CC-BY-SA-2.0, FlickrPhoto: Michael Davis-Burchat. Don't Let the Name Fool You

For the past several months now, I have been on an extended research trip for the express purpose of taking a close look into China’s domestic A-share market. While many investment professionals typically rely on screening functions to select potential portfolio holdings in specific sectors, when it comes to mainland China’s domestic-listed, A-share companies, you will want to proceed with caution.

In recent years, many Chinese companies, and especially A-share listed firms, have been using their capital—either with cash or with shares—to make acquisitions. Some firms are expanding their operations within specific value chains (either upstream or downstream), some are adding more products or service offerings and some are even entering entirely different sectors from where they began. In a few extreme cases, firms have transformed themselves by divesting their original businesses and re-emerged in a new industry. In the interim, they may even continue to maintain their old firm name before revisions reflect their new business models.

I’ve recently met with several firms that have made acquisitions within the past two years. Through my discussions with management teams, I gained insight into the motivations that have driven recent acquisitions. Due to the economic slowdown, firms that have been operating in traditional industries, such as the property and manufacturing sectors, are facing some difficulty. So expanding into more value-added areas in related industries is an attractive move. Alternatively, major shareholders or management teams may decide to strategically pivot and enter new areas in order to tap other growth drivers or convert the company entirely. Due to the lack of relevant talent and the time it takes to develop expertise organically in new areas, a firm in this situation may also opt to purchase a strong existing player in the new sector.

This kind of diversification and business transformation makes sense. As in many cases, firms can either leverage current resources to create synergy with the new businesses, or if they venture into an area they are not familiar with, they can pay a reasonable price for a leader with a good track record and then allow the acquired management team to retain a partial stake. If these firms don’t change, they may not survive by merely adhering to their old business strategies. In other words, they have little choice but to adapt.

On the other hand, there are also firms that make acquisitions in “hot” areas such as information technology, health care and media. Acquisitions are sometimes made simply for the sake of having exposure to such industries despite a lack of any concrete plans for development in the sector. A company may also make so many acquisitions in a single year that integration becomes problematic. In nearly all cases, there are profit guarantee clauses embedded in the acquisitions, and if the acquired firms are unable to meet targets, there are penalties imposed.

Though many firms have thus far delivered on profit guarantee clauses, there is still no guarantee that all profit targets will be met at the end of the contract term. Meanwhile, in cases where profit targets are not met, the acquirer must then write down assets.

As long-term investors, our job is to identify those firms with solid management teams who have clear objectives for acquisitions to provide new growth areas for themselves and to avoid those that pursue “hot” concepts to support their stock prices in the short term. As Chinese investors become more mature, they will eventually reward only firms that achieve long-term earnings growth from such acquisitions.

CC-BY-SA-2.0, Flickr. Are Investors Too Complacent About US Inflation?

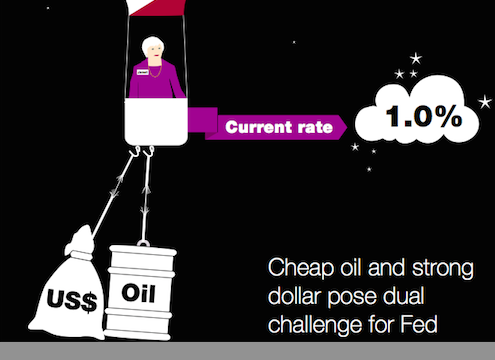

Low inflation has been an unwelcome thorn in the side of the US Federal Reserve (Fed) and remains the most elusive piece of the Fed’s interest rate puzzle. The decision to raise interest rates in December was predicated on consistent growth in the US jobs market and an assumption that this would eventually feed through to higher inflation. However, the sluggish outlook for inflation has been a key reason why the market’s expectations for further interest rate hikes this year have been delayed. But inflation has recently shown signs of stirring again, with the Fed’s core measure of inflation increasing by 1.7% over the year, a level close to its target of 2%. This has surprised investors and puts into question the consensus view that inflation is likely to remain below the Fed’s target for an extended period. As commodity prices potentially form a base we pose the question: ‘Are investors too complacent about US inflation?’

When looking at the key factors that drive US inflation, we can see that external inputs (mainly the oil price and the US dollar) have had a significantly negative impact on inflation readings over the past 18-24 months (see Figure 1). This does not come as much of a surprise, as within that time frame we have seen the price of Brent crude oil fall from circa US$100 per barrel in mid-2014 to US$40 per barrel currently, and the US dollar has appreciated strongly versus most major currencies. What is of greater interest is the extent to which these transient factors have been implicitly priced into future estimates for inflation, and that the more persistent drivers of inflation — which have been operating in a more normal fashion — have been largely overlooked.

The Federal Reserve Bank of St. Louis recently attempted to quantify the mispricing of inflation expectations by extracting the implied expectations of future oil prices from the breakeven expectations of inflation rates. Assuming that the non-energy elements of the CPI basket are at historically normal levels, inflation expectations are so low that they imply the oil price would reach zero by 2019 – a wholly unrealistic assumption in itself. This exercise illustrates that if the core elements of the CPI basket remain robust, energy prices have to remain at very low levels going forward for inflation to meet current expectations. If the logic of this analysis is reversed and we take a view that energy prices do stabilise, or even rise in line with the forward curve, it raises a more pertinent point; that the market is expecting almost non-existent rates of non-energy CPI over the next year. Providing the US economy does not fall into recession, it is hard to believe that these expectations will materialise.

Clearly the case for higher headline inflation rates is dependent on the path that oil prices will take over the next year. While the oil price is likely to be volatile in the near term, we think that highlighting a range of plausible scenarios can be helpful in understanding the potential range of inflation outcomes. We model five potential scenarios that range from oil prices testing the lows and rebounding to reaching the market consensus of US$60 per barrel by the end of the year.

Taking this one step further we calculate the year-on-year contributions using these oil price estimates, energy weightings and the historical elasticity between energy CPI and the oil price. We can see from Figure 2 that the strong negative contribution of energy to CPI ties in with the steep drop in oil prices we witnessed at the end of 2014 and beginning of 2015. This negative effect diminished as oil prices stabilised and started to recover. We can see that by the end of 2016 energy prices are likely to positively contribute the CPI, even in the more conservative scenarios.

While the central case is that inflation rates remain well contained, it is naïve to ignore the potential risk that the market could be surprised by higher inflation rates. Our nowcasting models suggest inflation and wages will be firm going forward and our commodity team believes that robust oil demand and a material decline in oil supply will provide support to the oil price. If there is a more sustained oil price recovery, consistent with our commodity team’s forecast of approximately US$60 per barrel, there is a meaningful risk that inflation could even overshoot to the upside. This is a tail risk that neither the bond, currency or equity markets are prepared for.

Philip Saunders is Co-Head of Multi-assets at Investec.

In the wake of a sharp recovery, equity market investors’ attention has been drawn to geopolitics. From the terrorist attack in Belgium, to President Barack Obama’s historic visit to Cuba, to the narrowing of the U.S. presidential field, newsworthy but largely noneconomic events have predominated. Post earnings season, without key data announcements, markets have lacked meaningful drivers and have been largely directionless, but without the turbulence that has often been seen recently.

Investors can be forgiven for pushing the pause button. In the opening five weeks of the quarter, the markets were characterized by fears of global deflation, apprehension over growth rates in the U.S. and China—and price volatility. At the time, we suggested that economic concerns were exaggerated. Indeed, reassuring consumer, manufacturing and housing trends in the U.S. and a rebound in oil prices, along with a modest increase in the renminbi’s valuation, helped ease fears and contributed to the market’s subsequent V-shaped recovery. On the monetary front, the market’s expectations for a pullback by the Federal Reserve on planned rate increases and the ECB’s easing actions reduced headwinds for risk assets and alleviated concerns about a damaging deflationary cycle.

In a sense, the relative market stability of the past week should be reassuring in the context of the global newswire. Investors have learned that geopolitical events, no matter how tragic or appalling in nature, need to be assessed in relation to economic impact. The terrible bombings in Belgium had an immediate but moderate effect on the markets. But only if such tragedies lead to meaningful changes in personal spending, business confidence and the like do they affect the broader economic picture.

A more positive narrative could be found in President Obama’s visit to Cuba—the first such visit by a sitting U.S. president since 1959. But, again, the economic significance is more tied to future developments: whether the current thaw between the two countries extends to a lifting of the U.S. embargo and the development of meaningful business relationships. Substantial disputes remain, most prominently on human rights, and we will be watching the situation with interest.

Finally, the turbulent U.S. election race is at long last narrowing, as Donald Trump and Hillary Clinton have solidified their front-runner status but continue to face rearguard competition from Ted Cruz and John Kasich, and Bernie Sanders. This is an important election, with real economic impacts for the U.S., particularly as they relate to the health care sector, infrastructure and tax policy (among other key flashpoints), as well as for our global trading partners. The unpredictable nature of this year’s process has been, to a degree, a headwind for equity markets. As the race continues to develop, and as we have a clearer sense of what the major candidates would seek to achieve in office, we may start to see market action reflecting the anticipated outcome. The situation bears watching, because, as we’ve said, fiscal policy is an important component in driving U.S. economic growth to a higher level. Monetary policy cannot alone solve the current growth problem.

More than likely, investor attention in the short term will move away from these situations as we start to see more market data that clarifies the Fed’s path on interest rates, economic growth and, ultimately, the outlook for earnings in the latter part of 2016. At that point, equities will have reason to get back into motion.

Neuberger Berman’s CIO insight column by Joseph V. Amato

CC-BY-SA-2.0, FlickrPhoto: Amaradestiempo en Pixabay. Mexican Pension Funds Made a 516 Million Dollar Profit in 2015

The 11 Mexican public retirement funds managers, also known as Afores had commision based revenues of 26,817 million pesos in 2015, which is equivalent to $1,554.61 million (considering 17.25 pesos per dollar, the rate at the end of 2015). According to official figures published on regulator’s website, consar.gob.mx, this amount represents 1.06% of the resources administered at year end, reflecting growth of 5.2% in 2015, slightly higher than the previous year’s 4.7%.

Meanwhile, net income of the 11 Afores stood at 8,898 million pesos or $516 million with a negative growth of -2% (in pesos) over the previous year. Interestingly, in 2014 the growth in this category was 13%, which shows how complicated was the year that just ended; because while in 2014 the peso-denominated assets grew 15.7%, in 2015 growth was of only 7.1%. Assets under management of Afores ended the year at 148,300 million dollars. It is important to highlight that current comparisons are made in pesos, as these companies produce pesos, and given that the currency depreciation of 17% in 2015 distorts the figures if looked at in dollars.

The afore business requires economies of scale. They need a significant investment in systems to handle a large number of customers (53.6 million workers) and thus must be efficient in their operation; as well as having the ability to bring new customers and retain affiliated workers. Regardless of size, all are interested in having more customers, however the incentive is greater for small and medium ones.

Breaking up the fee income, 40% corresponds to operating costs; 26% to membership and transfer costs; 17% is administrative overhead; 7% cash operating costs of operating personnel and service workers; 4% regulatory costs; and 3% cash operating costs for investment and risk management.

One point that the CONSAR has done much emphasis on recently, refers to expenditure by the Afores for membership and transfer which has gone from 31% of fee’s income in 2014 to 26% in 2015. Afore Pensionissste with a 13% expenditure is the afore with the lowest cost of membership and transfer; however it is important to mention that is also the afore with the lowest number of promoters. Afore XXI Banorte, Banamex and Coppel spent 21% of their fee’s income in promotion; while Profuturo spent 34%, Invercap 42% and MetLife 48%.

For the 11 Afores on the market the main challenge is to grow their income at a larger rate than the drop in commissions every year. During 2015 only 6 Afores succeeded in doing so.

CC-BY-SA-2.0, FlickrPhoto: Roberta Schonborg. Scared of Defaults? Don’t Worry, There’s a Bright Side

It’s hard to talk about high-yield bonds today without addressing defaults. So here’s our take on the matter: Default rates will rise over the next few years. But don’t fret: returns are likely to rise, too.

Defaults have been below average for years, so an increase shouldn’t come as a huge surprise. High-yield bonds have always been riskier than other types of bonds. And it’s not uncommon for some issuers to default as the credit cycle winds down and borrowing costs rise.

But a higher average default rate doesn’t mean returns have to suffer—provided you’ve been selective about your exposures. Over the past two decades, jumps in the average default rate have usually been followed by big increases in returns (Display).

The reason is tied partly to investor psychology. Defaults usually aren’t spread evenly across the high-yield market, which includes many different regions and sectors. Nonetheless, investors tend to respond to a rise or an expected rise in defaults by punishing the whole high-yield market.

The result: plenty of sound credits trading at very attractive valuations. For example, a large share of defaults in 2001 and 2002 were telecom companies that had borrowed heavily but ran into trouble when the dot-com bubble burst. That led to selling across the US high-yield market. But investors who bought bonds in nontelecom sectors in the years after 2002 did well. In 2003, US high-yield returns soared to 29%.

Beyond Energy, Values Look Compelling

We think something similar is going on now, with energy, metals and mining companies standing in for telecoms. With the price of oil near multidecade lows, we expect these types of companies to account for a large share of defaults over the coming years.

Many investors have reacted to recent volatility as they did in 2002—by bailing out of the market altogether. As a result, some non–energy sector bonds now offer higher yields than they have in years.

That’s important, because starting yield—now above 8% on average—is one of the best predictors of what investors can expect to earn over the next five years. In 2009, high-yield defaults hit a record high—but so did high-yield returns. At one point that year, the average yield on the Barclays US Corporate High Yield Index exceeded 20%.

Even so, investors can’t afford to be cavalier about the market and its risks. It’s critically important to be selective, even among higher-quality bonds. That’s especially true in US high yield, which is in the later stages of the credit cycle, and Asian high yield, which is already in contraction. A global, multi-sector approach makes sense, since different regions and sectors are at different stages of the cycle.

But we think it would be a mistake to abandon high yield altogether. The biggest risk today isn’t a rise in defaults—it’s pulling out of the market prematurely and missing the opportunity to buy before it rebounds.

Gershon M. Distenfeld is director high yield at AB.

CC-BY-SA-2.0, FlickrPhoto: Aristipo Crónica Popular. Oil: Up, Up And...?

The New Year began in disastrous fashion for the oil market with Brent crude touching 12 year lows in January, which followed a year to forget in 2015. Confidence in the prospects for the oil price seemed irreversibly low when the decision to lift Iranian sanctions was announced and Chinese economic growth statistics continued to paint a rather bleak picture for global growth. However, oil has undergone a swift and material recovery since bottoming out on 18 January. The bounce in sentiment has not been exclusive to oil, with iron ore, copper and coal also experiencing a surge in their respective prices. The key question from here remains: is the rise in oil sustainable, or is it little more than a short squeeze which lacks any fundamental basis?

As outlined in our ‘Multi-Asset Brief’ in January, we believed the tide was beginning to turn in oil and that Brent crude touching a low of US$27.88 per barrel in January was not justified. Since that paper’s release we have witnessed a few interesting developments, not least of which has been a tentative agreement between Saudi Arabia and Russia over a planned production cap. While the deal itself was viewed as having little impact on supply over the short term, as it was predicated on other key producers (including Iran) also capping production, it was symbolic that a deal by a Saudi-led Opec is still possible in the current environment. The oil cartel had previously refrained from limiting supply, despite the weak market conditions, preferring to keep the market oversupplied to implicitly drive out incumbent shale producers.

The much publicised end to Iranian sanctions finally came on 16 January when a nuclear deal was struck between Iran and six of the world’s western powers. There was little doubt within the market that the easing of Iranian sanctions would cause a significant uptick in oil supply, although the jury is still out on how much and how quickly Iran can increase its production to anything that resembled its pre-sanction high. Since the sanctions were lifted, the increase in Iranian output has significantly undershot consensus market expectations, driven by ageing infrastructure and lack of investment, which has reduced its capacity to increase production for the time being. The oil market has also benefited from a drop in oil production in Iraq and Nigeria, with the former experiencing the largest decline due to a stoppage in flow along a pipeline carrying oil across the Kurdish border.

In a phenomenon which began in October 2014, the US oil rig count has continued to transition lower, falling approximately 72% from its peak. At the same time, global oil capital expenditure (capex) has also decreased, with Simmons forecasting it to fall approximately 50% in 2016 which followed a similar reduction in 2015. While the fall in rig count and capex has been swift and material, the drop in US oil production has been modest in comparison, although we began to see consistent declines being recorded in February. We believe the market over anticipated the speed at which production would decline in response to the falling capex, which exacerbated the downward pressure on oil prices, as production remained stubbornly high. Nonetheless, our view is for US production to follow a similar path to the fall in rig counts for the remainder of the year and into 2017, as we believe shale producers will be reluctant to increase drilling spending with prices below their respective marginal costs of production.

A looming factor that has the potential to jeopardise the recent rally in the oil market is the historically high level of oil inventories. The above-trend level of inventories has been caused by two main factors:

Oil supply strongly exceeding oil demand

A steep forward curve which acts as a strong incentive to build inventories. However, recently we have seen the forward curve flatten, thus minimising the incentive to build inventories as the premium received from doing so is comparatively less. A flattening forward curve, as oil inventories are high, in the short term should see new supply come online, which theoretically threatens an already oversupplied market. While we are obviously cognisant of this risk, we believe consistently falling inventories will be supportive of a more stable oil market.

We held the view earlier in the year that an oil price at sub US$28 per barrel was not sustainable over the longer term and not in line with fundamentals. The recent recovery has been swifter than even our expectations. In light of the current uncertainty in the market, we believe the path over the short term for oil will be volatile, particularly as the threat of inventories swamping the market is very real. However, over the longer term, we are more constructive on both the stability of the market and its eventual price, as falling capital expenditure and rig counts begin to have a more pronounced impact. Similarly, the tentative agreement by Opec members to freeze production, while complex and contingent on a number of factors, is still a potential positive for controlling supply over the longer term. As for the positioning of our portfolios, we are conscious of the short-term risks that lie ahead, although we do believe there are genuine factors which are now supportive of a higher oil price.

Philip Saunders is co-Head of Multi-Asset at Investec.

When they write the final history of central banks and the global financial crisis, the six weeks from January 29 to March 16, 2016 will be a prominent late chapter.

We went from the Bank of Japan’s (BoJ) surprise adoption of a negative interest rate to the Federal Reserve finally giving ground to market bearishness, with yet another game-changing intervention from the European Central Bank’s (ECB) “Super” Mario Draghi in between. Not coincidentally, the S&P 500 Index rallied 11% from its lows during the same period. Central banks have been looking into the abyss of spiraling negative rates and all-out currency war over recent months—and the last two weeks saw them pull back from the edge.

My colleagues and I have discussed how corrosive negative rates could be for banks and, potentially, for the financial system at large. On top of this, benefits from resulting currency weakness were always likely to be outweighed by slow global growth, rising import costs and other countries entering the fray. Markets felt instinctively uncomfortable: The BoJ’s decision sparked a punishing fortnight for risk assets and a backlash from domestic savers and consumers. If ever a monetary easing announcement backfired, this was it.

Discussion spread well beyond Neuberger Berman, in a tone that I would describe as modestly critical.

Central banks themselves have been part of the conversation, sometimes in public (think of the normally dovish New York Fed President Bill Dudley describing talk of negative rates in the U.S. as “extraordinarily premature” on February 12) and sometimes behind the scenes. At the ECB’s policy announcement and press conference on March 10, a new consensus seemed to be revealed.

The irony is that the ECB did cut its deposit rate again, to -0.40%. It took some of the sting out by extending liquidity to banks at the same rate for five years, and also expanded its quantitative easing program and added corporate bonds to the securities it could purchase. Risk markets liked the news and the euro dived. But Draghi’s comments during the press conference were the real story: “We don’t anticipate it will be necessary to reduce rates further,” he said. He acknowledged the danger that would pose to banks and confirmed a shift “from rates instruments to other, nonconventional instruments.” Suddenly the headline wasn’t negative rates anymore, but the “nonconventional” stuff. Markets really liked that—and the euro soared.

When the BoJ held rates steady five days later, despite a gloomy economic assessment, and added measures to shield banks from its negative rate, that fit the new consensus.

And the Federal Reserve last week? In holding rates and revising its rate projections substantially downward, it finally responded to what markets had been asking for (via their pricing of risk assets and Fed Funds futures) after months trying to break free of those expectations.

But it fit the consensus in other ways, too. In 2015, the roadmap for the Fed’s policy trajectory was unclear: a bit about China and global conditions, a bit about U.S. employment and inflation, but not much about how it was all related. Last week, the message was crystal: We can’t consider U.S. prospects without taking account of global conditions. Despite very modest Fed policy moves so far, U.S. financial conditions have tightened significantly. Why? Because of U.S. dollar strength. And why is the dollar so strong? Because slowing growth led to aggressive monetary easing and weaker and weaker currencies in the rest of the world.

With the ECB and the BoJ choosing more direct stimulus over the rates-and-currencies channel, however, many believe the dollar is unlikely to rise much further from here. The resulting loosening of U.S. conditions may give the Fed wiggle room for its two hikes in 2016. This is what the Fed gains from the new consensus. With Thursday’s core inflation print surprising to the upside, is it possible that Fed Fund futures, which responded to the Fed announcement by lowering the implied probability of a hike in June, are now behind the curve?

We’ll see. The past two weeks have seen a major transition in central bank philosophy, and possibly a renewed sense of coordination. So far, markets have been euphoric at this turn away from the abyss and back towards some kind of “normality.” How this normality ultimately plays out remains an open question.

The Fed’s dovish turn coming out of its March 15-16 meeting took many market participants by surprise. The Federal Reserve’s median projection for Fed Funds rate increases in 2016 fell from four in December to two, reflecting concerns about the impact of lower global growth and tighter financial market conditions on US GDP and inflation.

The median forecast for core PCE inflation at the end of 2016 remained unchanged at 1.6%, while the forecast for headline PCE fell from 1.6% to 1.2%. Finally, perhaps in recognition of relatively moderate wage inflation, the estimate for longer run median NAIRU (non-accelerating inflation rate of unemployment) was reduced to 4.8% from 4.9%.

The Fed took these decisions despite having up to the minute economic and market data that should have, in our view, allayed their concerns about the impact of both global growth and tighter conditions on US GDP and inflation. Recent US GDP, employment and inflation data have remained stable or are somewhat better than December levels, despite lower global growth. Having recovered from the early year sell-off, financial conditions on March 15, the day prior to the release of their statement, remained similar to those observed in December, when the Fed decided to raise rates. After reviewing the available data, one may conclude that either the Federal Reserve has erred in its current decision, and has given up some of its flexibility to raise rates, or that the Fed decided that their December hike was a mistake.

Below, we have highlighted a number of relevant economic and market levels at December 16, following the release of the Fed’s December statement and projections, and on March 15, prior to their release of their March 16 statement and projections.

The bond market’s response to the European Central Bank’s (ECB) latest easing measures was immediate and broadly positive, but the implications for the real economy are harder to gauge.

The market’s immediate reaction to the latest easing measures announced by the ECB on 10 March was, in some respects, counter-intuitive. Most investors will be used to seeing government bond yields fall in the wake of greater-than-expected policy easing, but in this instance, 5-year and 10-year Bund yields rose steeply.

This is because Bund yields had already been driven to extremely low levels during January and February’s firmly ‘risk-off’ market tone. The ECB’s latest support measures cheered markets, and resulted in some of the ‘safety premium’ embedded in Bund valuations being reduced.

A boost for bond bulls

Indeed, there is little doubt that the latest steps from ECB President Mario Draghi are positive for financial markets. The first phase of ECB asset purchases, in early 2015, focused on buying government debt. This pushed government bond prices up and nudged investors into riskier assets to replace the lost yield.

The fact that risk assets – currently non-banking investment grade corporate bonds – are now included in the expanded €80 billion-a-month asset purchase scheme, means that the ECB is driving down the cost of risk more directly. We expect investment grade corporate bonds will continue to perform strongly from here. Credit spreads should narrow, and investors will reach for higher-yielding corporate assets. This impact has also been positive for equity markets, because the cost of capital has improved.

Will the changes make a “real” difference?

The implications for the real economy are less clear-cut. A high proportion of the liquidity which should have entered the US economy through its own QE schemes became ensnared in the banking system, and the velocity of money didn’t appreciably pick up. There was no real spike in lending, and regulatory changes meant that the mortgage market remained somewhat impaired. Of course, if QE had never been implemented, then the condition of the US economy could have been far worse.

In our view, the likelihood of the ECB achieving its vaunted 2% inflation target, even within five years, is low. The output gap, which bears down on both worker and company pricing power, is too significant for prices to improve to the 2% target growth rate. Economic growth – currently forecast to be around 1.4% in 2016 – is insufficient to close this output gap quickly. The ECB, in our view, will need to do more.

The waiting game

This, then, begs the question of why Mario Draghi followed up the latest policy announcements with the suggestion that further rate cuts are “unlikely”. The euro, having fallen after the deposit rate was reduced, rose as soon as Mr Draghi made the comment. However, we see his observation as largely practical. Running a negative interest rate policy is unlikely to work in the long term, as it would encourage investors to hoard cash. Excessively negative rates mean that even the cost of insuring cash deposits ‘in-house’ could be less significant than the cost of depositing funds with the ECB.

However the ECB proceeds from here, it seems unlikely that the deposit rate will be the tool that they reach for. For now, we believe that the amended policy environment has bolstered existing support for risk-asset markets and settled simmering nerves. Patience will be required to see quite how effective the measures will be for stimulating more economic growth.

CC-BY-SA-2.0, FlickrPhoto: Todd Chandler. Foreigners are Interested in Participating in the Mexican Asset Management Marketplace

The interest of foreign operators to enter the Asset Management business in Mexico keeps on growing.

Late last year, the Swiss bank Julius Baer completed the acquisition of 40% of the Mexican company NSC Asesores, a firm that serves as an independent financial advisor in Mexico since 1987. BNP Paribas Investment Partners Mexico last month announced its foray into the Mexican market through mutual funds and mandates.

The Azimut Group expects to receive authorization in the near future to become a fund operator. Azimut Group acquired Mexican Más Fondos owns more funds (founded in 2002) which is the largest integrated distributor of investment companies in Mexico.

A few days ago we read in the news that Afore XXI Banorte finally funded the two mandates it gave BlackRock and Schroders back in 2013. BlackRock received 320 million dollars and Schroders 220 million dollars.

This business has very interesting numbers, where many firms want to enter but only five have been able to do since only two Afores have participated in this type of vehicle. Although CONSAR allowed mandates since 2011, Afore Banamex was able to fund the strategy until 2013 and Afore XXI Banorte just in the last month.

According to updated information of the regulator (Consar), US$ 2.2 billion have been promised to five Global Asset Managers: BlackRock, Pioneer, Schroders, Franklin Templeton and Banque Paribas. Approximately 60% of the resources allocated come from Afore Banamex and 40% from XXI Banorte. If all Afores diversify using a mandate, this amount is equivalent to only 8% of the US$28.4 billion that the 20% limit allows. Currently the Afores manage about US$142 billion in assets.

The appetite for having a presence in Mexico is due to a growing market with increasingly sophisticated needs; as well as confidence in the country, given Mexico has become a very attractive market in Latin America, as well as a sizeable potential revenue.

Some firms are redefining their business in Latin America as in the case of Deutsche Bank which will sell or close its business in 10 countries, five of them in Latin America -including Mexico, however, from my point of view, the reason for this has more to do with specialization than with a disdain for the region.

Considering the appetite to enter the Mexican market, local and foreign participants who are already present, can not sit and wait it out while strong competition is displayed. In fact, there is speculation that there are a couple of signatures embedded in evaluation processes and more advanced in local authorizations.