CC-BY-SA-2.0, FlickrPhoto: Swaminathan. Pioneer Investments: “Global Conditions are More Favorable to Emerging Markets"

The emerging market’s outlook has improved slightly since the beginning of the year. Global conditions seem somewhat more favorable: the dollar has moved within a very narrow range and analysts at Pioneer Investments believe that the danger of a strong appreciation of the dollar has been avoided.

In addition, US interest rates have stabilized and it seems that the Fed will carry out the process of monetary normalization with extreme caution. Prospects for commodities are positive and the firm’s coincident indicator for China remains relatively strong, suggesting that the growth dynamic is widespread.

“Equity valuations in emerging markets are not particularly attractive overall but we like India and, in China, the sectors representing the new economy versus the old China. From a medium-term perspective, the uncertainty of Trump’s policies could force or encourage China to accelerate the transition to a domestic demand based economy.”

Also India

As for India, Pioneer Investments estimates that it still represents an investment opportunity backed by mostly endogenous factors, “although it has suffered from the credit crunch, the economy has weathered well and domestic consumption has already shown signs of recovery in the first Quarter of the year,” they explain.

Inflation is bottoming out and at Pioneer investments they expect that in 2017 it will stay at the target level of the Indian central bank (RBI). Although valuations are expensive, they are supported by returns (in particular by ROE) and the estimated earnings per share growth for the next 12 months has been revised upwards to 7%. The results season has been positive to date.

“The currency is undervalued in the medium to long term, which contributes to competitiveness. The perception of value should be adjusted, since we hope that the structural reforms will cause a revaluation of Indian stocks. Emerging market currencies also offer opportunities for arbitrage: we prefer the currencies of commodity-exporting countries with high carry versus those of manufacturing countries, both for structural reasons and for the positive carry,” they conclude.

CC-BY-SA-2.0, FlickrWei Li, Head of Investment Strategies for the EMEA Region at iShares (BlackRock). / Courtesy Photo. Blackrock: “Reflation will be Global and, Historically, Stocks Have Performed Better in this Environment”

The year began with expectations that have continued to evolve until turning around completely. Investors were enthusiastic about American equities, waiting for Trump to implement some of his electoral promises, such as tax reform and infrastructure investment, while they regarded Europe with suspicion due to its political instability and upcoming elections. “In the first few months of the year, the opposite has happened,” says Wei Li, Head of Investment Strategies at iShares (BlackRock) for the EMEA region.

In fact, the appetite for the European stock market versus the American stock market has been noticed in the flows. In this context, the firm’s investment preference goes includes equities, with European and Japanese markets as favorites, as well as emerging markets. “Our expectation of higher yields emphasizes our overall preference of stocks over bonds. Historically, stocks have performed better in reflation environments because, in our view, they are geared towards global growth and offer profit while maintaining diversification,” she says.

The firm believes that global yields will increase further, but they will find certain restraints, as for example the effect of the monetary policies. “That’s why we believe that investors need to go beyond traditional equity and bond exposures to diversify portfolios in this environment, and include allocations based on alternative factors and assets,” adds Li.

In addition, the expert believes that, in this environment, trade is the key factor, and that there is a lot of headroom to invest in assets linked to it. Li argues that the best option is to use diversification as a strategy, as well as focus on company fundamentals, “particularly in those regions that can benefit most from trade, such as Japan, Europe, and emerging countries,” she adds. She also believes it’s logical to return to value strategies in view of the expected rise in interest rates by central banks: “We expect to start seeing more value and for the momentum factor to have more weight in the strategies” she says.

Global Reflation

The firm points out that we are at a turning point in global economic growth, about which Li explains that “it is an extraordinarily long and slow cycle;” which means that there is no rapid acceleration of the economic recovery, but rather that it is constant, and which, according to Li, is seen, for example, in the very parallel behavior of currencies such as the Dollar and the Euro.

In general, there have been two main trends in these first months, the consequences of which can still be seen. On the one hand, the “extraordinarily low volatility,” she says, partly because of the role central banks have played; and, on the other, the reflation. “Reflation will be global. We see signs indicating this, such as a rebound in inflation expectations and an improvement in economic activity and business estimates indicators,” she says. And that inflation mentioned by Li is another of the dynamics that is already a reality and which will continue over the next few months. According to Li, “this increase will come mainly from energy, and will be reflected in the costs, of for example, transport.

First Quarter

According to BlackRock’s vision of the first quarter of the year, there has been a strong movement of investment flows that have shifted from American to European equities. “The reason for this was disillusionment with Trump’s policies, which have difficulties in getting through Congress, and good business results in Europe, where the recovery continues slowly but steadily,” Li says.

For Li, following Macron’s victory in the French elections, sentiment on Europe changed radically, which has been fundamental for investment in the Old Continent. “We no longer see such danger in European politics and populism is perceived to be waning. This optimism is reinforced by the countries’ macro indicators, which show how recovery is general and not just being pulled along by one or two countries,” she argues.

Another important aspect of these first three months has been the positive behavior of emerging markets. “We see that, in general, they have stabilized and are creating investment opportunities. Including China, where the fiscal stimulus announced last year has been very effective,” Li summarizes.

CC-BY-SA-2.0, FlickrThe event was held at the Ritz-Carlton Coconut Grove in Miami on May 18th and 19th.

. Emerging and Asian Equities, Floating Rate High Yield Bonds, and Multi-Assets: These are the Bets of the Participating Asset Managers on Day 1 of the Miami Fund Selector Summit

In a scenario marked by numerous macroeconomic and geopolitical challenges, in which it will be very difficult to obtain the same returns as in the past, five asset managers offer their ideas for achieving attractive returns. In equities, Henderson Global Investors sees opportunities in China, while Asian consumer history is the guideline for equity investment in one of Matthews Asia’s best-known strategies; and the value style, the key for obtaining attractive emerging market returns according to Brandes Investment Partners. In a segment as complicated as fixed income is today, M&G Investments sees opportunities in high yield and in floating rate high yield bonds. Beyond a single asset, Aberdeen Asset Management is committed to a multi-asset and diversified approach that invests in truly innovative market segments.

These strategies were presented during the first day of the third edition of the Fund Selector Summit 2017, a meeting aimed at the main selectors and investors in USA Offshore funds and a joint venture between Open Door Media and Funds Society, held in Miami over those two days.

Multi-assets: a strategy based on diversification

Simon Fox, Senior Investment Specialist at Aberdeen Asset Management, explained why it is important to take an innovative and different stance when investing in multi-assets: instead of using market timing strategies, something very difficult to do, or those based on the use of derivatives, which are complex and dependent on the asset managers’ abilities and the bets taken, he supports the preference for a more active strategy focused on the diversification and search of opportunities in new market segments. For the expert, diversification needs to be improved because traditional portfolios based solely on fixed and variable income, which have worked very well over the last few decades, when fixed income not only played a defensive role, but also provided a large source of returns, will not offer the same returns from now on: “The future will be marked by lower global growth and lower yields and that means that traditional assets will offer lower returns than they have in the past”: thus, in an environment of more adjusted prices in equities and credit, a study by McKinsey Global Institute points to a fall in returns over the next 20 years of 250 basis points in US stocks (compared to the average for the period 1985-2014) and 400 in fixed income.

And all that without taking into account risks and concerns, such as China or Brexit, in addition to others: “The biggest risk for a multi-asset portfolio is not the short, but the long term, because there are factors that have supported global growth in the past that will not be repeated, or which may even become obstacles,” explains the specialist, pointing to examples of demography, adjustment in China, or de-globalization.

Given this scenario, the need to diversify arises, with clear advantages: “It is what many investors have been doing over the years, adding more assets to the portfolios, not only to find more sources of growth, but also to reduce volatility.” And, as a bonus, the traditional obstacles to diversification (such as transparency, illiquidity, regulation, commissions…) are dissipating, so that “currently, it is possible to diversify better thanks to the size and the globality gained by asset managers and by the greater exposure and access to different assets”. As examples in this regard, Fox points out bonds in India (which can offer annual returns above 7%, and is a market that benefits from the improvement in fundamentals – in fact, the asset manager has a fund focused on this asset- ), or access to equities through a smart beta perspective (focusing on low volatility or on obtaining income). The alternative spectrum also opens new opportunities, such as aircraft leasing (which can offer returns close to 10%), or insurance-linked securities.

In short, “there are now many more opportunities than in the past,” leading Aberdeen AM to speak about multi-multi-assets rather than of multi-assets, as the best way to deliver long-term profitability, according to Fox. In this regard, the asset manager has two strategies, one focused on obtaining income and another on growth, both with similar positions and a low turnover due to its focus on fundamentals and long-term vision (five to ten years).

Opportunities in Asian Equities

In this environment, equities also continue to be an attractive option for portfolios. And Asia is a region worth considering. For Rahul Gupta, Manager at Matthews Asia, “Asia is the past, present, and also the future,” he says, explaining the meaning of investing in the continent for the asset manager. Citing Vietnam as an example, he speaks about its social evolution from an economy based on agriculture to one of consumption and industrialization… a trend which he uses to his fund’s advantage.

“Asian middle class will be a very important economic force in the world and what they buy and that on which they spend, will be increasingly important for business and investment,” adds the asset manager. In his opinion, the major catalyst for growth and rising incomes – and therefore for consumption – will be productivity improvements in Asia. As an example, wages are growing faster on the continent than in most of the rest of the world.

Not surprisingly, the main anchor for the Matthews Pacific Tiger fund – managed by Gupta – is domestic demand; the second guide, the search for businesses that grow sustainably, over a cycle, even if the figures are lower. “The growth is there, you do not have to look for it, but you do have to look for those businesses,” he says. As evidence of the importance of sustainability in the search for growth, the asset manager explains that, for some industries in China, a lower growth environment is more favorable because it helps to achieve “more rational” capital development and returns for the “healthier” investors.

The fund has two important biases: first, it is underweight in more cyclical sectors, such as materials or energy, which do not offer such sustainability in growth; secondly, it is mainly positioned in companies from emerging Asian countries, which offer more growth than the more developed ones. A third feature of the fund is that it has more allocation to businesses with a median capitalization than its comparables: “Historically, in these firms we find more opportunities or sustainable growth, and less linear, and that leads to the creation of greater alpha.”

The asset manager also explains the importance of active management in Asia, given the rapid pace of the movement that is taking place in the continent, and aiming at choosing the good names – looking for opportunities in sectors where the indices have less weight but which rapidly gain positions at breakneck speed in the economies – but also to avoid “horror stories”. The objective of the fund is to capture the same return as the Asian stock market but with less volatility, thanks to its focus on companies with good balance sheets, good management and attractive valuations.

What About China?

Within Asia, you cannot forget the story of China, in which Charlie Awdry, Manager of Henderson Global Investors, sees opportunities. The expert points out the improved macroeconomic scenario, marked by a growth-reform, and deleveraging triangle, as well as a boost in consumerism, a benign impact of Trump’s presidency and a stronger renminbi this year. “Concern over the fall of the currency during the last few years was evident, but the downward movement has already stopped,” he points out.

But the Henderson Horizon China Fund seeks to capture opportunities at the micro-economic level, rather than at the macro-level: hence the asset manager, rather than focusing on the country’s growth, analyzes the PMI data to conclude that Chinese companies are reinvesting… and growing with greater force. And not just private ones: the environment of major reforms following the 19th Communist Party Congress will allow some state controlled firms (SOEs) to make better capital allocations and raise their dividends. That is the reason why the asset management company, while still relying mainly on the Henderson Horizon China Fund for private companies, also holds important positions in this type of companies (34% of the fund). In general, and in an environment of rate increases due to economic but also to regulatory reasons, the asset manager sees a greater differentiation between companies, as the supply of cheap money moderates… something that offers opportunities to active managers.

For the expert, the most robust part of the Chinese economy is always consumption, and he points out the evolution of the sectors of the new China (information technology, healthcare, consumption…) over those of old China. With respect to the differentiation between growth and value, and taking into account that the first has beaten the second and that the gap of valuations has extended, he believes that at some point the value will return to scene and, to play that story, there’s nothing better than to invest in banks. The reasons: the improvement in the quality of its fundamentals, and the benefits which an improvement in the macro and in valuations generates in this sector. Investment from a tactical point of view also makes sense, as banks offer dividends of 5% -6%: “There are not many places where those levels are found,” says the asset manager, who also mentions as a catalyst the momentum of the Hong Kong -Shanghai Connect to invest in A shares.

Awdry, who mentioned the advantages and opportunities when investing in China in Hong Kong, Shanghai, Shenzen, or even in shares of Chinese companies listed in the US. (which offer attractive prices: “You have to sell US companies and buy Chinese”), explains the overweight of sectors such as discretionary consumption or financial firms, in the Henderson Horizon China Fund, versus the underweight in telecommunications or utilities, a long-short fund 130 / 30, with a market exposure of 90% -100% and focused on taking advantage of rises but also protecting against falls. Not forgetting the possibility of making money – and not just protecting capital – with short positions (currently the portfolio has about 40 long and 12 short). And all of this, with a bottom-up perspective and a selection of values.

The Value in the Emerging Markets Opportunity

Without leaving the emerging world, Brandes Investment Partners relies on the idea of investing in these markets from a value perspective. “We believe that with a value-oriented approach, there is a great opportunity in emerging markets,” says John Otis, Institutional Client Portfolio Manager at the asset management company. Among the beliefs that support this vision and commitment to value, he points out that stock markets are not always efficient, that price is key to determining long-term results – which explains their strong bias towards the price factor -, and emphasizes how being contrarian offers opportunities for beating the market and how patience is critical to generate attractive returns. That is why the asset manager, based in San Diego and with 28 billion dollars in assets, is faithful to the value philosophy since its foundation in 1974.

But, why value when investing in emerging markets? Gerardo Zamorano, Director of the entity’s Investment Group, explains that, in general, an investor would have obtained higher returns by positioning in the lowest historical valuation deciles… something that intensifies when investing in emerging markets: “A lot of people buy emerging for growth, but if everyone thinks the same, you end up paying more for it, and, even if the fundamentals are good, you can run the risk of paying too much,” he warns. On the other hand, he explains that sometimes we tend to be too negative with a country because of political and economic aspects… leading to volatility and sharp price falls and this can generate opportunities for his strategy, materialized in the Brandes Emerging Markets Value. The expert indicates his preference for good companies, but with good prices.

And he points out that the fund is 90% different from the index, with a very strong active share, which is explained by several reasons: among them, investment in companies of all capitalizations (which makes them have a large weight in small and mid Caps, unlike the index), the fact that they take advantage of the overreactions to macro or political events (the asset manager points out the investment in Mexico after Trump’s election, or in Brazil currently, after the last corruption scandal), their willingness to invest in situations that others fear for governance or regulatory reasons, or their search in all corners of the emerging universe, even in those with little or no coverage. In addition, the fund includes non-index securities, such as developed-market companies linked to emerging markets (companies listed in Luxembourg but with assets in Latin America, or Austrian banks with their main operations in Eastern Europe, as examples), Hong Kong securities – although the index classifies it as a developed market-, border market companies (such as a mini-conglomerate in Pakistan, or some positions in Argentina or Kuwait…) and securities of countries that are not in the global indices – a bank in Panama, or some firms in Saudi Arabia. All this explains its great differentiation with respect to the index.

Among the positions, Zamorano points out China’s underweight (where he prefers to invest in the consumer sector, but not in banks) and the overweight of Brazil, Russia, Mexico or Chile; by sectors, they’re overweight on cars and components, or discretionary consumption, and they’re underweight in information technologies (because of their high prices in markets such as China, or their dependence on a single product in others such as Taiwan).

As a positive aspect for investing in emerging markets, he also points out that these markets have seen outflows since 2013 and that, global portfolios are underweight in the asset, so he sees “potential for a change of mentality.” That, without taking into account the attractive valuations, improved margins and corporate returns, or the continuity of value investing’s comeback.

Floating Rate High Yield Bonds

In debt, and although opportunities seem to be more limited than in other markets, such as equities or multi-asset portfolios, there is still where to look. James Tomlins, M&G Investments Portfolio Manager, explained his vision for the high yield segment, and also talked about floating rate high yield bonds, where he now sees more opportunities and a more defensive form of exposure to credit risk than the traditional high yield.

Of course, the asset manager warns of valuations: high yield credit spreads are fairly valued, but offer very little potential for capital gains. With respect to defaults, he explains that they are reducing very fast but that, because there are still traces of stress, their positions in both traditional and floating rate high yield strategies are defensive.

In a review of the markets, Tomlins points out that high yield has been volatile in recent years, especially in the US, indicating that the prospects of returns are more attractive precisely in the American giant, as compared to Europe. As for the global market for floating rate high-yield bonds, the movement direction is the same as that of conventional high yield, but the amplitude is smaller, so it is a way to access credit spreads with a lower beta: “If you seek exposure to credit spreads, while at the same time preserving capital, floating rate bonds are more attractive.” Added to this is the fact that upward rate movements have no impact on that market; what’s more, coupons move in line with rates, something to consider in an environment where the Fed is likely to undertake three rate hikes throughout the year.

As for the universe and its portfolio (M&G Global Floating Rate High-Yield), Tomlins explains that the low risk duration and the majority of “senior secured” issues outweigh the risks posed by majority B positions from a rating perspective. In the portfolio, in some cases where they see that the traditional high yield market offers greater spread and potential earnings from the same credit risk, they resort to the strategy of investing in the traditional high-yield bond and covering the duration. In the fund, 23% of positions use this strategy, compared to 43% in physical floating rate or 24% in CDS (because of their better convexity).

Pixabay CC0 Public DomainPhoto: Krysiek. SRI: Also With Passive Management?

Innovation in the field of responsible investment funds is a fact, as these criteria (environmental, social, and good governance) are increasingly applied to more asset classes, whether equities, fixed income, emerging debt, or high yield, as well as to thematic products. This innovation also concerns passive management, and managers such as Candriam, Degroof Petercam AM, BNP Paribas IP, or Deutsche AM, for example, have both, actively managed, and indexed or passive SRI vehicles. Recently, Deutsche Asset Management has created the db x-trackers II ESG EUR Corporate Bond UCITS ETF (DR), a fixed income ETF to offer investors exposure to the corporate bond market, denominated in Euros, of companies that meet certain environmental, social, and corporate governance requirements.

These types of launches reignite the debate on whether it’s feasible to apply SRI management, which requires a large degree of analysis, to passively managed vehicles. The entities with ISR offer of both types believe that it is equally possible, although others characterized by a more active management, such as Mirova (Natixis Global AM’s SRI specialist), or Vontobel, have their doubts.

“Although most of the SRI management is done through active management, there are very interesting SRI ETFs, such as the BNP Paribas Easy Low Carbon Europe ETF, which invests in the 100 European companies with largest capitalization and the lowest carbon footprint,” says Elena Armengot, explaining that BNP Paribas Investment Partners manages 15.3 billion in ETFs, where they exclude any security that is on their exclusion list, and also, ETFs that replicate MSCI indices exclude the arms industry.

“The experience we have with SRI in passive management is proof that it also makes sense, and the issue in this field is the level of SRI quality that we target and the index to replicate,” Candriam says

Petra Pflaum, from Deutsche AM, argues that both active and passive management can be applied to SRI.”Passive products may include the use of indexes constructed from an eligible universe based on SRI characteristics of a company or a country” the expert explains; and says that they will expand the business in passive management in this area, after its recent launch.

UBS ETF is also defensive of SRI in passive management: “In UBS AM’s offer of ETFs, we have the largest range in Europe of fixed income and equity funds with a SRI filter, with a total of 9 funds and 1.2 billion Euros, which replicate MSCI indexes with SRI filter, such as MSCI World, MSCI Emerging Markets, MSCI EMU, MSCI USA, MSCI Pacific, MSCI Japan, and MSCI UK, for the equity indexes, and the MSCI Barclays Euro Area Liquid Corporates and US Liquid Corporates indexes, which are both investment grade fixed income,” explains Pedro Coelho, Head of UBS ETF in Spain.

“We believe that ETFs have their market, and of course any initiative to boost SRI is welcome: if passive management bets on these types of vehicles linked to socially responsible indexes, it will definitely give a definite boost to the integration of extra-financial criteria in Investor portfolios”, argues Xavier Fábregas from Caja Ingenieros Gestión.

However, active management adds value to the extra-financial analysis that can hardly be obtained otherwise, for example, corporate dispute management requires a more global approach, without adhering to an index, or to a certain universe, he adds.

Only Active Management

And there are also those who believe that the SRI philosophy is applied much more efficiently with active management: for Edmond de Rothschild AM, active management is the best way to achieve social and environmental profitability. According to Sonia Fasolo, SRI Manager at La Financière de l’Echiquier, “it is very natural that passive management also develops in the same way, but it must be remembered that a large part of SRI tries to get involved with companies to help them adopt better standards and practices; I have doubts that ETF managers will get involved with the companies, or deal with certain issues during the general assemblies,” she adds.

“We believe in active management, and we are convinced that in order to achieve high returns, investors need to follow an approach that is strongly linked to profitability and that fully integrates ESG issues into fundamental analysis rather than replicate indexes. When replicating indexes, investors are exposed to risks that may be unknown and indexes also tend to apply exclusion criteria that limit the investment universe,” says Ricardo Comín from Vontobel.

At Mirova, Natixis Global AM’s SRI specialist, they warn of the need to assess the risk of ETFs and doubt as to their ability to apply SRI criteria with the same effectiveness as active management.

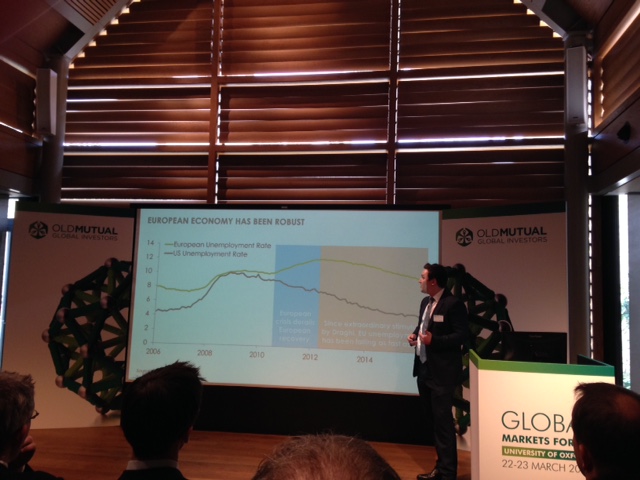

Pixabay CC0 Public DomainPaul Shanta, Head of Fixed Income Absolute-Return at Old Mutual Global Investors, at a recent conference in Oxford.. Old Mutual GI: “Trump Did Not Invent US Inflation; Rather, He Cannot Curb the Expectations”

For just under six months, markets have begun to anticipate with great force the arrival of inflation. One of the most powerful triggers, which caused the Fed to adopt a more aggressive stance and raised alarm bells among investors, was Donald Trump’s arrival to the US presidency; elected in the November elections, he’s been leading the country since last January. However, when referring to the reflationary trend in the market, Paul Shanta, Head of Fixed Income Absolute Return at Old Mutual Global Investors, is very graphic in pointing out that the inflationary trend goes far beyond politics. “Trump did not invent US inflation,” he said firmly in the framework of a recent event held in Oxford by the management company.

“By 2014 we were starting to see a rise in wages and in core services in the country. Inflation was there before Trump,” he recalls. Pressures began with interest rates in negative territory and, it soared as early as last July. So, according to the expert, it would be more appropriate to say that “Trump cannot do anything to curb inflationary expectations,” instead of saying that it is he who generates them.

It is true, however, that the President’s plans are inflationary: the tax cut project, the infrastructure program, and his commercial proposals, will support that increase in prices that occurred prior to his arrival

However, the market is not accounting for higher inflation- it expects only 2% up to 2026 – and that’s where the fund management company sees opportunities:Shanta explains how they position their debt fund with absolute return strategy to benefit from this imbalance, with positions to benefit from a rebound in US inflation. “The interest rate markets are getting ahead of themselves,” he says.

On the situation in Europe, he values Draghi’s work in achieving, like the Fed in the US, the falling unemployment is rate in many countries. And points out that “Inflation is not just the story of the US,” since consumer prices are also rising, and in markets such as Italy, France, Germany, and Spain are already reaching 3%. “Inflationary pressures are starting in Europe, with underlying Euro area inflation rising,” he insists.

However, there are also imbalances between market projections (from 1.3% at the end of 2020, with 67 basis points of ECB rate increases in that period), and reality (the ECB projects 1, 7%), therefore something’s amiss. “It‘s not consistent: expectations of market inflation are too low, while expectations of rate increases are very high.” The fund management company tries to take advantage of these differences.

The Arrival of Turbulence

At the conference, Mark Nash, a multi-sector fixed income manager, warned that in fixed income, “the days of earning easy money are over” and pointed out that after a rally environment in all assets (fixed income doubled its value in six years), there is a time for changes, marked by structural factors, causing him to predict volatility and turbulence.

Among those changes to be considered, populism in the face of problems such as low wages, inequality, or immigration; the demographic changes, with the growth of the aging population and the increase in dependency ratios; the new role of central banks … “Financial assets will be impacted: there are many turbulences ahead.”

Pixabay CC0 Public DomainWilliam Landers, Courtesy photo. BlackRock’s Landers: "Mexico Stock Market Opportunities Could Become More Attractive"

In recent years, Brazil’s investment history cannot be reviewed without seeing a mixed picture, but one thing that William Landers, Head of BlackRock’s Latin American team, is confident of, is that Michel Temer’s arrival in government following Dilma Rousseff’s ‘impeachment’, is going to turn policies around, placing the country on its way to recovery. However, in the short term, much of what happens in emerging markets will depend on the proceedings of the Trump administration.

Landers, who is a portfolio manager of the firm’s range of Latin American equity funds, estimates that a key factor in capital flows this year will have to do with the possibility of the U.S. government launching a corporate tax reform. “A plan of this kind would make U.S. companies more attractive to investors and would draw in the money that is in foreign subsidiaries to put it to work in the United States,” he explains.

Precisely because of the doubts aroused by Trump’s policies, Landers’ team keeps Mexico strongly underweight in the portfolio. “If as an investor you have a vision between 1 and 3 years, then there are many Mexican stocks that make sense. But we’re probably going to have the chance to buy these shares cheaper, so our vision right now is to wait. In Mexico what we are really waiting for is to see a better market entry point.” In fact, BlackRock believes that even Peru or Argentina are more interesting markets in which to be right now.

Brazil Sets the Stage for Improvement

In Latin America, Brazil’s economy provides the other end of the spectrum to Mexico’s ‘stand by’ story. If during the last quarter of 2016, following Trump’s victory, Mexico raised interest rates by 100 basis points to 5.75% to contain peso volatility, Brazil was going in the opposite direction by starting a relaxation cycle with a cut of 50 basis points, placing the interest rate at 13.75%.

“If we look at what we have learned in 2016, especially when it comes to equities, we can say that the market was not looking at what was happening at the time. What I mean, from an economic perspective, is that growth was still negative in several Latin American countries, inflation remained very high in some of them, and then came a series of events that no one believed could possibly happen, such as China’s earlier last year, Brexit, the Fed’s measures, Trump…. but something very important happened in the region, which was Dilma Rousseff’s impeachment in Brazil. This really changed the country’s direction in such a way that we still don’t know what the result will be, but it has put the present Temer government on its way to solve the country’s problems,” he explains.

Landers believes that, in a way, Brazil’s economy is similar to the US economy, in that it depends on its own growth. Although the US market is very open and Brazil’s is not, the BlackRock portfolio manager points out that both countries have exports that are equivalent to only 10% of their GDP. Thus, he says, for Brazil, the rate of inflation is much more important than the growth rate in the United States or China.

“It is true that there are several companies in BOVESPA, the local stock exchange, that depend on global trade. I’m thinking of Vale, or Bradespar, which we recently added to our portfolio. For these companies, it is relevant what happens in China, and whether Donald Trump finally sets an infrastructure spending plan in motion, which would also be positive in the short term for Chile or Peru.”

During the last 10 years, we have seen an unprecedented expansion in Brazil’s middle class, and that they managed to control inflation, drop interest rates significantly, and return job creation to double-digit rates. On that basis, Brazil has just gone through a political moment in which it has had to restore credibility in its institutions. And Landers believes it has managed to do so.

“We are seeing that investors are regaining trust in the country, business owners also feel more confident about the economy. In short, confidence has improved. It is true that consumption still does not reflect this and has not yet recovered, just as employment has not. But you can see that it is headed down that path, and I believe that in the first quarter of this year we will see that things are starting to improve somewhat” he says.

And he adds: “However, even if Brazil does not reach the growth rate we expect, going from a negative growth rate in the last years of -3.5% or -4% to a positive growth rate of 0.5% is a jump that we are not going to see in any other economy in the world, and this is really going to cause the central bank to start cutting interest rates, although it will not do so very aggressively and will not surprise the market with these measures. So this is the story that makes us think that Brazil is going to do well and that’s why 2/3 of our investments are here. Brazil has a lot of room for growth.”

Changes in the Portfolio

During the last quarter of 2016, BlackRock’s BGF Latin American Fund, which selects between 50 and 70 equity securities in Latin America, divested positions in a number of Mexican securities.

In Brazil, the fund maintains a large overweight, favoring companies that stand to benefit from improved governance and from falling interest rates.

Pixabay CC0 Public DomainLeft Tony Glover, right, Naruki Nakamura. "An Investment in Japanese Fixed Income is a Bet on The JPY"

With a current attractive business situation, political, fiscal and monetary support and a healthy inflation, the Japanese debt market offers investment opportunities according to BNP Paribas Investment Partners.

Tony Glover, Tokyo-based head of the investment management department at the company believes that “it really depends on the assumptions that the investor has. An investment in Japanese fixed income (for a European investor) is a bet on the JPY. Investors in our Parvest Bond JPY fund generally do so if they think the JPY will strengthen, as it tends to do in times of market stress (i.e. a ‘risk-off’ play). A strengthening JPY generally puts downward pressure on the equity markets (as earnings forecasts are usually revised down) – so if the investors’ assumption is a strong JPY, then fixed income might be the better investment. But as I said to clients in Madrid last month, we think that the equity markets currently look attractive due to 1) earnings growth, 2) inexpensive valuations, 3) expected corporate governance improvements, 4) increased activity by domestic investors.”

Naruki Nakamura, head of Fixed Income with BNP Paribas Investment Partners Japan, and Fund Manager of the Parvest Bond JPY believes that if you look at flow indicators published by MoF (Japanese Ministry of Finance), foreigners have been heavy buyer of short and intermediate JGBs for months at deep negative yen base yield. “Why they buy? I assume the buyers are USD based investors who are buying with currency swap hedging. Toward the end of November last year (Nov 29), the spread went as far as -0.85%. 2 Year JGB was traded around -0.17%. If the USD based investor buy 2 year JGB with currency swap hedges, USD based yield can be as high as 1.95%, which is much higher than 2 Year Treasury yield of around 1.1% then (Very rough estimation without considering transaction cost). Investors with ample USD and who do not care about illiquidity, such as Sovereign wealth fund or Foreign reserve, might think it attractive. Any way, if you are an institutional investor with currency swap capability, have ample cash and unwilling to invest in deep negative yield short Bunds (or better have 0% return rather than sizable negative rate return), willing to sacrifice liquidity, willing to take Japanese sovereign risk, JGB market might be the candidate to put money in. As of now, basis swap has recovered to some extent and 2-year JGB’s yield is at deeper negative level, however, short Bunds yields are much lower due to ECB/risk off, so relative attractiveness may be bigger.”

Apart from FX hedging base, he agrees on that some European investors use JGB to take JPY FX risk. “In the past, JPY strengthened in the risk-off environment. Although Japanese fiscal situation continues to deteriorates, we think the Japanese crisis is at least 5 years away. So, if an Euro based investor wants to diversify the investment, buying unhedged JGB might make sense, especially if the investor is worried about Europe-oriented risk-off.”

“As of BOJ policy, as you might know, they changed their policy frame work in September 2016. They used to think unlimited quantitative ease could solve the problem, but they no longer think so. Currently they are reluctant to either increase QE nor go deeper into negative yield policy rate. They only want to fix the entire JPY yield curve at current level. Which means, we do not expect JPY to decline excessively from Japanese monetary policy factor for now . (So, for example, if US tightens more than market expectation, JPY may fall versus USD.) If there is another global financial crisis, we expect JPY to initially strengthen sharply. Then, if the JPY’s appreciation is excessive, BOJ may again change their policy to add aggressive monetary ease, which likely to curve the appreciation.” He concludes.

Pixabay CC0 Public DomainPhilippe Berthelot, courtesy photo. "As Rate Volatililty Might Prevail this Year, We’d Have a Propensity to Favour Credit Risk"

With the rates normalization process already underway, Philippe Berthelot, Head of Credit Management Teams (Corporate and structured credits) at Natixis Asset Management talks in an exclusive interview with Funds society about where he sees value and highlights two of their funds: Natixis Euro Short Term Credit y Natixis Short Term Global High Income.

– Is it possible to talk about danger when we talk about the current situation in fixed income? Are the investors in danger when they take in account the arrival of the growth, the inflation, and the following rise in interest rates?

A rising rate environment may not be that supportive indeed for fixed income products in general, as it can lead to some disappointing performances. That said, 2017 is totally different from a 1994 scenario, we just expect 10 year rates to be 30-40bp higher by ear end in the USA and in Europe!

– Which are your previsions of the interest rate hikes in USA this year and how will this affect to the assets? There will be contagion in Europe? Will the ECB need to take solutions soon?

The FED is expected to raise rates 3 times this year (a hike of 25 bp already made yesterday) but really nothing to worry on the ECB side. What would matter the most in Europe would be hints at “tapering:” it is likely to occur next year. For the time being, political risk is a driver of sentiment with Dutch / French and German elections

– Is there danger of capital turnover from fixed income to equity?

It is genuinely true that a rise of nominal rates, at first, is supportive for risky asset classes like equities and even credit. With further growth prospects in Euroland this year Equities should outperform Fixed Income, caeteris paribus.

– In this environment, is it still a good asset to invest or should we sharpen the caution at the time to invest in debt? Is it still possible to find value in credit, for example?

There are so many different animals within what is labelled “fixed-income” ! For instance, the bulk of ABS and senior secured loans are made floating-rate products, as such they’re not very sensitive to a rise of interest rates ! HY spreads are also negatively correlated to rates, which means that sub investment grade bonds should fare quite well this year. Last but not least, focusing on short duration investments is another way of performing almost always positively whatever the state of nature.

– In which sectors of fixed income are we still finding value? And where do we find the biggest risks?

Financials and subordinated financials are very cheap vs corporates (as they are not eligible to the ECB QE). High beta sector like AT1 , Hybrid securities should perform quite well this year.

– Do you prefer credit risk or duration risk? Why? It seems that now the most popular choice is to maintain a low duration… why?

As rate volatililty might prevail this year, we’d have a propensity to favour credit risk : lower in ratings with shorter duration risk

– Natixis Euro Short Term Credit y Natixis Short Term Global High Income are two solutions that are driving. What characteristics have these vehicles and what can they contribute to the portfolios?

Natixis Euro Short Term Credit is a core plus fund : mainly IG plus a HY tilt than can up to 15% of its assets. In order to benefit from a better yield we also have a substantial exposure on subordinated financials. On top of it the fund duration is below 2 years, which is exhibits limited sensitivity to a rate rising environment.

The second fund, Natixis Short Term Global High Income, is also targeting fixed income investments with duration to worst below 2 years within the HY space this time with an average exposure to 50% Europe and 50% US. It features a much higher yield due do its very HY nature.

– Where can we find the best opportunities in credit: Europe or USA? What do you prefer; high yield or investment grade?

The answer is threefold: credit quality is much better in Europe with lower default rates and lower leverage, US fixed income will likely be hurt by a rising rate cycle , but carry is much better off in the USA (assuming no dollar hedge from an Euro investor point of view)

– Do you like the profitability risk profile that the debt and emerging credit present?

We do have very little exposure but hard currency corporate exposure in some specific names. There is a another team to deal with local currency in Emerging credit exposure.

-What returns can be expected on credit and with short durations facing this year?

You may expect the current carry with limited capital gains : 0.8% to 1.0% in Euro IG and ca 3% to 4% for Global HY short duration.

– Does the fact of taking short duration limit the returns?

It provides the best sharpe ratio in general, with the highest carry per unit of risk. It limits draw-downs to the detriment of lower expected returns.

Pixabay CC0 Public DomainJim Caron, portfolio manager and senior member on the Morgan Stanley Investment Management Global Fixed Income team . "A Rate Hike by the ECB May Not Occur Until Later in 2018 at the Earliest"

The primary risk to fixed income is a sudden and sustainable rise in interest rates. The conditions for this to occur is for the market to believe both domestic and global growth will be on a sustainable trend higher and that inflation will rise. However, according to Jim Caron, portfolio manager and senior member on the Morgan Stanley Investment Management Global Fixed Income team, there is little evidence that such a robust and sustainable event will actually occur. In his interview with Funds society he mentions that “We believe growth and inflation conditions are on the rise, but at a modest pace, not quickly. The key for fixed income investors is to create a durable portfolio that is actively managed. This provides one the ability to construct a portfolio with assets that are less sensitive to interest rates, such as credit related products, and provides the opportunity for the fund manager to manage duration risks. If done properly, bond funds can still produce positive excess returns even as rates rise.”

What are your expectations of rate hikes in the US this year and how will it affect the assets? Will there be contagion in Europe and will the ECB soon have to take solutions?

We believe the Fed will hike rates two times this year, with the risk being they hike three times. As we see it, the Fed will proceed cautiously as there are still many unknowns with US resect to fiscal policy, political risk events in Europe and economic risks surrounding trade and China. The ECB faces the same challenges but is further behind in the post crisis recovery cycle than the US. A rate hike by the ECB may not occur until later in 2018 at the earliest.

Is there a danger of capital turnover from fixed income to equity?

We recognize that there are other risks to fixed income in terms of capital flows. Many are over invested in fixed income and under invested in equities. If economic conditions convincingly improve, then investors may reallocate away from bonds into equities. This is a risk. However, if bond yields rise enough, it could slow the economy and this would re-attract investors to fixed income. So, there are limitations to how high and how fast bond yields can rise in the current environment.

In this environment, is it still a good asset to invest in or should we exacerbate caution when investing in debt? Is it still possible to find value, for example by assuming a global and flexible fixed income perspective?

Fixed income will continue to be a large part of a balanced portfolio. Yes, we believe there are still opportunities in fixed income, but it needs to be managed differently. We believe flexible and active management is essential. A flexible strategy should perform better than a passive strategy because the bond manager can allocate risk away from sectors of the bond market with the most sensitivity to rising rates and into other sectors that are less sensitive to rising rates.

In which fixed income areas still you find value? Where is there more risk?

We believe there are certain ‘winning characteristics’ for fixed income assets in the current environment: 1) assets with improving fundamentals, 2) attractive yield and carry, 3) positive idiosyncratic factors such as valuation and supply an demand technicals and 4) assets with more credit sensitivity rather than interest rate sensitivity.

Do you prefer credit risk or duration risk? why?

The assets we think will perform best are: 1) US non-agency mortgages – these assets benefit from improving fundamentals and have positive supply and demand technicals in addition to having good carry and more credit rather than interest rate sensitivity. 2) Emerging markets: we like commodity exporters both in external and local EM. For local EM we also select countries whose fundamentals are improving, have attractive yields and undervalued currencies. 3) Middle market high yield: these are companies with less than $1Bn of debt outstanding whose performance is driven more by idiosyncratic credit factors rather than interest rates. Sectors we like are Manufacturing, exploration and production energy and food and beverage sectors. We believe high quality sovereign bonds, which are most rate sensitive will perform worst.

European peripheral debt: are there still opportunities in markets such as Spain?

We think European peripheral bond markets are risky and we hold minimal exposure. The risk stems from political uncertainty. However, once the election cycles pass across Europe, we do see value in owning peripheral bonds. However, we think they will first cheapen over the next several months.

What returns can be expected from assets facing this year?

Bond market returns will vary across asset class and strategy. In our unconstrained and actively managed fund, Global Fixed Income Opportunities, we think we can achieve a 5-6% return. Our asset selection and weightings are skewed to less interest rate sensitive products such as non agency mortgages, EM and high yield. In addition, we are underweight duration and for additional protection against a rise in yields.

Pixabay CC0 Public DomainPhoto: LinkedIn. Cristina Campabadal Founds CCS Finanzas, a Multi Family Office with Offices in Barcelona and Presence in Miami and New York

After more than 15 years working in the financial and wealth management industries, as financial adviser, first in Spain and then in the United States – where she specialized in Latin American clients -, Cristina Campabadal has created CCS Finanzas, with the intention of protecting and accompanying clients in managing their wealth, with a difference.

The new Multi Family Office has an office in Barcelona and presence in Miami and New York, and offers advice on equity, access and search of investment opportunities, negotiation of external commissions, direct dealings with suppliers, investment monitoring and revision of accounts, as well as supporting and complementing existing individual family offices or family governance matters and foundations.

In her new company, she has the support of an Advisory Board, which includes four respected professionals, a team of analysts, and an art adviser based in New York, who will advise clients on their portfolio of art collections and investments in works of art, and which will be one of the differentiating points of this newly created Multi Family office.

Prior to the founding of the firm, and for the past two years, Campabadal has worked as an advisory associate at WE Family Offices in Miami. Previously, she had worked as director for Latin America and Development in a Spanish Multi Family office. Previously, she was linked to Banco Santander International Private Banking in Miami, where she was financial adviser for Latin American clients – Andean region – and to Grupo BBVA, in the Private Banking business for HNWI in Spain…

Graduated in Economics from the University of Barcelona, Spain, she has several advanced certificates in Wealth Management, including investments, banking, and tax matters.