historically, rate cuts have increased the price of outstanding bonds, benefiting those who already had duration exposure. However, for new investment flows, a low-rate environment implies limited yields and narrower spreads.

In this scenario, the securitization of alternative assets becomes an effective way to capture attractive spreads without disproportionately increasing exposure to market volatility. Managers can offer vehicles backed by stable cash-generating assets that complement and reinforce the return structure of a multi-asset portfolio.

Competitive advantage of securitization for asset managers

Rising unemployment and the expectation of rate cuts in the U.S. mark a turning point in asset allocation strategies. In this new environment, securitization consolidates itself as a mechanism that provides competitive advantages:

Transforms investment strategies into a vehicle with easy access and international reach.

Expands the client base quickly and efficiently.

Enables portfolio diversification beyond equities and fixed income.

The creation and issuance process is fast and cost-efficient.

Provides liquidity to traditionally illiquid assets (such as real estate).

Enhances capital-raising capabilities.

Adds scalability to investment strategies.

Diversifies funding sources.

Involves low operational costs.

Can be issued on relatively small asset portfolios.

For asset managers, the key will be integrating these vehicles into portfolio architecture not as substitutes but as strategic complements that strengthen the value proposition to increasingly demanding clients in a macroeconomic environment filled with uncertainty.

With FlexFunds, it is possible to design and issue efficient, flexible investment vehicles tailored to each client’s needs. Our solutions are designed for managers seeking to scale their strategies in international capital markets and broaden their investor base.

For more information, please contact our specialists at info@flexfunds.com.

Despite the short- and medium-term challenges Chile faces, investors remain confident in the country’s potential. This was clearly reflected in the panel “Why Invest in Chile?” held during Chile Day Madrid, hosted at Casa América in the Spanish capital.

In this expert panel, moderated by Soledad Vial, Editor of Economía y Negocios at El Mercurio, participants discussed both the strengths and the improvements needed for Chile’s economy to take off. Rosario Navarro, President of Sofofa—the trade federation representing Chile’s private business sector—opened the discussion by highlighting the country’s key advantages, particularly a “privileged environment” and strong “geological potential.” She also pointed to the steady reduction of poverty, a notable GDP, and advancing infrastructure.

David Ruiz de Andrés, CEO of Grenergy, stated that the reasons to invest in Chile are clear: the country has a stable renewable energy policy, which he called “fundamental.” He also emphasized Chile’s openness to international investment and its ability to become “a benchmark” and laboratory in sectors such as energy storage. “Chile has copper, lithium, and the best solar resource in the world,” said Ruiz de Andrés, adding that the country “could become a major data exporter.”

Vicente Huertas, General Manager of Indra Group for Peru, Chile, and the Southern Cone, affirmed that Chile continues to be a reference point, particularly in the field of digitalization. He also highlighted the country’s mobility and “excellent communications,” as well as the regulatory stability needed for long-term investments. Meanwhile, Cristián Infante, CEO of Arauco, underscored that “Chile remains attractive,” even as the company expands into new markets such as Brazil.

Challenges to Address

Panelists agreed on the need for Chile to boost economic growth. “The country needs to regain the momentum it had when we first arrived here,” said Ruiz de Andrés, who added that Chile “must believe in the enormous potential it has.” He cited Grenergy’s “Oasis Atacama” project, for which the company has brought 12 international banks into Chile.

The relationship between investors and both local and national governments, as well as with local communities, was another key topic. “I know more ministers in Chile than in Spain,” noted Ruiz de Andrés. Infante highlighted the proactive role local governments play in supporting investment, stating that this creates a “virtuous circle.” Both executives emphasized their companies’ sensitivity to local communities. “It becomes a learning process when there is dialogue with the community, because when they get to know you, they support your activity,” said Infante.

Huertas focused on advances in regulations related to cybersecurity, artificial intelligence, and other technologies “that will help develop these capabilities.” Navarro emphasized the many good practices brought into Chile that “have raised standards” and encouraged demanding high standards in relationships with local communities where projects are developed.

Electoral Outlook

The roundtable also addressed business leaders’ expectations ahead of the country’s upcoming elections. Overall, the panelists expressed little concern. Ruiz de Andrés hopes the outcome marks the beginning of a new cycle in which Chile believes in its own capabilities. Infante would be satisfied if the country stopped seeing “the glass as half empty.” He reminded attendees that Chile “has a solid foundation and all the candidates are aware of the challenges that need to be addressed.”

With Indra operating in Chile for 25 years, Huertas asserted, “We are not afraid of the elections.” He clarified that key issues like cybersecurity and digitalization “are state matters” that go beyond specific administrations and are certain to remain “a growth driver.”

Navarro shared a similar view: “The business world invests long-term and lives through many governments,” she said, adding that there is a clear consensus that Chile must return to growth—“but not at any cost.”

What the New Government Should Prioritize

Panelists also shared what they believe the new government should prioritize. Huertas suggested the need for “territorial integration,” noting a digital divide and calling for modernization of systems. Ruiz de Andrés pointed out a “huge gap” between management training and that of the rest of the workforce, concluding that “we must enable social mobility.”

Infante called on candidates to implement “efficient laws” that allow for project development, arguing that “the way to generate resources is not through higher taxes.” According to Navarro, Chile must improve its competitiveness—in taxes, permitting, labor market regulation, and productivity. She also called for reforms to the education system, stating that “the way we educate isn’t working,” and proposed dual education as a potential solution.

Central banks are in the spotlight this week with a very full calendar, as the U.S. Federal Reserve (Fed) speaks tomorrow, the Bank of England (BoE) on Thursday, and the Bank of Japan (BoJ) on Friday. These meetings follow last week’s European Central Bank (ECB) decision and come alongside macroeconomic data that will frame monetary policy decisions in the coming days.

“Beyond these three central bank meetings, the economic data agenda is fairly light. On Monday, manufacturing data was released in China, while Tuesday will bring industrial production figures in the EU and the ZEW business climate index in Germany. Thursday will see the release of weekly jobless claims in the U.S., which will likely attract attention following the recent weak labor report. After all, the Fed’s mandate includes ensuring full employment and price stability,” states Hans-Jörg Naumer, Global Head of Capital Markets & Thematic Research at Allianz Global Investors.

Following the Jackson Hole symposium, the Fed’s FOMC meeting is undoubtedly the most notable. BofA experts forecast a 25 basis point cut, bringing the rate to 4%-4.25%, with the 2026 median still reflecting two more cuts. “Powell’s press conference will echo labor market developments and provide insights into the tariff impact on production and prices. Rates and the exchange rate could be interpreted as an aggressive cut. In principle, ‘we rule out any possible appreciation of the dollar,’” states Bank of America’s outlook.

Regarding the data on the FOMC’s table, experts at the firm predict a solid retail sales figure for August, above consensus, which should keep uncertainty alive about the strength of spending and weakness in labor data. “Moreover, we forecast that unemployment claims will fall to 240,000 in the week ending September 13, as the previous week’s increase was mainly due to the deadline for filing claims related to flooding in Texas,” they note.

BoE: Rates to Remain Unchanged

Regarding the BoE meeting, which remains highly attentive to CPI and employment data, the bank’s experts anticipate it will maintain its stance with a 7–2 vote, with a risk of a more dovish voting pattern. “The benchmark rate will remain at 4% on Thursday. The recent emphasis by the Monetary Policy Committee (MPC) on elevated inflation expectations suggests a risk that policy will remain unchanged for the rest of the year. This week’s releases on the labor market and CPI will be key. The pace of quantitative tightening (QT) for 2025/26 will also be announced: annual sales are expected to drop from £100 billion to £75 billion, with risks skewed toward a greater reduction,” states Shaan Raithatha, Senior Economist and Strategist at Vanguard.

BofA shares a similar view: “The July labor market report should show a stable unemployment rate at 4.7% (with upside risks) and further progress in wage growth (with private sector wages growing at 4.7% year-on-year). We expect UK CPI inflation to decrease slightly to 3.7% in August, and services inflation to fall from 5% to 4.7%.”

According to Raithatha, the short-term outlook has turned more hawkish. “Upward revisions to payroll declines suggest the labor market is weakening rather than collapsing. And the MPC signaled a change in tone at the August meeting, with a renewed focus on second-round effects of elevated inflation expectations (see chart). Thus, our forecast for one more cut before the end of the year is at risk. We are inclined to postpone it until 2026 if the labor market and CPI data (due Tuesday and Wednesday) broadly meet expectations,” he explains.

In the view of David Rees, Head of Global Economics at Schroders, stagflationary pressures would also prevent the BoE from implementing further interest rate cuts. He explains that it is unlikely GDP growth will exceed 1% significantly, but capacity constraints mean even such modest growth rates will keep inflation elevated for some time.

“In fact, we fear inflation will exceed 4% in the coming months and remain above 3% at least until mid-2026. Without a sharper weakening in the labor market or fiscal tightening in the autumn budgets, it is likely that the bank rate will remain at 4% in the immediate future,” notes Rees.

BoJ: Waiting for Its Moment

In Japan’s case, experts start from the premise that the country’s outlook is mixed, with growth supported by exports but moderate domestic demand. They also note that political uncertainty—the resignation of the prime minister—limits fiscal stimulus and structural reforms. In the view of Luca Paolini, Chief Strategist at Pictet AM, the BoJ is in a wait-and-see mode. “For now, with moderating inflation in services, there is no pressure to accelerate rate hikes. But it may carry out two rate increases in 2026, and its quantitative tightening will continue,” he notes.

Edmond de Rothschild AM highlights that headline inflation slowed from 3.3% to 3.1% but still remained above the Bank of Japan’s target, while core inflation held steady at 3.4%, giving the monetary authority room to maneuver.

“We expect the Bank of Japan to keep its official interest rate unchanged at 0.5%. We believe the bank will maintain its current message of closely monitoring data as of August and that the current political instability will not affect its rate hike decisions. We forecast that core CPI, similar to Japan’s measure, will decelerate further to 2.7% year-on-year, from 3.1% year-on-year. Core CPI, as defined by the BoJ (excluding energy), should also decelerate, as anticipated by Tokyo’s main CPI,” add BofA analysts.

Global investment firm Carlyle and Invesco have announced an agreement under which Carlyle will acquire intelliflo, a UK-based provider of cloud-based management software for independent financial advisors (IFAs), previously owned by Invesco. According to the asset manager, this transaction includes intelliflo’s U.S. subsidiaries, including RedBlack, a provider of SaaS portfolio rebalancing tools, and intelliflo Portfolio, a portfolio management software solution for registered investment advisors (RIAs) in the U.S.

Regarding deal details, the firm states that the purchase price of up to $200 million consists of $135 million at closing and up to an additional $65 million in potential future earn-outs. As part of the transaction, intelliflo’s U.S. subsidiaries will be established as an independent company named RedBlack, managed by a separate leadership team. This separation will allow both companies to better serve their current clients and markets. intelliflo will focus exclusively on delivering leading software and innovation to the UK and Australian markets, while RedBlack will concentrate on serving RIAs and other financial advisors in the U.S. Carlyle will support the separation of both companies from Invesco and work alongside their respective leadership teams to execute their growth plans.

The investment will be funded through Carlyle Europe Technology Partners (CETP) V, a €3 billion fund that invests in technology companies across Europe. The CETP team has extensive experience in financial software, wealthtech, and sector-specific SaaS, with recent investments in companies such as SER Group, CSS, SurePay, and Calastone.

“intelliflo is a critical software provider in the UK wealth management ecosystem, with a deeply loyal client base. We are excited to partner with Nick, Bryan, and their team to unlock the full potential of the company and lead it into its next phase of growth,” said Fernando Chueca, Managing Director on CETP’s investment advisory team.

For his part, Nick Eatock, CEO and founder of intelliflo, commented: “This is a very exciting moment for intelliflo. Carlyle’s investment reflects their confidence in our business, and their extensive experience in scaling software companies makes them the ideal partner for our next phase of growth. With Carlyle’s support, we will remain focused on delivering strong value to our clients, with renewed momentum in developing innovative solutions for the evolving needs of our core markets in the UK and Australia.”

“Our team is highly motivated by the opportunity to focus all our energy on the U.S. market as an independent and agile company. RedBlack has a long history of delivering market-leading software solutions to our RIA client base in the U.S. We’re excited to have the backing of a partner with Carlyle’s reputation and expertise, which will allow us to continue supporting financial advisors in the best possible way,” added Bryan Perryman, CEO of the new RedBlack.

“As intelliflo and the newly formed RedBlack begin their next growth phases alongside Carlyle, we are confident that both companies are well positioned to continue their success and innovation in the wealthtech space. We look forward to continuing our collaboration with intelliflo and RedBlack through our shared relationship with wealth advisory clients,” concluded Doug Sharp, Senior Managing Director and Head of Americas and EMEA at Invesco.

Founded in 2004 and headquartered in London, intelliflo offers a comprehensive software platform used by over 30,000 professionals across approximately 2,600 advisory firms, supporting the management of around £450 billion in client assets. Its platform includes CRM, financial planning, client onboarding, compliance workflows, and reporting functions. Its cloud-native, client-specific SaaS architecture integrates with more than 120 third-party applications. The transaction aims to strengthen intelliflo’s leadership in the UK and accelerate its growth in Australia.