How to Succeed in the Advisory Business by 2040

| For Gabriela Huerta | 0 Comentarios

According to Boston Consulting Group (BCG), “the wealth management industry is over 200 years old. Yet for most of that history, providers have operated according to the same general playbook. It took the massive digital and regulatory disruption of the past 20 years to begin shaking up industry business models, and evidence suggests that most providers have moved slowly, with many still adhering to traditional ways of private banking.”

Wealth managers must take action on multiple fronts in order to navigate ongoing market volatility and build fresh capabilities that will enable them to create sustainable competitive advantage over the next decade, according to a new report by BCG, titled Global Wealth 2020: The Future of Wealth Management—A CEO Agenda.

BCG’s 20th annual study of global wealth management takes a 20-20 view of the industry, looking back over the past two decades as well as ahead to 2040. Its review of global market sizing, which encompasses 97 markets, provides a detailed retrospective on wealth growth over the past 20 years—and its resilience through downturns—and evaluates the potential long-term impact of the COVID-19 crisis.

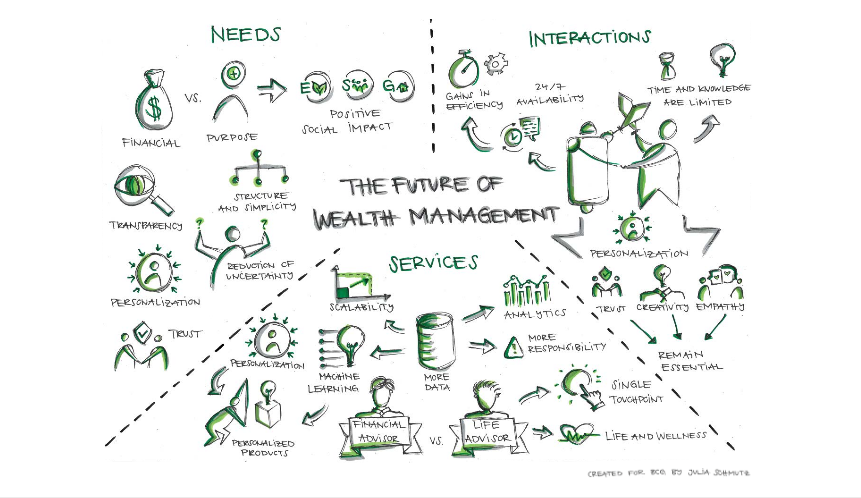

BCG has also created a vision for the future of wealth management, examining how the industry’s value proposition and offerings will change over the next two decades, how forms of interaction will evolve, and which new business models will emerge. Finally, BCG offers wealth management CEOs a comprehensive agenda for protecting the bottom line, prioritizing the areas in which they hope to win in the future, and building appropriate supporting capabilities.

“Effectively serving the world’s wealthy is going to get far more complex in the years ahead,” said Anna Zakrzewski, a BCG managing director and partner, coauthor of the report, and global leader of the firm’s wealth management segment. “As the demographics of wealth shift, so will the needs and expectations of wealth clients. With all the choices available, clients don’t necessarily want more—they want better. In addition, the disruptive forces that emerged at the beginning of the century are accelerating. And as digitization lowers barriers to entry to wealth management as a business, competition will intensify and offerings that once provided differentiation will face commoditization.”

Global Wealth Growth. According to the report, a striking feature of wealth growth over the past two decades has been its extraordinary resilience. Despite multiple crises, wealth growth has been stubbornly robust, strongly recovering from even the most severe tests. Today, more wealth is in more hands, and the wealth gap that separated mature markets and growth markets at the beginning of the century has narrowed dramatically. Globally, personal financial wealth has nearly tripled over the past 20 years, rising from $80 trillion in 1999 to $226 trillion at the end of 2019.

The CEO Agenda. In the report, BCG outlines three potential scenarios for post-COVID-19 growth: “quick rebound,” “slow recovery,” and “lasting damage.” Regardless of which scenario emerges, wealth management providers are likely to face more pressure, and many of them were already in challenging positions before COVID-19. Client needs and expectations are changing at an accelerated pace, competition is intensifying, and cost-to-income ratios have been significantly higher than prior to the previous financial crisis (77% in 2018 compared with 60% in 2007).

Although some wealth management providers have made advances in recent years in adapting their businesses to the changing environment, nearly all still have considerable work to do. CEOs must treat 2020 as a pivotal point. BCG’s recommended agenda for wealth management CEOs features three key imperatives:

- Protect the bottom line by pursuing smart revenue uplift, optimizing the front-office setup, streamlining compliance and risk-management processes, and improving structural efficiency.

- Win the future by developing more-personalized value propositions, enhancing ESG and impact-investment offerings, designing challenger plays, and leveraging ecosystems and M&A.

- Build capabilities by gaining better client understanding, attracting top talent, investing in digital and data, and designing a state-of-the-art technology platform.

“The last twenty years have witnessed many peaks and valleys,” said BCG’s Anna Zakrzewski, “and the next twenty will likely bring the same. Although some of the necessary initiatives may not be new, there is much more progress to be made. By acting decisively now, wealth managers have an opportunity to build on their current momentum and position themselves optimally for the future.”

In BCG’s opinion, the melding of technology and human capabilities will enable levels of customization for clients that previously would’ve been too costly, and the wealth management model will expand and refocus during the next two decades as the divide between people and machines fade. However, this will also put further pressure on margins.

“In addition, younger generations, accustomed to pricing transparency in other parts of their professional and personal lives, will insist on greater fee transparency from their wealth advisors,” the report said. “Online comparison tools will make it easy for them to search for the most competitive offerings. Together, these pressures could cut margins on investment services by half, with the result that wealth management providers will have to meet clients’ burgeoning demands and find new ways to drive value with just a fraction of today’s resources.”

To counter that, wealth management firms should shift to dynamic, value-based pricing not necessarily linked to assets under management.

Elsewhere, BCG said the need for scale, specialization and choice could cause the wealth management industry to remake itself around four models, Large-scale consolidation, Niche Plays, Retail Bank and Asset Manager Expansion, and Entrance of Big Tech.

A copy of the report can be downloaded here.