The U.S. Securities and Exchange Commission (SEC) has published a planned order—currently open to public comment before any changes or developments—that specifically applies to Dimensional Fund Advisors and allows the firm to add exchange-traded share classes to mutual funds. According to experts, this is a discussion the industry has long anticipated.

“The Commission is taking a long-awaited step toward modernizing our regulatory framework for investment companies, reflecting the evolution of collective investment vehicles from being primarily daily redeemable funds to exchange-traded funds (ETFs),” said Commissioner Mark T. Uyeda.

As explained by Reuters, under the proposed change, a mutual fund could offer investors the opportunity to participate in its investment portfolio in the form of an exchange-traded product, known as an ETF share class. “Investors would be able to buy and sell shares of the exchange-traded mutual fund throughout the day at market price through their brokerage accounts, instead of waiting for a mutual fund order to settle at the end-of-day price. This has the potential to open access to a range of existing funds for investors who prefer owning ETFs due to their low cost, tax advantages, or liquidity,” they noted.

Offering different share classes of the same mutual fund is not new. As Reuters points out, these classes are currently often targeted at different investor groups or carry varying fee structures. However, they note that the change could blur the line between exchange-traded funds and traditional mutual funds.

In Uyeda’s view, this is a principled modernization. He emphasized that the application includes several safeguards: board oversight, adviser reporting, conflict monitoring, and investor disclosure. “These are not mere administrative formalities—they are essential guardrails and uphold the fiduciary duty,” he added.

For many in the industry, this planned order signals the SEC’s intent and marks the direction of change the agency aims to pursue. In this regard, Uyeda was clear: “The publication of this notice represents a substantive step forward, not just a procedural formality. It’s a signal that the Commission is willing to reexamine outdated restrictions, embrace innovation, and consider an exemption that could equally benefit investors, fund sponsors, and markets. It reflects the same innovative spirit that led to the creation of the first ETF more than three decades ago.”

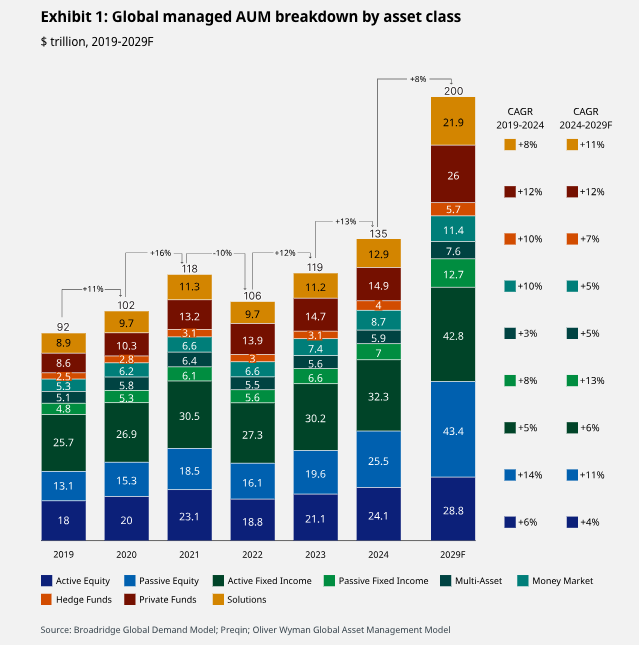

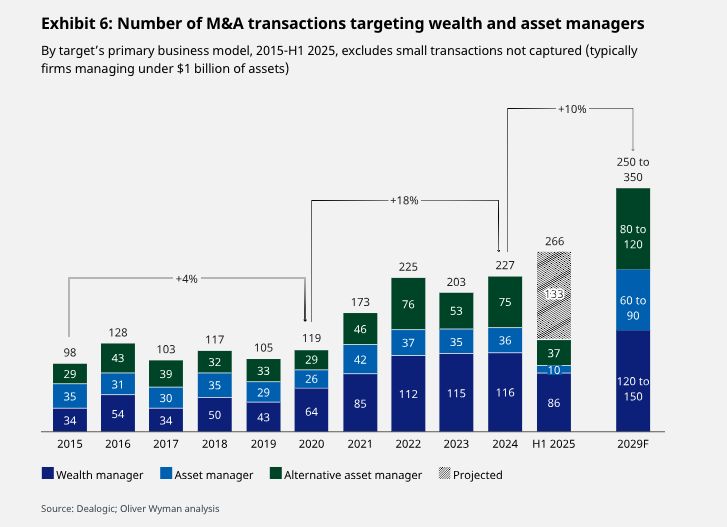

The consolidation of the asset management industry is unstoppable. According to the latest edition of the report prepared by Morgan Stanley and Oliver Wyman, the number of asset managers will decline by 20% over the next five years. Additionally, global assets are projected to reach all-time highs of $200 trillion, representing an annual growth rate of around 8% and a cumulative increase of 48%.

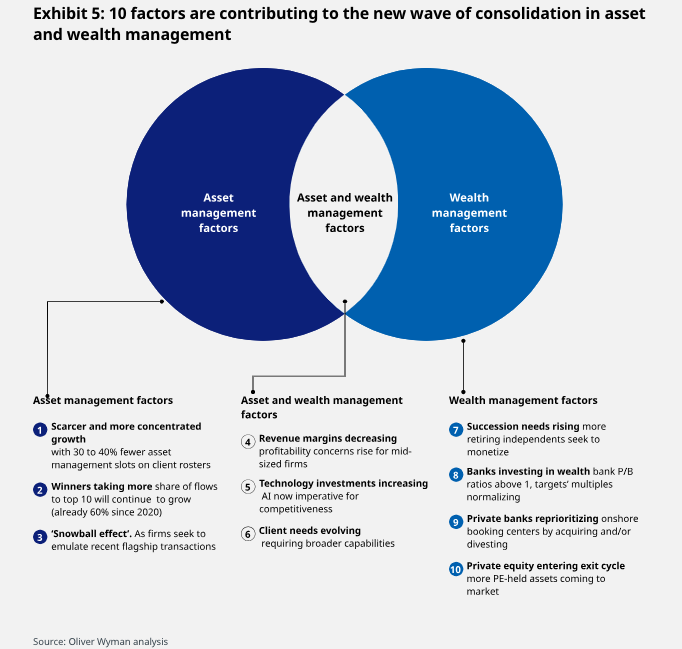

These conclusions were reached after analyzing how the asset management business is evolving and how the industry consolidation process is progressing. “As players consolidate, internalize, and shift toward strategic partnerships, and wealth management clients raise their expectations and professionalize their relationships (for example, through the use of family offices and multi-family offices), growth opportunities are becoming scarcer and more concentrated. We expect the combination of these factors to drive consolidation, as mid-sized players become attractive acquisition targets for leaders seeking greater scale and diversification,” the report states.

According to the analysis in the report, the effects are already being felt: the number of transactions has entered a new normal of over 200 significant deals per year since 2022—double the rate of the previous decade—in both asset management and wealth management. “The asset management industry is no longer producing new fund or ETF managers: with an average of more than 150 over the past two decades, net annual additions of traditional asset managers have dropped to a handful in the past three years. Even the active private markets are showing a similar trend,” it notes as a key data point.

Consolidation Continues

The report estimates that by 2029, there will be over 1,500 significant transactions in asset and wealth management, resulting in up to 20% fewer asset managers with at least $1 billion in assets over the next five years. “Success in this new era of consolidation will require asset and wealth managers to consider mergers and acquisitions as a central lever in their growth strategies,” the report concludes in light of this trend.

When it comes to deal activity, mid-sized asset managers (with between $500 billion and $2 trillion in assets) are the most exposed. According to the report, they show lower profitability—with operating margins around 26%—compared to larger managers (around 44%) and smaller ones (around 36%). Their profitability has fallen by approximately 4 percentage points since 2019, while small and large firms have remained relatively stable. Furthermore, the report estimates that there will be between 30% and 40% fewer clients for asset managers, as clients consolidate, internalize more than they outsource, and seek to do more with less.

The Outcome of M&A Deals

Although most mergers in the asset management sector have historically struggled to deliver meaningful improvements in cost-to-income ratios, the report argues that “a new mergers and acquisitions strategy can generate value.” According to its analysis, approximately 40% of traditional managers managed to improve their cost-to-income ratios three years post-deal, with the greatest cost savings coming from support and control functions. The firms that succeeded were those that balanced aggressive cost-cutting with careful management of client attrition following the merger. Moreover, three years after the deal, one-fourth of merged firms significantly outperformed the market’s organic growth rates. “Successful firms focused on client and product complementarity rather than merely on generating cost synergies,” the document notes.

Another key finding is that half of the alternative investment firms acquired by traditional managers grew significantly faster than the market by leveraging—and improving—the traditional manager’s distribution scale. In this regard, the report concludes that further value is likely to be unlocked by incorporating alternative managers into pension funds in Europe and the United States.

Types of Transactions

These arguments are fueling sector consolidation, which, according to the report, is taking place through three types of transactions. It notes that bank-affiliated wealth managers involved in M&A activities improved their cost-to-income ratio (CIR) by 0.5 points between 2022 and 2024, while others saw their CIR increase by 2.3 points. “This is the result of a careful reprioritization of domestic accounting hubs and subsequent acquisitions and divestitures,” the report explains.

It also expects more banks to expand into non-bank wealth management channels (independent managers and digital distribution).

In the consolidation of independent wealth managers (RIAs, IFAs, etc.), multiple arbitrage has historically driven most of the value creation, followed by cost synergies. However, attention is now shifting toward capturing revenue synergies driven by enhanced tools and increased investment in data and analytics. The report identifies that the next frontier for independent managers focused on UHNW clients (with $30 million or more in investable assets) is international expansion.

“Looking ahead, we expect most of the activity to come from cross-sector deals with insurance companies and asset managers that reassess whether they are the right owners of their asset management businesses and consider the possibility of pursuing mergers and acquisitions,” the report states among its main conclusions.

CaixaBank, ING, Banca Sella, KBC, Danske Bank, DekaBank, UniCredit, SEB, and Raiffeisen Bank International have announced the creation of a euro-linked stablecoin, designed in accordance with the European Union’s Markets in Crypto-Assets (MiCA) regulation. This new digital payment instrument, based on blockchain technology, aims to establish itself as a trusted benchmark within the European financial ecosystem.

The stablecoin will enable near-instant, low-cost, and 24/7 available payments and settlements, including cross-border transactions, programmable payments, improvements in supply chain management, and the settlement of digital assets such as securities and cryptocurrencies. According to Mariona Vicens, Director of Digital Transformation and Advanced Analytics at CaixaBank, “Technology is profoundly transforming financial infrastructure, especially the standards for conducting payments and transactions. At CaixaBank, we have been pioneers in early-stage innovations that later contributed to the transformation of payment services, collaborating with authorities and regulators in both retail and wholesale digital payments.”

“With this same vision,” Vicens added, “we are driving a project that has gained strong support from leading banking institutions and has high potential to attract further backing from other financial and technological players. We believe this initiative can mark an important step in building a robust and reliable European digital payments ecosystem that reinforces Europe’s strategic autonomy in the payments space.”

The stablecoin will be regulated under the EU’s MiCA regulation and is expected to be issued in the second half of 2026. The stablecoin consortium, with the aforementioned banks as founding members, has established a new company in the Netherlands, which will apply for an electronic money institution license and be supervised by the Dutch central bank.

The consortium is open to the addition of more banks, and the appointment of a CEO is expected in the near future, pending regulatory approval. The initiative aims to provide a European alternative in a stablecoin market currently dominated by USD-denominated options, contributing to Europe’s strategic autonomy in payments. Participating banks will be able to offer value-added services such as stablecoin wallets and custody.

The announcement of a strategic alliance between Nvidia and OpenAI marks a new milestone in the race for leadership in artificial intelligence. Nvidia has committed to investing up to $100 billion to finance the deployment of at least 10 GW of capacity based on its GPUs, using the new Vera Rubin architecture, which will replace Grace Blackwell as the technological spearhead. The first phase will enter operation in the second half of 2026.

This collaboration adds to other significant initiatives by both companies: OpenAI has already worked with Microsoft, Oracle, and the Stargate consortium, while Nvidia has intensified its strategic alliances, including investments in Intel and agreements with players in France and Saudi Arabia.

From a financial standpoint, although the contract details are still unknown, the construction of a 1 GW data center implies GPU investments in the tens of billions of dollars, which could be reflected in Nvidia’s results in the coming years.

Preference for GPUs and Signals in Market Sentiment

This agreement, together with the previous deal between OpenAI and Broadcom, reinforces the perception that GPUs continue to be preferred over ASICs for inference tasks, even once models are trained. However, Monday’s stock market reaction—a moderate drop in Nvidia shares—reveals that investors are beginning to interpret this news as subtle warnings.

Behind this skepticism lies the business structure: Nvidia has been investing in cloud-based startups that rely on its GPUs. This “circular relationship,” where the provider funds its own customers, now shows a scale that unsettles some analysts.

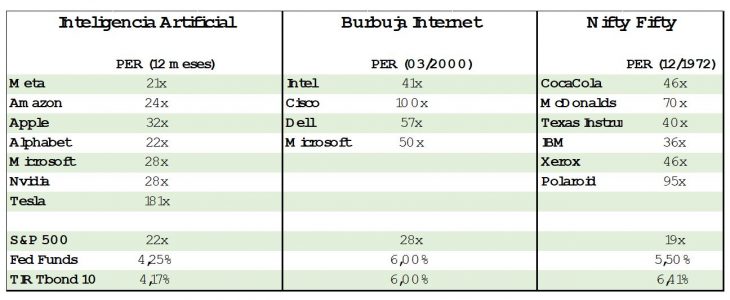

Valuations and Systemic Risks: Is History Repeating Itself?

Although current valuations of big tech companies have not yet reached the levels of the dot-com bubble or the Nifty Fifty of the ’70s, they remain demanding. The recent rally in fixed income has allowed investors to maintain long positions in these companies without discomfort, as it has not negatively affected multiples. But the environment warrants attention.

One of the key risk areas lies in the review of tariffs enacted under IEEPA (International Emergency Economic Powers Act). According to The Washington Post, institutional investors are buying rights to legal claims for the payment of these tariffs at $0.20 per dollar. This anticipates a move: if the Supreme Court rules that the charges were illegal, the Treasury could be forced to reimburse up to $130 billion.

Impact of IEEPA: Two Paths to Instability

If the Court overturns the tariffs enacted under IEEPA, the impact on the markets could come through two channels:

Volatility and Regulatory Uncertainty

The removal of the current framework would open a period of uncertainty. Although most of the affected countries have already accepted the new tariffs—which rose from 2.5% in 2023 to nearly 19%, according to the Yale Budget Lab—the Trump administration would resort to other mechanisms such as Section 232. In fact, it has already announced tariffs of 25% on heavy trucks and 30% on upholstered furniture. Restrictions on semiconductors manufactured outside the United States are also under consideration, which would force companies to double their domestic capacity.

Significant Fiscal Loss

The Treasury would lose about $500 million in daily revenue—funds that markets already factor in as partial offsets to the fiscal deficit generated by the OBBA plan. The immediate effect would be a rise in long-term bond yields, which would compress equity valuations in the short term.

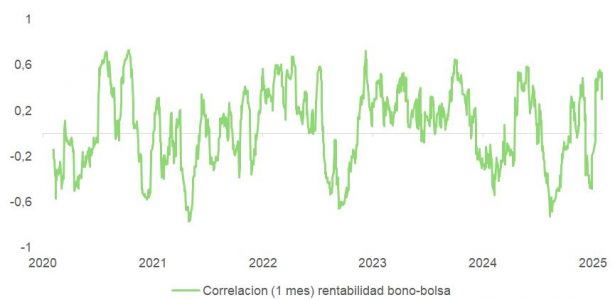

Yields, Correlations, and Sensitivities

In this context, the correlation between fixed income and equities is at peak levels. This means that any upward movement in interest rates has greater potential to negatively impact stock prices, especially in an environment of elevated multiples.

The market continues to price in an accommodative Fed: the yield curve projects a terminal rate below 3% by December 2026. This has limited the downside in the 10-year bond yield, currently anchored around 4%.

The key to rate direction lies in labor data. Differences within the FOMC over whether to implement one or two additional cuts before year-end will be resolved—if inflation expectations remain stable—based on employment trends.

Labor Outlook: Mixed Data, Mixed Reactions

The decline in immigration and the slow normalization of the labor market after the pandemic complicate projections. This structural disruption makes it difficult to apply historical models reliably.

The market is particularly sensitive to any data that could disrupt the current balance. Statistics such as those released this Thursday will be key, as they could trigger volatility in the short end of the curve and define its steepening.

A deterioration in the labor market, if interpreted by the Fed as structural rather than cyclical, could prompt more aggressive cuts in the short term. This scenario would benefit tech stocks, which have historically thrived in environments with negative real rates and moderate but sustained growth expectations.

HSBC has announced the appointment of Víctor Matarranz as Head of International Wealth and Premier Banking (IWPB) for the Americas and Europe, effective October 1, 2025. Matarranz will relocate to London from Madrid and will join the Global Operating Committee of IWPB. The bank has been reorganizing this division, in which Barry O’Byrne was appointed CEO last October, with the aim of strengthening what has become its main profit engine.

Matarranz, who until last year led the Wealth Management and Insurance unit at Santander, will oversee the group’s wealth banking strategy outside Asia. According to the bank’s statement, he will be responsible for expanding HSBC’s wealth management businesses in these regions — including the United States, Mexico, the Channel Islands, and the Isle of Man — and for opening new opportunities in key global corridors. “Víctor’s extensive experience in leading wealth management businesses in these regions will help us refine our focus on serving high-net-worth and UHNWI clients, both in local markets and across global corridors,” said O’Byrne in a statement.

“I’m truly delighted to be joining HSBC as Head of International Wealth & Premier Banking for the Americas and Europe. I look forward to working with Barry O’Byrne and the HSBC International Wealth and Premier Banking leadership team as we leverage HSBC’s unique global strengths and advance our ambition to become the world’s leading international wealth manager. Our focus on connecting clients across global corridors — from the affluent to UHNWI — particularly in the U.S., Mexico, and Europe, is a strategic opportunity I’m excited to help drive,” Matarranz posted on his LinkedIn profile.

For his part, Barry O’Byrne, CEO, International Wealth and Premier Banking at HSBC, stated: “Our connectivity with the Americas and Europe plays an important role in achieving our goal of becoming the world’s leading international wealth manager. We’re thrilled to welcome Víctor, whose broad experience in leading wealth businesses in these regions will help us sharpen our focus on serving affluent and ultra-high-net-worth clients, both domestically and across global corridors.”

Víctor Matarranz joins HSBC from Banco Santander, where he held senior executive roles in Madrid and London over a 13-year period, most recently as Global Head of Wealth Management and Insurance. During his time at Santander, he managed private banking, insurance, and asset management businesses — primarily in the Americas and Europe — and led key strategic projects and M&A initiatives as Group Head of Strategy. He was also a partner at McKinsey & Company, where he spent over a decade advising banks across the Americas and Europe on distribution, digitalization, and new business development.

Photo courtesyDaniel Popovich, portfolio manager in the Investment Solutions division at Franklin Templeton

Foundations and public pension regimes have been moving in search of a sophisticated multi-asset allocation, according to Franklin Templeton. In Brazil, the “Building Blocks” product, developed by the firm’s Investment Solutions division, has seen demand, according to Daniel Popovich, portfolio manager in the Investment Solutions area. “Today, the debate is how to invest offshore, no longer whether I should invest. We discuss need, functionality, and benefit: should there be more or less equity exposure? If the interest is solely fixed income, we sometimes challenge that: wouldn’t it make sense to complement it with equities or alternatives to improve the risk/return ratio?” the executive said in an interview with Funds Society.

He explains that, in response to those questions, the solution presented by Franklin Templeton was the development of a sophisticated product that allows allocators easy access to a personalized, multi-asset approach. These are the building blocks. “The idea is to allow the investor to make an international allocation tailored to their risk and return needs, by combining three funds,” he says. In this case, the funds (or “blocks”) are FIFs (funds of funds), each accessing a category of investments: global equities, global fixed income, and international liquid alternatives (equivalent to liquid hedge funds). All of them carry currency exposure.

According to the portfolio manager, the customization occurs through the combination of the three blocks: the fund for each block is the same for everyone, and the investor chooses the weights according to their profile and objectives (e.g., 40/30/30). As Popovich summarizes: “The client can choose the percentage they want to allocate to each of the three funds, and the fund is the same for everyone.” For those who wish to consolidate everything into a single line, the asset manager can structure a “wrapper” FIC that allocates across the three building blocks. Typical liquidity is up to 10 calendar days for redemptions (which may be longer for strategies like credit).

“For example: in the traditional 60-40 portfolio (60% equities, 40% fixed income), it’s possible to allocate 60% to the equity building block and 40% to the fixed income block and immediately access a broad, well-diversified portfolio across regions, styles, asset classes, and managers — all efficiently packaged and aligned with major regulations,” explains the manager, also discussing the cost reduction for allocators.

“This structure reduces the aggregate cost because it combines active funds — where we access cheaper share classes thanks to volume and negotiation power — and ETFs, which are more efficient in terms of fees. The local management fee was designed so that, in aggregate, we are competitive with the market’s feeder funds,” he notes. “We’re bringing the kind of work that was previously done only in a tailored way for large pension funds, now to several smaller foundations and RPPS, with a very similar offering.”

Goal of 500 Million Reais in the Medium Term

Launched last year, the product currently has about 100 million reais ($18.8 million) in assets, with roughly 70% coming from EFPCs and 28% from RPPS (Regime Próprio de Previdência Social). “The goal is to increase that to 500 million reais ($94.3 million) within the next 6 to 9 months,” says Popovich.

To unlock larger volumes, the manager cites “a closing in Brazil’s interest rate curves” as the main trigger. Although the focus is institutional, a small portion of retail investors is also entering the funds, which are currently distributed on the Mirae platform.

Janus Henderson Group and Victory Park Capital Advisors (VPC), a firm specializing in private credit and majority-owned by Janus Henderson, have announced that CNO Financial Group, a U.S. life and health insurer and financial services provider, will acquire a minority stake in VPC. In addition, CNO will provide a minimum of $600 million in capital commitments to new and existing VPC investment strategies.

Founded in 2007 and headquartered in Chicago, VPC has a track record of nearly two decades providing tailored private credit solutions to both established and emerging companies. The firm was acquired by Janus Henderson in 2024, expanding Janus Henderson’s institutional and private credit capabilities. VPC has specialized in asset-backed private lending since 2010, in consumer credit, small business financing, real estate, litigation finance, and physical assets. Its set of investment capabilities also includes sourcing and managing customized investments for insurance companies. Since its inception, VPC has invested over $11 billion across more than 235 investments.

Headquartered in Carmel, Indiana, CNO offers life and health insurance, annuities, financial services, and workplace benefit solutions through its family of brands, including Bankers Life, Colonial Penn, Optavise, and Washington National. CNO manages 3.2 million policies and $37.3 billion in total assets to help protect its clients’ health, income, and retirement needs.

Transaction Commentary

“We are very pleased to welcome CNO as a strategic partner in our investment in VPC. This collaboration reinforces our shared belief in the long-term potential of asset-backed private credit markets and further deepens Janus Henderson and VPC’s insurance presence. By partnering with like-minded institutions, we continue to enhance our ability to deliver client-led solutions aligned with our strategy to amplify our strengths,” said Ali Dibadj, CEO of Janus Henderson.

“We are excited to partner with CNO to further accelerate VPC’s growth and expand and scale our investment capabilities for the benefit of our clients. CNO’s investment demonstrates VPC’s strong track record of delivering private credit solutions across sectors, our differentiated expertise, and our highly developed sourcing channels, as well as the significant value we bring to our investors and portfolio companies,” said Richard Levy, CEO and founder of Victory Park Capital.

Gary C. Bhojwani, CEO of CNO Financial Group, added: “Our investment alongside Janus Henderson in VPC underscores CNO’s strategic focus on partnering with firms that complement our investment capabilities. This partnership enables us to benefit from VPC’s unique and differentiated expertise in asset-backed credit, both as an investor and a strategic partner, while supporting our ROE objectives. We look forward to working with their highly experienced and respected management teams.”

According to the asset manager, this transaction adds to Janus Henderson’s recent momentum in the insurance space with the previously announced multifaceted strategic partnership with Guardian. Upon completion of this transaction, Janus Henderson Group will remain the majority owner of VPC.

The challenge of water and sanitation has been one of the United Nations Sustainable Development Goals since 2016. And within this niche, there are investment opportunities—also through ETFs. Water is a vital element, not only for sustaining life, but also for the development of new technologies and industries. In First Trust’s opinion, water infrastructure represents “an attractive investment opportunity,” driven by new catalysts and emerging trends such as water-intensive manufacturing, the shift to liquid cooling for AI data centers, and hydraulic fracturing in the energy sector.

The firm explains that the reindustrialization of the U.S. economy will lead to a drastic increase in water demand in the coming years, especially in sectors that are major water consumers, such as semiconductor manufacturing. As these and other projects expand, First Trust forecasts that “substantial investments” will be needed in water infrastructure.

In addition, advances in generative AI have captured global attention. To meet the growing performance demands of AI, global data center capacity is expected to grow by 52% between 2024 and 2027. In this context, keeping high-performance processors cool presents a significant challenge for traditional air-cooling systems, which has led the sector to adopt liquid cooling. Here, the firm cites JLL estimates, indicating that hybrid cooling—70% liquid and 30% air—“has become the standard thermal management strategy for new data centers.”

Hydraulic fracturing (“fracking”) also continues to be a key driver of demand for water infrastructure, according to First Trust. Fracking involves injecting high-pressure water, sand, and chemicals into underground rock formations to extract oil and gas. A single fractured well can consume between 1.5 and 16 million gallons of water.

Moreover, fracking produces “flowback water,” a toxic byproduct that requires treatment using technologies such as microfiltration and reverse osmosis. “From sourcing water to its treatment, transport, and control, fracking processes—which consume vast amounts of water—generate considerable demand for water resources,” the firm notes.

In light of these emerging trends, investing in U.S. water infrastructure becomes increasingly important. The 2025 report by the American Society of Civil Engineers (ASCE) on the state of U.S. infrastructure gave poor marks to water systems, including a low pass for drinking water, a solid pass for wastewater, and a failing grade for stormwater systems.

This reflects decades of underinvestment, as data from the Congressional Budget Office shows that spending on water infrastructure has grown only 0.3% over the past 20 years. The ASCE estimates that $1.65 trillion will be needed between 2024 and 2033 for drinking water, wastewater, and stormwater infrastructure. With only $655 billion funded, “the remaining $1 trillion funding gap is the largest of any infrastructure sector.”

Investors can benefit from these macro trends by including ETFs that focus on water-related industries in their portfolios. One such option is the First Trust Water ETF, listed on the NYSE. It tracks the ISE Clean Edge Water Index, composed of 36 stocks focused on the drinking water and wastewater sectors, including water distribution, infrastructure development, purification and filtration, as well as related services like consulting, construction, and metering.

Another option is BlackRock’s iShares Global Water UCITS ETF U.S. Dollar (Distributing), which tracks the S&P Global Water Index. This year, its valuation has increased by just over 15%, through investments in companies involved in the global water sector, across both developed and emerging markets. As a complement, Amundi offers the Amundi MSCI Water UCITS ETF Dist, which aims to replicate the performance of the MSCI ACWI IMI Water Filtered Index.

A further option is the Invesco Water Resources ETF, based on the Nasdaq OMX Global Water Index, which seeks to replicate the performance of companies listed on global exchanges that produce products designed to conserve and purify water for homes, businesses, and industries. This ETF is listed on the Nasdaq.

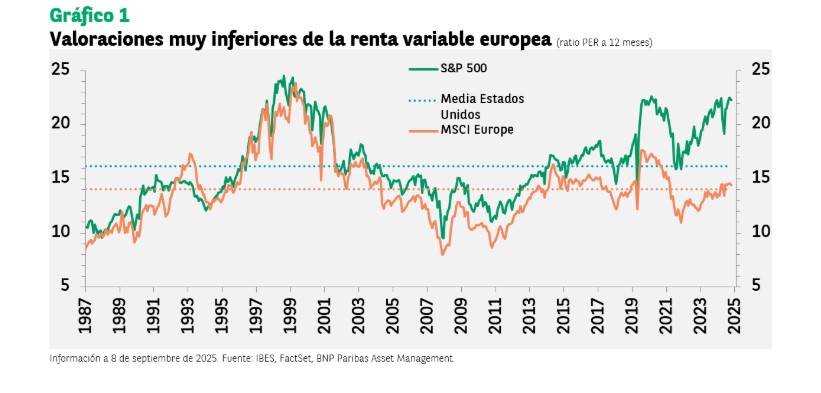

After ten years of U.S. equity dominance, asset managers emphasize that this year’s resurgence in European equities remains intact. In their view, the factors that make it attractive are still valid: more reasonable valuations, a favorable monetary policy from the European Central Bank (ECB), and unprecedented fiscal stimulus measures.

According to Aneeka Gupta, Director of Macroeconomic Research at WisdomTree, we’ve seen a paradoxical first half of the year. In her analysis, 2025 was the year in which U.S. stock markets underperformed their international rivals by the widest margin since 1993. “Suddenly, it became fashionable to talk about how the era of American exceptionalism was coming to an end, as uncertainty rose around Trump’s tariff policies, along with the growing fiscal deficit, a weakening U.S. dollar, and the unveiling of DeepSeek,” she notes.

As a result, Europe emerged as the region making a major comeback in 2025. “Eight of the most profitable stock markets in the world were European, thanks to lower energy costs and the loosening of fiscal rules in Germany. The U.S. had outperformed Europe over the past five years by nearly 23.5% (measured in dollars), due to stronger earnings growth,” Gupta points out.

With this context in mind, the WisdomTree expert believes that equity risk premiums now show a wide gap: “Approximately 2% in the United States, 6% in Europe, and 7% in Japan and the broader emerging markets universe. Over the next twelve months, asset allocation decisions will depend on these valuation cushions, policy divergences, and the evolution of trade alliances.”

Don’t Overlook Europe

“In our view, attractive valuations make a strong case for European equities: they are currently trading at a substantial discount compared to the U.S. market. The twelve-month forward price-to-earnings ratio of the MSCI Europe index is currently at 14.6, slightly above its average since 1980, which is 14. By contrast, in the United States, valuations are approaching historic highs, with an expected earnings ratio of 22 times. In addition, the average dividend yield in Europe is approaching 3.3%, which far exceeds the U.S. average of around 1.3%,” argues BNP Paribas AM.

Despite Europe’s greater prominence this year, Hywel Franklin, Head of European Equities at Mirabaud Asset Management, believes it remains “a forgotten opportunity” on a structural level. According to his analysis, for much of the past decade, investors have overlooked this market, distracted by the extraordinary momentum of high-growth U.S. stocks. “Today, the difference between the two is quite striking. A single large-cap U.S. company now carries more weight in global indices than the entire stock market of any individual European country. That imbalance in attention is precisely what makes Europe so interesting,” Franklin comments.

Even after its strong performance so far this year, the Mirabaud AM executive considers that valuations remain attractive, both in absolute terms and relative to the U.S., reflecting the extreme levels of skepticism that have already been priced into European equities. “And here’s the key point: in the small and mid-cap (SMID) market, one in three companies is still trading more than 60% below its historical high. That’s not a market that’s ‘gone too far’; it’s a market with enormous recovery potential,” he argues.

Not Ignoring the U.S.

That said, the S&P 500 index continues to reach new all-time highs almost daily, despite the macroeconomic slowdown. “The U.S. equity market is experiencing a strong upswing, driven primarily by its tech giants and supported by solid fundamentals, an upcoming easing cycle, and a resilient global economic outlook,” notes Yves Bonzon, CIO of Julius Baer.

In his view, the fundamentals of U.S. companies also showed a strong earnings season and, on the other hand, the AI boom is gaining momentum, with both startups and established giants making bold bets on the growth and reach of this revolutionary technology.

“In addition to earnings optimism, U.S. companies continue to be models in capital return to shareholders. Share buyback authorizations in the United States reached one trillion dollars by the end of August 2025, compared to less than 900 billion dollars at the same time last year,” Bonzon comments.

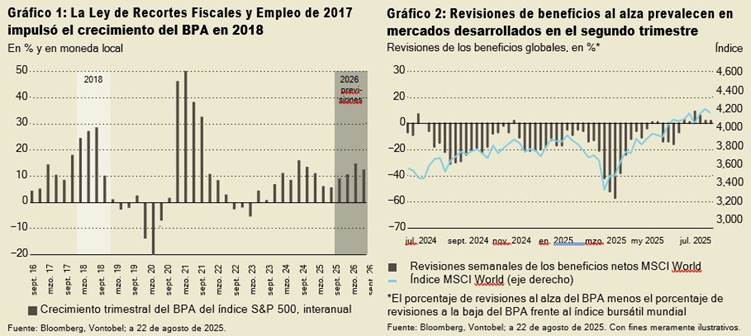

Equities: Unstoppable?

What is clear for asset managers is that equities continued to climb the “wall of worry” during what is usually a quiet summer period in the Northern Hemisphere, with most regional indices hitting all-time highs in local currencies. As explained by Mario Montagnani, Senior Investment Strategist at Vontobel, the bullish sentiment is based on a strong second-quarter earnings season, optimistic forecasts, relief from tariff uncertainty, rate cuts, anticipated leadership changes at the Fed, and expected 2026 stimulus measures that could boost earnings per share (EPS) as in 2018.

“The earnings season delivered solid surprises with minimal tariff effects, marking a turning point in momentum and suggesting that previous revisions may have been too pessimistic. Looking ahead, earnings surprises are likely to play a key role in stock performance, given high valuations,” adds Montagnani.

However, the Vontobel strategist acknowledges that inflation remains the main driver of equity market developments. “Billions in tariffs now impact the U.S. economy each month, but who really bears the cost? The pass-through to consumer prices is more nuanced than many assume. Tariffs do not automatically get passed on to consumers. Their impact depends on factors such as a company’s competitive position, demand elasticity, distribution model, time lags, and supply chain structure,” he notes.

In his view, this is evident in “the U.S. Producer Price Index (PPI28) data, where importers often absorb the initial impact through margin pressure, and the historical correlation between the PPI and the U.S. Consumer Price Index (CPI29) has been weak, suggesting that producer prices are not a reliable predictor of consumer inflation.”

Women are about to inherit a considerable share of the $124 trillion that makes up the so-called “great wealth transfer.” However, according to Capital Group in its latest report, many of them show reluctance to invest their inheritance. On average, women invest 26.4% of their inheritance compared to 36.2% of men.

The report reveals that four out of ten women wish they had allocated more to investment, versus three out of ten men. In addition, women save more—14.3% compared to 11.1% for men—and also spend a larger portion of what they receive, 15.4% compared to 11.3%. Another notable finding is the difference in the type of financial advice they seek. According to the report, 27% of women look for guidance on social media or from finfluencers, double the rate of men at 15%. Likewise, 68% of women trust that artificial intelligence and other technologies will improve financial advice through greater personalization and easier access, compared to 59% of men.

“In the next two decades, $124 trillion will change hands, and women will inherit a significant share of this wealth. Now is the time for them to take control of their financial future. Our study shows that although many save more and invest less, some later regret not having invested a larger portion of their inheritance. The good news is that it’s never too late to start,” said Alexandra Haggard, Head of Asset Class Services for Europe and Asia-Pacific at Capital Group.

Other Findings

The results also show that although women will play a central role in the redistribution of global wealth, barriers still persist in their relationship with investing. For Capital Group, this scenario presents a double perspective: a challenge for the financial sector and an opportunity for more women to take an active role in managing their wealth.

In Haggard’s view, many women turn to social media and financial influencers for financial guidance, but as their financial needs grow more complex, the role of professional advice becomes more important. “As the process of the ‘great wealth transfer’ moves forward, the wealth management sector must adapt to women’s growing influence over wealth. At Capital Group, we have partnered with wealth managers to provide thought leadership in investing, events, and training to help their female clients invest with confidence and build long-term wealth,” she explained.

This research is based on a survey of 600 high-net-worth individuals in Europe, Asia-Pacific, and the United States.