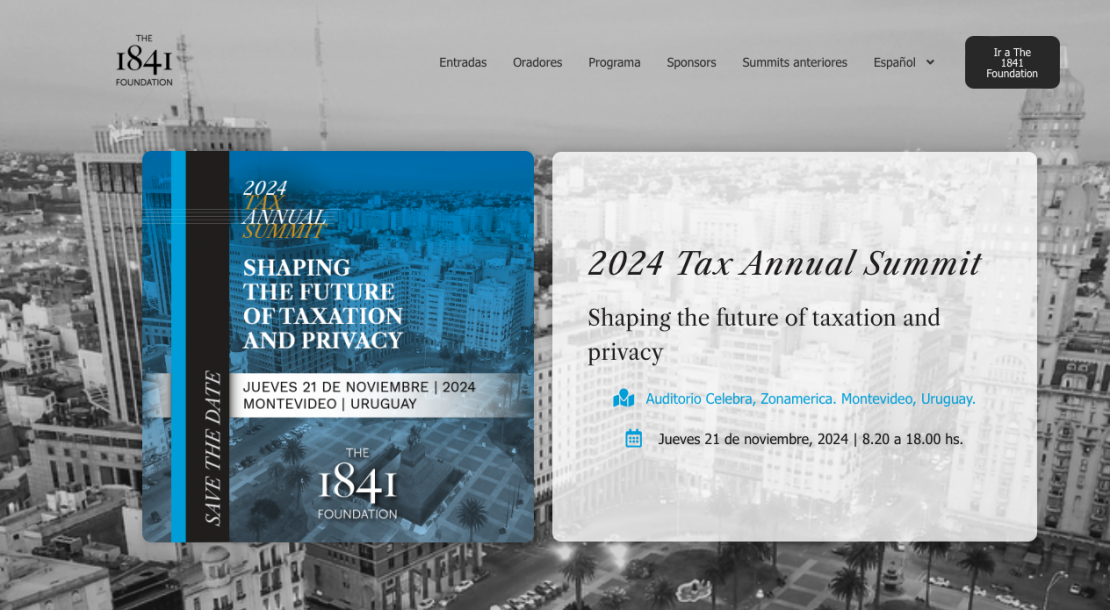

The election of Donald Trump has clarified the trajectory of fiscal policies in 2025, though uncertainty remains in Latin America regarding Argentina’s future direction. Tax expert Martin Litwak offers his view on potential changes and provides a summary of 2024’s fiscal trends, which will be further discussed at the Tax Annual Summit on November 21 in Montevideo.

Here is the updated agenda and registration information.

Trump, New Tax Cuts, Continuity of FATCA, and Public Spending Uncertainty

With caution regarding a government yet to take office, Litwak predicts the following:

(a) Trump’s second term will likely be more “Trumpist” than his first, given that he won with a greater margin (including a higher number of electors) and now holds a majority in both chambers. Additionally, he secured the popular vote—a feat he did not achieve in 2016 or 2020. The Republican Party is also more unified behind him than during his first administration.

(b) With the Republican majority in both chambers, it is probable that Trump’s first-term tax cuts will be extended for another ten years, possibly with an additional corporate tax rate reduction. However, concerns linger about the potential resurgence of a “border-adjustable tax.” Regardless, any fiscal policy pursued by Trump is expected to be significantly better than what Kamala Harris had proposed (e.g., wealth taxes, increased corporate taxes for certain sectors, unrealized capital gains tax, among others).

(c) In terms of foreign trade and global relations, another period of “deglobalization” is expected. While this has negative implications for the region (e.g., increased tariffs on specific products), it also holds a potentially positive aspect, such as the possible defunding of the OECD.

(d) Regarding FATCA implementation and international information exchange, Trump did not eliminate this legislation during his first term nor replace the U.S. tax system based on nationality with a residency-based one. Therefore, it is unlikely that he will do so now, although he did nearly halt the signing of new IGAs (intergovernmental agreements), a trend Litwak hopes will continue.

(e) The big question mark pertains to Trump’s stance on public spending—a non-issue during his first term but potentially more relevant now. It will be interesting to see what role Elon Musk might play in the administration.

Expectations for 2025

“Looking ahead to 2025, I believe the key factor will be what President Milei can achieve in Argentina,” says Litwak.

So far, despite Milei having been in power for nearly a year, there has been no substantial tax reduction. Only the Personal Assets Tax and the “Impuesto PAIS” have been lowered, but the news is less positive upon closer examination. The Personal Assets Tax, which should have been abolished, was only reduced gradually without significantly raising the non-taxable minimum. An aggressive offer was made to those willing to prepay five years of this tax.

The Impuesto PAIS was reduced, but Milei had significantly raised it upon taking office. The subsequent reduction did not fully offset the initial increase. The major question concerning this tax is what will happen in 2025, as it is set to expire on December 31, 2024.

How Did Argentina’s Capital Amnesty Work?

“We predicted the amounts to be regularized quite accurately and stated from the start that two figures would stand out at the end of this new amnesty—one positive and one less so,” notes Litwak. The positive figure relates to the total regularized funds, while the less favorable one pertains to the revenue the government collected through the regularization tax.

Additional Conclusions:

(a) The amnesty primarily attracted taxpayers with undeclared cash holdings. (b) It was not attractive to high-net-worth individuals or those holding other types of assets. (c) The key issue for Argentine taxpayers is not whether to enter the amnesty but how to structure their assets regardless of their decision.

Changes in 2024 and What Happened in Latin America

There have been relatively few tax changes this year, in contrast to the prior three to four years in the region, Litwak observes. Colombia and Brazil stand out as countries with significant changes, along with major tax increases in Argentina and Bolivia, the latter having introduced a wealth tax.

Colombia’s Fiscal Reform of 2022 (Law 2277) brought multiple changes that affected 2023 and are now becoming evident in 2024, including an additional 5% surcharge on corporate income tax for oil and coal companies, financial institutions, and insurance and reinsurance firms, a permanent wealth tax, and increased taxes on foreign corporations with significant economic presence.

Brazil has made changes affecting deferral of gains from offshore investments, prompting high-net-worth families to consider fiscal relocations or restructuring trust arrangements.

In Bolivia, the introduction of a “Wealth Tax” in 2021 imposed rates ranging from 1.4% to 2.4% based on net worth.

In Argentina, President Alberto Fernández‘s government established or increased 18 taxes, contributing to the country’s record-high tax burden. This includes the IVA, Income Tax, and the Wealth Tax.

Finally, countries like Ecuador and Uruguay, despite being market-oriented, have failed to deliver significant tax cuts, which is disappointing.

Information about the Tax Annual Summit 2024 can be found by clicking here

Organized by The 1841 Foundation

The 1841 Foundation of the U.S. Internal Revenue Code, meaning donations are tax-deductible