The outcome of the election in India, where 642 million people voted, has surprised analysts and the market. Narendra Modi, the favorite, has declared victory, but it was much closer than expected. According to the experts from investment firms, the fact that Modi’s party lost the simple majority raises some questions but does not undermine the country’s strong growth drivers.

“After exit polls pointed to a landslide victory for Modi, markets saw heavy selling on Wednesday morning as it appears Modi’s Bharatiya Janata Party (BJP) lacks a simple majority, erasing the 2.5% gains made the previous day following the exit poll results. The NDA (National Democratic Alliance) coalition can still form the new government with about 300 seats; however, Modi seems to have lost the majority, so while he can remain prime minister, coalition partners may oppose some of his initiatives, leading to the market reaction,” explains Liam Patel, Small-Cap Equity Investment Manager at abrdn.

Kenneth Akintewe, Head of Asian Sovereign Debt at abrdn, views this as a classic case of “buy the rumor, sell the fact.” He attributes part of the voter dissatisfaction with Modi to high food inflation, agricultural sector difficulties, and cuts in certain subsidies.

“India has experienced high growth levels, but not everyone has benefited, and consumption has not been as strong. The election result will serve as a wake-up call for the government and could act as an important catalyst for refocusing. However, these are not easy challenges to address. This underscores the urgency of developing a prosperous manufacturing sector to create more well-paid jobs and continue pushing reforms to strengthen the economy and generate the resources needed for economic transition, such as through privatizing public enterprises and monetizing assets,” notes Akintewe.

The Templeton Emerging Markets Equity team at Franklin Templeton describes the election outcome in India as clearly disappointing for investors compared to initial expectations. “Nonetheless, it is important to focus on the long term, and we do not foresee significant political changes in Modi’s likely third term. India’s growth drivers remain centered on manufacturing, infrastructure, and consumption.”

Impact of the Election Result

If the final result is achieved with a coalition majority, abrdn’s expert believes that while India is expected to continue progressing, there is a risk of more populist policies being implemented. “Fortunately, on the fiscal side, the starting point is a much stronger fiscal performance than expected and a structurally stronger fiscal position that provides significant buffers, reinforced by higher transfers from the Reserve Bank of India (RBI) to the government,” says Akintewe.

The Templeton Emerging Markets Equity team believes that while the election results may have potential negative consequences for certain market sectors, they do not believe it changes the overall policy direction of the BJP-led National Democratic Alliance (NDA). “In the manufacturing sector, the focus will remain on developing the manufacturing base through the Production-Linked Incentive (PLI) program. Additionally, infrastructure growth will shift from the public to the private sector, with particular attention to manufacturing, including renewables,” they explain. On consumption, they note that consumption stimulation will continue, with potentially renewed focus on rural incomes, including higher fiscal transfers. “This is likely to benefit the discretionary and staple consumer sectors, where our investments in India are concentrated,” they conclude.

India in Investment Portfolios

Regarding the main challenges ahead for the Indian market to become the top emerging country in investor portfolios, Avinash Vazirani, Investment Manager, Indian Equities, at Jupiter AM and Director of the Jupiter India Select Fund, indicates that it is simply a matter of time. “Investors tend to be slow to adapt to market paradigm shifts. Over the last two decades, China has had the highest weighting in global emerging market indexes; India has been gradually gaining a higher weighting as its economy and stock market grow faster, and we believe this process will continue in the coming decades,” he argues.

He points out that the best opportunities in this market are found in “companies exposed to India’s internal growth, especially in sectors such as healthcare, where we see possibilities for spending to grow faster than the economy in general, as current spending levels are low compared to other countries.”

“Investors should know that the most common benchmark for Indian funds (MSCI India) is concentrated in large and mega-cap stocks, which can trade at higher valuations than equally attractive companies lower down the market cap spectrum but still quite large by European standards,” he concludes.

A Solid Economy

Mark Matthews, Head of Research for Asia at Julius Baer, believes the changes introduced in India’s management over the last ten years have placed the economy in a solid position. Among these milestones are the demonetization of banks, the goods and services tax, the bankruptcy code, the real estate law, the corporate tax reduction, and the privatization of government-controlled companies.

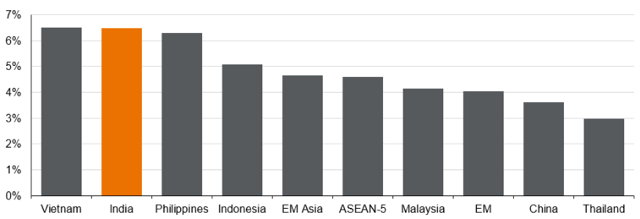

“Although the BJP’s power has been diluted, it remains intact. The momentum of current economic reforms remains strong and will not fade. GDP growth in the January-March quarter, at 7.8% year-on-year, confirms an economic cycle that we believe still has several years to run. This should translate into annual earnings growth of around ten percentage points over the next few years. Finally, on June 28, India will be included in JP Morgan’s emerging markets bond index, with inclusion in two more bond indexes expected to follow. The result is that tens of billions of dollars will flow into the Indian economy from abroad over the next two years,” comments Matthews.

Ashish Chugh, Portfolio Manager at Loomis Sayles (Natixis IM), believes the BJP’s growth- and investor-friendly agenda will continue. “India has many structural growth drivers that will continue regardless of the party in power. Additionally, significant investments in physical and digital infrastructure over the last decade will continue to boost productivity and economic growth. This election result does not change India’s path to becoming the world’s third-largest economy in the coming years,” argues Chugh.

In this regard, Vivek Bhutoria, Emerging Markets Equity Portfolio Manager at Federated Hermes Limited, highlights that the country’s economy is set to grow around 7% in the foreseeable future and, in nominal terms, possibly around 11%. “The drivers of this growth are very sustainable. If we look at other major economies, while they face the challenge of an aging population, India will add between seven and eight million people to its workforce each year, which is a significant competitive advantage. Urbanization is occurring, which will generate growth in various sectors of the economy,” Bhutoria points out.

He believes policies are being implemented to attract investments, and the global supply chain realignment will benefit India over time. “We are already starting to see some benefits in terms of exports of electronics and chemicals. Additionally, other factors, such as investment in infrastructure and digital investments, are converging at the same time,” concludes Bhutoria.\

JP Morgan AM indicates that the BJP’s plans for its third term include efforts to become the third-largest country by GDP, from its current fifth position, within the next five years. “We expect the government’s overall tone and general policy outlook to remain unchanged. Given the election results, the government is likely to move forward in less controversial areas. Continued focus on infrastructure spending, boosting manufacturing capacity as part of the Make in India program, and its integration as a more significant player in supply chains will continue. Areas where India can see rapid improvements, such as continued urbanization, formalization, and digitalization, should unlock more growth potential. Where India has a competitive edge, such as labor costs, IT services, and business support, more promotion is likely,” notes Ian Hui, Global Market Strategist at JP Morgan AM.

However, he clarifies that now the more divisive issues will likely require more political maneuvering to achieve, if at all possible.

“Constitutional changes are out of reach without a two-thirds majority in the Lok Sabha. Others will require more political capital: land and labor reforms, rationalizing food and fuel subsidies now seem more challenging to pass. The next government budget will be key to understanding the approach to developments,” Hui concludes.

By Funds Society

By Funds Society