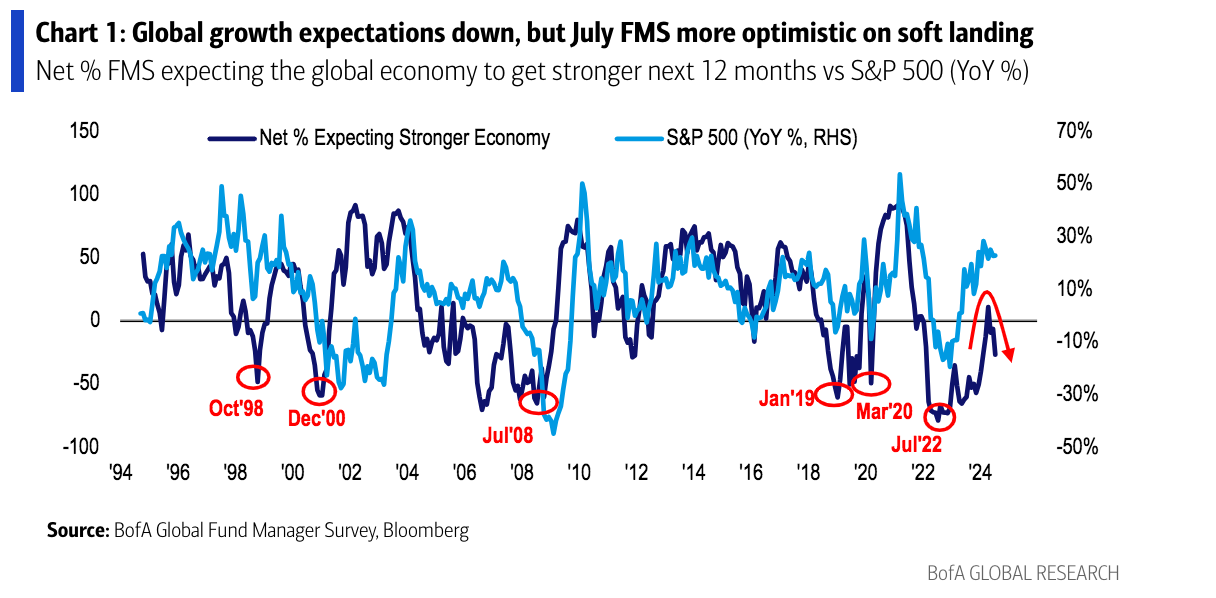

Optimism remains among investors, according to the global manager survey conducted monthly by Bank of America. According to the entity, they remain bullish driven by the expected Fed rate cuts and strong expectations that a soft landing will eventually be achieved in the U.S. economy.

However, it is noteworthy that growth expectations in July are lower and that FMS cash levels have risen to 4.1%. “Monetary policy is too restrictive according to 39% of investors, the most restrictive since November 2008, but this, in turn, reinforces the belief that global interest rates will drop in the next 12 months,” noted BofA.

56% of managers expect the Fed to cut rates for the first time at the FOMC meeting on September 18, while 87% estimate that the first Fed cut will occur in the second half of 2024. “84% expect at least two Fed rate cuts in the next 12 months: 22% predict two cuts, 40% predict three cuts, and 22% predict more than three cuts,” the survey specifies.

A soft landing is the most plausible option for 68% of respondents compared to 11% who expect a hard landing and 18% who expect neither. The bank’s conclusion is key: “We believe that hard landing risks are undervalued, given the slowdown in U.S. consumption, the labor market, and public spending. This makes us more bullish on bonds and gold in the second half of 2024.” They add that the shift in conviction from “long stocks and short bonds” expects an impact on the soft landing narrative and policy consolidating the existing conviction.

Investors’ global growth expectations decreased to a net 27% as they anticipate a weaker economy. In this regard, the entity explains that the increased pessimism about global growth this month is partly due to more negative U.S. growth prospects.

In fact, 53% of investors expect the U.S. economy to weaken, the highest percentage since December 2013. For now, two out of three investors still do not expect a global recession in the next 12 months. Specifically, 67% say a recession is unlikely, slightly down from 73% in June.

Complementing this view, “higher inflation” is no longer the main risk identified by managers, replaced by geopolitics. “87% expect lower rates, 81% a steeper yield curve, and 62% predict at least three Fed cuts in the next 12 months, starting on September 18,” noted BofA.

Asset Allocation

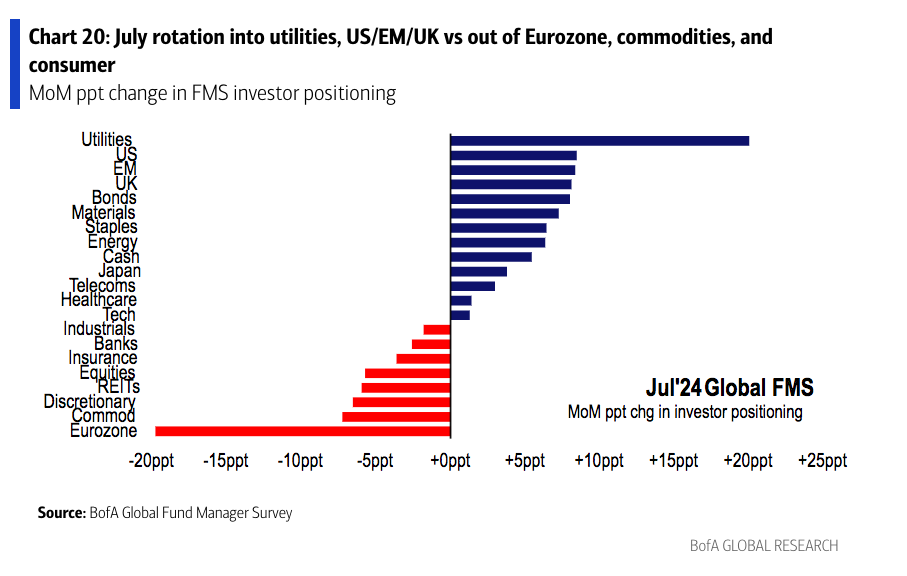

In this context, investors generally increased their allocation to utilities, U.S., emerging markets, and the UK, and reduced their exposure to the eurozone, commodities, and discretionary spending. Specifically, in July, investors remain overweight in equities and underweight in bonds. Notably, eurozone equity allocation fell to 10%, with a 20 percentage point month-over-month decline; the largest monthly drop since July 2012. Conversely, equity investors are more overweight in healthcare, technology, and telecommunications.

“71% of investors believe that being long in the Seven Magnificent is the most crowded trade. July marks the 16th consecutive month in which it has been the most crowded trade. 45% of respondents do not believe AI is a bubble, but a growing 43% of investors do,” added BofA.