Alejandro Rubinstein has joined Insigneo as Senior Vice President. Based in the Brickell office in Miami, he will focus on providing advisory and brokerage services to clients in the United States, Chile, Colombia, and Peru, according to a statement issued by Insigneo,.

Rubinstein, who brings more than 25 years of experience in international markets, comes from Merrill Lynch. His expertise in global financial services and focus on customized solutions for clients aligns with the company’s strategy, the press release said.

“I’m excited to be part of Insigneo’s innovative culture, where expertise and creativity combine to deliver outstanding client experiences,” said Rubinstein.

As Senior Vice President, he will leverage Insigneo’s platform of resources and services to expand his business and develop financial strategies tailored to his clients’ needs, the firm adds.

“We are pleased to have Alex join the Insigneo team,” said Jose Salazar, Market Head of Miami. “His experience in international markets complements our robust platform of services and resources. We look forward to growing together and developing his business.”

Citi will lose its Global Head of Private Banking, Ida Liu, as the executive announced in a LinkedIn post.

“After nearly two decades at Citi, including the privilege of serving as Global Head of Citi Private Bank, I have made the decision to leave the firm and embark on the next chapter of my professional journey,” Liu posted on LinkedIn.

The expert, with more than 25 years of experience, joined Citi in 2007, where she held various positions until her most recent role as Global Head of Private Banking, according to her LinkedIn profile.

“Great careers are defined by embracing new challenges and opportunities, and this is the right time to leverage my global experience, leadership expertise, and passion for growth in bold and exciting new ways,” added the executive of the U.S. bank.

In addition to Citi, Liu worked at Merrill Lynch (1999-2004) and Vivienne Tam (2004-2007).

CC-BY-SA-2.0, FlickrPhoto: ankakay

. Moneda Asset Management Announces US$100 Million Investment from CPPIB Credit Investments Inc.

The ETF industry started 2025 on the right foot. Among the standout news at the beginning of the year is that asset manager BlackRock launched a new Bitcoin exchange-traded fund (ETF) on Cboe Canada, according to information from the Canadian stock exchange released earlier this week. The announcement was confirmed in a statement issued by BlackRock itself.

This Canadian fund, registered as the iShares Bitcoin ETF, will trade under the same symbol, IBIT, as BlackRock’s U.S. product. Additionally, shares denominated in U.S. dollars will trade under the symbol IBIT.U, according to the stock exchange.

“The iShares fund offers Canadian investors a way to gain exposure to Bitcoin while helping eliminate the operational and custodial complexities of holding Bitcoin directly,” said Helen Hayes, Head of iShares Canada at BlackRock.

The ETF is designed to provide Canadian investors access to BlackRock’s primary U.S. spot Bitcoin fund, iShares Bitcoin Trust (IBIT). It will invest all or most of its assets in IBIT, according to a statement from Cboe Canada.

Likewise, this fund will join a dozen other Bitcoin ETFs already trading on Canadian exchanges, according to sources at Nasdaq.

According to figures from BlackRock, its U.S. IBIT ETF has become the world’s most popular Bitcoin fund. Since its launch in January 2024, this fund has recorded over $37 billion in net inflows.

As recently as November, U.S. Bitcoin ETFs surpassed $100 billion in net assets for the first time, according to data from Bloomberg Intelligence. It is expected that Bitcoin ETFs will attract approximately $48 billion in net inflows this year.

The week has begun with the tech sector reeling. On Monday, Nvidia led a market slump—dropping as much as 17%—triggered by the strong performance of the low-cost generative AI assistant developed by Chinese company DeepSeek. According to experts, the emergence of a potentially more efficient approach to AI processing—reducing model training costs by 86%—raises questions about the necessity of the billions of dollars planned for infrastructure and intellectual property investment.

As a result, the S&P 500 index dropped 1.5%, and Nvidia‘s decline—the largest single-day market capitalization loss for the company at $589 billion—dragged the Nasdaq Composite down 3.1%. “The emergence of the new competitor has primarily impacted the entire data center value chain. This includes chip manufacturing equipment makers like ASML (-7.2%), high-performance chip manufacturers (Nvidia and Broadcom (-17.4%)), as well as companies specializing in energy infrastructure like Schneider Electric (-9.6%) or the real estate side of data centers like Digital Realty (-8.7%),” explain analysts at Banca March.

What explains these movements? In recent days, the generative AI assistant developed by DeepSeek has become the most downloaded app for iPhone, surpassing the popular ChatGPT application from OpenAI. Nvidia‘s drop has been the most visible consequence of this shift, driven by fears about the impact DeepSeek could have on the demand for high-end microchips.

“DeepSeek could be a seismic shift for the AI industry. If its advancements hold true, model training costs would drastically decrease, changing the game for everyone,” says Víctor Alvargonzález, founder of Nextep Finance. In his view, one of the main reasons behind Wall Street’s recent sell-off—particularly Nvidia‘s worst-ever trading session in U.S. stock market history—is DeepSeek‘s promise to reduce algorithm training costs. Estimates suggest that training costs could drop from the current $50 million per model to just $7 million or less, thanks to process simplification and a 75% reduction in memory requirements.

Amid these declines, Louise Dudley, portfolio manager of global equities at Federated Hermes Limited, believes there are still many questions left unanswered. “For Nvidia, as a key supplier of premium chips worldwide, the concern is whether companies will need fewer chips in the future. However, the company responded to the news by highlighting ‘excellent progress,’ signaling optimism about ongoing AI model developments, which are still in their relative infancy.

For companies involved in building data centers, the short-term impact is likely to be significant, as demand has been very strong. The new DeepSeek model code will be reviewed for potential performance improvements. Existing projects under development are at risk, and this will be a key focus for investors. This news will likely increase both corporate and consumer appetite for AI tools, given improved accessibility, leveraging this innovation and accelerating AI adoption timelines,” Dudley points out.

Market Reactions and Expert Insights

According to Hyunho Sohn, portfolio manager of the Fidelity Funds Global Technology Fund, Chinese AI startup DeepSeek has introduced AI models that perform comparably to OpenAI’s ChatGPT models while being significantly more cost-effective. “This efficiency advantage has raised a series of questions about the perceived ‘winners’ in the global AI ecosystem, the implications for hyperscaler capital expenditures, and the effectiveness of sanctions and export bans aimed at preventing high-level generative AI progress in China.

This is an evolving situation, and we may see short-term volatility until it becomes clear how much more efficient this technology really is. While broader implications must be assessed on a case-by-case basis, I generally believe this development will be deflationary,” Sohn states.

Despite the shockwaves, Fidelity’s portfolio manager believes this is ultimately beneficial for end-users and service providers, though it could have negative implications for hardware. “This is similar to what we saw in the early days of the internet when people vastly underestimated the scale of innovation, technological adoption, and service-based business potential, while greatly overestimating the total addressable market (TAM) for hardware,” explains Sohn.

In the view of Amadeo Alentorn, manager of the Global Equity Absolute Return fund and head of the systematic equity team at Jupiter AM, DeepSeek’s rise is part of a broader trend that has been developing for months. In recent times, there have been major advances in Small Language Models (SLM), which contrast with the large models used by companies like OpenAI. The central question has been whether it is possible to build more precise, specialized models that focus on specific areas, such as law or medicine, rather than encompassing all knowledge.

“So far, the rise of artificial intelligence has primarily benefited a small group of large companies. However, recent advancements suggest that we may be witnessing a paradigm shift, where smaller companies can also leverage this technology without needing massive infrastructure investments. Identifying which companies will lead this new AI phase is a complex task, but what is clear is that this evolution promotes diversification within the sector. AI could expand beyond tech giants and create new business opportunities across various industries,” Alentorn asserts.

High Valuations Under Scrutiny

In this context, Fidelity’s portfolio manager acknowledges that, as he has been saying for some time, many AI semiconductors are expensive, with sentiment, valuations, and momentum slowing down—“the most interesting opportunities lie within the services ecosystem.”

“It’s still early, but I would add that the rapid developments in generative AI highlight the need for proximity and connection throughout the tech ecosystem—something we are well-positioned for, given the breadth and depth of our research coverage,” Sohn adds.

For Oliver Blackbourn, portfolio manager in the Multi-Asset team at Janus Henderson, AI has long been considered a highly complex area of development, with industry leaders perceived as having technological advantages that would allow them to maintain rapid growth. In his view, the expectation of high earnings growth has been used to justify elevated valuations, making these stocks highly vulnerable to any disappointment.

“Competition always seemed like the biggest threat, but also the hardest to assess for investors. The market’s reaction to a perceived radical shift in the competitive landscape has been fierce. Before U.S. markets opened today, Nasdaq 100 futures had fallen 3.9%, and ASML—one of Europe’s companies most exposed to the AI theme—had dropped more than 10%,” Blackbourn notes.

In his opinion, while it is easy to get ahead of events, it is also important to remember that high expectations have driven up valuations across the U.S. stock market and, consequently, global equities. “If we start to see U.S. stock valuations drop significantly, there is a risk that this will spill over into other high-valuation areas in Europe and Asia.

Similarly, with U.S. consumers more exposed than ever to the stock market, there is a broader risk of negative feedback loops if consumer confidence is shaken. A significant tightening of financial conditions due to stock market losses could quickly change the Federal Reserve’s outlook,” Blackbourn concludes.

We know—the words you’ve probably heard the most last week are Donald Trump. The first week of the 47th U.S. president’s term has been intense, marked by 25 Executive Orders. These range from withdrawing from the Paris Climate Agreement and the World Health Organization to declaring a national emergency on the southern border and an energy emergency. Other areas addressed include tariffs, immigration, and ending federal workers’ remote work policies.

Experts call for caution amid the noise

“So far, he hasn’t enacted any tariffs on imports. It’s unlikely that announcements of new policy measures from the Oval Office—whether they’re implemented or not—will decrease in the short term. Reacting preemptively to these is a losing proposition for investors. At the same time, as shown by the recent tariff threats against Canada and Mexico and the related currency movements, higher financial market volatility is likely to become a permanent feature of the new Trump administration,” notes Yves Bonzon, CIO of Julius Baer.

One of the most attention-grabbing announcements, beyond concerns about tariffs, has been the Stargate initiative, which brings together SoftBank, Oracle, and OpenAI in a joint venture committed to investing $100 billion in early-stage AI. The plan starts with a data center in Texas and aims to reach $500 billion in four years.

According to analysts at Banca March, this initiative boosted the tech sector, especially Microsoft, Nvidia, and Arm, which will build the infrastructure. “For context, it’s estimated that the total investment—regular business and AI deployment—of the four major hyperscalers (Amazon, Meta, Microsoft, and Alphabet) will reach $260 billion in 2025. This shows the ambition and relevance of the announced investments. The new president highlighted the strategic importance of maintaining leadership in AI development, particularly against growing competition from China. However, Elon Musk commented on the social network X that the initiative doesn’t yet have the financial capacity to deploy such a large investment, marking the first public disagreement between Trump and the entrepreneur,” the analysts highlight.

Another Executive Order formally established the Department of Government Efficiency (DOGE).

Although Elon Musk and Vivek Ramaswamy had discussed cutting $2 trillion from the government’s annual $6.8 trillion budget, the text didn’t mention any spending cuts. “Monday’s action shifts the effort away from direct spending cuts and more toward improving efficiency through technological advancements. Ironically, these improvements will likely cost more in the short term (and could require Congressional allocation) even if they save money in the long term. We’ll have to wait to see what DOGE achieves before it expires in mid-2026,” notes Libby Cantrill, Head of Public Policy at PIMCO.

Tariffs and Trade

Everything related to trade and tariffs is drawing the attention of analysts and investors, who undoubtedly see it as a concern. “On trade, we expect Trump to reinstate at least some tariffs on China to the levels implemented during his first term as an immediate first step, with potential for steady increases from there. He could also initiate Section 301 trade investigations into Mexico, Canada, and the EU, which would be a precursor to tariff increases. Ultimately, our baseline trade assumptions incorporate a significant rise in tariffs on China but a more targeted approach by sector and product with other countries, avoiding a global baseline tariff. However, a more expansive use of emergency powers related to trade, including invoking the International Emergency Economic Powers Act (IEEPA), could indicate that trade policy is shifting toward our ‘Trump Unleashed’ scenario,” says Lizzy Galbraith, political economist at abrdn.

In Cantrill’s view, tariffs may not have been raised immediately. “We’d caution against reading too much into what’s more likely a delay rather than an absence of future tariff action. At the same time, we believe widespread tariffs on Mexico and Canada—particularly at the 25% level—are less likely than targeted, country-specific tariffs elsewhere. We still think the EU and China are quite vulnerable.

In the coming days and weeks, as the administration approaches its first 100 days, a flurry of decrees related to immigration, tariffs, and deregulation is expected. These will provide clues about the overall direction of its policy.

U.S. Equities

Meanwhile, the Q4 2024 earnings season in the U.S. started off well and will pick up speed next week. As Bonzon recalls, expectations for S&P 500 earnings in 2025 are ambitious, though “not unattainable,” with limited room for positive earnings surprises. “The risk/reward ratio outlook for the S&P 500 has significantly deteriorated compared to two years ago. After two consecutive years of double-digit returns driven largely by valuation multiple expansion, the index is fully valued, though not excessively,” states the CIO of Julius Baer.

In general, Bonzon notes that analysts currently forecast a year-over-year earnings growth of 14.8% for the S&P 500 in 2025. While this is certainly achievable, it leaves little room for positive surprises. “After two consecutive years of returns driven largely by valuation multiple expansion—resulting in a fully valued, but not overly expensive, index—the burden increasingly falls on earnings to drive returns,” he concludes.

The world is experiencing a new environment marked by a cycle of interest rate cuts by the major central banks in developed markets, as well as in emerging regions. According to experts, over the past quarter, most monetary institutions have adopted a more cautious stance.

The best example of this is the Fed, which has once again shifted its focus to inflation, as economic activity has remained strong while disinflation has stalled. “The Fed maintains its data-dependent approach and is beginning to shift its attention to the labor market. We believe labor market conditions could shape the path of its future policy decisions. Similarly, the Bank of England and the European Central Bank also cut interest rates by 25 basis points in the third quarter of 2024, emphasizing data dependency without precommitting to any specific interest rate trajectory,” explain experts from Capital Group.

According to Invesco in its outlook for this year, rates remain generally restrictive in major economies but are easing. “On the one hand, the Fed is likely to remain neutral by the end of 2025, but improved growth prospects may delay rate cuts. On the other hand, European central banks are easing their policies, with relatively weaker growth than the U.S.,” they note.

Divergences in Monetary Policy

This reality brings us to a key conclusion: yes, we are in a cycle of rate cuts, but there will be noticeable divergences in the monetary policies of the major central banks. In fact, Capital Group believes that this divergence will play a significant role in the coming months.

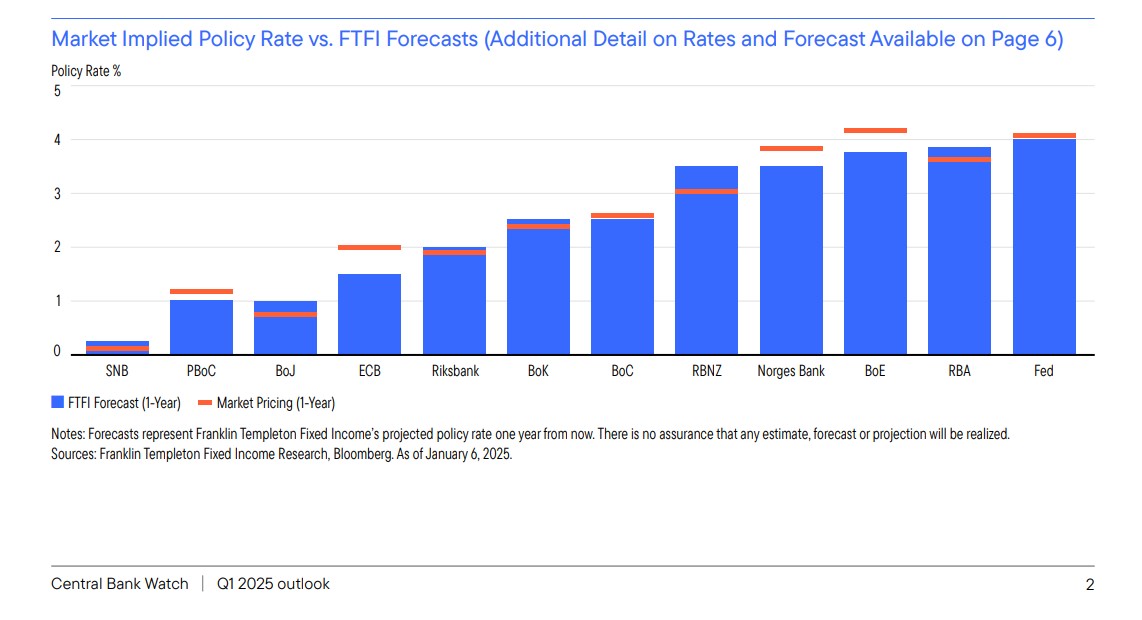

This is reflected in the Central Bank Watch report, prepared by Franklin Templeton, which reviews the activity of G10 central banks, plus two additional countries (China and South Korea), along with their forecasts.

According to the report, the Fed’s shift in strategy has refocused its attention on inflation, as economic activity has remained robust while disinflation has stalled. “The policies of the newly elected president are also likely to influence the Fed’s interest rate projections, which currently only anticipate two cuts in 2025. Across the Atlantic, the European Central Bank and the Bank of England are observing insufficient growth but remain cautious about the future interest rate path, as domestic and geopolitical uncertainties remain high,” the report states.

“Monetary policy divergence is likely to remain a prominent theme in the coming months. The Bank of Japan remains the exception among developed markets, as it has embarked on a rate hike cycle to end an era of negative interest rates. We maintain a relatively cautious stance regarding Japanese rates, as the central bank may make further policy adjustments in response to potential currency pressures. In Europe, the trajectory of monetary easing could depend on the weight policymakers place on downside growth risks compared to the pace and progression of wage pressures and services inflation,” Capital Group experts emphasize.

Another conclusion from the Franklin Templeton report is that “most central banks have become more cautious than they were a quarter ago.” According to their analysis, while the Bank of Canada cut its benchmark rate by 50 basis points in December, this may be its last significant move. “The Riksbank also seems to be taking a more neutral stance, and we believe the Reserve Bank of New Zealand will need to implement fewer cuts than the market currently anticipates. Meanwhile, the Swiss National Bank and the People’s Bank of China remain the most dovish,” the report highlights, noting the behavior of other key monetary institutions.

Lastly, the document underscores that some central banks face a set of dilemmas. “We believe the Norges Bank will lower rates, likely in the first quarter, followed by the Reserve Bank of Australia in the second quarter. Both were among the last to join the easing trend. Meanwhile, the Bank of Japan is expected to continue raising rates gradually in 2025. However, we believe the rigidity of inflation gives the central bank ample room to adopt a more aggressive stance,” the report concludes.

Jupiter Asset Management has announced that the investment team and assets of Origin Asset Management, a global investment boutique based in London, were transferred to Jupiter on January 21, 2025. This integration follows the acquisition announcement made on October 3, 2024.

According to the firm, this addition strengthens its presence in the strategic institutional client channel and enhances its capabilities in emerging market equities, while also expanding its expertise in other multiregional equity strategies. The team, led by Tarlock Randhawa, includes Chris Carter, Nerys Weir, Ben Marsh, and Ruairi Devery-Kavanagh. As noted by Jupiter AM, the team’s solid track record is based on an investment process that combines a quantitative asset selection approach with proprietary algorithms and rigorous qualitative analysis.

Following the announcement, Kiran Nandra, Head of Equities at Jupiter, stated: “Origin is the latest example of Jupiter’s ability to attract highly successful investment talent with strong commercial vision. We aim to expand our investment capabilities to serve a wide range of clients. Last year’s arrival of Adrian Gosden and Chris Morrison, followed by Alex Savvides and his team, significantly strengthened our UK equities expertise. Likewise, we eagerly anticipate the addition this year of the prestigious European equities team comprising Niall Gallagher, Chris Sellers, and Chris Legg.”

For his part, Tarlock Randhawa, who leads the team, added: “We are excited to join Jupiter, where the active and differentiated management philosophy, combined with a strong client focus, is clearly evident. The transition for our clients will be seamless, and we believe they will benefit from Jupiter’s commitment to excellence in client experience.”

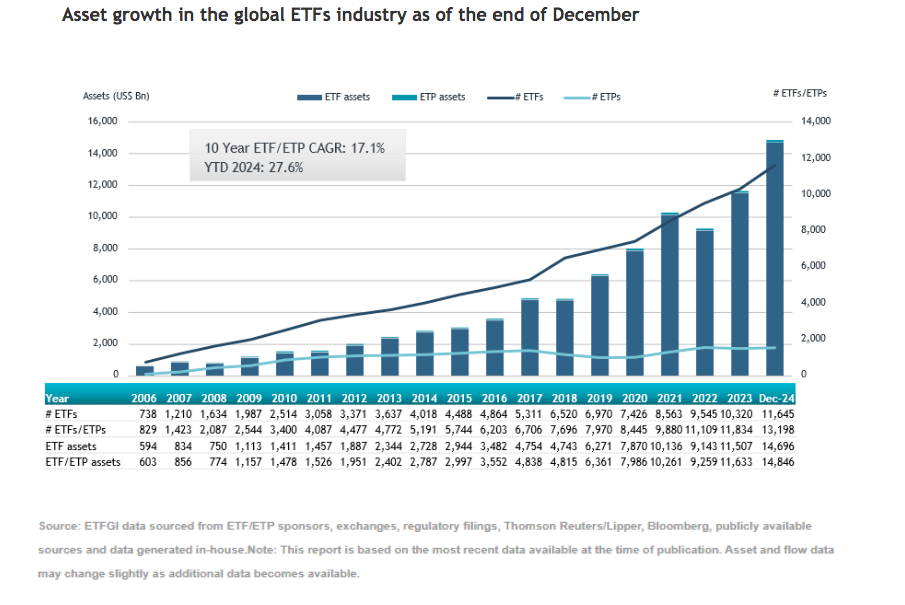

In December, the global ETF industry captured $207.73 billion, raising net inflows for all of 2024 to $1.88 trillion, according to the report by ETFGI. This marks a new record for the sector, surpassing the previous high of $1.29 trillion recorded in 2021 and, of course, exceeding the 2023 total of $974.50 billion.

Additionally, global ETF assets stood at $14.85 trillion in 2024, the second-highest level ever recorded, only below the record of $15.12 trillion in November of the same year. “Assets under management increased by 27.6% in 2024, rising from $11.63 trillion at the end of 2023 to $14.85 trillion at the close of 2024,” notes the latest report by ETFGI.

Regarding the behavior of flows, the ETFGI report shows that out of the $207.73 billion in net inflows, equity ETFs captured $151.58 billion, raising 2024 net inflows to $1.11 trillion, far exceeding the $532.28 billion in 2023. As for fixed income ETFs, these vehicles attracted $16.14 billion in December, bringing 2024 net inflows to $314.32 billion, higher than the $272.90 billion in 2023.

Looking at other asset classes, commodity ETFs reported net outflows of $1.11 billion in December, bringing 2024 net inflows to $3.91 billion, better than the net outflows of $16.88 billion in 2023. Meanwhile, active ETFs attracted net inflows of $41.78 billion in December, bringing 2024 net inflows to $374.30 billion, much higher than the $184.07 billion in net inflows in 2023.

According to Deborah Fuhr, managing partner, founder, and owner of ETFGI, “The S&P 500 index declined 2.38% in December but rose 25.02% in 2024. Developed markets, excluding the U.S. index, declined 2.78% in December but increased 3.81% in 2024. Denmark (down 12.34%) and Australia (down 7.90%) recorded the largest declines among developed markets in December. The emerging markets index increased 0.19% during December and rose 11.96% in 2024. The United Arab Emirates (up 6.42%) and Greece (up 4.21%) recorded the largest increases among emerging markets in December.”

Evolution of Offerings

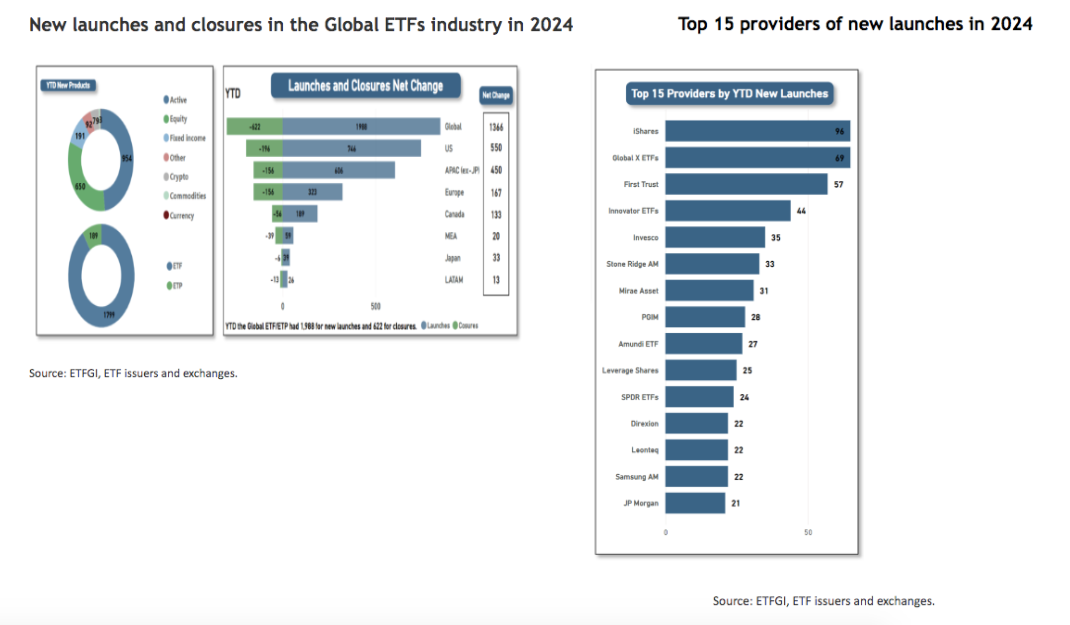

The ETFGI report also highlights that the global ETF industry reached a new milestone with 1,988 new products launched in 2024. It explains that this represents a net increase of 1,366 products after accounting for 622 closures, surpassing the previous record of 1,841 new ETFs launched in 2021.

Specifically, the distribution of new launches in 2024 was as follows: 746 in the United States, 606 in Asia-Pacific (excluding Japan), and 323 in Europe. Additionally, a total of 398 providers contributed to these new launches, which are distributed across 43 exchanges worldwide. Notably, iShares launched the largest number of new products, with 96, followed by Global X ETFs with 69 and First Trust with 57.

“There were 622 closures from 177 providers across 29 exchanges. The United States reported the highest number of closures with 196, followed by Asia-Pacific (excluding Japan) with 156, and Europe also with 156. Among the new launches, there were 954 active products, 650 indexed equity products, and 191 indexed fixed-income products,” noted ETFGI.

Between 2020 and 2024, the global ETF industry experienced significant growth in the number of launches, increasing from 1,131 to 1,988. In 2024, the United States and Asia-Pacific (excluding Japan) recorded the highest number of launches, reaching 746 and 606, respectively, while Latin America had the fewest launches, with only 26. The United States and Canada achieved record numbers of new launches in 2024, with 746 and 189, respectively. Additionally, Asia-Pacific (excluding Japan) achieved its launch record in 2021, with 645; Europe set its record of 434 in 2021; Latin America recorded 41 in 2021; Japan reached 44 in 2023; and the Middle East and Africa achieved 86 in 2020.

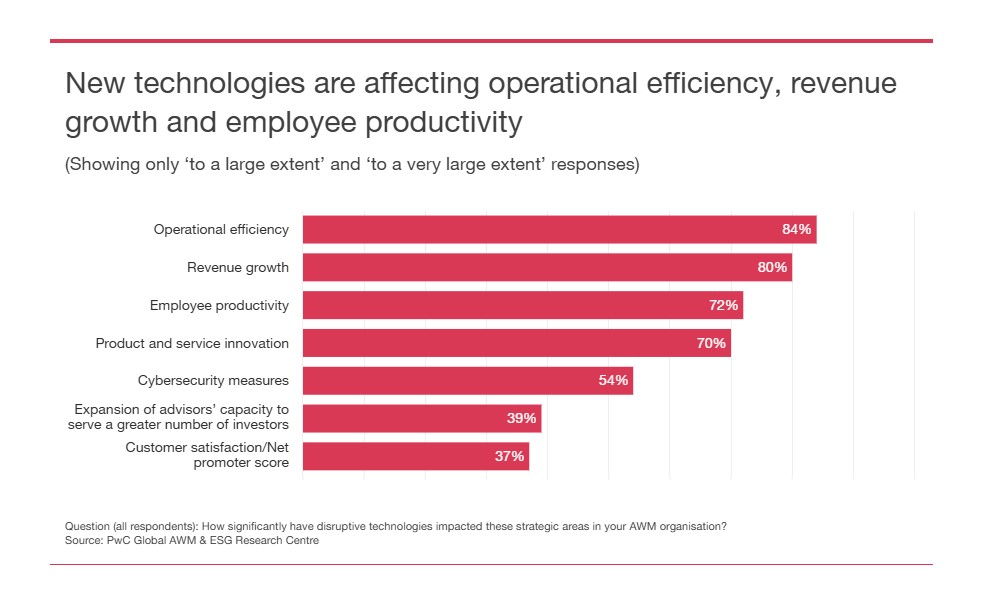

80% of asset management and wealth management firms state that AI will drive revenue growth, while the “technology-as-a-service” model could boost revenues by 12% by 2028, according to the Asset and Wealth Management 2024 report by PwC. A significant finding is that 73% of organizations believe AI will be the most transformative technology in the next two to three years.

The report reveals that 81% of asset managers are considering strategic alliances, consolidations, or mergers and acquisitions (M&A) to enhance their technological capabilities, innovate, expand into new markets, and democratize access to investment products, in a context marked by a significant wealth transfer. According to Albertha Charles, Global Asset & Wealth Management Leader at PwC UK, disruptive technologies, such as artificial intelligence (AI), are transforming the asset and wealth management industry by driving revenue growth, productivity, and efficiency.

“Market players are turning to strategic consolidation and partnerships to build technology-driven ecosystems, eliminate data management silos, and transform their service offerings amid a major wealth transfer, where affluent individuals and younger audiences will play a more significant role in shaping demand for services. To emerge as leaders in this new digital market, asset and wealth management organizations must invest in their technological transformation while ensuring they reskill and upskill their workforces with the necessary digital capabilities to remain competitive and innovative,” explains Charles.

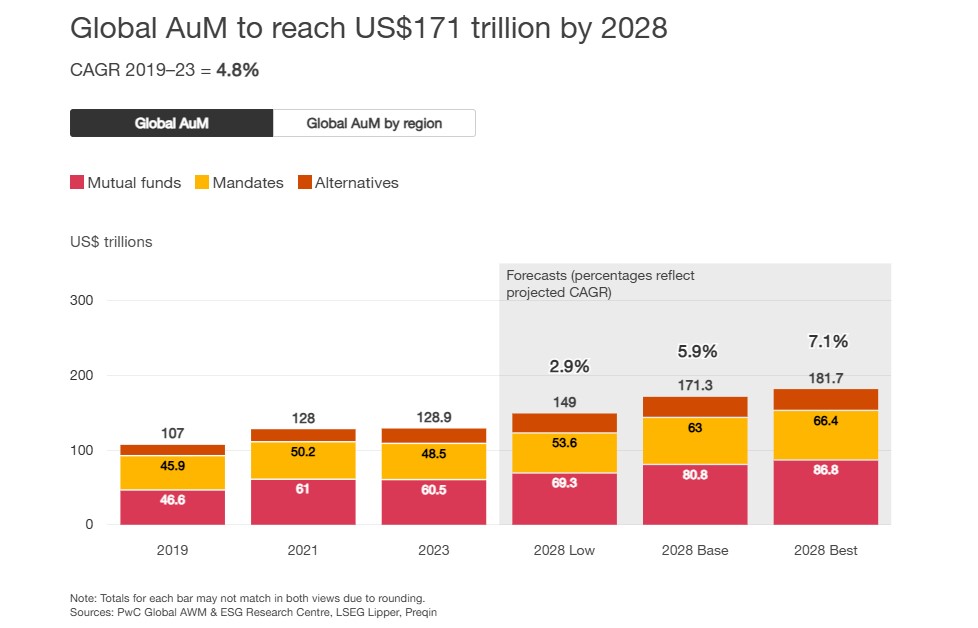

This focus will be critical in addressing an industry whose assets under management are expected to reach $171 trillion by 2028. According to PwC projections, the sector will see a compound annual growth rate (CAGR) of 5.9%, compared to last year’s 5%. Notably, alternative assets stand out, expected to grow even faster with a CAGR of 6.7%, reaching $27.6 trillion during the same period.

“Despite the potential of alternative assets, only 18% of investment firms currently offer emerging asset classes, such as digital assets, though eight out of ten firms that do report an increase in capital inflows,” the report notes in its conclusions.

Key Trends

Taking into account this growth forecast and the role technology will play, PwC’s report identifies several trends. The first is that tokenization stands out as a key opportunity, with tokenized products projected to grow from $40 billion to over $317 billion by 2028, representing a CAGR of 51%.

Tokenization, or fractional ownership, can democratize finance by expanding market offerings and reducing costs. According to PwC, asset managers plan to offer tokenization primarily in private equity (53%), equities (46%), and hedge funds (44%).

Another identified trend is the consolidation and development of technology ecosystems while talent remains the top priority. In this context, 30% of asset managers report facing a lack of relevant skills and talent, while 73% see mergers and acquisitions as a key driver for accessing specialized talent in the coming years.

“The conclusions of this report highlight the urgent need for asset managers and firms to rethink their investment strategies. Their long-term viability will depend on a radical, fundamental, and ongoing reinvestment in how they create and deliver value. Strategic alliances and consolidation will play a vital role in creating technology ecosystems that facilitate greater exchange of ideas and knowledge. Smaller players will be able to modernize their systems quickly and cost-effectively, while larger players will gain access to critical talent and information for growth, particularly as new and emerging technologies like AI transform the investment management landscape,” says Albertha Charles, Global Asset & Wealth Management Leader at PwC UK.

To prepare the report, 264 asset managers and 257 institutional investors from 28 countries and territories were surveyed.

Celeste Boadas Joined Raymond James for Its Private Wealth Management Division in Coral Gables.

Boadas joins as a Client Service Associate “with a dedication to excellence in customer service and a passion for fostering meaningful relationships,” says the firm’s statement.

With experience in the international insurance industry since 2016, she comes from Insigneo, where she held customer service roles between 2020 and 2024.

She holds a Bachelor’s degree in Fine Arts from the Art Institutes and an MBA in Strategic Business Management from ADEN Business School, with a specialization from George Washington University. Celeste has earned the SIE and Series 7 designations, “underscoring her commitment to professional growth and excellence,” adds the firm’s statement.

“Celeste assists clients by addressing their needs and inquiries regarding investment accounts with professionalism and efficiency. She also plays a key role in onboarding and managing client relationships, ensuring that every interaction is seamless and enriching. Her personal and detail-oriented approach sets her apart, allowing her to build trust and deliver personalized solutions,” the statement continues.

The advisor, originally from Venezuela, is an active member of the Body & Brain community and a certified sound healing practitioner in Miami.

Additionally, she volunteers in programs that promote balance and personal growth through body and mind practices. In her free time, she enjoys wellness activities that reflect her holistic approach to life and work, the statement concludes.