Héctor Contreras, an international client advisor at Morgan Stanley, has joined the firm’s Century Club, as announced by Contreras, who is based in Houston, in a post on his LinkedIn profile.

“I am very proud to announce that I have been named a member of the prestigious Century Club of Morgan Stanley, an exclusive group of the firm’s financial advisors,” Contreras wrote on the professional networking platform. “I appreciate this recognition of my dedication to providing first-class service to my clients,” he added. Less than a month ago, he was promoted to Senior Vice President at the investment bank, where he has worked since 2014.

The Century Club of Morgan Stanley is an exclusive group of financial advisors. To become a member, advisors must meet certain criteria for performance, conduct, compliance, revenue, experience, and assets under supervision.

Before joining Morgan Stanley, Contreras—a graduate of the Instituto Tecnológico y de Estudios Superiores de Monterrey—worked as an advisor at Citi, Chase, and Merrill Lynch.

HSBC has added 30 years of experience to its wealth management business with the addition of Arturo Montemayor.

The advisor, who was registered in BrokerCheck on February 4, joins from Merrill Lynch, where he had been working since September 2021.

Montemayor, a well-known figure in Miami’s industry, has worked at major banks throughout his career.

He began his career at Citi in 1984 for the Mexico office, initially in corporate banking and real estate before moving into private banking. In 2005, he joined Deutsche Bank in Geneva and later in Miami, according to his LinkedIn profile.

He then held positions at the wirehouses Morgan Stanley and JP Morgan, alternating between Miami and New York while working with Latin American clients.

He is an industrial engineer and holds an MBA from the Instituto Tecnológico Autónomo de México.

The adoption of generative artificial intelligence in the banking sector will experience exponential growth, according to the IBM Institute for Business Value 2025 Outlook for Banking and Financial Markets.

In 2024, 8% of banks systematically developed the technology, while 78% used it tactically. Additionally, the report indicates that more institutions are moving from pilot projects to broader execution strategies. This includes the implementation of agentic AI to improve operational efficiency and customer experience.

Furthermore, banking convergence continues to be a key factor in financial performance, the report adds. The restructuring of business models and processes will be crucial in distinguishing the most competitive banks from the rest.

In this context, 60% of surveyed CEOs believe that accepting a certain level of risk is necessary to leverage the benefits of automation and strengthen their market position.

Another key aspect highlighted in the report is the evolution of customer behavior. More than 16% of consumers globally are already comfortable with fully digital banks that have no physical branches. However, competition is shifting toward higher-value services, such as embedded finance and advisory services for high-net-worth clients and small and medium-sized enterprises (SMEs).

The report also includes an analysis of industry leaders’ sentiment, customer behavior, and economic data from eight key markets: the United States, Canada, the European Union, the United Kingdom, Japan, China, and India. The findings will help financial institutions and their ecosystem partners anticipate the trends shaping the future of the sector.

For more information and access to the full report, please visit the following link.

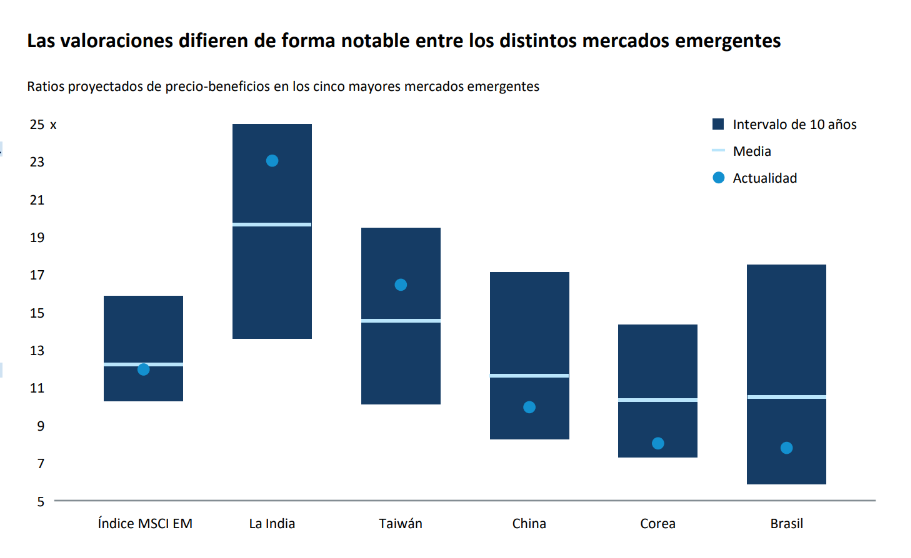

The new Donald Trump administration brings uncertainty to emerging markets. However, investment firms believe it is essential to look beyond this and remember that these regions have stronger markets and that the Federal Reserve‘s monetary policy continues to favor risk assets.

According to Kirstie Spence, portfolio manager at Capital Group, many of the major emerging markets can leverage various tools: higher reserve volumes, positive real interest rates with room to decline, fewer imbalances than developed markets, and exchange rates that are fairly valued or undervalued.

“They have policy flexibility to weather the storm if needed. Except for the less consolidated economies, external balances are solid. Additionally, inflation is trending downward in a restrictive monetary policy environment. Fiscal indicators are often a weak point for these markets, but most major emerging markets have extended their debt maturity profile and are now issuing more in local currency,” argues Spence.

She also notes that a Federal Reserve less inclined to cut rates could put pressure on central banks in less developed emerging economies, making it difficult for them to maintain higher interest rates, especially in countries concerned about inflation and financial stability risks. “In more developed emerging markets, particularly in the Asian region, central banks have shown greater confidence in getting ahead of the Federal Reserve, given the absence of systemic pressures on financial systems and the development of deeper, more liquid domestic markets,” she adds.

According to Claudia Calich, Global Head of Emerging Debt at M&G, it is interesting to analyze that the disinflation story in emerging markets is practically complete, with few exceptions in high-inflation countries such as Argentina, Turkey, Egypt, and Nigeria. “It is remarkable how poorly Latin America performed in 2024, affected by both currency depreciation and rising yields. There is much less room for rate cuts, given the expected inflation path in most inflation-targeting economies. However, there is potential for a yield rebound if country-specific concerns ease, such as improved fiscal prospects in Brazil or greater clarity on trade between the U.S. and Mexico, and if currencies stabilize or recover some of the depreciation seen in 2024,” says Calich.

Implications for Investors

Given this backdrop, asset managers are looking for investment opportunities in emerging markets, with debt being one of the most analyzed areas. According to M&G’s expert, local currency bonds in emerging markets remain underappreciated, which could be a good signal for contrarian investors willing to step in and endure some volatility. “However, high short-term interest rates in key markets like the U.S., U.K., and, to a lesser extent, the Eurozone, remain a hurdle for this asset class, and global macroeconomic uncertainty doesn’t help. Local currency bonds in emerging markets still face strong competition from high short-term rates in the U.S., U.K., and Eurozone. This could improve in the future as central banks continue easing, but the risk of ‘higher for longer’ rates remains, especially if U.S. inflation expectations deteriorate due to tariffs,” she explains.

Additionally, M&G acknowledges that they remain selectively constructive on emerging market currencies, as their valuations have become even more attractive after last year’s sell-off. “However, timing the right moment to act is complex, as the fate of the U.S. dollar will largely depend on the policy mix adopted by the new administration,” Calich notes.

The Heavyweights

When discussing investment opportunities, Chris Thomsen, portfolio manager at Capital Group, highlights two “heavyweights”: India and China. In his view, both emerging markets have followed very different trajectories over the past five years, with Indian equities significantly outperforming Chinese equities.

“Valuations reflect these differences. While both markets offer attractive opportunities, they come with their own risks and investment drivers. The increasing penetration of mobile phones among India’s young and vast population has benefited telecom companies like Bharti Airtel, but the high valuation levels make selectivity crucial,” explains Thomsen.

On the other hand, he points out that China’s massive domestic consumer market could be boosted by government stimulus measures, creating opportunities for well-positioned digital companies. “Some companies like Tencent and NetEase hold dominant positions, have strong cash flows, and high-quality management teams. However, investing in China remains risky due to ongoing tensions with the U.S. and the trade priorities of the new Trump administration,” says the Capital Group manager, adding that the reconfiguration of global supply chains presents opportunities in Brazil, Mexico, and Indonesia.

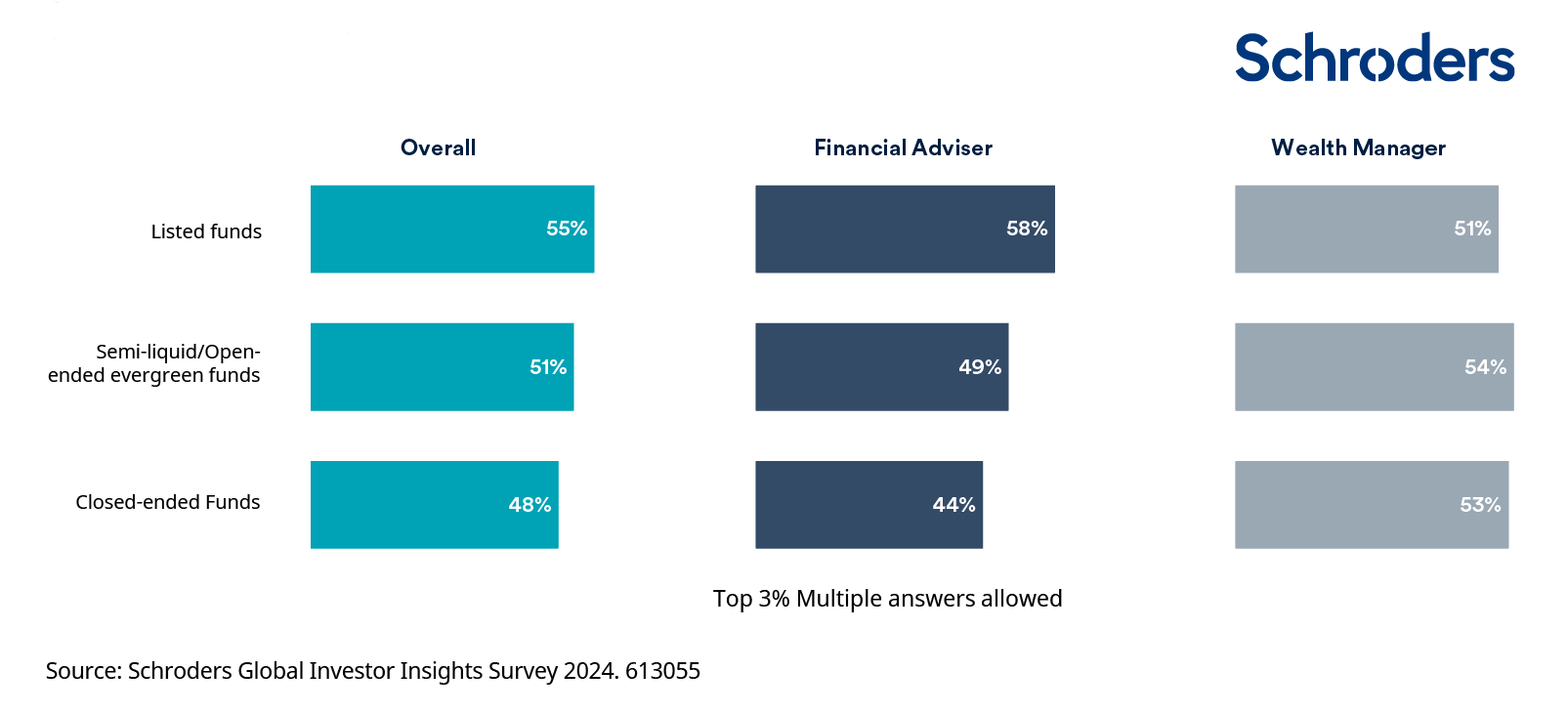

The increasing allocation to private markets in response to market evolution by wealth managers and financial advisors is a clear trend in the industry. In fact, according to the Global Investor Insights Survey (GIIS) by Schroders, more than half of these professionals are currently investing in private markets, with an additional 20% expecting to do so within the next two years.

The survey, which includes 1,755 wealth managers and financial advisors globally—representing $12.1 trillion in assets—reveals that private equity (53%), private multi-asset solutions (47%), and renewable infrastructure equity (46%) are the top three private market asset classes where advisors and wealth managers expect their clients to increase allocations in the next 1-2 years.

Regarding how they expect client allocations to private market asset classes to change over the next 1-2 years, two-thirds of wealth managers and financial advisors highlight the potential for higher returns compared to public markets as the primary benefit of private market investing for their clients. This was closely followed by the ability to achieve diversification through different return drivers (62%). Additionally, on average, most investor allocations to private markets represent between 5%-10% or 1%-5% of their total portfolio exposure.

According to Carla Bergareche, Global Head of Wealth Management at Schroders’ Client Group, while many wealth managers and financial advisors are already investing in private markets on behalf of their clients, allocation sizes remain significantly lower than the 20% or more seen in family office and institutional investor portfolios.

“This gap represents a significant opportunity to strengthen client engagement with private markets. We therefore expect these markets to play an increasingly important role in wealth investment portfolios as investors become more aware of the potential for strong and diversified returns,” explains Bergareche.

Access to Private Market Investments

Another key finding is that just over half of surveyed wealth managers and advisors indicated that they access private market opportunities through exchange-traded funds, closely followed by semi-liquid or open-ended indefinite-duration funds (51%). Despite these opportunities, lack of liquidity is cited as the main challenge when discussing private markets with clients.

According to Schroders, 49% of respondents stated that greater financial education for clients would help drive demand, followed by better-suited product structures (42%) and lower investment minimums (42%).

“There is no doubt that private wealth will play a very significant role in private markets in the future. Until now, wealth managers and advisors have had limited options to access these markets compared to their institutional counterparts, which explains why, despite their intent, we still see relatively low allocations,” says Tim Boole, Head of Private Equity Product Management at Schroders Capital.

However, in his experience, the emergence of new vehicles, such as semi-liquid funds, has expanded available access points, representing a significant advancement in providing greater flexibility for investors to achieve their financial goals through private markets. “It’s no surprise that these structures are favored by this client segment,” Boole adds.

Wealth Transfer as a Key Priority

Additionally, the firm highlights that wealth transfer has been identified as a priority for 59% of wealth managers and financial advisors worldwide. In North America, 66% consider it a priority, compared to 57% in the UK, 57% in Asia-Pacific, and 58% in EMEA.

The report shows that wealth transfer discussions are more deeply embedded in the Americas. Specifically, Latin America has the highest level of engagement globally, with 58% of advisors stating they have addressed this topic with more than half of their clients. In EMEA and Asia-Pacific, participation is lower, with 43% and 46% of advisors engaging in these discussions, primarily due to cultural sensitivities.

After a few weeks of intense market reactions to Donald Trump’s statements, investors have shown they can tolerate the volatility his words generate. “Throughout the week, the market has focused more on the positives than the negatives. In all cases, it seems that the parties have given themselves time to negotiate—the new Chinese tariffs will take effect on February 10—allowing stock markets to resume their upward trend on Tuesday. Additionally, inflation fears remain under control, which has strengthened fixed-income markets, especially longer-duration bonds,” analysts at Banca March noted.

For Yves Bonzon, CIO of Julius Baer, the U.S. stock market no longer fears potential tariffs, seeing them merely as a negotiation tool for Trump to extract benefits from the involved governments. “We now know that the president views the stock market as one of the best indicators of his policy success. He cannot ignore the consequences of imposing tariffs of this magnitude on U.S.-Mexico-Canada Agreement partners. If we add trade with Mexico and China, which currently faces 10% tariffs, nearly half of U.S. imports are now subject to these new levies,” explains Bonzon.

This perspective aligns with the views of Samy Chaar, Chief Economist and CIO Switzerland at Lombard Odier, and Luca Bindelli, Head of Investment Strategy at the firm: “Trump’s White House is deeply challenging the post-1945 global order, but for now, policy initiatives are mostly aligned with campaign rhetoric. As a result, our baseline expectations for the U.S. economy and markets remain unchanged.”

Experts at EDM also note that despite macroeconomic and political uncertainties, equity investors have remained optimistic, pushing stock prices higher (S&P 500 +4.0%; MSCI World +3.6%). “However, gains are starting to be more diversified than in 2024, which was characterized by a strong concentration in tech-driven returns. Bond markets are seeing rising yields due to higher medium- and long-term inflation expectations, fueled by negative price adjustments. There is no doubt that concerns over the growing U.S. debt are behind this increased demand for higher returns,” EDM stated in its latest report.

Market Outlook

According to MFS IM, global equity markets have not yet fully priced in significant downside risks. The firm argues that, in general, tariffs—if implemented as currently expected—will negatively impact stocks, primarily reflecting concerns about a combination of slower global growth and higher interest rates. “This is evident in price action, or how stock prices reacted immediately after the U.S. announcement,” they explain. However, MFS IM emphasizes that when assessing broader market implications, it is crucial to differentiate between companies based on their export exposure.

Conversely, in fixed-income markets, MFS IM believes the risk of a trade war had already been fully priced into global bond markets. “One of the most pronounced transmission channels has been the currency markets, with the Canadian dollar and Mexican peso suffering sharp losses against the U.S. dollar. Both currencies have since recovered due to negotiations that delayed tariff implementation,” they acknowledge.

Regarding U.S. fixed income, MFS IM believes this latest development will likely further constrain the Federal Reserve’s ability to ease policy in the future, given the potential impact of a one-off price adjustment on domestic inflation. “As a result, initial interest rates are likely to rise, triggering some flattening of the yield curve,” they indicate.

For Connor Fitzgerald and Schuyler Reece, fixed-income portfolio managers at Wellington Management, during times of market uncertainty, investors tend to flock to safe-haven assets, causing demand for U.S. Treasury bonds to surge. “We believe the best time to consider Treasuries is before volatility hits. If fixed-income portfolios already contain U.S. Treasuries when negative market events occur, investors can dynamically rotate their allocations, anticipating the shift from credit to Treasuries, and execute transactions at potentially more attractive levels on both sides of the trade,” they argue.

Chaar adds: “We expect 10-year Treasury yields to settle around 4.5% over the next 12 months, suggesting limited pressure on equity valuations. We maintain our preference for corporate bonds, which should offer higher yields than government bonds for comparable maturities. In fact, U.S. corporate bonds should still benefit from a likely pro-growth agenda in the U.S. (through deregulation and tax cuts) and relatively stable spreads, whereas government bonds may continue to face challenges due to rising budget deficits and refinancing needs, increasing yield volatility.”

Flexible Portfolios

From a portfolio management perspective, the current situation underscores the importance of remaining flexible and maintaining composure in the face of volatility, as such periods are often accompanied by excessive noise and fluctuating headlines. “While we remain attentive to news flows, we do not believe current market movements have created opportunities for significant changes in our asset allocation,” states Felipe Villarroel, portfolio manager at TwentyFour AM (a Vontobel boutique).

Regarding long-term implications, Villarroel believes it is too early to determine how the balance of power will shift under Trump’s administration. “That said, we believe U.S. exceptionalism and its enduring status as a safe-haven asset and recipient of foreign capital are partly due to the predictability of its policies. Today, market sentiment on this has not changed, but there may come a point where investors start feeling uneasy. These characteristics are also factored into credit rating agencies’ assessments and influence the ongoing evaluation of a country’s AAA rating. We doubt rating agencies will react to Trump’s initial salvos; however, if tariffs remained in place, GDP growth assumptions would change, potentially triggering a review,” Villarroel concludes.

GAM Investments has announced the addition of three professionals from the European equity team at Janus Henderson Investors. According to the asset manager, “these strategic hires reinforce GAM’s commitment to providing clients with access to the highest quality in investment, along with exceptional results.”

The team will be led by Tom O’Hara, alongside Jamie Ross and David Barker, also from Janus Henderson. The three bring extensive experience, having managed over 6.5 billion euros in European equity funds for institutional and retail clients worldwide. According to the firm, these professionals will join GAM in the coming months.

Following the announcement, Tom O’Hara stated: “For decades, GAM has attracted some of the best talent in the industry for the benefit of its clients. Its strong track record in European equities has directly shaped my approach to investing. I take on this new challenge with pride and look forward to contributing to GAM’s sustainable long-term growth.”

Meanwhile, Elmar Zumbuehl, CEO of GAM Group, commented: “We are delighted to welcome Tom, Jamie, and David to GAM. We are confident that their extensive experience and proven investment success will be a valuable asset to our firm. Attracting such outstanding investment professionals highlights GAM’s distinctive and appealing culture, our strategy, and our long-term commitment.”

After a pause in December, gold reached new all-time highs, outperforming all other asset classes in 2024. This upward trend has continued in 2025, and by the end of January, gold had broken its own records, reaching $2,798.40 per ounce. According to experts, this strong performance is driven by its demand as a safe-haven asset amid geopolitical uncertainties and concerns about the impact of tariffs imposed by Donald Trump’s administration on the global economy.

“Global gold demand was much stronger toward the end of last year than available data suggested. The World Gold Council’s demand trends for the fourth quarter of 2024 showed strong growth in investment demand and central bank purchases, which further reinforced bullish sentiment in the gold market and pushed prices to a new all-time high,” explains Carsten Menke, Head of Next Generation Research at Julius Baer.

According to Ned Naylor-Leyland, investment manager for gold and silver at Jupiter AM, the gold market is currently in a bull phase, but the broader market has not yet fully participated, which suggests there is still room for further gains. He notes that gold mining companies have increased production and profit margins, but their stock prices have not risen at the same pace.

The Impact of Tariffs

According to Menke, global gold trade between the U.S. futures market and European physical markets could be affected by the tariffs Trump has threatened to impose. “This is creating uncertainty among gold traders and widening the price gap between New York and London. In theory, tariffs—if implemented—should not alter the long-term supply and demand balance in the global gold market or international benchmark prices. That said, if market imbalances arise in the short term due to tariffs, prices will need to signal the need to attract sufficient supplies to the U.S.,” he explains.

In this regard, Menke argues that the fundamental impact on global gold demand would be more related to prolonged trade tensions, which could be one of the bullish factors of Trump’s presidency. “Overall, we believe his administration could generate a wide range of possible outcomes, both bullish and bearish. Our outlook on gold remains positive, primarily based on the resumption of central bank purchases rather than Trump’s presidency,” he clarifies.

The Role of Central Banks

Another key factor supporting gold’s rally is that several major central banks, including the European Central Bank, the Bank of Canada, and Sweden’s Riksbank, are implementing interest rate cuts, increasing gold’s appeal. Although the Federal Reserve decided to keep rates unchanged, investors anticipate two additional rate cuts this year, which could also support the metal’s price.

“Countries like China, India, and Turkey have increased their gold reserves to diversify assets at the expense of the U.S. dollar. Globally, central banks purchased 694 tons of gold in the first few months of the year; in November, the People’s Bank of China announced it would resume gold purchases after a six-month pause,” notes Diego Franzin, Head of Portfolio Strategies at Plenisfer Investments, part of Generali Investments.

According to Franzin, monetary policy decisions also play a crucial role in the gold market. “During the phase of rising interest rates, gold was the ultimate hedge against inflation, which monetary policies were fighting. In the current phase of rate cuts, gold continues to offer an alternative to other asset classes, although the cost-benefit ratio of holding gold has increased. Gold prices saw a slight dip after the Fed’s rate cut in December. However, it is worth noting that the U.S. central bank also indicated that next year’s rate cuts would be slower than previously expected,” he states.

Outlook

Considering these factors, some experts, such as Franzin, estimate that gold could reach $3,000 per ounce, supported by the continuation of the aforementioned trends and a potential resurgence of inflation driven by fiscal and trade policies under the new Trump administration. “There are also expectations of another increase in U.S. public debt,” he adds.

“Beyond central bank purchases, gold market demand has been largely driven by sophisticated investors, such as hedge funds and algorithmic traders, who have pushed gold futures higher,” adds the Jupiter AM manager.

At Plenisfer Investments, they believe that regardless of short-term price trends, gold will continue to play several key roles in an investment portfolio in 2025. *”It will remain a strong diversification element, helping to reduce portfolio volatility due to its low correlation with other assets. It will continue to offer protection against inflation, which historically occurs in waves and could persist, particularly in the U.S., above the levels currently expected by markets.

Lastly, it will remain a safe-haven asset in times of economic or geopolitical uncertainty,” concludes Franzin.

One of the key recommendations made by international asset managers at the beginning of the year was the need to filter out the noise surrounding Donald Trump‘s approach to policymaking. The trade war launched by his administration, which has put the word “tariff” in most headlines since yesterday, is a clear example of why investment firms gave that advice.

If we look at the latest developments, China has imposed tariffs on U.S. products set to take effect on February 10. Specifically, it has announced a 15% tariff on coal and liquefied gas and a 10% tariff on oil, agricultural machinery, high-displacement cars, and pickup trucks. Canada’s response was similar, with Prime Minister Justin Trudeau announcing 25% tariffs on U.S. products. Meanwhile, after a “friendly” phone call with Claudia Sheinbaum, president of Mexico, Trump has decided to pause the 25% tariffs on the country for a month in exchange for a series of commitments on border and trade security.

Time to Negotiate?

According to experts, this first move in the trade war by all parties confirms what many had anticipated: tariffs will be used as a bargaining tool. “As we predicted, Trump is starting his term by using trade policy decisions as a shock weapon within a broader framework of future negotiations, allowing him to partially rebalance trade with some economies. We already saw this tactic during the NAFTA renegotiation when Trump’s threats to withdraw from the trade alliance successfully pressured for a new agreement,” state analysts at Banca March.

Experts at the firm believe that China, having already experienced a trade war, is less inclined to give in to such pressure. Trump is now expected to speak with Chinese President Xi Jinping in the coming days, raising hopes that both leaders may reach an agreement to avoid a new trade war.

For Damian McIntyre, Head of Multi-Asset Solutions at Federated Hermes, these announcements signal to the world that Trump is willing and able to use tariffs as a tool. “While this could ultimately be a negotiation tactic, it has the potential to reshape global investment narratives, including the need for higher risk premiums for countries he perceives as unfair players. Whether it’s tariffs and geopolitical tensions or AI and profits, investors face many risks in today’s market. We believe that investing in a globally diversified range of assets is one way for investors to maintain strong and resilient portfolios,” says McIntyre.

In this context, asset managers are focusing on the imbalances in public accounts and their impact on national economies. “Contrary to what Trump’s rhetoric suggests, it is not the exporting countries that pay the tariffs. U.S. importing companies pay these tariffs to the Treasury. Mechanically, the first impact will be on U.S. companies. For the end consumer, an increase in customs duties has a macroeconomic effect similar to that of a tax hike. It has a temporary impact on inflation and a downward effect on demand, which tends to push prices lower. The main risk, therefore, is a demand-driven growth shock rather than an inflation shock,” explains Enguerrand Artaz, analyst at La Financière de l’Échiquier.

“Trump knows that an open trade war would mean higher inflation for the average U.S. citizen, something he will likely want to avoid in the end. Meanwhile, we must get used to a more volatile 2025 than the previous year, where risk assets, particularly fixed income, will continue to offer attractive entry opportunities,” say analysts at Banca March.

Market Reactions

The first two days following these announcements have also provided insight into how markets are digesting the possibility of a new trade war. According to Robeco, the swift execution of Trump’s tariff threats surprised markets, causing volatility in equities, while safe-haven assets like gold and the dollar surged. “After Trump abruptly withdrew his threat of general tariffs on Colombia earlier last week following a migrant deportation deal, the market was convinced that Trump’s bite would be softer than his bark,” says Peter van der Welle, Strategist for Sustainable Multi-Asset Solutions at Robeco.

Van der Welle believes that the latest tariff announcements on Canada and Mexico show that Trump’s bite is primarily tied to his willingness to seal a border security deal and achieve his political goal of restricting migration. “With markets now forced to guess Trump’s next trade policy moves, U.S. trade policy uncertainty has reached its highest level in 40 years, except for the summer of 2019, when the U.S.-China trade war was at its peak. We expect market volatility to remain high in the short term, reflecting a significant risk of another major trade announcement targeting China, Europe, and/or Japan,” he notes.

Key Takeaways for Investors

Michael Medeiros, macroeconomic strategist at Wellington Management, believes that the most important factor for investors to consider in this situation is the increased likelihood of higher inflation volatility, a lower probability of supply-side improvements in the economy, and the significant link between tariff revenues and tax cuts through budget reconciliation. “These tariffs represent Trump delivering on his campaign promises. He is doing what he said he would do, and that is another key factor to keep in mind,” says Medeiros.

Economists at BofA agree that using tariffs as a bargaining tool has increased trade policy uncertainty and expect this trend to continue. “For markets, we see three key takeaways: the U.S. administration is transactional—nothing is final until it’s signed; U.S. economic policy threats should be taken seriously and literally; and the U.S. ‘bailout’ policy may be further from financial relief than the market expects. Investors have suggested that the stock market serves as the U.S. administration’s performance marker and that any policy shift affecting risk assets will be quickly reversed. We advise caution,” they state in their latest report.

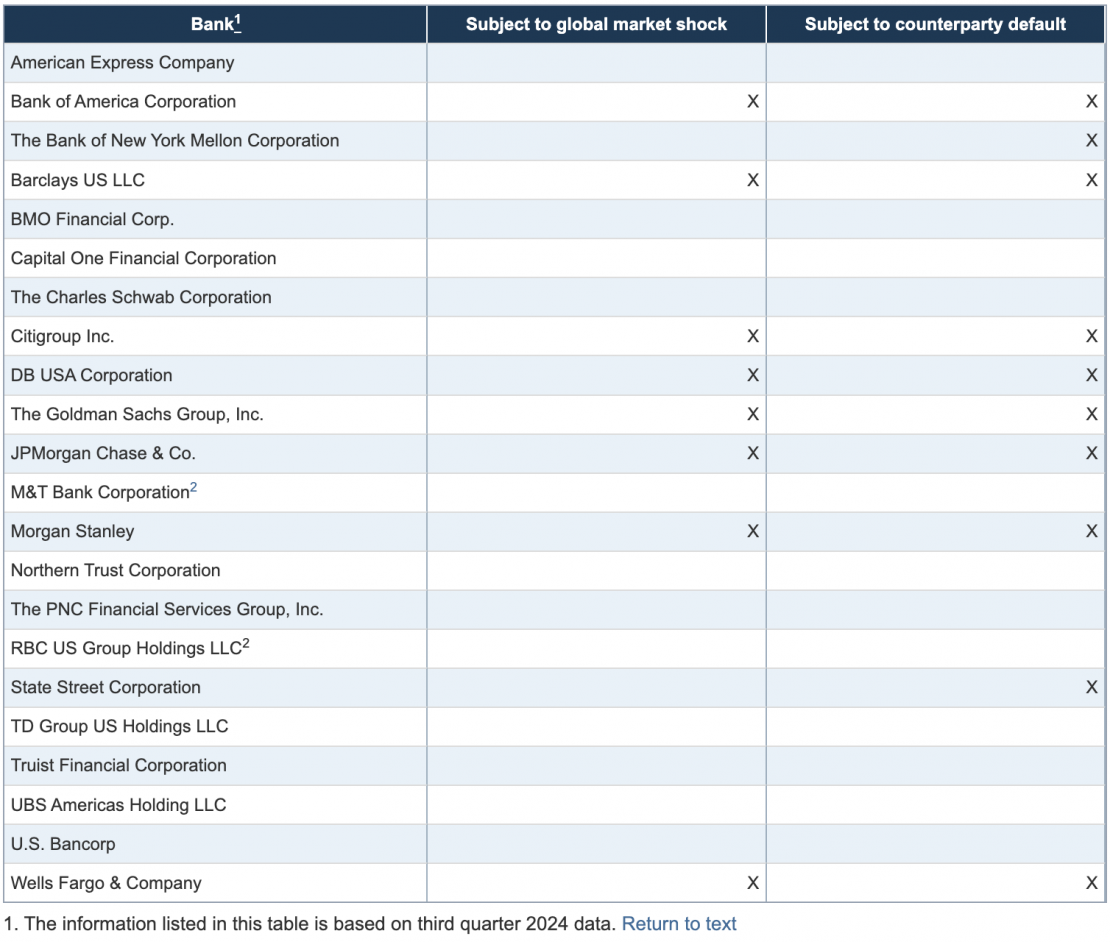

On Wednesday, the Fed published the hypothetical scenarios for its annual stress test, in which 22 banks will be tested against a severe global recession, increased strain in commercial and residential real estate markets, and corporate debt market stress, according to a statement.

While the scenarios are not forecasts and should not be interpreted as predictions of future economic conditions, the test incorporates various macroeconomic data points.

For example, the test assumes that the U.S. unemployment rate rises by nearly 5.9 percentage points, reaching a peak of 10%. This increase in unemployment is accompanied by high market volatility, widening corporate bond spreads, and a sharp decline in asset prices, including an approximate 33% drop in home prices and a 30% decline in commercial real estate prices, according to the Fed‘s statement.

Additionally, “large banks with significant trading or custody operations are also required to incorporate a counterparty default scenario component to estimate potential losses from the unexpected default of the firm’s largest counterparty amid a severe market disruption.” Meanwhile, banks with major trading operations will undergo a test featuring a global market shock component, primarily affecting their trading positions and related activities.

The following table outlines the components of the annual stress test applied to each bank, based on data from the third quarter of 2024:

This year’s exploratory analysis includes two separate hypothetical elements designed to evaluate the banking system’s resilience to a broader range of risks. One element examines how banks would respond to credit and liquidity disruptions in the non-bank financial institution sector during a severe global recession.

The second component of the exploratory analysis involves a market shock scenario that will apply only to the largest and most complex banks. This scenario hypothesizes the failure of five major hedge funds, combined with a decline in global economic activity and rising inflation.

Unlike the stress test, the exploratory analysis is designed to assess additional hypothetical risks to the banking system as a whole, rather than focusing on the specific outcomes for each individual bank. The Fed will publish aggregated results from the exploratory analysis alongside the annual stress test results in June 2025.

The Fed plans to take steps soon to reduce the volatility of stress test results and begin improving the transparency of the models used in the 2025 tests. Additionally, the Fed intends to initiate a public comment process this year regarding its comprehensive changes to the stress testing framework.

The annual stress test evaluates the resilience of large banks by estimating their losses, net income, and capital levels—which serve as a buffer against losses—under hypothetical recession scenarios that extend two years into the future.